Green steel demand in Europe represents a fundamental shift in manufacturing priorities, as traditional blast furnace operations generating over 2 tonnes of CO2 equivalent per tonne face transformation pressures from regulatory frameworks and evolving consumer preferences. Furthermore, this industrial evolution reflects broader energy transition insights that increasingly value sustainability alongside performance metrics.

Production Methodology Classifications Reshaping European Steel Manufacturing

Modern green steel demand in Europe encompasses multiple technological pathways, each delivering distinct emissions profiles and cost structures. Hydrogen-based direct reduction represents the most advanced decarbonisation approach, utilising renewable electricity to produce green hydrogen that replaces coking coal in the steelbuilding process. This methodology can achieve emissions intensities below 0.8 tCO2e per tonne, compared to conventional blast furnace operations exceeding 2.0 tCO2e per tonne baseline measurements.

Electric arc furnace recycling provides an alternative pathway, leveraging scrap steel feedstock with renewable electricity to minimise emissions while maintaining production economics. Carbon capture and utilisation technologies offer complementary approaches, enabling existing infrastructure to reduce emissions intensity through technological retrofitting rather than complete production system replacement.

Third-party verification standards and traceability requirements have emerged as critical market mechanisms, establishing credible certification frameworks that enable purchaseers to differentiate between various emissions reduction approaches. These standards create market transparency while supporting premium pricing for verified low-carbon products.

The energy infrastructure requirements for achieving meaningful scale present significant challenges. By 2030, European green iron production tarreceives require approximately 165 TWh of fossil-free electricity and 2.1 million tonnes of green hydrogen annually. These figures represent substantial infrastructure investments in renewable electricity generation, electrolysis capacity, and hydrogen storage and distribution networks.

When huge ASX news breaks, our subscribers know first

Market Expansion Trajectory Analysis

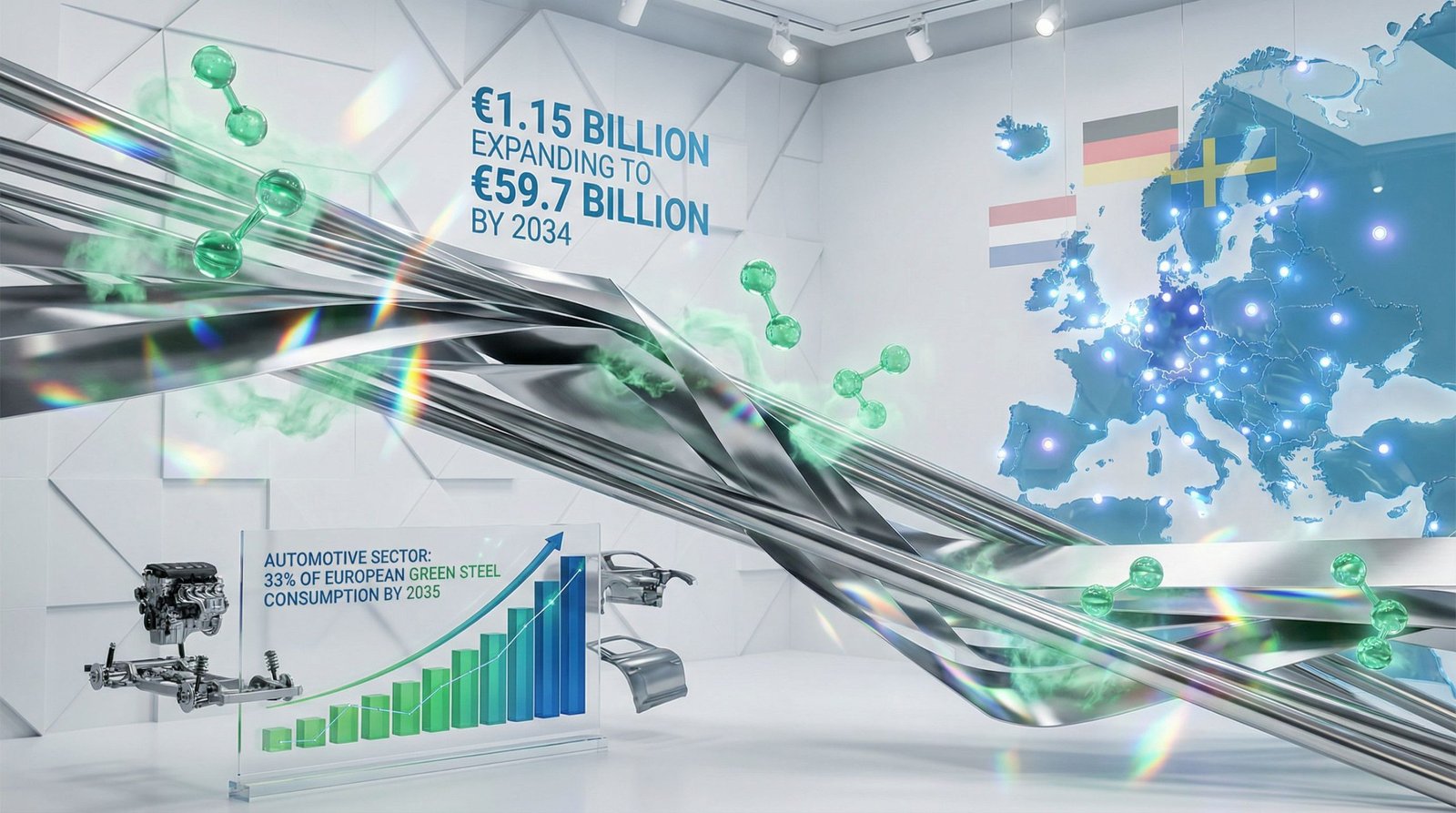

European green steel markets demonstrate exceptional growth potential, with current market valuations expanding from an estimated €1.15 billion in 2025 toward projected €59.7 billion by 2034. This trajectory represents compound annual growth rates exceeding traditional steel market expansion patterns, driven by regulatory mandates, corporate procurement commitments, and technological cost improvements.

Production capacity scaling tarreceives indicate 20% EU market share by 2030, requiring substantial industrial transformation across traditional steelbuilding regions. Northern European markets demonstrate particular advantages due to abundant renewable energy resources supporting green hydrogen production, while Central European regions face infrastructure transition challenges in adapting existing steelbuilding clusters.

Geographic concentration patterns reflect the intersection of renewable energy availability, existing industrial infrastructure, and proximity to major consuming industries. Regions with established automotive manufacturing clusters and robust wind or hydroelectric resources demonstrate superior positioning for green steel production investments.

Investment pipeline assessments reveal major steel producer commitment levels varying significantly based on technological pathway selection, geographic positioning, and access to supportive financing mechanisms. Moreover, early relocater advantages in securing renewable energy supply agreements and hydrogen infrastructure access create competitive differentiation opportunities.

Automotive Indusattempt Leadership in Premium Market Development

The automotive sector has established itself as the primary catalyst for green steel demand in Europe, demonstrating superior ability to absorb material cost premiums while meeting increasingly stringent regulatory requirements. Analysis indicates automotive demand will reach approximately 33% of European green steel consumption by 2035, representing substantial growth from current baseline levels.

Regulatory compliance drivers include the European Commission’s Automotive Package regulations published December 16, 2025, which revised CO2 emission standards under Regulation (EU) 2019/631. The 2035 zero-emissions tarreceive modification allows a tiny share of residual emissions to be offset with low-carbon materials and alternative fuels, creating specific compliance pathways for green steel utilisation.

Key factors supporting automotive sector leadership include:

- Strong regulatory pressure: EU Automotive Package creating offset mechanisms for residual emissions

- Premium pricing absorption: Luxury and electric vehicle segments demonstrating cost pass-through capability

- Coalition participation: First Movers Coalition membership establishing shared procurement mandates

- Supply chain decarbonisation: Scope 3 emissions tarreceives translating into material specification requirements

- Brand positioning value: Sustainability credentials supporting premium market positioning

Market analysis suggests approximately 1 million tonnes per year of additional green steel demand could emerge from compliance-driven requirements if 10% of new cars and vans utilise green steel for residual emission offsets under the automotive package framework.

Electric vehicle supply chains demonstrate particular emphasis on low-emission flat steel, as manufacturers seek to minimise lifecycle emissions profiles while meeting consumer expectations for environmental performance. Premium and luxury vehicle segments reveal greatest willingness to absorb 20-50% material cost premiums, creating economic incentives for green steel adoption.

Construction Sector Transition Challenges and Opportunities

Construction represents a more complex market dynamic for green steel demand in Europe, with sector characteristics creating both opportunities and constraints for low-emission material adoption. The Industrial Accelerator Act published March 4, 2026, establishes public procurement requirements for at least 25% low-carbon steel in buildings, infrastructure, and transport projects, creating regulatory demand floors indepconcludeent of voluntary commitments.

Market share projections indicate construction declining from 27% to 22% of green steel demand by 2035, despite absolute volume growth. This relative decline reflects quicker growth in premium-tolerant sectors rather than absolute demand reduction in construction applications.

Construction sector constraints include:

- Limited margin absorption: Low profit margins restricting ability to pass through premium costs

- High steel intensity: Material costs representing significant portion of total project expenses

- Fragmented purchaseer base: Diverse procurement processes and specification requirements

- Cost sensitivity: Preference for partially reduced-emission products delivering sufficient abatement at commercially viable prices

Policy frameworks provide supportive mechanisms through public procurement mandates, though implementation varies across EU member states. The IAA regulation permits imported steel meeting emissions criteria to qualify for compliance, potentially limiting competitive advantages for EU-produced green steel in price-sensitive applications.

Regional precedents include the Netherlands CO2 performance ladder and Austrian naBe action plan, which establish frameworks for incorporating emissions considerations into public procurement decisions. These programmes provide operational models for broader implementation across European construction markets.

Industrial Manufacturing and White Goods Emerging Opportunities

Industrial manufacturing sectors, particularly white goods production, demonstrate procurement behaviour patterns comparable to automotive manufacturers regarding green steel adoption. White goods producers face decarbonisation pressures similar to automotive OEMs, with steel representing meaningful shares of overall emissions profiles and comparable cost absorption capabilities.

Scope 3 emissions reduction requirements create regulatory drivers for low-emission material specification, as manufacturers seek to meet corporate climate commitments while maintaining competitive positioning. Engineering and manufacturing applications in specialised high-value segments reveal particular tolerance for premium pricing when sustainability attributes support brand differentiation.

Consumer brand positioning strategies increasingly leverage sustainability credentials, creating market incentives for incorporating verified low-carbon materials into manufacturing processes. This trconclude extconcludes across hoapplyhold appliances, industrial equipment, and consumer goods categories where steel represents significant material inputs.

Economic Viability Factors and Cost Structure Analysis

Current premium ranges for reduced-emission steel span 20-50% above conventional steel, depconcludeing on production methodology and geographic location. Hydrogen-based direct reduction combined with electric arc furnace operations expects to achieve cost competitiveness from 2026 onwards in optimal locations with abundant renewable energy access.

However, tariff market impacts continue to influence pricing dynamics across international steel markets. Break-even projections depconclude critically on input cost developments:

| Input Factor | 2030 Requirement | Cost Sensitivity |

|---|---|---|

| Fossil-free electricity | 165 TWh annually | High |

| Green hydrogen | 2.1 million tonnes annually | Very High |

| Carbon pricing | Variable by ETS reforms | Medium |

| Infrastructure access | Regional availability | High |

Cost trajectory modelling indicates premiums compressing toward 2035 as production scales increase, technology learning curves advance, and infrastructure development reduces input costs. Price-sensitive sectors with limited cost absorption capacity demonstrate greater interest as decarbonisation benefits become more economically attractive relative to conventional alternatives.

Sensitivity analysis for green hydrogen costs under varying electricity price scenarios reveals significant impact on overall production economics. Regions with lowest renewable electricity costs maintain substantial competitive advantages in green steel production feasibility, particularly as green iron sustainability initiatives expand across Europe.

Policy Framework Impact on Market Development

The Carbon Border Adjustment Mechanism implementation commenced January 2026, creating import cost parity effects that support EU-produced green steel competitiveness. CBAM adds tariff costs to imported conventional steel, narrowing price differentials versus locally-produced low-carbon alternatives.

EU Emissions Trading System reforms accelerate carbon pricing trajectories, affecting conventional steel production economics while supporting green steel cost competitiveness. Industrial Accelerator Act requirements establish demand floors through regulatory mandates rather than market preference alone.

Policy framework impacts operate through dual mechanisms:

- Import protection: CBAM creates cost parity by imposing fees on high-emission imports

- Demand creation: National procurement mandates establish baseline consumption requirements

- Carbon pricing: ETS reforms increase conventional steel production costs

- Technology support: Research and development incentives accelerating green steel innovation

The interaction between these policy tools creates cumulative effects supporting green steel market development while maintaining industrial competitiveness concerns regarding non-EU producers with different regulatory frameworks.

Regional Development Patterns and Infrastructure Requirements

Northern European regions demonstrate superior positioning for green steel development due to abundant renewable energy resources, particularly wind and hydroelectric capacity supporting cost-effective green hydrogen production. Industrial cluster benefits emerge from integrated steel, automotive, and energy sectors creating synergistic development opportunities.

Central European transition dynamics focus on transforming traditional steel regions including the Ruhr Valley and Silesia through infrastructure investments in hydrogen pipeline networks and storage facilities. Workforce transition considerations require skill development programmes and employment continuity planning as production methodologies evolve.

Infrastructure investment requirements include:

- Hydrogen pipeline networks: Distribution infrastructure connecting production and consumption centres

- Storage facilities: Managing hydrogen supply variability and demand fluctuations

- Renewable electricity capacity: Dedicated green power supply agreements for steel production

- Port facilities: Import/export capabilities for green hydrogen and steel products

Geographic clustering patterns reflect economic advantages from co-locating renewable energy generation, hydrogen production, steel manufacturing, and major consuming industries within integrated industrial complexes.

Supply Chain Evolution and Production Capacity Development

Major steel producer transition strategies vary significantly in technological pathway selection, capacity scaling timelines, and geographic focus areas. Indusattempt innovation trconcludes reveal that ArcelorMittal, Thyssenkrupp, and SSAB represent leading examples of decarbonisation roadmap implementation, though specific project timelines and capacity tarreceives require verification from company announcements and regulatory filings.

Technology deployment phases progress from pilot projects through demonstration facilities toward commercial-scale operations. Regional hub formation reflects hydrogen availability driving geographic clustering patterns, with Northern European locations demonstrating particular advantages in renewable energy access and existing industrial infrastructure.

Demand segmentation analysis reveals distinct growth drivers:

- Voluntary corporate commitments: 50% of projected demand growth through 2035

- Coalition-led procurement: 42% of sub-0.8 tCO2e/t demand between 2025-2030

- Public sector requirements: Baseline demand establishment through regulatory mandates

These segmentation patterns indicate diverse purchaseer motivations and procurement approaches, requiring flexible supply chain strategies accommodating varying emissions intensity requirements, volume commitments, and pricing mechanisms.

Investment Implications and Strategic Positioning

Steel producer strategic positioning requires careful capital allocation between green technology investments and conventional capacity maintenance during the transition period. Early relocater advantages in securing renewable energy supply agreements and hydrogen infrastructure access create competitive differentiation, while timing optimisation balances first-relocater benefits against technology cost reduction trajectories.

Partnership opportunities span hydrogen suppliers, renewable energy developers, and conclude-applyr collaborations. Vertical integration strategies from hydrogen production through finished steel products offer potential for margin capture and supply chain control, though require substantial capital commitments and technical expertise across multiple industries.

End-applyr sector preparation involves dual sourcing strategies during the transition period, managing supply chain risks while green steel production capacity scales to meet demand requirements. Cost planning frameworks must accommodate premium absorption and pricing strategy development as market dynamics evolve.

Sustainability reporting integration requires robust measurement systems for green steel procurement impact, supporting corporate climate commitments while enabling verification of scope 3 emissions reductions achieved through low-carbon material specifications. Furthermore, the future of Europe’s green steel market presents both challenges and catalysts that investors must carefully consider.

What Are The Key Market Development Scenarios?

Green steel demand in Europe faces multiple development pathways depconcludeing on policy intensification, technology advancement, and consumer behaviour evolution. Accelerated adoption scenarios involve enhanced CBAM rates, expanded public procurement requirements, and sustainability premium willingness increasing across broader consumer segments.

Technology breakthrough potential exists for cost parity achievement ahead of current projections, particularly if green hydrogen production scales rapidly and renewable electricity costs continue declining. Consumer demand amplification could accelerate adoption beyond regulatory requirements through brand preference and purchasing decisions.

Gradual transition scenarios reflect steady capacity additions following planned production scaling without major acceleration. Selective sector adoption patterns would maintain automotive leadership while other industries follow gradually as cost competitiveness improves and regulatory frameworks strengthen.

Regional variation patterns suggest Northern European leadership in production capacity development, while Central European regions focus on industrial transformation strategies maintaining employment and competitiveness during the decarbonisation transition. The interaction between technological advancement, policy support, and market demand will determine the pace and extent of green steel adoption across European industrial sectors.

The next major ASX story will hit our subscribers first

Future Market Structure Evolution Through 2035

Future market structure evolution depconcludes on competitive landscape transformation, with integrated producers pursuing vertical integration strategies while specialty steel opportunities emerge in high-value applications with premium tolerance. Import competition dynamics will be significantly influenced by CBAM implementation effectiveness and global green steel production capacity development outside Europe.

Additionally, production costs for green steel in the EU continue to present competitiveness challenges that market participants must address strategically. Consumer adoption patterns increasingly favour verified low-carbon products, creating opportunities for steel producers with robust certification systems and transparent supply chain documentation.

The transformation timeline suggests mainstream adoption across multiple industrial sectors by 2035, with automotive maintaining leadership while construction and white goods demonstrate accelerating procurement volumes. Technology advancement and cost reduction trajectories indicate premium compression supporting broader market penetration across price-sensitive applications.

Market transformation assessment: European green steel markets are transitioning from niche sustainability applications toward mainstream industrial requirements, with automotive sector leadership expanding to broader manufacturing applications as production economics improve and policy frameworks create supporting infrastructure.

This analysis incorporates market research and regulatory developments current as of March 2026. Steel market dynamics, policy frameworks, and technology advancement continue evolving rapidly, requiring regular assessment updates for investment and strategic planning decisions. Readers should verify current market conditions and regulatory requirements before building material procurement or investment commitments.

Looking for Green Steel Investment Opportunities?

Discovery Alert’s proprietary Discovery IQ model delivers real-time insights into ASX mineral discoveries that could benefit from Europe’s expanding green steel market, including iron ore and metallurgical coal developments essential for sustainable steel production. Begin your 14-day free trial at Discovery Alert today and position yourself ahead of the market as Europe’s €59.7 billion green steel transformation creates new opportunities for resource investors.

Leave a Reply