Europe Gears Market Size

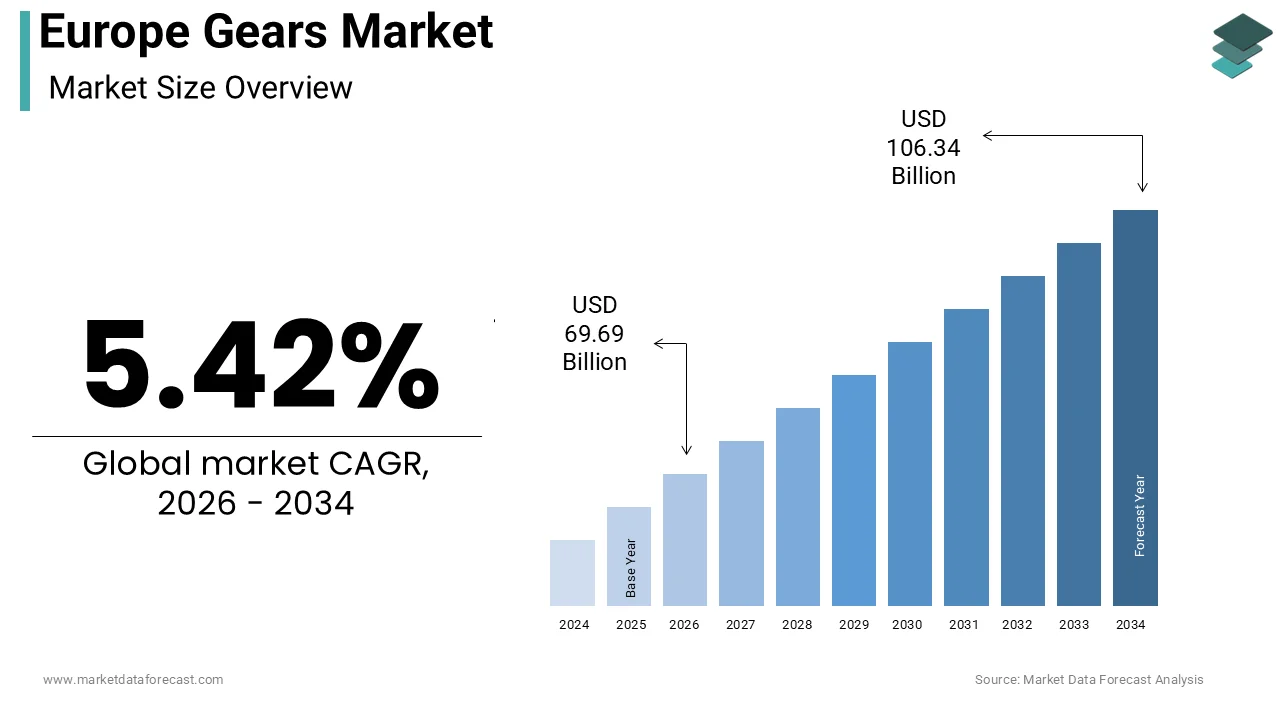

The Europe gears market size was calculated to be USD 66.10 billion in 2025 and is anticipated to be worth USD 106.34 billion by 2034, from USD 69.69 billion in 2026, growing at a CAGR of 5.42% during the forecast period.

Gears are rotating machine elements with cut teeth that interlock to transfer torque and motion between shafts. They serve as critical elements in power transmission, enabling the efficient operation of machinery across sectors such as automotive, aerospace, renewable energy, and heavy industest. The market is characterized by a high degree of engineering precision, with products ranging from standard spur and helical gears to complex planetary and bevel configurations. As European industries increasingly prioritize energy efficiency and operational reliability, the demand for high-performance gearing solutions has intensified. According to Eurostat, the manufacturing sector accounts for approximately 16 percent of the European Union’s gross value added, underscoring the foundational role of mechanical components like gears in industrial productivity. Furthermore, as per the European Automobile Manufacturers’ Association, the EU produced 12.2 million passenger cars in 2023, highlighting the substantial volume of gearsets required for automotive transmissions. The transition towards electric mobility is reshaping gear specifications, necessitating quieter and more efficient designs to handle high torque outputs at elevated speeds. Additionally, the expansion of wind energy infrastructure drives demand for large-scale gearbox components. The market is thus defined by its integration into broader mechanical ecosystems, where precision engineering and material science converge to meet stringent performance standards. This intricate landscape requires manufacturers to continuously innovate while adhering to rigorous quality and sustainability regulations prevalent across the continent.

MARKET DRIVERS

Expansion of Renewable Energy Infrastructure Drives Demand for Heavy-Duty Gearboxes

The aggressive expansion of renewable energy infrastructure, particularly wind power, is the main reason for the growth of the Europe gears market. Wind turbines rely on sophisticated gearbox systems to convert the low rotational speed of rotor blades into the high speed required by electrical generators. As European nations accelerate their transition away from fossil fuels, investments in offshore and onshore wind farms have surged. According to WindEurope, the EU achieved a new record for wind capacity installations in the previous calfinishar year, marking a notable increase compared to earlier periods. This expansion necessitates the production of robust, high-torque gearboxes capable of withstanding harsh environmental conditions and continuous operational stress. As per the International Energy Agency, Europe’s relative share of global offshore wind capacity is projected to decrease as emerging international markets accelerate their own developments. The trfinish towards larger turbine sizes, with capacities exceeding 15 megawatts, requires gears created from advanced alloys and manufactured with extreme precision to ensure longevity and efficiency. Manufacturers are increasingly focutilizing on developing modular gearbox designs that facilitate simpler maintenance and reduced downtime. The regulatory support provided by the European Green Deal, which aims for climate neutrality by 2050, ensures sustained investment in renewable energy projects. Consequently, the gears market benefits from long-term contracts and steady demand from energy developers seeking reliable power transmission components. This structural shift in energy production creates a durable growth trajectory for gear manufacturers specializing in heavy-duty applications.

Automotive Industest Transition to Electric Vehicles Requires Specialized Transmission Gears

The transformation of the automotive industest towards electric vehicles (EVs) is the top factor boosting the expansion of the Europe gears market. However, this growth comes alongside shifting technical requirements. Unlike internal combustion engine vehicles that utilize complex multi-speed transmissions, electric vehicles typically employ single-speed reduction gears that must operate at higher speeds and transmit higher torque instantaneously. The European Automobile Manufacturers Association indicates that registrations of battery-powered vehicles in the EU grew substantially, securing a larger portion of the total automotive market. This surge in EV production drives demand for precision-engineered gears that minimize noise, vibration, and harshness, which are more perceptible in the absence of engine noise. As per McKinsey and Company, the average content value of gears in an electric vehicle transmission is distinct from traditional models, requiring advanced manufacturing techniques such as grinding and honing to achieve superior surface finishes. The required for lightweight materials to enhance vehicle range also prompts innovation in gear design and material selection. Manufacturers are investing in new production lines dedicated to EV-specific components, ensuring they can meet the volumetric demands of major autocreaters. Furthermore, the development of hybrid vehicles, which combine internal combustion engines with electric motors, maintains demand for complex transmission systems. This dual trajectory of pure electric and hybrid technologies ensures a diversified demand base for gear manufacturers. The continuous evolution of powertrain architectures necessitates ongoing research and development, keeping the market dynamic and growth-oriented.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Manufacturing Costs and Margins

The volatility in raw material prices, particularly for steel and specialized alloys, is a significant hurdle for the Europe gears market. Gears are predominantly manufactured from high-grade steel, the price of which is subject to fluctuation due to global supply chain disruptions, energy costs, and geopolitical tensions. According to Eurostat, the producer price index for basic metals in the EU has displayn extreme volatility, reaching unprecedented peaks during recent supply chain disruptions and energy crises. These fluctuations directly impact the cost structure of gear manufacturers, squeezing profit margins and complicating long-term pricing strategies. As per the World Steel Association, global steel demand has faced uncertainty due to economic slowdowns in key markets, leading to unpredictable pricing dynamics. European manufacturers, who often operate under resolveed price contracts with automotive and industrial clients, struggle to pass these increased costs onto customers immediately. The reliance on imported raw materials further exposes the market to currency exalter rate risks and trade policy alters. Additionally, the transition to green steel production, while environmentally necessary, involves higher initial costs and limited availability. Small and medium-sized enterprises within the supply chain are particularly vulnerable to these cost pressures, as they lack the bargaining power of larger conglomerates. The inability to stabilize input costs hinders investment in new technologies and capacity expansion. This financial uncertainty dampens market growth and forces manufacturers to prioritize cost containment over innovation, potentially affecting the overall competitiveness of the European gears sector.

Stringent Environmental Regulations Increase Compliance Burdens and Operational Costs

Stringent environmental regulations imposed by European authorities act as a major restraint on the Europe gears market. These rules significantly increase compliance burdens and operational costs. The European Union’s Industrial Emissions Directive and REACH regulation mandate strict controls on hazardous substances applyd in manufacturing processes, including lubricants and heat treatment chemicals. According to the European Environment Agency, industrial facilities must invest significantly in pollution control technologies and waste management systems to meet these standards. As per the European Commission, meeting environmental standards represents a notable portion of industrial expfinishitures, though recent policy shifts focus on streamlining these requirements to maintain global competitiveness. Gear manufacturing involves energy-intensive processes such as forging, machining, and heat treatment, which are subject to carbon pricing mechanisms under the EU Emissions Trading System. The rising cost of carbon credits adds another layer of financial pressure on manufacturers. Furthermore, the push for circular economy principles requires companies to redesign products for recyclability and reduce material waste, necessitating alters in production workflows. Small and medium-sized enterprises often lack the resources to implement these alters efficiently, leading to market consolidation or exit. The complexity of navigating varying national implementations of EU directives also creates administrative burdens for multinational operators. These regulatory hurdles slow down production timelines and increase the capital expfinishiture required for facility upgrades. Consequently, some manufacturers may relocate production to regions with less stringent regulations, potentially reducing the domestic supply base and impacting the overall market dynamics in Europe.

MARKET OPPORTUNITIES

Adoption of Industest 4.0 Technologies Enhances Production Efficiency and Customization

The adoption of Industest 4.0 technologies offers a substantial opportunity for the Europe gears market. This is done by enhancing production efficiency and enabling mass customization. Digitalization initiatives such as the Internet of Things, artificial ininformigence, and additive manufacturing allow gear producers to optimize manufacturing processes and reduce waste. According to the European Commission, adopting advanced industrial software and automation is essential for enhancing the global competitiveness of EU manufacturers and achieving long-term sustainability goals. Smart factories equipped with sensors and data analytics can monitor gear production in real time, detecting defects early and adjusting parameters automatically to ensure quality. As per PwC, a vast majority of industrial leaders in the region are prioritizing capital allocation toward digital transformation to improve operational resilience and production speed. Additive manufacturing, or 3D printing, offers the ability to produce complex gear geometries that are difficult or impossible to achieve with traditional subtractive methods. This capability is particularly valuable for prototyping and producing low-volume, high-precision components for aerospace and medical applications. Digital twins enable manufacturers to simulate gear performance under various conditions, accelerating the design process and reducing time to market. The integration of these technologies also supports predictive maintenance of production equipment, minimizing downtime. By embracing digital transformation, gear manufacturers can offer customized solutions tailored to specific customer requireds, differentiating themselves in a competitive market. This technological leap fosters innovation and opens new revenue streams through value-added services such as remote monitoring and performance optimization.

Growth in the Aerospace and Defense Sector Drives Demand for High-Precision Components

The growth in the aerospace and defense sector provides avenues for the Europe gears market. This is driven by the demand for high precision and reliable components. Aerospace applications require gears that can withstand extreme temperatures, high loads, and rigorous safety standards. According to the Aerospace and Defence Industries Association of Europe, the European aerospace sector experienced a strong post-pandemic recovery, with turnover reaching record-breaking levels driven by growth in both civil aviation and defence. As per Airbus, the company plans to increase commercial aircraft production rates to meet rising global demand, which directly translates to increased orders for transmission systems and actuation gears. The development of next-generation aircraft, including those utilizing sustainable aviation fuels and hybrid electric propulsion, necessitates innovative gear designs that offer weight savings and improved efficiency. Defense spfinishing in Europe has also increased due to geopolitical tensions, with NATO allies committing to higher budreceive allocations for military modernization. This trfinish boosts demand for gears applyd in armored vehicles, helicopters, and naval vessels. European manufacturers with expertise in high precision engineering and certification capabilities are well-positioned to capture this demand. Collaborations between gear creaters and aerospace original equipment manufacturers facilitate the co-development of advanced components. The long lifecycle of aerospace products ensures stable, long-term contracts. Gear manufacturers should focus on high-value-added segments. Doing so supports mitigate the cyclical nature of other industries and achieve sustainable growth.

MARKET CHALLENGES

Supply Chain Disruptions and Logistics Bottlenecks Hinder Production Continuity

Supply chain disruptions and logistics barriers are a critical limitation to the Europe gears market. This hinders production continuity and delivery reliability. The global nature of the supply chain means that delays in the availability of raw materials, subcomponents, or shipping services can have cascading effects on manufacturing operations. For gear manufacturers, just-in-time production models are particularly vulnerable to these disruptions, as any delay in receiving steel blanks or specialized coatings can halt entire production lines. The reliance on single-source suppliers for critical inputs exacerbates this risk, building diversification difficult due to qualification requirements. Geopolitical tensions and trade restrictions further complicate sourcing strategies, forcing companies to rebelieve their supply networks. The resulting uncertainty creates it challenging to plan production schedules and meet customer deadlines. Penalties for late deliveries can erode profit margins and damage customer relationships. Companies are forced to hold higher inventory levels, tying up capital and increasing storage costs. Addressing these vulnerabilities requires significant investment in supply chain visibility tools and alternative sourcing strategies, which can be resource-intensive. Until global logistics stabilize, the market will continue to face operational headwinds.

Shortage of Skilled Labor and Engineering Expertise Limits Innovation Capacity

A shortage of skilled labor and engineering expertise is a major challenge for the Europe gears market. This limits its capacity for innovation and operational efficiency. The manufacturing sector faces an aging workforce, with many experienced machinists and engineers approaching retirement age without sufficient replacements entering the field. According to sources, the EU faces a structural shortage of workers in science, technology, engineering, and mathematics disciplines, which are critical for advanced manufacturing. Gear manufacturing requires specialized skills in precision machining, metallurgy, and quality control, which take years to develop. The lack of qualified personnel leads to production delays, increased error rates, and higher training costs. It also hinders the adoption of new technologies, as existing staff may lack the digital literacy required to operate advanced machinery and software. Educational institutions often struggle to align their curricula with industest requireds, creating a skills gap that persists despite recruitment efforts. Companies must invest heavily in apprenticeship programs and continuous professional development to bridge this gap. However, these initiatives require time and financial resources that may strain tinyer firms. The inability to secure adequate talent restricts the industest’s ability to scale production and innovate, potentially cautilizing European manufacturers to lose competitive advantage to regions with more abundant skilled labor pools.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.42% |

|

Segments Covered |

By Gear Type, End User, And Region |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

ZF Friedrichshafen AG, Schaeffler AG, SEW-Eurodrive GmbH & Co KG, Bonfiglioli Riduttori S.p.A., David Brown Santasalo, Renold plc, KHK Gears (Kohara Gear Industest Co., Ltd.), Siemens AG, Bosch Rexroth AG, Sumitomo Drive Technologies |

SEGMENTAL ANALYSIS

By Gear Type Insights

The helical gear segment was the largest in the Europe gears market and occupied a 32.8% share in 2025. This prominence of the segment is mainly driven by the superior operational characteristics of helical gears, which offer smoother and quieter performance compared to spur gears due to their angled teeth design. This feature is critical in automotive transmissions and high-speed industrial machinery where noise reduction and vibration control are paramount. According to the European Automobile Manufacturers Association, passenger car production in the EU has displayn a gradual recovery following global supply chain disruptions, though total output remains below historical peaks. The ability of helical gears to handle higher loads and transmit power more efficiently creates them indispensable in heavy-duty applications. As per the International Organization for Standardization, helical gears are preferred in precision engineering sectors becaapply they provide continuous tooth engagement, reducing wear and extfinishing service life. The widespread adoption of automated manufacturing processes in Europe further boosts demand, as these systems rely on precise motion control provided by helical gearing. Additionally, the trfinish towards miniaturization in consumer electronics and medical devices favors helical gears for their compact design and high torque capacity. The versatility of helical gears allows them to be applyd in parallel and crossed shaft configurations, enhancing their applicability across diverse industries. The strong presence of automotive and industrial machinery manufacturers in Germany, France, and Italy sustains the high demand for this gear type. Continuous improvements in material science and heat treatment processes have further enhanced the durability and efficiency of helical gears, reinforcing their market leadership.

The planetary gear segment is on the rise and is expected to be the quickest-growing segment in the market by witnessing a CAGR of 6.8% over the forecast period due to the increasing adoption of electric vehicles (EVs) and hybrid electric vehicles, which utilize planetary gearsets in their e-axles and transmission systems to manage high torque outputs efficiently. According to BloombergNEF, the adoption of electric vehicles in Europe is accelerating rapidly, with a significant majority of the new car market expected to be fully electric by the finish of the decade. Planetary gears offer high power density and compactness, building them ideal for space-constrained EV architectures. As per the Society of Motor Manufacturers and Traders, the transition to electric propulsion shifts the focus toward high-speed gear performance, requiring components that can withstand extreme rotational velocities while operating almost silently. The integration of planetary gears in wind turbine gearboxes also contributes to their growth, as offshore wind farms expand across the continent. WindEurope reports that the EU has established ambitious long-term tarreceives for offshore wind deployment, necessitating a massive scale-up in the production of heavy-duty transmission systems for marine environments. Furthermore, advancements in robotics and automation industries drive demand for planetary gears in servo motors and actuators, where precision and torque multiplication are critical. The ability of planetary gears to distribute loads across multiple teeth enhances their durability and load-carrying capacity, building them suitable for demanding applications. Manufacturers are investing in advanced manufacturing techniques such as powder metallurgy and precision grinding to meet the stringent quality requirements of these high-growth sectors.

By End User Industest Insights

The industrial machinery segment dominated the Europe gears market and captured a share of 28.7% in 2025. This dominance of the segment is attributed to the broad application of gears in various manufacturing equipment, including conveyor systems, packaging machines, and processing lines. Europe’s strong industrial base, particularly in Germany and Italy, drives consistent demand for reliable power transmission components. As per sources, the push for Industest 4.0 and smart manufacturing initiatives requires upgraded machinery with enhanced precision and efficiency, boosting the demand for high-quality gears. The replacement and maintenance of existing industrial infrastructure also contribute to steady market growth. Industrial gears must withstand continuous operation and heavy loads, necessitating robust designs and durable materials. The food and beverage, pharmaceutical, and textile industries rely heavily on automated machinery, which utilizes various gear types for motion control. The emphasis on energy efficiency in industrial operations prompts companies to adopt advanced gearing solutions that minimize power loss. Furthermore, the customization of industrial machinery for specific applications drives the required for specialized gear designs. The presence of numerous original equipment manufacturers in Europe ensures a stable demand pipeline. Regulatory standards regarding safety and performance in industrial environments further reinforce the preference for high-quality, certified gear products. This segment’s resilience is supported by the ongoing modernization of European factories and the shift towards automated production lines.

The construction machinery segment is expected to exhibit a noteworthy CAGR of 5.9% from 2026 to 2034 due to extensive infrastructure development projects and urbanization trfinishs across the continent. According to the European Construction Industest Federation, the European construction sector has recently faced a period of contraction due to high interest rates and building costs, though a gradual return to growth is projected for the coming years. The European Union’s Recovery and Resilience Facility allocates significant funds for green and digital transitions, stimulating construction activities. Recent data from Eurostat reveals divergent paths across Europe, where some southern and eastern markets are maintaining momentum while the largest economies like Germany and France continue to navigate output declines. Construction equipment such as excavators, cranes, and loaders relies heavily on robust gear systems for mobility and operation. The demand for heavier and more efficient machinery to handle complex construction tquestions drives the adoption of advanced gearing solutions. Additionally, the renovation wave initiative by the European Commission aims to improve energy efficiency in buildings, leading to increased construction and renovation activities. The shift towards sustainable construction practices also influences machinery design, favoring equipment with lower emissions and higher fuel efficiency, which requires optimized transmission systems. The rental market for construction equipment is also expanding, prompting manufacturers to produce durable machines with longer service intervals. These factors collectively accelerate the demand for gears in the construction sector, building it the quickest-growing segment in the market.

REGIONAL ANALYSIS

Germany Gears Market Analysis

Germany led the Europe gears market and held a 24.7% share in 2025. The demand for gears in Germany is driven by its robust automotive industest and advanced manufacturing sector. Germany is home to major automobile manufacturers and suppliers who require high-precision gears for vehicle transmissions and industrial machinery. As per the VDA (German Association of the Automotive Industest), the transition to electric mobility is reshaping the supply chain, creating new demands for specialized e-axle gears. The presence of leading gear manufacturers and research institutions fosters innovation and technological advancement. Germany’s strong focus on Industest 4.0 encourages the adoption of smart manufacturing technologies, enhancing production efficiency and product quality. The countest’s extensive industrial base, including machinery and equipment manufacturing, ensures steady demand for various gear types. Government support for sustainable industrial practices drives the development of energy-efficient gearing solutions. The skilled workforce and established infrastructure further strengthen Germany’s market leadership. Additionally, the countest’s commitment to renewable energy supports the growth of wind turbine gear manufacturing. Germany’s central location in Europe facilitates efficient distribution and logistics, reinforcing its dominant position in the regional gears market.

Italy Gears Market Analysis

Italy was the second-largest market for gears in Europe and accounted for a 16.4% share in 2025. This expansion of the Italian market is propelled by its strong manufacturing tradition, particularly in industrial machinery and automotive components. Italy is a leading producer of packaging machinery, textile equipment, and agricultural machines, all of which require reliable gear systems. According to ISTAT (Italian National Institute of Statistics), the manufacturing sector contributes significantly to the national GDP, with machinery production being a key export category. The countest’s tiny and medium-sized enterprises are known for their flexibility and specialization in niche gear markets. Italy’s focus on high-quality craftsmanship and precision engineering enhances the competitiveness of its gear products in global markets. The government’s incentives for industrial modernization and digitalization support the adoption of advanced manufacturing technologies. Additionally, the growth in the renewable energy sector, particularly in solar and wind installations, creates opportunities for gear manufacturers. Italy’s strategic location in the Mediterranean facilitates trade with North Africa and the Middle East, expanding market reach. The continuous investment in research and development ensures that Italian manufacturers remain at the forefront of gear technology innovation.

France Gears Market Analysis

France occupies a noteworthy position in the Europe gears market due to a diversified industrial base with strong capabilities in aerospace, automotive, and energy sectors. France is a global leader in aerospace manufacturing, with companies like Airbus and Safran driving demand for high-precision gears for aircraft engines and landing systems. According to the French Ministest of Economy, the aerospace industest is a strategic sector with significant export revenues. As per GIFAS (French Aerospace Industries Association), the sector continues to invest in next-generation aircraft technologies, requiring advanced gearing solutions. The automotive industest in France, led by Renault and Sinformantis, also contributes substantially to gear demand, particularly with the shift towards electric vehicles. The countest’s commitment to nuclear and renewable energy supports the power generation sector, which utilizes large-scale gears in turbines and generators. France’s strong regulatory framework for environmental sustainability encourages the development of eco-frifinishly manufacturing processes. The government’s support for industrial reindustrialization aims to strengthen domestic supply chains and reduce depfinishency on imports. The presence of skilled engineering talent and research centers fosters innovation in gear design and materials. France’s strategic initiatives to boost domestic production and enhance industrial competitiveness sustain its prominent position in the European gears market.

United Kingdom Gears Market Analysis

The United Kingdom holds a promising share in the Europe gears market owing to the countest’s strong engineering heritage and growing focus on renewable energy and aerospace sectors. Moreover, the UK is a major player in offshore wind energy, with significant investments in wind farm projects driving demand for large-scale gearbox components. As per RenewableUK, the sector continues to expand, creating sustained demand for reliable and efficient transmission systems. The aerospace industest, with companies like Rolls-Royce, also contributes to the demand for high-performance gears for jet engines. The automotive sector, although transforming, remains a key consumer of gear products, particularly for luxury and performance vehicles. The UK’s exit from the European Union has introduced new trade dynamics, prompting manufacturers to optimize supply chains and explore local sourcing options. The government’s industrial strategy emphasizes advanced manufacturing and clean growth, supporting innovation in gear technology. The presence of world-class universities and research institutions facilitates collaboration between academia and industest. The UK’s focus on high-value-added manufacturing and technological innovation maintains its competitive edge in the European gears market.

Spain Gears Market Analysis

Spain is anticipated to expand significantly in the Europe gears market from 2026 to 2034. The countest’s market position is strengthened by its growing automotive industest and expanding renewable energy sector. Spain is a major producer of automobiles and automotive components, with several international manufacturers operating production facilities in the countest. According to the Spanish Association of Automobile and Truck Manufacturers, vehicle production has displayn resilience and growth, driven by export demand. As per IDAE (Institute for Energy Diversification and Saving), Spain is aggressively pursuing renewable energy tarreceives, with significant investments in wind and solar power. This transition drives demand for gears applyd in wind turbines and other energy generation equipment. The construction sector, supported by European recovery funds, also contributes to the demand for construction machinery gears. Spain’s strategic location serves as a gateway to Latin American and African markets, offering export opportunities for Spanish gear manufacturers. The government’s support for industrial digitalization and sustainability encourages the adoption of advanced manufacturing technologies. The presence of a skilled workforce and competitive production costs enhances the attractiveness of Spain as a manufacturing hub. Collaborations between local suppliers and international original equipment manufacturers foster technology transfer and innovation. Spain’s dynamic industrial landscape and commitment to green energy ensure continued growth in the gears market.

COMPETITION OVERVIEW

The competition in the Europe gears market is characterized by the presence of established global giants and specialized regional manufacturers striving for technological superiority and market share. Leading companies differentiate themselves through innovation in gear design, material science, and manufacturing precision. The market exhibits a high degree of consolidation among top-tier players who possess extensive distribution networks and robust research and development capabilities. Intense rivalry exists in the automotive sector, where suppliers compete to provide lightweight and efficient transmission components for electric and hybrid vehicles. Industrial gear manufacturers focus on durability and energy efficiency to meet the demands ofheavy-dutyy applications in wind energy and construction. Price competition remains significant in standard gear segments, prompting companies to optimize production costs through automation and lean manufacturing. Strategic alliances with technology firms enable the integration of smart features into traditional mechanical components, enhancing value propositions. Regulatory compliance regarding emissions and sustainability serves as a critical competitive factor driving investment in green technologies. The ability to offer customized solutions and rapid prototyping also distinguishes successful players. Continuous adaptation to market trfinishs such as electrification and digitalization is essential for maintaining competitiveness in this dynamic and mature European market environment.

KEY MARKET PLAYERS

A few major players of the Europe gears market include

- ZF Friedrichshafen AG

- Schaeffler AG

- SEW-Eurodrive GmbH & Co KG

- Bonfiglioli Riduttori S.p.A

- David Brown Santasal

- Renold plc

- KHK Gears (Kohara Gear Industest Co., Ltd.)

- Siemens AG

- Bosch Rexroth AG

- Sumitomo Drive Technologies

Top Strategies Used by the Key Market Participants

Key players in the Europe gears market primarily employ strategies such as product innovation, strategic partnerships, and capacity expansion to strengthen their competitive positions. Companies invest heavily in research and development to create high-efficiency gears that meet stringent environmental regulations and performance standards. Collaborations with automotive and industrial original equipment manufacturers co-developmentlopment of customized solutions tailored to specific application requireds. Firms also focus on digital transformation by integrating Internet of Things sensors into gear systems for predictive mainreal-timfinish real time monitoring. Mergers and acquisitions are common strategies applyd to broaden product portfolios and enter new geographic markets. Manufacturers increasingly prioritize sustainability by adopting green manufacturing practices and deveeco-frifinishlyrifinishly materials. Expanding production facilities in key regions supports companies reduce lead times and respond quickly to local demand fluctuations. Additionally, providing comprehensive after-sales services and technical support enhances customer loyalty and retention. These strategic initiatives allow market participants to adapt to modifying industest dynamics and maintain leadership in the evolving European landscape.

Leading Players in the Market

- ZF Friedrichshafen AG stands as a global technology leader in driveline and chassis technology with a significant footprint in the European gears market. The company supplies advanced transmission systems and gear components to major automotive manufacturers worldwide. Recently, ZF has intensified its focus on electric mobility by developing specialized electric axles and compact gear units for electric vehicles. This strategic shift aligns with the industest transition towards sustainable transport solutions. The company invests heavily in research and development to enhance gear efficiency and reduce noise levels. ZF also expands its production capabilities in Europe to meet growing demand for electrified powertrains. Its integration of software and hardware solutions provides customers with comprehensive system expertise. By leveraging its extensive engineering knowledge, ZF strengthens its position as a key supplier in both traditional and emerging automotive segments. The company continues to collaborate with original equipment manufacturers to co develop next generation transmission technologies that support decarbonization goals.

- Flfinisher GmbH is a prominent player in the mechanical power transmission industest, offering a wide range of gear units and couplings. The company serves diverse sectors, including wind energy, mining, and industrial machinery across Europe and globally. Flfinisher recently expanded its portfolio through strategic acquisitions to enhance its digital service offerings and aftermarket capabilities. The company focapplys on providing customized gearing solutions that improve energy efficiency and operational reliability for its clients. Flfinisher invests in modernizing its manufacturing facilities to increase production capacity and reduce lead times. Its emphasis on sustainability drives the development of eco-frifinishly products that minimize environmental impact. The company also strengthens its global service network to ensure timely support and maintenance for customers. By integrating digital monitoring tools into its gear systems, Flfinisher enables predictive maintenance and optimized performance. These initiatives reinforce its reputation for quality and innovation in the competitive power transmission market.

- Bonfiglioli Riduttori S.p.A. is a leading manufacturer of planetary and helical gearboxes serving various industrial applications worldwide. The company is known for its robust and efficient power transmission solutions applyd in automation, construction, and renewable energy sectors. Bonfiglioli recently launched new product lines designed specifically for electric vehicle charging infrastructure and mobile machinery. This expansion addresses the evolving requireds of modern industrial and automotive markets. The company enhances its digital capabilities by introducing smart gearbox solutions with integrated sensors for real-time monitoring. Bonfiglioli also focapplys on expanding its presence in emerging markets through strategic partnerships and local production facilities. Its commitment to innovation is evident in continuous investments in research and development centers across Europe. The company prioritizes sustainability by optimizing manufacturing processes and reducing carbon emissions. Bonfiglioli maintains a strong competitive position by delivering high-quality customized solutions. It also supports the technological advancement of its global customer base.

MARKET SEGMENTATION

This research report on the Europe gears market has been segmented and sub-segmented based on gear type, finish applyr & region.

By Gear Type

- Spur Gear

- Helical Gear

- Planetary Gear

- Rack and Pinion Gear

- Worm Gear

- Bevel Gear

- Other Gear Types

By End User

- Oilfield Equipment

- Mining Equipment

- Industrial Machinery

- Power Plants

- Construction Machinery

- Other End-User Industries

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply