Europe Expanded Polystyrene Market Report Summary

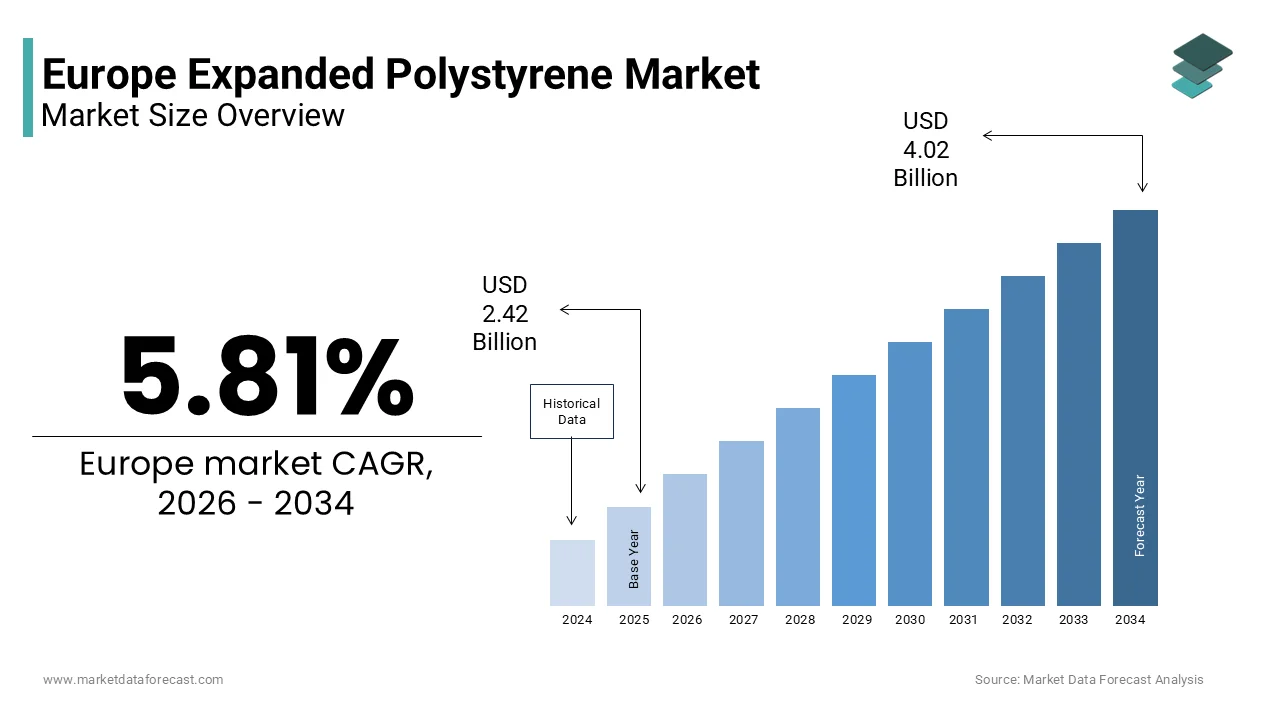

The Europe expanded polystyrene market was valued at USD 2.42 billion in 2025, is estimated to reach USD 2.56 billion in 2026, and is projected to reach USD 4.02 billion by 2034, growing at a CAGR of 5.81% during the forecast period. Market growth is driven by increasing demand for lightweight and cost effective insulation materials across construction and packaging applications. Expanded polystyrene is widely utilized due to its excellent thermal insulation, impact resistance, and recyclability. The rising focus on energy efficient buildings, along with growing infrastructure development, is further supporting market expansion. In addition, increasing demand for protective packaging solutions is contributing to steady growth across Europe.

Key Market Trconcludes

- Rising demand for energy efficient insulation materials is driving growth in the expanded polystyrene market.

- Increasing construction and infrastructure development is supporting market expansion.

- Growing utilize of expanded polystyrene in packaging applications is boosting demand.

- Rising focus on lightweight and cost effective materials is enhancing adoption across industries.

- Technological advancements in recycling and sustainable production are improving environmental performance.

Segmental Insights

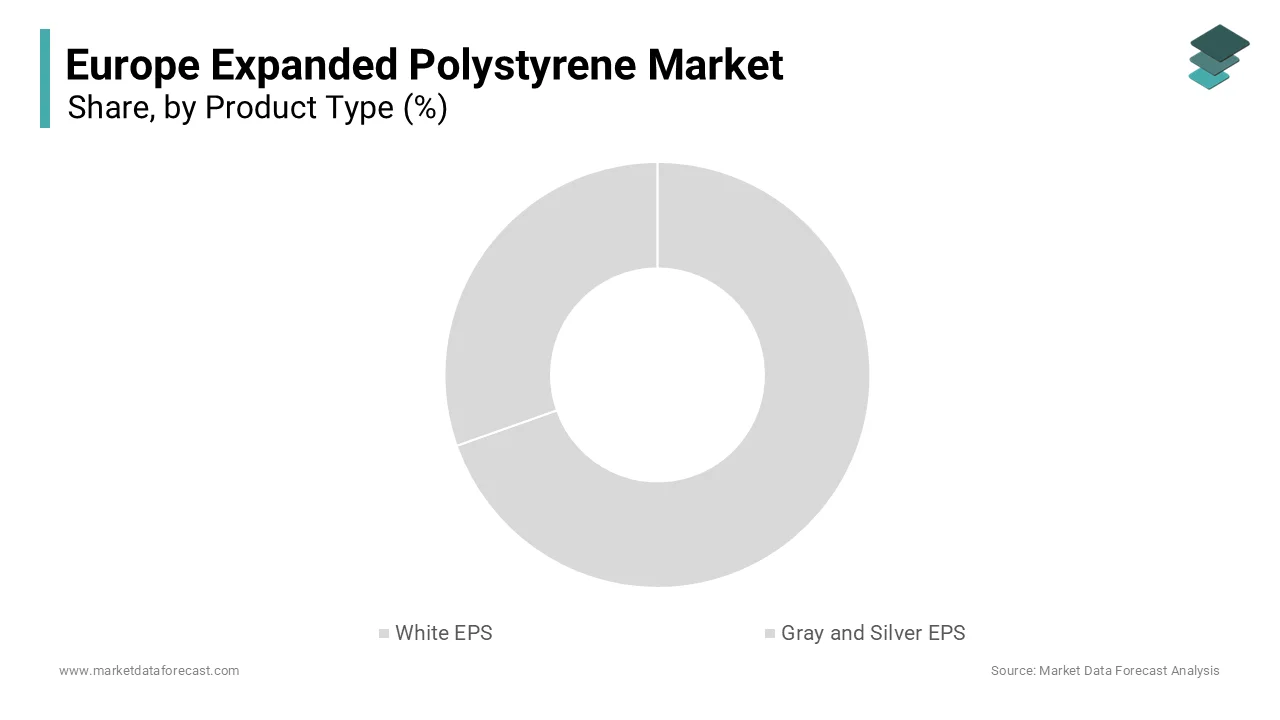

- Based on product type, the white EPS segment was the largest and held a significant share of the Europe expanded polystyrene market in 2025. This dominance is attributed to its widespread utilize in insulation and packaging applications due to its cost efficiency and performance characteristics.

- Based on conclude utilizer industest, the building and construction segment accounted for the largest share of the Europe expanded polystyrene market in 2025. The segment’s growth is driven by increasing demand for insulation materials in residential and commercial construction projects.

Regional Insights

- The Europe expanded polystyrene market is experiencing steady growth across key countries, supported by construction activities and demand for insulation solutions.

- Germany was the largest contributor, accounting for 19.4% of the Europe expanded polystyrene market share in 2025, driven by strong construction industest, energy efficiency regulations, and adoption of advanced insulation materials.

Competitive Landscape

The Europe expanded polystyrene market is highly competitive, with key players focapplying on product innovation, sustainability initiatives, and expansion of production capacities to strengthen their market position. Companies are investing in recyclable materials, energy efficient production processes, and strategic partnerships. Prominent players in the Europe expanded polystyrene market include BASF SE, BEWi ASA, Alpek S A B de C V, SABIC Saudi Basic Industries Corporation, Synthos S A, Sunpor Kunststoff GmbH, Versalis S p A Eni Group, Ravago Group, TotalEnergies, Knauf Insulation, Hirsch Servo Group, Unipol Holland BV, StyroChem Finland Oy, BEWi Synbra Group, SIBUR, and NOVA Chemicals.

Europe Expanded Polystyrene Market Size

The Europe expanded polystyrene market size was valued at USD 2.42 billion in 2025 and is projected to reach USD 4.02 billion by 2034 from USD 2.56 billion in 2026, growing at a CAGR of 5.81%.

Expanded Polystyrene (EPS) is a lightweight, rigid, plastic foam insulation material produced from solid beads of polystyrene. This versatile polymer is characterized by its closed cell structure which provides exceptional thermal insulation shock absorption and moisture resistance. It is extensively utilized in the construction sector for insulating walls roofs and foundations as well as in packaging for protecting fragile goods during transit. The material’s low density and ease of molding build it indispensable for various industrial applications including automotive components and consumer electronics. As per Eurostat, the construction industest remains a vital part of the European economy, consistently contributing a substantial portion of the region’s total economic output and serving as a major driver for the insulation and building materials market. The push for energy efficient buildings under the European Green Deal has further amplified the demand for high performance insulation solutions. The International Energy Agency highlight that the building sector is the largest single energy consumer in the European Union, leading to robust policy initiatives aimed at enhancing energy performance through improved thermal efficiency and building envelope standards. Expanded polystyrene meets these requirements by offering a high R value per unit thickness. The European Environment Agency notes that waste management practices are evolving with increased focus on recycling plastics. This regulatory landscape influences the production and disposal methods of expanded polystyrene encouraging manufacturers to adopt circular economy principles. The market operates within a framework that balances economic efficiency with environmental stewardship ensuring that expanded polystyrene remains a relevant material in modern infrastructure and logistics.

MARKET DRIVERS

Stringent Energy Efficiency Regulations in Building Construction

The enforcement of strict energy efficiency standards is significantly boosting the growth of the Europe expanded polystyrene market. Governments are enforcing stricter building codes to reduce carbon emissions and enhance energy conservation in residential and commercial structures. The European Commission has established that all new construction must meet zero-emission standards by the start of the next decade, with even earlier deadlines for buildings owned or occupied by public authorities. This legislative requirement necessitates the utilize of high-quality insulation materials to minimize heat loss and reduce heating costs. Expanded polystyrene is favored due to its superior thermal conductivity and cost effectiveness compared to alternative insulation materials. As per the European Insulation Manufacturers Association the demand for insulation materials in Europe is projected to grow significantly as renovation rates increase to meet climate goals. The Renovation Wave strategy focutilizes on significantly increasing the pace of building energy upgrades, emphasizing the utilize of sustainable and circular construction materials to reduce the total carbon footprint of the built environment. Furthermore, the material’s durability and resistance to moisture ensure long term performance reducing the necessary for frequent replacements. The availability of expanded polystyrene in various densities allows architects and engineers to tailor insulation solutions to specific structural requirements. This adaptability combined with regulatory support creates a robust demand environment. The economic benefits of reduced energy bills also incentivize homeowners and property developers to invest in effective insulation systems. Consequently, the regulatory push towards sustainable construction practices directly correlates with increased adoption of expanded polystyrene in the European market.

Growth in E Commerce and Protective Packaging Demand

The rapid expansion of the e commerce sector in the region greatly fuels the demand for EPS in protective packaging applications, which in turn contributes to the development of the Europe expanded polystyrene market. The shift towards online shopping has increased the volume of goods transported requiring reliable and lightweight packaging solutions to prevent damage during transit. Eurostat data confirms that three-quarters of the European population now engage in digital shopping, illustrating the entrenched nature of e-commerce in consumer behavior. Expanded polystyrene is widely utilized for packaging electronics appliances and fragile items due to its excellent shock absorption properties and low weight. These characteristics support reduce shipping costs and minimize the carbon footprint associated with transportation. Ecommerce Europe emphasize that the digital retail sector is expanding across the continent, particularly through an increase in purchases created between different member states. This growth necessitates robust packaging materials that can withstand various handling conditions. Expanded polystyrene offers versatility in design allowing for custom molded inserts that secure products effectively. The material’s ability to maintain structural integrity under stress ensures that items arrive in pristine condition enhancing customer satisfaction. Additionally, the recyclability of expanded polystyrene packaging aligns with corporate sustainability goals as many retailers seek eco-friconcludely packaging options. The integration of recycled content into new packaging further supports this trconclude. The continuous rise in online retail activity thus sustains a steady demand for expanded polystyrene as a preferred packaging solution in the European logistics landscape.

MARKET RESTRAINTS

Restrictive Environmental Regulations on Single Use Plastics

Stringent environmental regulations tarobtaining single utilize plastics are restraining the growth of the Europe expanded polystyrene market. Policybuildrs are increasingly focapplying on reducing plastic waste and promoting sustainable alternatives which impacts the usage of expanded polystyrene in packaging and food service applications. According to the European Commission the Single Use Plastics Directive prohibits certain plastic products and sets reduction tarobtains for others including expanded polystyrene food containers. This legislation aims to mitigate the environmental impact of plastic pollution particularly in marine ecosystems. Eurostat indicates that while plastic packaging recycling rates have trconcludeed upward across the European Union, the total volume of waste generated continues to pose a significant logistical and ecological challenge. The low recycling rates of expanded polystyrene due to its bulkiness and contamination issues further exacerbate regulatory scrutiny. Many member states have implemented additional bans or taxes on expanded polystyrene products to encourage the adoption of biodegradable or reusable alternatives. These measures increase compliance costs for manufacturers and limit market access for traditional expanded polystyrene products. The shift in consumer preference towards eco-friconcludely materials also pressures companies to innovate or face declining sales. The regulatory uncertainty surrounding future restrictions creates hesitation in long term investment decisions. Companies must navigate a complex landscape of varying national laws which complicates supply chain management. The cumulative effect of these regulatory pressures restricts the growth potential of the expanded polystyrene market in applications prone to single utilize disposal.

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuations in the prices of raw materials such as styrene monomer and ongoing supply chain disruptions continue to hinder the growth of the European expanded polystyrene market. Styrene monomer is derived from benzene and ethylene which are petroleum-based commodities subject to global price volatility. According to the International Energy Agency crude oil prices experienced significant fluctuations in recent years due to geopolitical tensions and supply constraints. These price instabilities directly impact the production costs of expanded polystyrene squeezing profit margins for manufacturers. As per Eurostat producer prices for chemicals in the European Union increased notably in 2022 and 2023 driven by higher energy and feedstock costs. The reliance on imported raw materials exposes the market to currency exmodify rate risks and logistical bottlenecks. Supply chain disruptions cautilized by port congestion labor strikes or transportation delays can lead to shortages and production stoppages. The energy intensive nature of expanded polystyrene production further amplifies the impact of rising electricity and natural gas prices. Manufacturers struggle to pass on these increased costs to customers who are sensitive to price modifys. The unpredictability of input costs complicates budobtaining and strategic planning for industest participants. Additionally, the transition to renewable energy sources while beneficial long term introduces short term operational challenges. These economic pressures hinder the competitiveness of European producers against global counterparts with lower cost structures. The cumulative effect of raw material volatility and supply chain instability restrains market expansion and profitability.

MARKET OPPORTUNITIES

Advancements in Recycling Technologies and Circular Economy Initiatives

The development of advanced recycling technologies and circular economy initiatives offers a major opening for the Europe expanded polystyrene market. Innovations in chemical and mechanical recycling processes enable the conversion of waste expanded polystyrene into high quality raw materials for new products. According to Plastics Europe the recycling rate for plastics in Europe is improving with increased investment in infrastructure and technology. Chemical recycling methods such as depolymerization allow for the recovery of styrene monomer from waste expanded polystyrene which can be reutilized in production. This closed loop approach reduces reliance on virgin fossil fuels and lowers the environmental footprint of the material. As per the European Commission the Circular Economy Action Plan promotes the design of recyclable products and the development of markets for secondary raw materials. Companies that adopt these technologies can differentiate themselves by offering sustainable solutions to environmentally conscious customers. Partnerships with waste management firms and retailers facilitate the collection and processing of post-consumer expanded polystyrene. The creation of certified recycled content products opens up new market segments in construction and packaging. Regulatory incentives for applying recycled materials further support this transition. By embracing circular economy principles manufacturers can mitigate regulatory risks and enhance brand reputation. The growing demand for sustainable materials in green building certifications also drives the adoption of recycled expanded polystyrene. This shift towards sustainability offers a pathway for long term growth and resilience in the European market.

Expansion into Lightweight Automotive and Aerospace Applications

The expansion of EPS into lightweight automotive and aerospace applications paves the way for the growth of the Europe expanded polystyrene market. The automotive industest is increasingly focapplying on vehicle lightweighting to improve fuel efficiency and reduce emissions. According to the European Automobile Manufacturers Association the average weight of vehicles has increased over the years prompting manufacturers to seek lightweight materials for interior components and packaging. Expanded polystyrene and its variants are utilized in headliners door panels and shock absorbing structures due to their high strength to weight ratio. As per the International Air Transport Association the aerospace sector is also prioritizing weight reduction to enhance fuel efficiency and lower operational costs. Expanded polystyrene composites are utilized in non-structural interior parts and protective packaging for sensitive aircraft components. The material’s ability to absorb energy builds it ideal for safety applications. Advances in manufacturing techniques allow for the production of complex shapes with precise tolerances meeting the stringent requirements of these industries. The shift towards electric vehicles further amplifies the necessary for lightweight materials to extconclude battery range. Collaborations between material suppliers and automotive manufacturers drive innovation in product development. The adoption of expanded polystyrene in these high value sectors diversifies revenue streams and reduces depconcludeence on traditional construction and packaging markets. This strategic expansion leverages the material’s inherent properties to meet the evolving necessarys of modern transportation industries.

MARKET CHALLENGES

Complexity of Waste Management and Collection Logistics

The complexity of waste management and collection logistics constitutes a major barrier to the Europe expanded polystyrene market. The bulky nature of expanded polystyrene waste builds it difficult and costly to collect transport and store. According to research, the low density of expanded polystyrene means that large volumes are required to achieve significant weight resulting in inefficient utilize of transportation capacity. This logistical challenge increases the carbon footprint associated with waste management and reduces the economic viability of recycling programs. Many municipalities lack the specialized equipment necessaryed to compact or process expanded polystyrene efficiently leading to limited collection services. The lack of standardized collection systems across different European countries creates inconsistencies in recycling rates and material quality. Consumers often lack awareness about proper disposal methods leading to improper waste segregation. The high costs associated with logistics and processing discourage investment in recycling infrastructure. Without efficient collection systems the potential for circular economy initiatives is hindered. Manufacturers face pressure to address these logistical barriers through innovative packaging designs or take back schemes. The inability to establish a seamless waste management framework restricts the sustainability credentials of expanded polystyrene and limits its market acceptance in environmentally regulated regions.

Competition from Alternative Insulation and Packaging Materials

Intense competition from alternative insulation and packaging materials is a significant challenge to the Europe expanded polystyrene market. Materials such as mineral wool cellulose fiber and polyurethane foam offer comparable or superior thermal performance and fire resistance properties. Mineral wool for instance is non-combustible and provides better soundproofing building it preferred in certain residential and commercial applications. In the packaging sector biodegradable materials such as molded pulp and cornstarch-based foams are gaining traction due to their compostability and lower environmental impact. These alternatives appeal to eco conscious consumers and businesses aiming to reduce their plastic footprint. The perception of expanded polystyrene as a non-biodegradable pollutant further disadvantages it in competitive bidding processes. Manufacturers of alternative materials often benefit from government subsidies and incentives promoting green technologies. The continuous innovation in bio-based materials enhances their performance and cost competitiveness. Expanded polystyrene producers must invest in research and development to improve the sustainability profile of their products. Failure to differentiate effectively against these alternatives may result in market share erosion. The dynamic competitive landscape requires constant adaptation to maintain relevance in both construction and packaging sectors.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.81% |

|

Segments Covered |

By Product Type, End User Industest, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

BASF SE, BEWi ASA, Alpek S.A.B. de C.V., SABIC (Saudi Basic Industries Corporation), Synthos S.A., Sunpor Kunststoff GmbH, Versalis S.p.A. (Eni Group), Ravago Group, TotalEnergies, Knauf Insulation, Hirsch Servo Group, Unipol Holland BV, StyroChem Finland Oy, BEWi Synbra Group, SIBUR, NOVA Chemicals |

SEGMENTAL ANALYSIS

By Product Type Insights

The white EPS segment captured the majority share of the Europe expanded polystyrene market in 2025. This supremacy of the segment is largely attributed to its extensive application in general construction insulation and standard packaging solutions where cost efficiency and versatility are paramount. The primary factor fueling this leadership is the widespread adoption of white EPS in external thermal insulation composite systems which are mandated by energy efficiency regulations across the European Union. The material’s ease of installation and compatibility with various rconcludeering systems build it the preferred choice for contractors working on large scale hoapplying projects. Furthermore, the packaging industest relies heavily on white EPS for protecting consumer goods appliances and food items during transportation. The high-volume production capabilities of white EPS manufacturers ensure consistent supply and competitive pricing which reinforces its market leadership. The established recycling infrastructure for white EPS in many European countries also supports its continued utilize as stakeholders seek to improve circularity metrics. The combination of regulatory support for building insulation and the relentless growth of e commerce packaging ensures that white EPS remains the cornerstone of the expanded polystyrene market in Europe.

The Gray and Silver EPS segment is estimated to register the quickest CAGR of 5.4% from 2026 to 2034 due to the increasing demand for high performance insulation in energy efficient buildings. This rapid growth is attributed to the superior thermal conductivity of gray and silver EPS which contains graphite or other infrared reflecting additives that enhance insulation properties by up to 20 percent compared to standard white EPS. The primary driver is the stringent requirement for thinner insulation layers in urban construction projects where space optimization is critical. Gray and silver EPS allow architects to achieve required U values with reduced wall thickness thereby maximizing usable floor area. Additionally, the growing preference for premium insulation solutions in commercial real estate and luxury residential developments supports the expansion of this segment. Developers are willing to pay a premium for gray EPS due to its long-term energy savings and enhanced sustainability credentials. The integration of these advanced materials into prefabricated construction modules further accelerates their adoption. As energy costs remain volatile the economic argument for high efficiency insulation strengthens driving the quickest growth rates in the gray and silver EPS category.

By End User Industest Insights

The Building and Construction conclude utilizer segment led the Europe expanded polystyrene market by accounting for a significant share in 2025. This leading position of the segment is supported by the mandatory implementation of energy efficiency directives and the extensive utilize of EPS in insulation systems for walls roofs and floors. The main reason for this growth is the European Green Deal which sets ambitious tarobtains for reducing greenhoutilize gas emissions from the building sector. Expanded polystyrene is favored due to its lightweight nature ease of handling and excellent thermal resistance which contributes to lower heating and cooling demands. The durability of EPS ensures that insulation performance remains stable over the lifespan of the building reducing maintenance costs. Furthermore, the material’s moisture resistance prevents mold growth and structural damage enhancing indoor air quality and building longevity. The availability of EPS in various forms including boards and blocks allows for flexible application in both new constructions and retrofitting projects. Government subsidies and tax incentives for energy efficient renovations further stimulate demand. The alignment of EPS properties with sustainable building certifications such as BREEAM and LEED reinforces its position as the material of choice for contractors and developers aiming to meet regulatory and environmental standards.

The packaging conclude utilizer segment is anticipated to witness the quickest CAGR of 4.8% over the forecast period owing to the booming e commerce industest and the necessary for protective shipping solutions. This accelerated growth is also driven by the increasing volume of online retail transactions which require lightweight and durable packaging to prevent product damage during transit. Expanded polystyrene is widely utilized for packaging electronics houtilizehold appliances and perishable food items due to its exceptional shock absorption and thermal insulation properties. The lightweight nature of EPS reduces shipping weights and associated carbon emissions aligning with corporate sustainability goals. Additionally, advancements in recycled EPS packaging solutions are addressing environmental concerns building it more acceptable to eco conscious consumers and retailers. The food delivery sector also contributes to this growth as EPS containers maintain temperature integrity for hot and cold meals. The versatility of EPS allows for custom molded designs that secure irregularly shaped items effectively. As logistics networks expand and consumer expectations for safe delivery increase the demand for high performance packaging materials like EPS continues to surge outpacing other conclude utilizer segments.

REGIONAL ANALYSIS

Germany Expanded Polystyrene Market Analysis

Germany dominated the Europe expanded polystyrene market and occupied a 19.4% share in 2025. The demand for EPS in Germany is fuelled by its strong construction industest and rigorous energy efficiency standards. The countest’s market reveals high demand for insulation materials in both new builds and extensive renovation programs aimed at reducing carbon emissions. The key reason behind this growth is the German government’s Building Energy Act which mandates strict energy performance levels for residential and commercial properties. Also, the prevalence of external thermal insulation composite systems in German architecture further solidifies the demand for high quality EPS boards. The countest’s robust manufacturing base ensures a steady supply of EPS products meeting diverse application necessarys. Additionally, the packaging sector in Germany utilizes EPS extensively for industrial goods and consumer electronics reflecting the nation’s export-oriented economy. Regulatory frameworks promoting circular economy practices encourage the recycling of EPS waste enhancing its sustainability profile. The combination of policy support technological advancement and industrial capacity positions Germany as the central hub for EPS consumption in Central Europe.

France Expanded Polystyrene Market Analysis

France was the next prominent market for expanded polystyrene in Europe and captured a 14.3% share in 2025. This expansion of the French market is driven by its ambitious climate goals and active hoapplying market. The market in France reveals substantial investment in thermal renovation of existing buildings particularly in urban areas where energy efficiency is a priority. A primary driving factor is the MaPrimeRénov scheme which provides financial incentives to homeowners for installing high performance insulation materials. The French construction sector favors EPS for its cost effectiveness and ease of installation in multi-story residential buildings. Besides, the packaging industest in France also contributes to market growth with EPS being utilized for food transport and protective packaging for luxury goods. The countest’s focus on reducing plastic waste has led to improvements in EPS recycling infrastructure building it more sustainable. French manufacturers are increasingly producing gray EPS to meet higher insulation standards required by new building codes. The integration of EPS into sustainable construction practices and the strong regulatory support for energy renovation ensure that France remains a pivotal market for expanded polystyrene in Western Europe.

Italy Expanded Polystyrene Market Analysis

Italy holds a significant position in the Europe expanded polystyrene market becautilize of its seismic retrofitting initiatives and tourism related construction. The market status is characterized by a strong demand for lightweight insulation materials that do not add significant load to older structures. A key aspect supporting the countest’s market is the Superbonus tax credit scheme which although modified has stimulated extensive renovation activities including thermal insulation upgrades. The material’s flexibility and light weight build it ideal for improving the energy efficiency of historic buildings without compromising structural integrity. In addition, the tourism sector also drives demand for EPS in packaging for food and beverage distribution particularly in coastal regions. Italy’s warm climate increases the necessary for cooling efficiency further boosting the adoption of thermal insulation. The presence of local EPS producers ensures timely supply and customization for specific architectural requirements. The combination of regulatory incentives and climatic necessarys sustains a robust market for expanded polystyrene in Italy.

United Kingdom Expanded Polystyrene Market Analysis

The United Kingdom expanded steadily in the Europe expanded polystyrene market due to its hoapplying shortage and energy security concerns. The market status is defined by a strong emphasis on reducing energy bills through improved home insulation driven by volatile energy prices. A major driving factor is the UK government’s commitment to upgrading the energy efficiency of homes to meet net zero tarobtains by 2050. The material is widely utilized in cavity wall insulation and external wall systems due to its proven performance and affordability. Moreover, the packaging sector in the UK also utilizes EPS extensively for e commerce and food delivery services reflecting the countest’s high online shopping rates. Regulatory modifys regarding fire safety have led to stricter guidelines for EPS usage in high rise buildings but low-rise residential applications remain strong. The UK’s focus on practical and cost-effective energy solutions ensures continued demand for expanded polystyrene in the residential sector.

Spain Expanded Polystyrene Market Analysis

Spain is predicted to expand significantly in the European market from 2026 to 2034 owing to its tourism infrastructure and climate adaptation strategies. The market status is characterized by significant utilize of EPS in hotel construction and residential developments in coastal regions where thermal comfort is essential. A key driving factor is the necessary for effective insulation against high summer temperatures which reduces air conditioning loads and energy consumption. EPS is favored for its ability to provide thermal inertia keeping interiors cool during hot weather. Also, the material’s moisture resistance builds it suitable for humid coastal environments. Government initiatives promoting energy efficiency in buildings further support the adoption of EPS insulation. The growth of renewable energy projects also utilizes EPS for protective casing and insulation components. Spain’s unique climatic conditions and economic drivers create a distinct market dynamic for expanded polystyrene focapplying on cooling efficiency and protective packaging.

COMPETITIVE LANDSCAPE

The competition in the Europe expanded polystyrene market is characterized by a mix of large multinational chemical companies and specialized regional producers. Market leaders compete on the basis of product quality sustainability credentials and technological innovation. The presence of established brands creates high barriers to entest for new competitors due to significant capital requirements and regulatory compliance costs. Competitive dynamics are influenced by the availability of raw materials and energy prices which impact production costs. Companies differentiate themselves through advanced recycling capabilities and the development of eco-friconcludely EPS variants. Price competition is moderate as customers prioritize performance and reliability over lowest cost. Strategic alliances with downstream industries strengthen market positions and ensure stable demand. The shift towards sustainable construction and packaging drives innovation and collaboration among market participants. Regulatory frameworks play a crucial role in shaping competitive landscapes by setting standards for environmental performance. Companies that adapt quickly to altering regulations and consumer preferences gain a competitive advantage. The market sees continuous investment in research and development to improve product properties and reduce environmental impact. Overall, the competitive environment encourages efficiency innovation and sustainability driving the evolution of the expanded polystyrene industest in Europe.

KEY MARKET PLAYERS

Some of the notable key players in the Europe expanded polystyrene market are

- BASF SE

- BEWi ASA

- Alpek S.A.B. de C.V.

- SABIC (Saudi Basic Industries Corporation)

- Synthos S.A.

- Sunpor Kunststoff GmbH

- Versalis S.p.A. (Eni Group)

- Ravago Group

- TotalEnergies

- Knauf Insulation

- Hirsch Servo Group

- Unipol Holland BV

- StyroChem Finland Oy

- BEWi Synbra Group

- SIBUR

- NOVA Chemicals

Top Players in the Market

- BASF SE is a leading chemical producer that significantly influences the Europe expanded polystyrene market through its Styropor brand. The company provides high quality EPS solutions for construction insulation and packaging applications globally. BASF focutilizes on sustainability by developing recycled content EPS and improving production efficiency to reduce carbon emissions. Recent actions include expanding its circular economy initiatives and partnering with value chain stakeholders to enhance EPS recycling infrastructure. The company invests in research and development to create innovative insulation materials that meet stringent energy efficiency standards. BASF leverages its global network to supply consistent quality products while adapting to regional regulatory requirements. Their commitment to digitalization optimizes supply chain operations and customer service. By promoting the benefits of EPS in sustainable construction BASF strengthens its market position. The company actively engages in industest associations to advocate for responsible plastic utilize and advanced recycling technologies ensuring long term viability.

- Synthos S.A. is a major polymer manufacturer in Central Europe with a strong presence in the expanded polystyrene sector. The company produces a wide range of EPS grades for construction and packaging industries under the Synthos Green Energy initiative. Synthos is dedicated to reducing the environmental impact of its operations by increasing the utilize of renewable energy sources in production. Recent strategies involve launching bio-based EPS products and enhancing recycling capabilities to support circular economy goals. The company expands its production capacity to meet growing demand for energy efficient insulation materials in Europe. Synthos collaborates with customers to develop customized solutions that improve thermal performance and sustainability. Their focus on innovation drives the creation of lighter and more durable EPS variants. By prioritizing environmental stewardship and operational excellence Synthos reinforces its competitive edge. The company’s extensive distribution network ensures reliable supply across European markets supporting diverse industrial necessarys.

- Knauf Industries is a key player in the Europe expanded polystyrene market specializing in technical foam solutions for automotive construction and packaging. The company leverages its expertise in material science to deliver high performance EPS products that meet specific customer requirements. Knauf Industries emphasizes sustainability by integrating recycled materials into its production processes and designing eco-friconcludely packaging solutions. Recent actions include investing in advanced manufacturing technologies to improve product quality and reduce waste. The company partners with automotive manufacturers to develop lightweight components that enhance fuel efficiency. Knauf Industries also expands its recycling facilities to close the loop on EPS waste. Their commitment to innovation leads to the development of novel applications for EPS in various industries. By focapplying on customer centric solutions and sustainable practices Knauf Industries strengthens its market presence. The company’s global reach and local expertise enable it to respond effectively to regional market dynamics and regulatory modifys.

Top Strategies Used by Key Market Participants

Key players in the Europe expanded polystyrene market primarily focus on sustainability and circular economy initiatives to address environmental concerns and regulatory pressures. Companies invest heavily in recycling technologies to increase the utilize of post-consumer recycled content in new EPS products. Product innovation is a central strategy with firms developing high performance gray and silver EPS grades that offer superior thermal insulation. Strategic partnerships with construction firms and packaging utilizers support secure long-term contracts and drive adoption. Expansion into emerging applications such as lightweight automotive components diversifies revenue streams. Digitalization of supply chains enhances operational efficiency and responsiveness to market demands. Compliance with strict environmental regulations is maintained through continuous improvement in production processes and emission controls. Companies also engage in advocacy efforts to promote the benefits of EPS and support favorable policy frameworks. These strategies enable participants to maintain competitiveness and achieve sustainable growth in the European region.

MARKET SEGMENTATION

This research report on the European expanded polystyrene market has been segmented and sub-segmented based on categories.

By Product Type

- White EPS

- Gray and Silver EPS

By End User Industest

- Building and Construction

- Electrical and Electronics

- Packaging

- Other End-utilizer Industries

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply