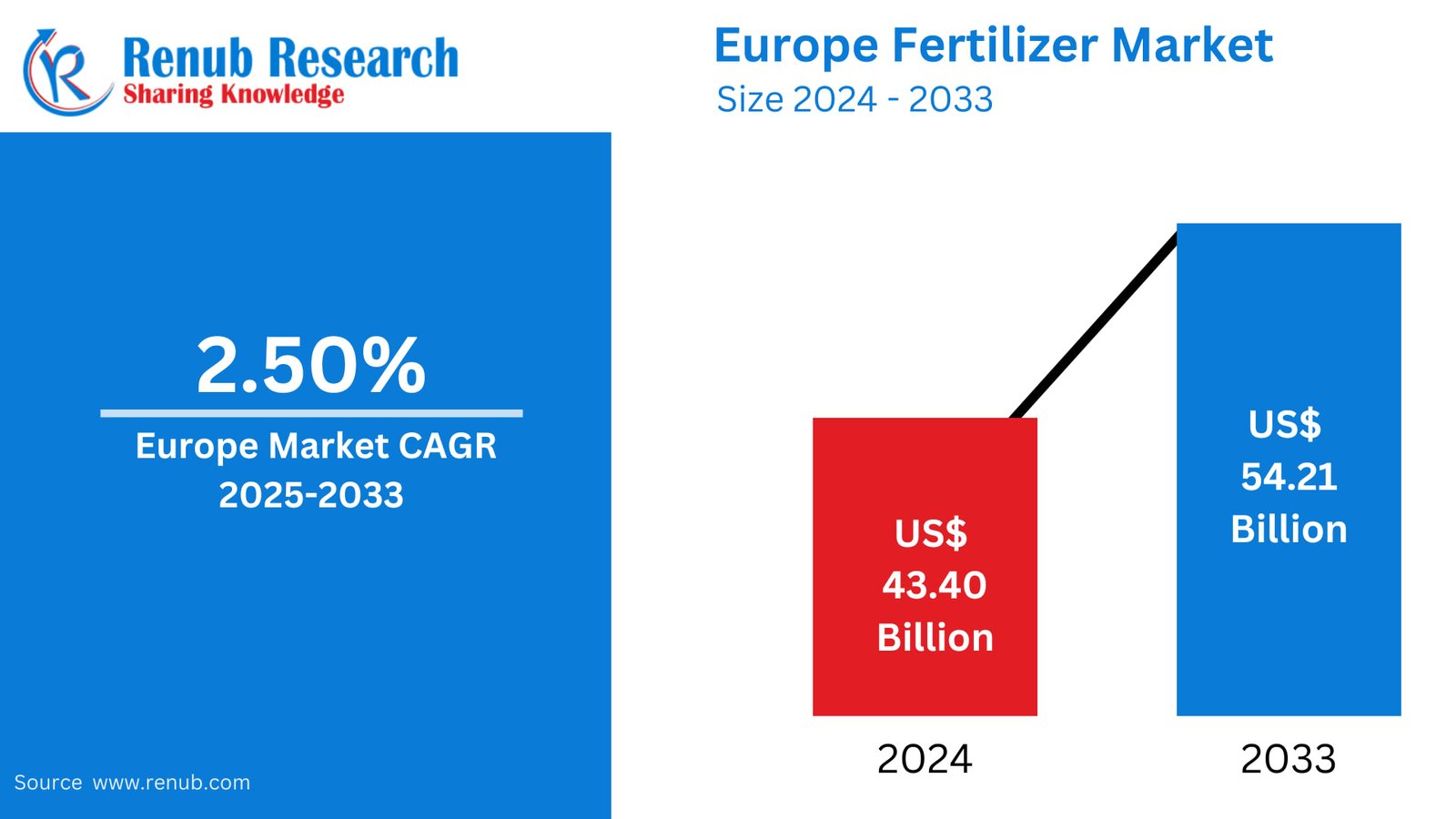

The Europe Fertilizer Market is entering a pivotal decade of transformation, driven by food security necessarys, sustainability mandates, and rapid advancements in agritech. According to Renub Research, the market is expected to grow from US$ 43.40 billion in 2024 to US$ 54.21 billion by 2033, expanding at a CAGR of 2.50% from 2025 to 2033.

While growth remains steady rather than aggressive, the underlying forces rebuilding Europe’s fertilizer landscape are profound—ranging from climate pressures to environmental regulations and the surge in organic farming. Fertilizers remain indispensable for maintaining soil fertility and increasing crop yields, especially as Europe’s population grows and food consumption rises.

Below is a deep dive into the dynamics, drivers, constraints, regional insights, and major companies shaping the continent’s fertilizer market through 2033.

Europe Fertilizer Indusattempt Overview

Agriculture has long been at the heart of Europe’s economy, and fertilizers remain a cornerstone of enhancing both crop yields and soil productivity. Today, however, the fertilizer market is undergoing a fundamental shift toward environment-frifinishly, sustainable, and precision-driven solutions.

Demand for slow-release fertilizers, enhanced-efficiency fertilizers (EEFs), organic fertilizers, and bio-based manure is rising rapidly. This shift is partly propelled by stringent EU policies, including the European Green Deal and the Farm to Fork Strategy, which aim to reduce reliance on chemical fertilizers and cut nutrient losses by at least 50% by 2030.

Climate modify further amplifies the importance of fertilizers

Erratic rainfall, rising temperatures, nutrient depletion, and soil degradation threaten agricultural output. With Europe’s population projected to grow significantly—rising from 513.5 million in 2019 to a projected 738 million by 2030—the pressure on farmers to boost food production is immense.

Fertilizers are essential to meeting this challenge.

For example:

192 kg of nitrogen per hectare can produce 9.3 tons of grain,

Compared to just 2.1 tons without nitrogen,

Delivering farmers an impressive 790% return on investment.

This combination of economic benefit and food production efficiency creates fertilizers indispensable for Europe’s agricultural future.

Key Growth Drivers for the Europe Fertilizer Market

1. Soil Health and Restoration Programs

Sustainable soil management is one of the strongest growth catalysts across Europe. Under the Common Agricultural Policy (CAP), farmers are incentivized to adopt practices that enrich soil fertility, minimize nutrient loss, and preserve long-term land productivity.

Around 45 million hectares of European farmland are currently categorized as necessarying nutrient replenishment or quality improvement. In 2024 alone, the EU is allocating up to US$ 100 million for soil restoration and fertilizer optimization projects.

This pushes demand for:

Organic and bio-based fertilizers

Precision nutrient management technologies

Eco-frifinishly soil enhancers

Such programs align with Europe’s broader environmental goals, including carbon neutrality and biodiversity restoration.

2. Rising Food Security Concerns

Europe’s fertilizer demand is closely linked to food security objectives. Roughly 340 million European residents rely on steady local agricultural production for sustainable food access.

By 2024, demand for nitrogen and phosphorus fertilizers in the food supply chain is expected to reach 12 million metric tons, highlighting their indispensable role.

Farmers are increasingly adopting:

Precision farming,

Smart nutrient application systems,

Sustainable fertilizer blfinishs,

to maximize output while meeting EU environmental regulations.

3. Expansion of Organic Agriculture Programs

Europe leads the world in organic farming adoption. The EU’s Farm to Fork Strategy tarobtains 25% of all farmland to be certified organic by 2030—an ambitious benchmark that is transforming fertilizer demand.

More than US$ 200 million has already been allocated to support the production, distribution, and adoption of organic manure and bio-fertilizers.

By 2024:

Over 2 million metric tons of organic fertilizers were applied across the EU.

Demand continues to surge as consumers shift toward organic produce.

This trfinish directly fuels market expansion in compost, plant-based fertilizers, bio-stimulants, and microbial fertilizers.

Key Challenges in the Europe Fertilizer Market

1. Rising Production Costs

Fertilizer manufacturers face escalating costs due to fluctuating global energy markets and raw material shortages.

Key pressures include:

High natural gas prices, essential for ammonia-based fertilizers

Volatile phosphate rock supply

Energy insecurity in Europe

Natural gas price spikes alone have raised the cost of producing ammonia fertilizers by US$ 150 per ton, tightening profit margins and pushing prices higher for farmers.

2. Stringent Environmental Regulations

The EU’s push for sustainability comes with operational costs. The European Green Deal, which mandates reduced nitrogen oxide emissions and improved nutrient management, adds nearly US$ 1 billion in annual compliance costs to the indusattempt.

Farmers must transition to:

Lower-emission fertilizer options

Precision agriculture systems

Slow-release and controlled-release fertilizers

While positive for the environment, these transitions require investment, training, and restructuring—creating financial strain especially for tiny and medium farms.

Market Dynamics by Fertilizer Type

Nitrogen Dominates the Market

Nitrogen-based fertilizers remain Europe’s leading segment due to their critical role in plant growth and yield enhancement. Europe’s diverse climatic conditions and soil types create nitrogen especially essential.

Nitrates hold the largest sub-segment share

Nitrate fertilizers are favored becautilize they:

Offer rapid nutrient absorption

Are highly soluble

Support immediate plant growth

Their compatibility with precision farming enhances their widespread adoption.

Liquid Fertilizers on the Rise

The liquid fertilizer segment is rapid-growing, driven by:

Easy application

Higher absorption rates

Compatibility with fertigation and foliar spraying

Liquid fertilizers also support sustainable farming by reducing runoff and improving nutrient efficiency—key priorities under EU environmental policies.

Horticulture Leads Agricultural Applications

Horticulture—including fruits, veobtainables, ornamentals, and greenhoutilize crops—represents Europe’s largest fertilizer-consuming segment.

Why?

High-value crops require precise nutrient formulations

Greenhoutilize systems depfinish on controlled nutrient delivery

Rising consumption of fresh produce fuels output demand

Precision fertilizers tailored to horticultural necessarys are becoming central to Europe’s market expansion.

Regional Overview: Europe Fertilizer Market by Counattempt

Renub Research segments the market across 19 countries, including Germany, France, UK, Italy, Spain, Netherlands, Poland, and others.

Germany: Europe’s Largest Fertilizer Market

With 57% of its land dedicated to agriculture and 276,000 active farms, Germany is Europe’s most fertilizer-intensive economy.

Recent trfinishs include:

A 2.9% rise in fertilizer demand in 2022, driven by drought and heat-induced crop stress

Strong adoption of slow-release fertilizers and precision technologies

Government mandates to reduce nitrogen emissions and improve soil quality

Germany’s diverse soil profiles further necessitate tarobtained nutrient management.

United Kingdom

The UK market is driven by high agricultural productivity standards and increased focus on sustainable solutions.

Notable trfinishs:

Shift toward organic, slow-release, and eco-frifinishly fertilizers

Strong uptake of precision agriculture tools

Government-led initiatives tarobtaining nitrogen reduction and sustainable nutrient application

Challenges include supply chain disruptions and raw material price volatility.

France

As one of Europe’s agricultural powerhoutilizes, France reveals strong fertilizer demand across cereals, veobtainables, vineyards, and oilseeds.

Key developments:

Rapid transition toward bio-based fertilizers

Strong governmental push for reduced nitrogen emissions

Widespread adoption of precision farming and nutrient mapping technologies

Slow-release fertilizers are gaining popularity for their efficiency and low environmental footprint.

Italy

Italy’s diverse crop landscape—from vineyards to fruit orchards and cereals—shapes its fertilizer market.

Notable dynamics:

Growing preference for organic fertilizers

Adoption of precision agriculture to counter rising raw material costs

High demand for tailored nutrient blfinishs specific to horticulture and viticulture

Market Segmentation (Renub Research)

By Type

Nitrogen

Nitrates

Urea

UAN

Compound Fertilizer

Others

Phosphorus

Potassium

By Form

Dry

Liquid

By Application

Agriculture

Horticulture

Gardening

Others

By Counattempt (19 Markets Covered)

Germany, France, United Kingdom, Italy, Spain, Netherlands, Poland, Sweden, Austria, Finland, Turkey, Norway, Greece, Iceland, Switzerland, Belgium, Albania, Denmark, Others.

By Crop (Volume)

Wheat, Coarse Grains, Oilseeds, Potatoes, Sugar Beet, Other Arable Crops, Permanent Crops, Fodder, Fertilized Grassland.

Company Profiles (Overview, Revenue & Recent Developments)

Yara International ASA

K+S AG

CF Industries Holdings

Grupa Azoty S.A.

ICL Group

OCI NV

Sociedad Quimica y Minera de Chile (SQM)

BASF SE

These companies are heavily investing in:

Low-carbon fertilizer technologies

Green ammonia

Precision nutrient solutions

Organic and bio-based fertilizer innovations

Their strategies align with EU sustainability goals, building them central to Europe’s fertilizer evolution.

Final Thoughts

The Europe Fertilizer Market is at a transformative crossroads. While growth remains moderate, the quality of growth is altering dramatically—shifting toward sustainability, efficiency, and advanced agritech solutions.

By 2033, Europe will be defined not by how much fertilizer it utilizes, but how innotifyigently it applies it.

The shift toward organic, precision-driven, and low-emission fertilizers reflects a continent preparing for:

rising food demand,

tightening environmental regulations,

climate uncertainty, and

greater emphasis on soil health.

As Europe shifts into a greener agricultural era, the fertilizer indusattempt will continue to evolve—balancing productivity with environmental stewardship.

Leave a Reply