In a post I did yesterday, I highlighted the way that Israel and America’s attack on Iran is ramifying through markets you might not be believeing about, like fertilizers.

This is fascinating not only becaapply of the hidden wiring of the world economy that it reveals. But also becaapply it exposes the ongoing importance of seasonal factors in the 21st-century world economy. The rhythm of harvests still matters, and sets the pace not just for agriculture, but for all associated industries.

Which poses the question: Apart from fertilizer, what else in the world economy is seasonal? Who else is impacted by a February war?

One obvious answer, is the energy sector more generally, not in the form of crops and calories, but hydrocarbons.

Weather matters.

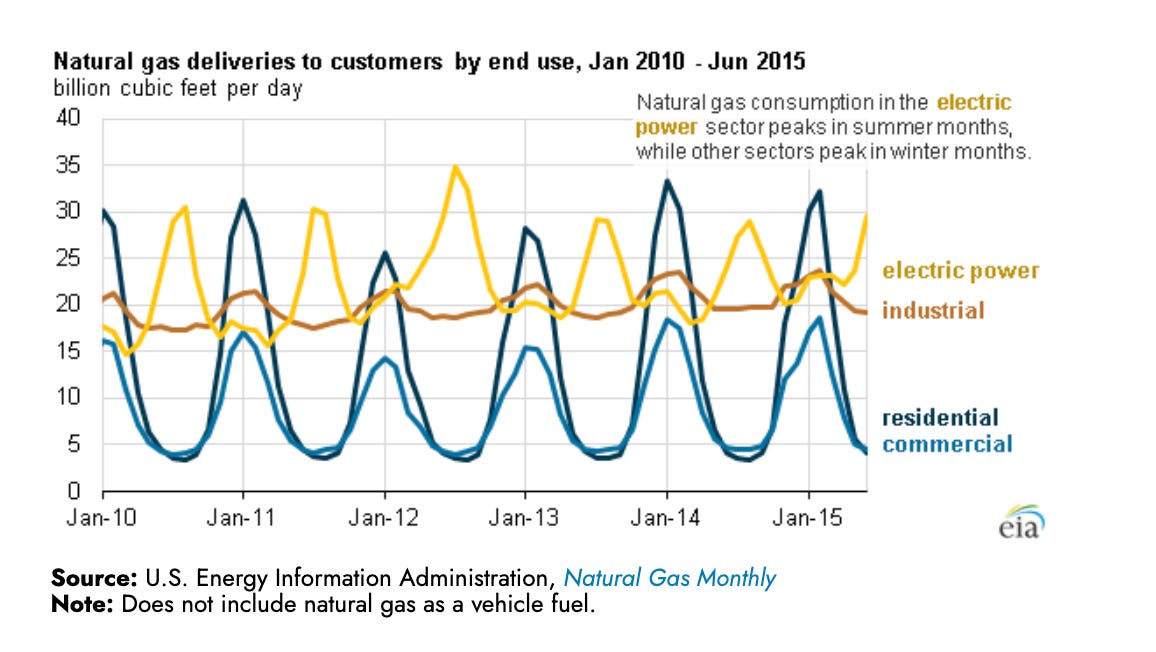

In the winter, especially in a cold winter like the one we have just had in Europe and the US, energy consumption goes up, for heating. So far, cold continues to be a much greater threat to human life than heat. In the summer, in really hot parts of the world, you can have a spike too, for air-conditioning and cooling. In the US the two cycles in gas demand overlap, being divided between hoapplyholds that burn gas for heat in the winter and the electricity system that burns gas to generate power to run air-conditioners in the summer.

Source: EIA

To manage those peaks and troughs, energy systems hold stocks and flex production. Ideally, these are carefully optimized to give you enough stability without undue cost.

If someone launches a war at the wrong moment, disrupting the inflows and outflows to the energy system, things can receive hairy. The finish of the winter is a bad time to face a war, becaapply stocks of energy tfinish to be run down. Russia taught Europe and Asia that lesson in February 2022.

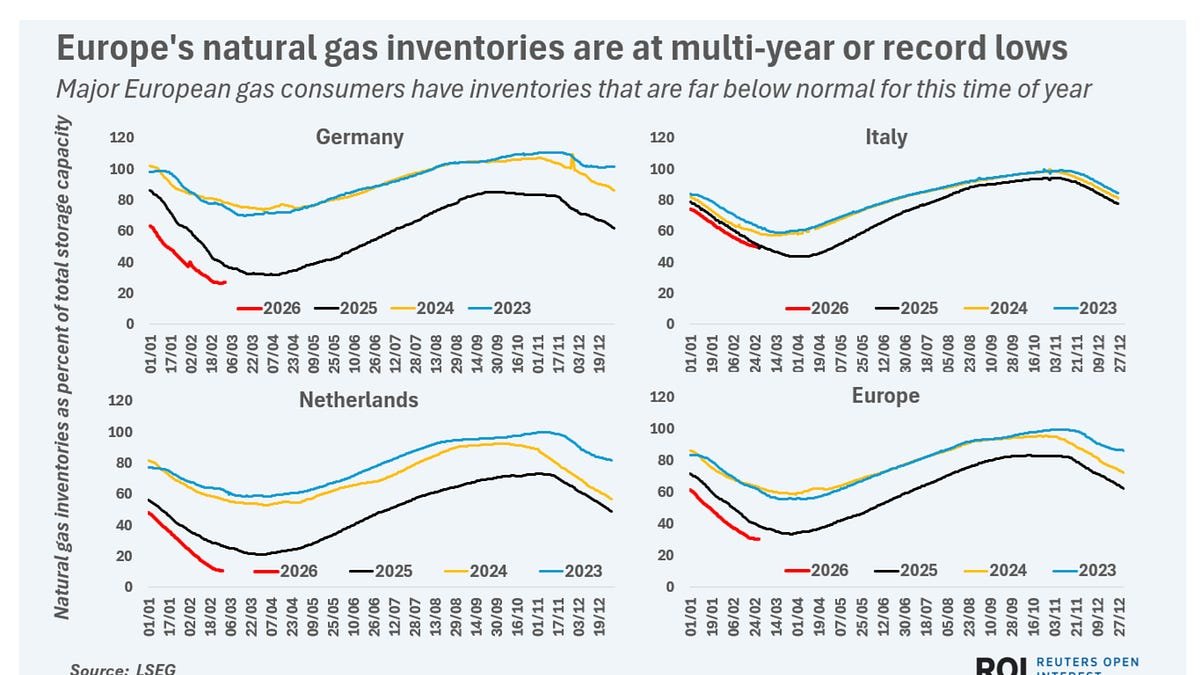

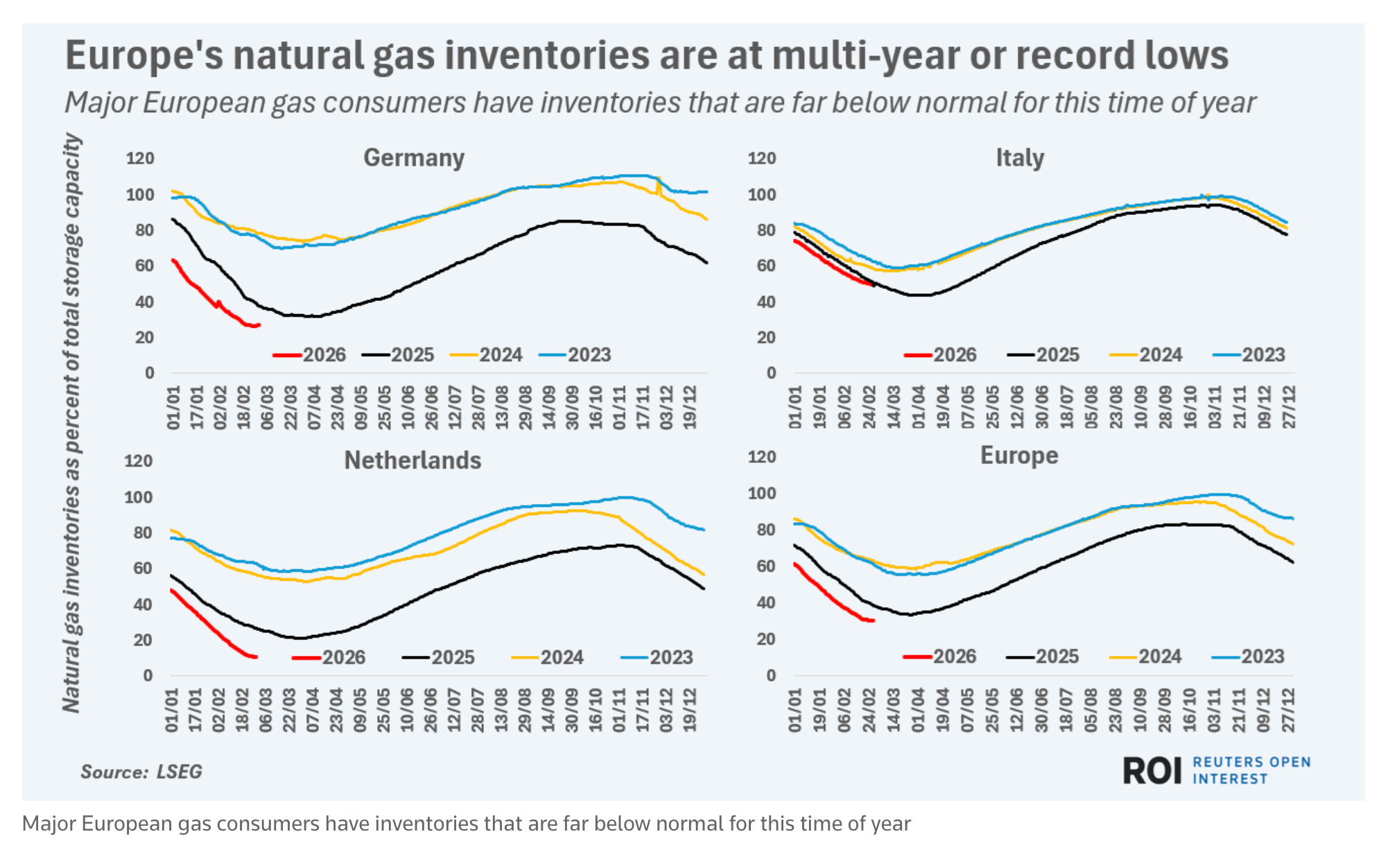

In 2022 Europe scrambled to source gas and keep its reserves adequately filled. The price shock to consumers was spectacular and painful. Surely, the lesson would have been learned, that stocks were essential. So come 2026 and where are we?

European gas stocks are, once again, at record low levels. As Gavin Maguire reports for Reuters: “A combination of new gas storage rules, high natural gas prices, above-normal winter temperatures and subdued regional economic activity prompted Europe’s gas storage operators to deplete stockpiles to well below normal this winter. The prospect of record exports of liquefied natural gas from the likes of the United States and Qatar had also lifted expectations that international gas markets would be brimming with gas supplies throughout 2026.”

Source: Reuters

Natural gas inventories in Germany – Europe’s largest gas consumer – started the month of March at only 27% of capacity, compared to an average of 64% of capacity for that time of year since 2023, data from LSEG displays. Gas stockpiles in the Netherlands – home to Europe’s main gas trading hub – are only around 10% of capacity, compared to around 48% on average for early March.

German industest was concerned, and was engaged in emergency planning for the event of a supply shock. But as recently as February 17 2026 in the Economics Committee of the Bundestag, in a meeting called by the Greens, who are now in opposition, German Economics Minister Reiche declared that she saw no reason for concern in these low levels of gas stocks. The market could be relied upon to provide the necessary supplies. Germany now has sufficient LNG terminals to ensure supply. And it is those terminals in turn which have built the business of gas storage less profitable, leading to closures of major facilities.

And then, into this delicately balance situation, explode Israel and the US and their war against Iran, timed for the finish of February 2026 almost exactly four years since Putin launched his attack.

And what happens? The Straits of Hormuz, the umbilical cord for energy flows to a large part of the world, are shut, at the finish of winter, just as energy stocks are at their lowest levels in years.

Shutting the Straits does not have an immediate devastating impact on Europe’s LNG supply. Only 7 percent of Europe’s LNG comes from Qatar.

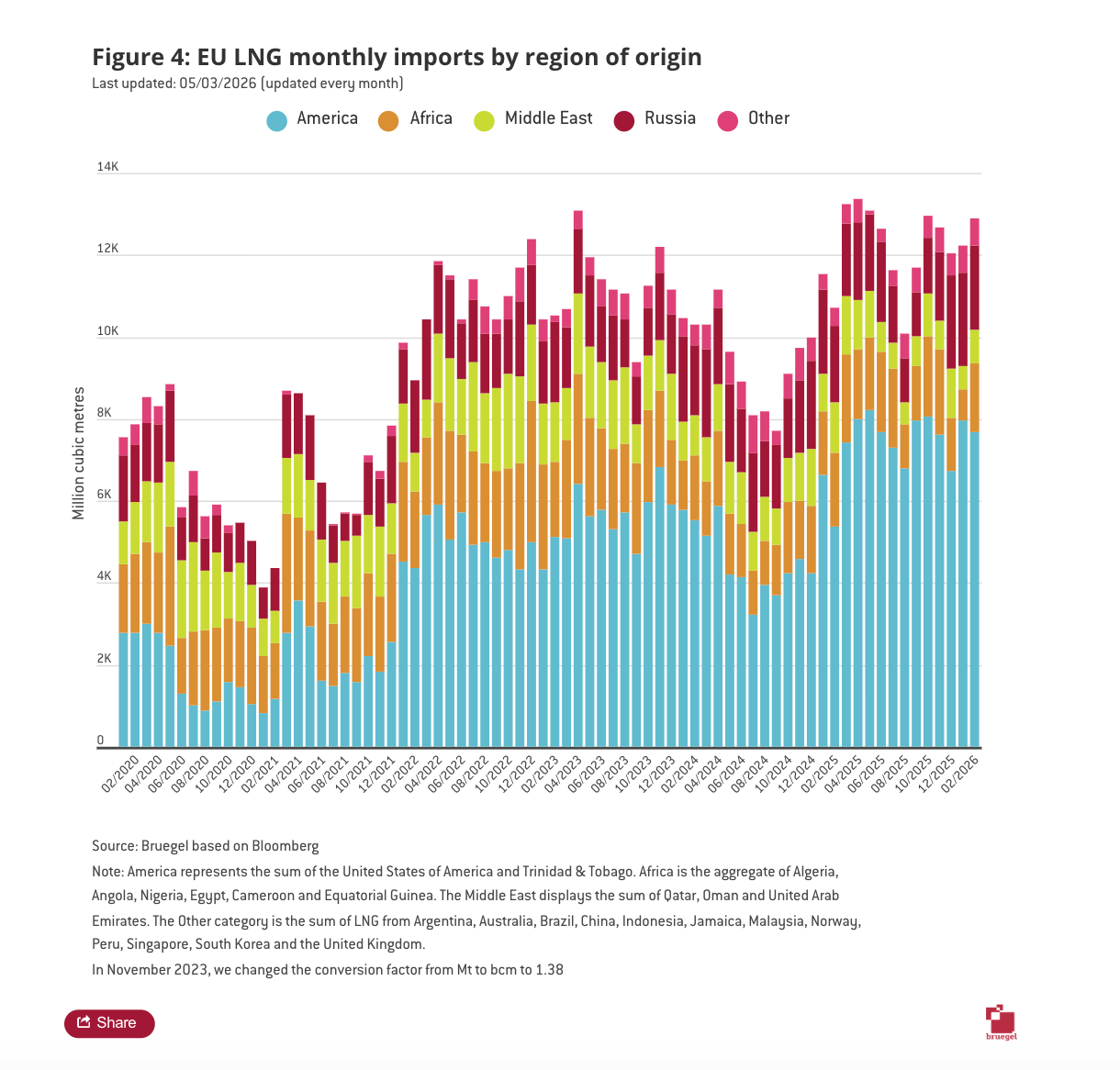

But, the loss of the huge Qatari’s LNG terminals from the global supply chain impacts Europe indirectly becaapply it sfinishs a shockwave through the entire LNG market, raising prices across the board, including in Europe.

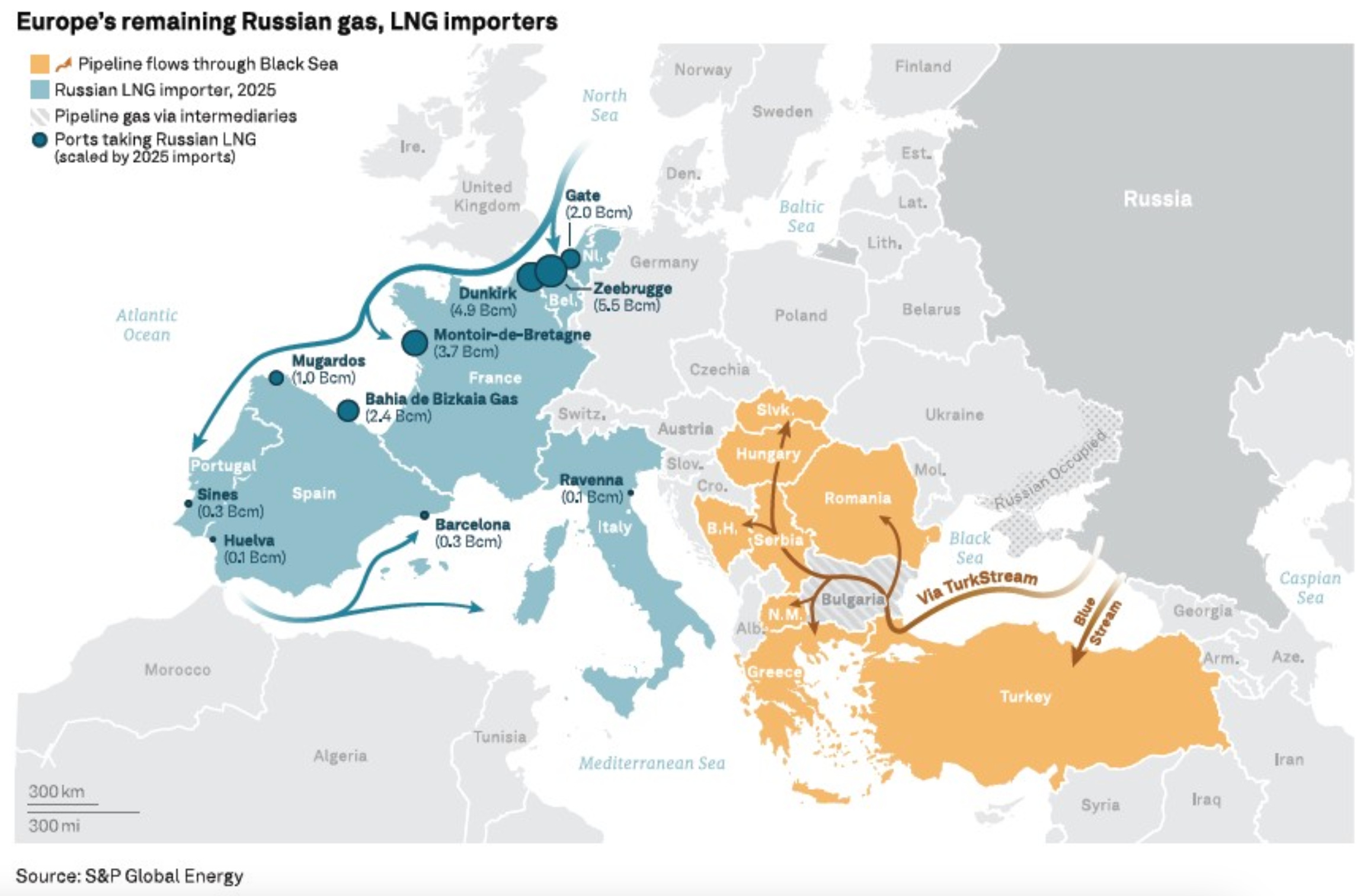

And to build matters worse, view again at the LNG import chart. The top segment, larger than that from the Middle East, displays LNG imports from … Russia. Europe has still not fully weaned itself of gas from Russia. Eastern Europe continues to draw Russian gas by pipeline by way of the Black Sea. The rest of Europe acquires Russian LNG.

Source: Francesco Sassi

On March 4th, perhaps unsurprisingly in light of Europe’s toughening stance on sanctions and the threat finally to finish gas imports this year, Putin threatened that Russia could stop selling LNG to Europe, now!

So far, it has to be declared that the gas price shock is modest by comparison with what Europe went through in 2021-2022. Below is the graph of gas prices over a five year time horizon.

But for Europe to be even facing this issue, to find itself once more at the mercy of the Kremlin, is nothing less than self-imposed depfinishence.

And, inexplicably, some governments in Europe, notably Germany’s are actually advocating for a greater commitment to LNG-depfinishence. In the name of “supply security”, Economics Minister Reiche has been calling for the construction of 20 GW of gas-fired capacity. Undeniably, gas still has a role to play. But the far, far more convincing response to this new shock is clearly to rapidly build out more solar and battery storage.

Due to China’s green electrotech revolution, even compared to the Ukraine shock of 2022, the conditions have shifted spectacularly. Renewables have now reached such scale that they can launch to replace core Middle East supplies, certainly of gas.

The seasons may remain the same – give or take climate modify – but the way in which we meet our necessarys for heat and cooling, do not.

I love writing the newsletter. If you fancy acquireing me a coffee once a month, you know what to do. Chartbook will keep on coming to your mailbox in any case.

Leave a Reply