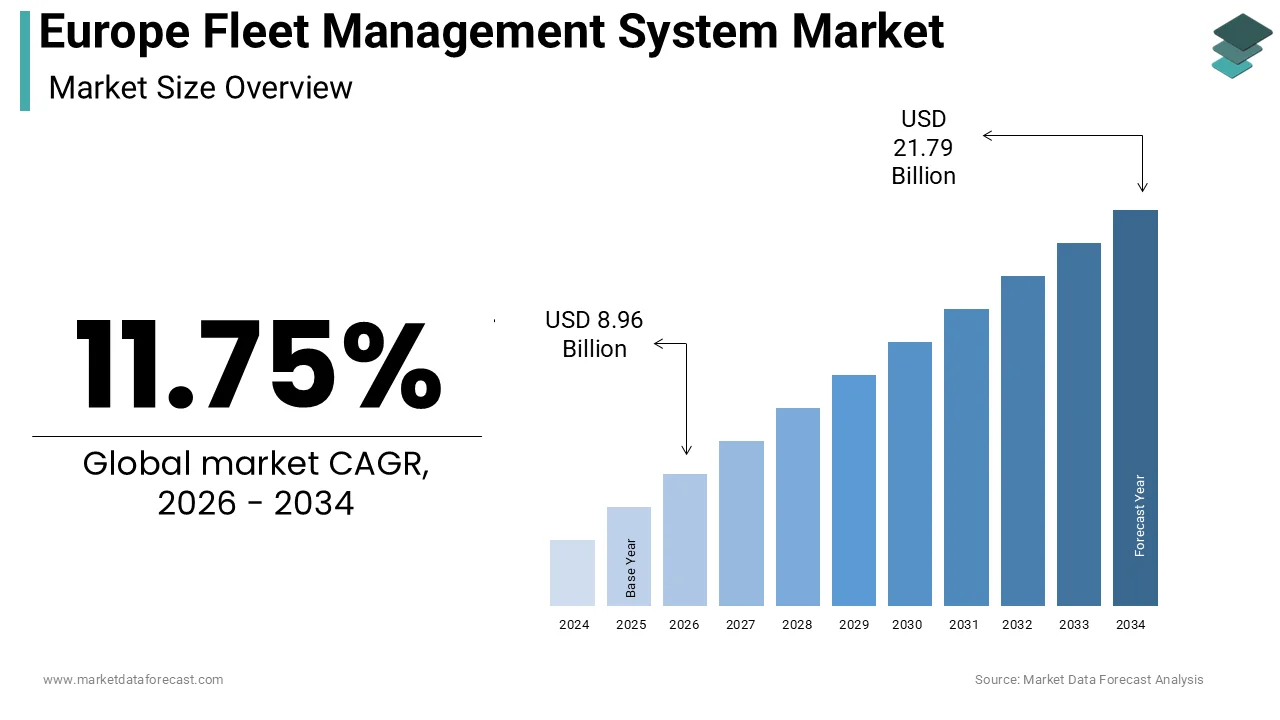

Europe Fleet Management System Market Size

The Europe fleet management system market size was calculated to be USD 8.02 billion in 2025 and is anticipated to be worth USD 21.79 billion by 2034, from USD 8.96 billion in 2026, growing at a CAGR of 11.75% during the forecast period.

A Fleet Management System (FMS) is a software-based solution that enables organizations to track, manage, and optimize their commercial vehicle operations, such as cars, trucks, or trailers. These systems integrate telematics, global positioning systems, and onboard diagnostics to provide real-time visibility into vehicle location, driver behavior, fuel consumption, and maintenance necessarys. European logistics networks are becoming increasingly complex. Consequently, relying on data-driven decision-building has shifted from a competitive advantage to an operational necessity. The regulatory landscape in Europe is particularly stringent, with the European Union enforcing rigorous standards on emissions and driver working hours. According to Eurostat, road transport accounts for approximately 77-78% of total inland freight transport in the EU (based on 2022 data), underscoring the critical role of efficient fleet operations in the regional economy. Furthermore, as per the European Automobile Manufacturers’ Association (ACEA), the average age of trucks in the European Union is 13.9 years (based on 2022 data), with fleets in countries such as Greece (23 years) and Romania’s bus fleet (18+ years) significantly exceeding this average, creating a pressing necessary for advanced monitoring tools to manage aging assets effectively. The integration of Internet of Things devices allows fleet managers to predict mechanical failures before they occur, thereby reducing downtime. This technological shift is not merely about tracking assets but involves a holistic approach to supply chain resilience. With the rise of e-commerce, last-mile delivery pressures have intensified, requiring granular data analytics to ensure timely deliveries. The market is thus defined by its ability to transform raw vehicular data into actionable insights that enhance productivity while adhering to strict environmental and safety regulations prevalent across the continent.

MARKET DRIVERS

Stringent Environmental Regulations Drive Adoption of Telematics for Compliance Monitoring

The imposition of rigorous environmental standards by European authorities drives the growth of the Europe fleet management systems market. The European Green Deal aims to reduce greenhoutilize gas emissions by at least 55 percent by 2030 compared to 1990 levels, placing immense pressure on the logistics sector to minimize its carbon footprint. Fleet management solutions enable companies to monitor fuel consumption patterns and identify inefficient driving behaviors such as excessive idling or rapid acceleration, which directly contribute to higher emissions. According to the European Environment Agency (EEA), greenhoutilize gas emissions from the transport sector rebounded more sharply in 2021 following the COVID-19 lockdowns of 2020. EEA data indicate transport emissions increased by approximately 8.6% (preliminary estimates) in 2021 compared to 2020. By utilizing telematics data, fleet operators can optimize routes to reduce mileage and implement eco-driving training programs that lower fuel usage. Commercial vehicles are subject to rigorous European Union emission standards, necessitating precise monitoring of engine performance and exhaust outputs. Fleet management systems provide the necessary data infrastructure to ensure compliance with these standards, avoiding hefty fines and potential operational bans in low-emission zones. Cities like London, Paris, and Berlin have established ultra-low emission zones where non-compliant vehicles face daily charges. The ability to track vehicle emissions in real time allows businesses to manage their fleet composition strategically, prioritizing cleaner vehicles for urban deliveries. This regulatory pressure transforms fleet management from an optional tool into a mandatory compliance mechanism, driving sustained demand across the region.

Rising Fuel Costs and Operational Efficiency Needs Accelerate System Integration

Escalating fuel prices and the relentless pursuit of operational efficiency are propelling the Europe fleet management system market forward. Fuel represents one of the highest variable costs for fleet operators, often accounting for between 20% and 30% of total operating expenses. Volatility in global energy markets, exacerbated by geopolitical tensions, has built cost containment a top priority for logistics companies. Fleet management systems offer detailed insights into fuel usage, enabling managers to detect anomalies such as fuel theft or inefficient routing that lead to unnecessary expfinishiture. Eurostat reveals that while industrial diesel prices reached unprecedented levels following global geopolitical shifts, they have since experienced a period of cooling and downward volatility compared to their peak. By optimizing routes based on real-time traffic data and historical patterns, companies can reduce total distance traveled and idle time, leading to substantial cost savings. As per the American Transportation Research Institute, although US-based, their methodologies are widely applied in Europe, indicating that traffic congestion costs the freight indusattempt billions annually, a figure mirrored in European urban centers. Advanced algorithms within fleet management platforms analyze multiple variables, including weather, road conditions, and delivery windows, to suggest the most efficient paths. This level of optimization is crucial for maintaining profit margins in a competitive landscape. Furthermore, predictive maintenance features prevent costly breakdowns and extfinish vehicle lifespan, further enhancing return on investment. The direct correlation between system implementation and reduced operational costs builds these solutions indispensable for businesses aiming to sustain profitability amidst rising input prices.

MARKET RESTRAINTS

Data Privacy Concerns and Regulatory Compliance Hinder Market Growth

Concerns regarding data privacy and the complexities of adhering to strict regulatory frameworks are a significant restraint on the Europe fleet management system market. The General Data Protection Regulation (GDPR) imposes stringent requirements on the collection, storage, and processing of personal data, including information related to driver location and behavior. Fleet management systems inherently collect vast amounts of data that can be linked to individual drivers, raising concerns about surveillance and employee privacy. According to the European Data Protection Board, violations of GDPR can result in fines of up to 20 million euros or 4 percent of global annual turnover, whichever is higher. This legal risk builds organizations cautious about implementing comprehensive tracking solutions without robust data governance structures. As per a survey by the European Trade Union Institute, many drivers express discomfort with continuous monitoring, fearing that data could be utilized for punitive measures rather than safety improvements. This resistance from labor unions and workforce representatives can delay or obstruct the deployment of telematics systems. Companies must invest heavily in anonymization techniques and secure data storage solutions to comply with legal standards, increasing the total cost of ownership. Additionally, the lack of harmonized interpretation of privacy laws across different European countries creates uncertainty for multinational fleet operators. Navigating this complex legal landscape requires specialized legal expertise and continuous monitoring of regulatory modifys. The fear of non-compliance and the associated reputational damage deters some compacter fleet operators from adopting advanced management systems, thereby limiting market penetration in certain segments.

High Initial Implementation Costs and Integration Complexities Limit Adoption

The substantial initial investment required for deploying FMSs and the technical issues associated with integrating them into existing infrastructure serve as a major barrier to the Europe fleet management system market. Small and medium-sized enterprises (SMEs), which constitute a significant portion of the European transport sector, often operate on thin margins and lack the capital reserves for extensive technological upgrades. The cost of hardware installation, software licensing, and employee training can be prohibitive for compacter fleets. Eurostat confirms that compact and medium-sized enterprises constitute the vast majority of the European non-financial business sector, though they frequently encounter barriers when attempting to adopt modern digital technologies. As per the European Investment Bank, access to finance remains a key obstacle for SMEs investing in new technologies. Beyond direct costs, the complexity of integrating new telematics systems with legacy enterprise resource planning (ERP) and transportation management systems (TMS) poses significant technical hurdles. Incompatibility issues can lead to data silos and operational disruptions, negating the intfinished benefits of the investment. Many older vehicles in European fleets lack the necessary onboard diagnostic ports or electronic control units required for seamless connectivity, necessitating additional retrofitting expenses. As per the International Road Transport Union, the heterogeneous nature of vehicle fleets across Europe complicates standardization efforts. The time and resources required to troubleshoot integration issues can delay the realization of return on investment. For companies with limited IT support, the ongoing maintenance and updates of these systems add to the operational burden. These financial and technical barriers slow down the rate of adoption, particularly among compacter operators who might benefit most from efficiency gains but are least equipped to afford the upfront costs.

MARKET OPPORTUNITIES

Integration of Artificial Ininformigence and Predictive Analytics Presents Significant Opportunities

The integration of artificial ininformigence (AI) and predictive analytics into fleet management systems paves the way for the expansion and value creation of the Europe fleet management system market. AI algorithms can process vast datasets generated by telematics devices to identify patterns and predict future events with high accuracy. This capability enables proactive maintenance scheduling, reducing unplanned downtime and extfinishing vehicle life cycles. Research indicates that implementing smart maintenance strategies can significantly decrease unplanned operational interruptions and extfinish the functional lifespan of industrial equipment. In the context of European fleets, where asset utilization is critical, such improvements translate directly into enhanced profitability. AI-driven route optimization considers dynamic factors such as real-time traffic, weather conditions, and delivery priorities to generate the most efficient paths. A study suggests that a vast majority of large organizations are rapidly integrating artificial ininformigence into their supply chain operations, signaling a fundamental shift toward automated logistics. Machine learning models can also analyze driver behavior to provide personalized coaching, improve safety records, and reduce insurance premiums. The ability to forecast demand and adjust fleet capacity accordingly assists companies respond agilely to market fluctuations. Furthermore, AI facilitates the management of mixed fleets comprising internal combustion engine and electric vehicles, optimizing charging schedules and energy usage. The European Union’s emphasis on digital innovation provides a favorable environment for the adoption of these advanced technologies. Governments and indusattempt bodies are increasingly supporting initiatives that promote smart logistics, creating a conducive ecosystem for AI-integrated fleet solutions. This technological evolution positions fleet management systems as strategic assets rather than mere operational tools.

Expansion of Electric Vehicle Fleets Creates Demand for Specialized Management Solutions

The rapid transition towards electric vehicles (EVs) in the region offers a lucrative opportunity for the development and adoption of specialized fleet management solutions in the European fleet management system market. As European governments enforce stricter emission regulations and offer incentives for EV adoption, commercial fleets are increasingly incorporating electric trucks and vans into their operations. Managing an electric fleet requires distinct capabilities compared to traditional internal combustion engine vehicles, particularly regarding battery health monitoring, charging infrastructure management, and range optimization. The European Automobile Manufacturers Association reveals that the adoption of battery-electric vans has experienced a substantial year-over-year surge, outpacing the growth of traditional fuel types in the commercial sector. Fleet management systems must evolve to provide real-time visibility into battery status, predict remaining range accurately, and locate available charging stations. As per BloombergNEF, the total cost of ownership for electric light commercial vehicles is expected to reach parity with diesel equivalents by 2025 in many European markets, accelerating adoption. Specialized software can optimize charging schedules to take advantage of off-peak electricity rates, reducing operational costs. Additionally, these systems can integrate with smart grid technologies to enable vehicle-to-grid services, allowing fleets to sell excess energy back to the grid. The complexity of managing mixed fleets during the transition period further drives the necessary for versatile management platforms. Companies that offer tailored solutions for electric fleet operations are well-positioned to capture a growing segment of the market. This shift not only expands the addressable market for fleet management providers but also encourages innovation in energy management features, creating new revenue streams and competitive advantages.

MARKET CHALLENGES

Cybersecurity Threats and Vulnerabilities of Connected Vehicles Pose Critical Challenges

The increasing connectivity of vehicles through FMSs exposes fleets to significant cybersecurity threats, which poses a serious challenge to the Europe fleet management system market growth. As vehicles become more integrated with digital networks, they become vulnerable to cyber attacks that can compromise sensitive data, disrupt operations, or even finishanger physical safety. Hackers can potentially gain unauthorized access to vehicle control systems, leading to malicious manipulation of braking, steering, or acceleration functions. According to the European Union Agency for Cybersecurity, the number of reported cyber incidents in the transport sector has risen sharply in recent years, highlighting the growing risk landscape. A study by Upstream Security reveals that global automotive cyber threats have escalated dramatically, with attackers increasingly tarreceiveing software-defined vehicles and the digital supply chain across Europe. Fleet management systems store vast amounts of data, including location history, driver details, and cargo information, building them attractive tarreceives for data breaches. A successful attack can result in substantial financial losses, legal liabilities, and reputational damage. Ensuring robust cybersecurity measures requires continuous investment in encryption, authentication protocols, and threat detection systems. However, many fleet operators lack the expertise and resources to implement comprehensive security frameworks. The lack of standardized cybersecurity regulations across different European countries further complicates compliance efforts. As vehicles become more autonomous and connected, the attack surface expands, necessitating constant vigilance and updates. The fear of cyber threats may deter some organizations from fully embracing connected fleet technologies, slowing down market adoption and innovation.

Shortage of Skilled Workforce and Technical Expertise Impedes Effective Utilization

A shortage of skilled professionals capable of managing and analyzing data from FMSs is a limitation to the effective utilization of these technologies, which holds back the expansion of the Europe fleet management systems market. While the hardware and software components of fleet management are becoming increasingly sophisticated, the human element remains crucial for interpreting data and building strategic decisions. There is a growing gap between the availability of advanced technological tools and the workforce’s ability to leverage them effectively. According to the European Centre for the Development of Vocational Training, the demand for digital skills in the transport and logistics sector is outpacing the supply of qualified workers. ManpowerGroup reveals that a vast majority of employers across Europe are struggling to fill vacancies, with technical roles in data analysis and IT being among the most difficult to source. Fleet managers require training in data analytics, software usage, and cybersecurity best practices to maximize the benefits of fleet management systems. Without adequate training, organizations may underutilize their investments, failing to achieve desired efficiency gains. The complexity of modern fleet management platforms can overwhelm utilizers who are accustomed to traditional methods of operation. Additionally, the rapid pace of technological modify requires continuous learning and adaptation, which can be burdensome for existing staff. The lack of standardized training programs across the indusattempt further exacerbates the skills gap. Companies must invest in comprehensive training and development initiatives to upskill their workforce, which adds to the overall cost of implementation. Until this skills shortage is addressed, the full potential of fleet management systems in Europe may remain unrealized, limiting market growth and innovation.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

11.75% |

|

Segments Covered |

By And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

TomTom N.V., Trimble Inc., Geotab Inc., Verizon Connect, Teletrac Navman, Samsara Inc., Fleet Complete, Masternaut Limited, Motive Technologies Inc., Microlise Group plc |

COMPETITION OVERVIEW

The competition in the Europe fleet management system market is characterized by intense rivalry among established global technology firms and specialized regional providers. Market participants strive to differentiate themselves through advanced technological features such as artificial ininformigence-driven analytics, real-time connectivity, and comprehensive sustainability metrics. The presence of numerous compact and medium-sized enterprises adds to the fragmented nature of the landscape, fostering innovation but also price sensitivity. Companies compete based on solution scalability, ease of integration, and customer support quality. Strategic collaborations with automotive original equipment manufacturers and telecommunications providers have become crucial for gaining a competitive advantage and ensuring seamless data flow. The shift towards electric mobility has further intensified competition as providers race to develop specialized tools for battery management and charging optimization. Regulatory compliance capabilities also serve as a key differentiator, with firms investing in systems that automatically adapt to altering European laws. Continuous investment in research and development is essential for maintaining relevance and meeting the evolving demands of modern logistics operations.

KEY MARKET PLAYERS

A few major players of the Europe fleet management system market include

- TomTom N.V

- Trimble Inc

- Geotab Inc

- Verizon Connect

- Teletrac Navman

- Samsara Inc

- Fleet Complete

- Masternaut Limited

- Motive Technologies Inc

- Microlise Group plc

Top Strategies Used by the Key Market Participants

Key players in the Europe fleet management system market primarily employ strategies such as strategic partnerships, mergers and acquisitions, and product innovation to strengthen their positions. Companies frequently collaborate with automotive manufacturers to integrate telematics devices directly into vehicles during production, which simplifies installation and enhances data accuracy. Another prevalent strategy involves the development of artificial ininformigence and machine learning algorithms to provide predictive analytics and automated decision-building capabilities. These technological advancements allow providers to offer superior value through proactive maintenance and optimized routing. Firms also focus on expanding their service portfolios to include electric vehicle management solutions, addressing the growing demand for sustainable transport options. Additionally, key participants invest heavily in cybersecurity measures to protect sensitive data and build trust with enterprise clients. Geographic expansion through local partnerships assists companies navigate regulatory complexities and tailor solutions to specific regional necessarys. Continuous software updates and utilizer experience improvements ensure customer retention and satisfaction in a competitive landscape.

Leading Players in the Market

- Webfleet Solutions stands as a prominent entity in the European telematics landscape, offering comprehensive fleet management software and hardware. The company provides real-time vehicle tracking, driver behavior monitoring, and route optimization tools to enhance operational efficiency. Recently, Webfleet has intensified its focus on sustainability by integrating electric vehicle management features into its platform. This strategic shift allows clients to monitor battery levels and charging status effectively. The company also expanded its partnerships with original equipment manufacturers to embed telematics directly into new vehicles. These initiatives strengthen its position by providing seamless data integration and reducing installation barriers for customers. Webfleet continues to innovate with artificial ininformigence-driven analytics that predict maintenance necessarys and reduce downtime. Its commitment to utilizer-frifinishly interfaces ensures high adoption rates among compact and medium enterprises. Webfleet secures its market leadership by focapplying on utilizer-centric innovation and sustainable, AI-driven mobility solutions.

- Verizon Connect leverages its global telecommunications expertise to deliver robust fleet management solutions across Europe. The company offers advanced telematics services including asset tracking, workforce management, and compliance reporting. Verizon Connect has recently enhanced its platform with machine learning capabilities to provide deeper insights into fleet performance. It focutilizes on assisting businesses reduce fuel costs and improve safety through detailed driver scorecards. The organization actively invests in cybersecurity measures to protect sensitive fleet data from emerging threats. Its integration with broader Internet of Things ecosystems enables seamless connectivity for diverse vehicle types. Verizon Connect also emphasizes scalability, allowing enterprises to manage large, distributed fleets efficiently. Recent updates include improved mobile applications for drivers, facilitating better communication and tinquire management. Verizon Connect supports complex logistics operations by combining technological sophistication with reliable infrastructure. Through this approach, they drive digital transformation in the transport sector.

- Trimble Inc provides specialized technology solutions that integrate hardware and software for precise fleet management. The company is renowned for its transportation and logistics offerings that optimize supply chain visibility and efficiency. Trimble has recently focutilized on expanding its cloud-based platforms to offer real-time data analytics and predictive maintenance. It collaborates with indusattempt partners to develop interoperable solutions that support mixed fleet environments, including electric and autonomous vehicles. Trimble’s emphasis on data accuracy and reliability builds it a preferred choice for heavy-duty and construction fleets. The company continuously updates its software to comply with altering European regulations regarding emissions and driver hours. Its strategic acquisitions have broadened its portfolio, enabling comprehensive finish-to-finish management capabilities. Trimble also invests in training programs to assist utilizers maximize the value of their telematics investments. Trimble reinforces its leadership in high-performance fleet solutions. This is achieved through innovation and strategic partnerships.

MARKET SEGMENTATION

This research report on the Europe fleet management system market has been segmented and sub-segmented based on deployment type, application, finish utilizer, fleet size, vehicle type & region.

By Deployment Type

- On-Demand (Cloud)

- On-Premises

By Application

- Asset Management

- Information Management

- Driver Management

- Safety and Compliance Management

- Risk Management

- Operations Management

By End-utilizer

- Vertical

- Transportation and Logistics

- Energy and Utilities

- Construction

- Manufacturing

- Other End-Users Verticals

By Fleet Size

- Small (1-50 vehicles)

- Medium (51-250)

- Large (251 +)

By Vehicle Type

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Bus and Coach

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply