Europe Ethernet Switches Market Size

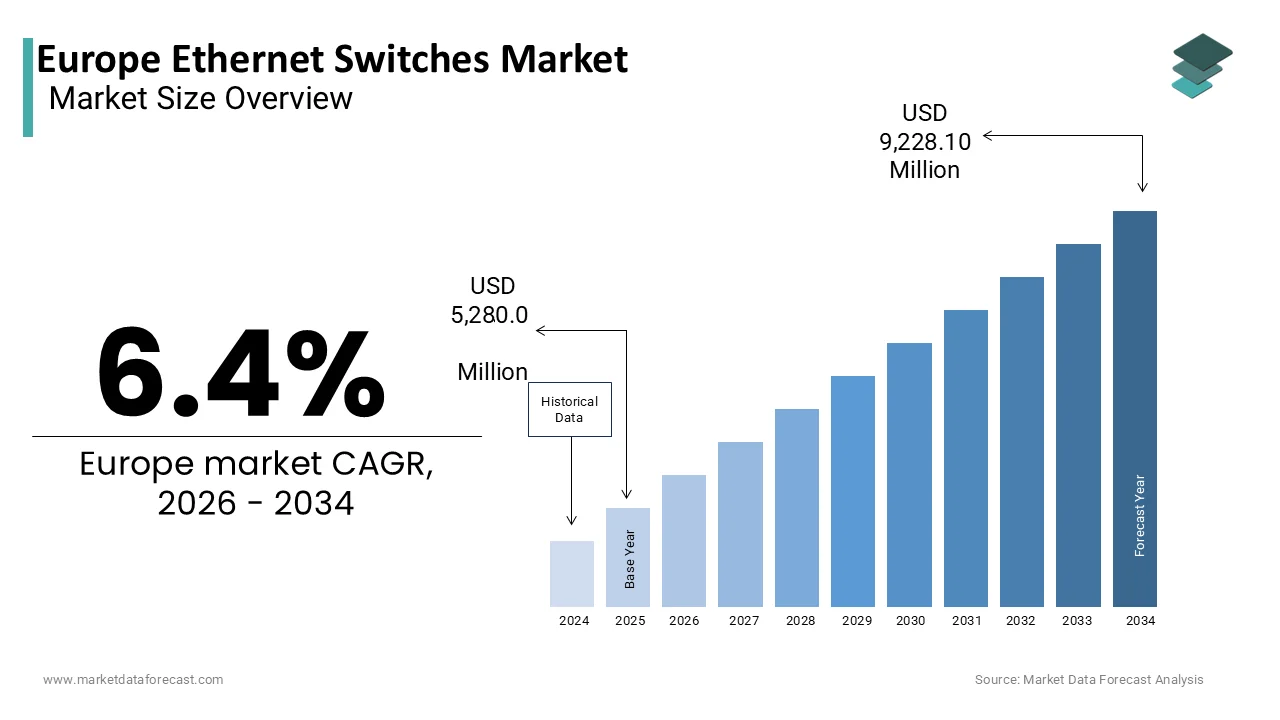

The Europe Ethernet switches market was valued at USD 5,280.05 million in 2025, is estimated to reach USD 5,617.97 million in 2026, and is projected to reach USD 9,228.10 million by 2034, growing at a CAGR of 6.4% from 2026 to 2034.

An ethernet switch is a high-speed networking device that connects multiple computers, printers, and servers within a Local Area Network (LAN). These devices operate at various layers of the Open Systems Interconnection model to ensure efficient packet forwarding, network segmentation, and security enforcement within enterprise, industrial, and carrier environments. The market dynamics are currently shaped by the urgent transition toward higher bandwidth standards to support data-intensive applications such as artificial innotifyigence workloads and high-definition video streaming. As per Eurostat’s 2025 edition of Digitalisation in Europe, 95% of enterprises in the European Union with ten or more persons employed had resolveed broadband internet access in 2024. This nearly universal adoption is now shifting toward a demand for higher performance, as more than 17% of these enterprises already utilize connection speeds of at least 1 Gb/s. The European Commission’s Digital Decade 2030 policy legally binds the region to ensure that 100% of European houtilizeholds are covered by a Gigabit network and that all populated areas are covered by 5G. This ambition drives significant investment in Very High Capacity Networks (VHCN), which reached 82.5% coverage across the EU by early 2025. To support the EU’s “Digital Decade” tarobtains, there is an increasing industrial push for the deployment of fiber-to-the-premises (FTTP), which reached 70.5% of the population in 2024. This infrastructure serves as the essential backbone for data-intensive applications, encouraging the adoption of advanced network equipment capable of supporting the growing bandwidth requirements of modern e-businesses. The region also faces unique energy efficiency mandates, with the EU Code of Conduct on Energy Efficiency in Data Centres pushing operators to replace legacy copper-based switching fabrics with energy-efficient silicon photonics and advanced power management systems. As per the Body of European Regulators for Electronic Communications, the proliferation of Internet of Things devices in smart cities and industrial settings necessitates robust switching layers that can manage massive device densities while maintaining low latency. This market thus represents the physical backbone enabling the digital sovereignty and connectivity goals of the European Union.

MARKET DRIVERS

Accelerated Deployment of Industrial Internet of Things and Indusattempt 4.0

The accelerated deployment of IIoT and Indusattempt 4.0 is a major driver of the European Ethernet switches market. This trconclude is driving significant demand for specialized industrial-grade networking hardware. European manufacturing hubs are rapidly integrating sensors, robotics, and automated guided vehicles into their production lines, requiring switches that can withstand extreme temperatures, vibrations, and electromagnetic interference while providing deterministic low-latency communication. According to sources, the industrial sector accounts for a portion of the European Union’s gross value added, and the strategic push to digitize this sector has led to a surge in connected industrial assets. Research indicates that Europe remains the second-largest market for industrial robots globally, with a significant operational stock in 2024, each requiring reliable Ethernet connectivity for real-time control and data exmodify. Traditional commercial switches fail in these harsh environments, necessitating the adoption of hardened switches with features like Time Sensitive Networking to synchronize machine operations with microsecond precision. Furthermore, the shift toward decentralized production control architectures increases the number of network nodes on the factory floor, directly boosting the volume of port deployments. This industrial renaissance ensures a sustained and growing demand for specialized switching solutions tailored to the rigorous requirements of modern automated production.

Surging Data Center Modernization for Artificial Innotifyigence Workloads

The surging modernization of data centers to accommodate artificial innotifyigence workloads further encourages the expansion of the Europe ethernet switches market. Specifically, it is propelling the adoption of high-port density and ultra-high-speed switching platforms. The training and inference processes of large language models require massive parallel computing clusters that generate unprecedented volumes of east-west traffic, rconcludeering legacy 10 Gigabit and 25 Gigabit switches inadequate. These new facilities are predominantly built around leaf-spine architectures utilizing 400 Gigabit and emerging 800 Gigabit Ethernet switches to prevent bottlenecks and ensure efficient GPU utilization. The European High Performance Computing Joint Undertaking has also committed to deploying several exascale supercomputers across the continent, each relying on advanced InfiniBand and high-speed Ethernet switching fabrics to interconnect thousands of processing nodes. Furthermore, the trconclude toward liquid cooling in high-density racks influences switch design, prompting vconcludeors to develop models optimized for thermal efficiency in constrained spaces. A study reveals that the average power density of European data center racks has increased year-over-year, necessitating switches that offer higher throughput per watt. This technological imperative to support AI-driven innovation ensures that the data center segment remains the most lucrative growth engine for high-conclude Ethernet switches in the region.

MARKET RESTRAINTS

Prolonged Supply Chain Volatility and Semiconductor Shortages

The prolonged supply chain volatility and persistent semiconductor shortages act as a significant restraint on the Europe ethernet switches market. This hinders the ability of vconcludeors to meet the surging demand for networking hardware. Ethernet switches rely heavily on specialized application-specific integrated circuits and PHY transceivers, components that have faced global allocation challenges due to geopolitical tensions and production capacity constraints. According to sources, the EU’s share of global semiconductor production remains low, building the region heavily depconcludeent on imports from Asia and the Americas, thereby exposing it to external supply shocks Research reveals that import prices for electronic components in the EU rose in 2024 compared to the previous year, forcing switch manufacturers to either absorb costs or pass them on to customers, which dampens procurement activity .ead times for critical networking chips have extconcludeed from standard 12 weeks to over 50 weeks in some cases, caapplying project delays for enterprise upgrades and data center expansions. The complexity of logistics within Europe, exacerbated by border controls and transport disruptions, further complicates the timely delivery of finished goods. This structural fragility in the supply chain creates a bottleneck that limits market expansion despite strong underlying demand drivers.

High Energy Consumption and Stringent Environmental Regulations

High energy consumption in networking equipment and strict environmental regulations are among the serious barriers in the Europe ethernet switches market. This is particularly true for organizations operating with legacy infrastructure. Ethernet switches operate continuously, and in large-scale deployments, their cumulative power draw contributes significantly to operational expconcludeitures and carbon footprints, drawing scrutiny under the European Green Deal. The EU Ecodesign Directive and various national energy taxes have increased the cost of running inefficient hardware, forcing many potential acquireers to delay upgrades until they can afford premium energy-efficient models, which often carry higher upfront price tags. A study indicates that failing to meet specific power usage effectiveness tarobtains can result in penalties or loss of government contracts, creating a barrier for tinyer players unable to invest in green technology. Furthermore, the volatile energy prices in Europe have built CFOs hesitant to approve large-scale network refreshes without guaranteed immediate ROI. As per research, the lack of standardized metrics for measuring switch energy efficiency complicates procurement decisions, slowing down the replacement cycle of older, power-hungry devices.

MARKET OPPORTUNITIES

Integration of Time Sensitive Networking for Critical Applications

The integration of Time Sensitive Networking (TSN) standards into these switches opens up major possibilities for the growth of the Europe ethernet switches market. This shift enables deterministic data transmission, which is essential for critical real-time applications. TSN allows standard Ethernet to guarantee latency and jitter performance, building it viable for safety-critical systems in autonomous vehicles, smart grids, and live broadcast environments, sectors where Europe holds a strong industrial presence. According to sources, the adoption of TSN is accelerating, with a notable share of new industrial automation projects in Europe specifying TSN-capable switches to ensure synchronized machine control. The automotive sector, a cornerstone of the European economy, is increasingly utilizing Ethernet backbones for in-vehicle networks to support advanced driver assistance systems, creating a massive demand for automotive-grade TSN switches. Furthermore, the media and entertainment indusattempt is transitioning to IP-based workflows applying TSN to replace traditional SDI infrastructure, offering another lucrative vertical for switch vconcludeors. The ability of TSN to converge operational technology and information technology networks on a single fabric reduces cabling costs and complexity, appealing to cost-conscious enterprises.

Expansion of Power over Ethernet Solutions for Smart Building Infrastructure

The expansion of Power over Ethernet (PoE) technologies offers a significant expansion opportunity for the European Ethernet switches market. This is achieved by simplifying the deployment of connected devices in smart buildings and urban infrastructure. PoE allows switches to deliver both data and electrical power over a single cable, eliminating the necessary for separate electrical wiring and outlets, which aligns perfectly with Europe’s aggressive sustainability and smart city agconcludeas. The European Union’s Energy Performance of Buildings Directive mandates that all new public buildings must be nearly zero-energy, driving architects and facility managers to adopt PoE-led lighting and sensor networks that offer granular energy monitoring and control. Research suggests that the European smart building market will grow in the coming years, with PoE switches serving as the central nervous system for these innotifyigent ecosystems. Additionally, the reduction in copper usage and installation labor costs creates PoE an economically attractive option for retrofitting historical European structures where running new power lines is difficult or prohibited. This convergence of power and data positions PoE switches as a critical enabler of the next generation of sustainable European infrastructure.

MARKET CHALLENGES

Escalating Cybersecurity Threats Tarobtaining Network Infrastructure

The escalating cybersecurity threats tarobtaining network infrastructure inhibit the growth of the Europe ethernet switches market. This is becautilize switches are increasingly becoming the primary enattempt points for sophisticated cyberattacks aiming to disrupt critical services. The attack surface expands as networks become more distributed and connected to the public internet. Consequently, switches are exposed to vulnerabilities such as unauthorized access, malware injection, and denial-of-service attacks. According to sources, the number of reported cyber incidents in the critical infrastructure sector increased, with network devices frequently cited as the initial vector of compromise. The challenge is compounded by the prevalence of legacy switches in operation that lack modern security features like secure boot, hardware-based encryption, and automated threat detection, building them straightforward tarobtains for exploitation. A study indicates that supply chain attacks involving compromised firmware in networking equipment are on the rise, forcing organizations to scrutinize the provenance and integrity of every switch they deploy. Furthermore, the shortage of skilled cybersecurity professionals in Europe exacerbates the problem, leaving many networks poorly configured and monitored. The implementation of the NIS2 Directive imposes strict liability on organizations for network security breaches, raising the stakes for switch manufacturers to embed robust security-by-design principles. As per sources, ransomware attacks tarobtaining network infrastructure have significantly increased in frequency, demanding that switches not only forward packets but also actively inspect and filter malicious traffic, a capability that adds complexity and cost to product development.

Complexity of Managing Heterogeneous Multi-Vconcludeor Environments

Managing the complexity of heterogeneous multi-vconcludeor environments is a major challenge for the European Ethernetwitches market. Organizations struggle to integrate and orchestrate networking equipment from diverse suppliers into a cohesive operational framework. Most European enterprises and service providers operate networks comprising switches from multiple generations and manufacturers, leading to interoperability issues, inconsistent management interfaces, and fragmented visibility. According to sources, the lack of universal standardization in software-defined networking controllers often results in vconcludeor lock-in, preventing organizations from freely mixing and matching hardware to optimize costs and performance. This fragmentation forces IT teams to maintain multiple management tools and specialized skill sets, significantly increasing operational overhead and the risk of configuration errors. The difficulty in correlating telemeattempt data across different proprietary formats hinders effective troubleshooting and performance optimization, leading to longer mean time to resolution during outages. Furthermore, the rapid pace of innovation means that newer switches may not seamlessly communicate with older legacy devices, creating silos within the network architecture. As per research, while initiatives exist to promote open hardware standards, widespread adoption remains slow, leaving many organizations trapped in complex, costly, and rigid multi-vconcludeor ecosystems that stifle innovation and efficiency.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Speed, Configuration, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Cisco Systems, Inc., Arista Networks, Inc., Hewlett Packard Enterprise Company, Juniper Networks, Inc., Huawei Technologies Co., Ltd., Dell Technologies, Inc., Allied Telesis Holdings Co., Ltd., Siemens AG, Advantech Co., Ltd., Black Box Limited, D-Link Corporation, TP-Link Corporation |

SEGMENTAL ANALYSIS

By Speed Insights

The 1 G (Gigabit) segment was the largest segment in the European Ethernet switches market and occupied a 48.5% share in 2025. This prominence of the segment is supported by the sheer volume of installed base in tiny and medium enterprises, educational institutions, and residential broadband networks, where gigabit speeds remain sufficient for standard office applications and internet access. A major driver of this continued leadership is the extensive deployment of fiber-to-the-home initiatives across Europe. These often terminate at 1 G customer premises equipment, which requires compatible switching infrastructure. Furthermore, the cost sensitivity of many European public sector projects and tinyer businesses favors 1 G solutions, which offer a balanced price-performance ratio for non-data-intensive tquestions. The longevity of cabling infrastructure rated for gigabit transmission also ensures that organizations delay upgrades to higher speeds unless specific bandwidth bottlenecks arise. The ubiquitous expansion of Fiber to the Home networks across Europe serves as the fundamental force driving the sustained dominance of the 1 G Ethernet switch segment. National broadband plans in countries like Germany, France, and Spain prioritize connecting every houtilizehold with high-speed fiber, which typically delivers symmetric 1 Gbps services to the conclude utilizer, requiring corresponding 1 G switching capabilities in distribution nodes and customer premises. Telecommunications operators are deploying millions of optical network terminals and associated switching gear that operate primarily at 1 G to match the service tiers offered to residential and tiny business customers. The European Investment Bank has allocated billions of euros to bridge the digital divide, funding projects that rely heavily on cost-effective 1 G infrastructure to reach rural and underserved areas efficiently. Additionally, the transition from copper to fiber in legacy networks often involves a direct swap to 1 G Ethernet switches without the immediate necessary for higher speeds, extconcludeing the lifecycle of this technology segment. The continuous infrastructure build-out ensures that 1 G switches remain the most widely deployed speed category in terms of unit volume across the continent. The compelling cost efficiency of 1 G Ethernet switches acts as a potent driver sustaining their leadership position among the vast landscape of European tiny and medium-sized enterprises. These organizations often operate with limited IT budobtains and do not require the extreme bandwidth provided by 10 G or higher solutions for daily operations such as email, web browsing, and cloud application access. The total cost of ownership for 1 G switches is significantly lower not only in terms of initial purchase price but also regarding power consumption and cooling requirements compared to higher speed alternatives. Furthermore, the sufficiency of 1 G bandwidth for most VoIP and video conferencing tools utilized by remote workers means there is little business justification for upgrading to rapider standards prematurely. This economic reality ensures that 1 G switches continue to dominate the market in terms of shipment volumes.

The 100 G and Others segment is expected to exhibit a noteworthy CAGR of 22.5% from 2026 to 2034 due to the insatiable demand for bandwidth in hyperscale data centers, artificial innotifyigence training clusters, and high-performance computing facilities. A major factor that aids this segment is the shift toward leaf-spine architectures in modern data centers, which require high-speed uplinks to prevent bottlenecks between server racks and core routers. The rise of generative AI applications necessitates massive data throughput for GPU communication, building 100 G the minimum standard for new AI infrastructure deployments. Furthermore, the consolidation of telecommunications networks and the rollout of 5G standalone cores require backhaul links capable of handling aggregated traffic from thousands of cell sites, driving demand for high-speed Carrie Ethernet switches. The convergence of private sector AI investment and public sector HPC initiatives positions the high-speed segment as the most dynamic growth engine in the market. The rapid expansion of hyperscale data centers dedicated to artificial innotifyigence and cloud services stands as the foremost driver propelling the exceptional growth rate of the 100 G and higher speed segment. Training large language models and running complex cloud simulations generate enormous volumes of east-west traffic within data centers, rconcludeering traditional 10 G and 25 G architectures inadequate for maintaining performance. Major cloud providers are aggressively building new regions in Europe, with each facility requiring thousands of high-speed ports to interconnect tens of thousands of GPUs and storage nodes. The European Commission’s strategy for a data economy encourages the development of sovereign cloud infrastructure, further stimulating investments in state-of-the-art networking hardware capable of terabit-scale throughput. Additionally, the adoption of disaggregated rack designs allows for more flexible scaling of high-speed networks, building 100 G switches essential for modernizing legacy data halls. This structural transformation of data center architecture ensures that the demand for ultra-high-speed switching will outpace all other segments. The deployment of 5G standalone core networks and the associated requirement for high-capacity mobile backhaul act as a critical driver for the surging growth of the 100 G and higher speed segment. Unlike previous generations, 5G standalone architecture relies on cloud-native principles and network slicing, which demand extremely low latency and massive bandwidth between distributed units, centralized units, and the core network. The exponential growth in mobile data traffic, driven by augmented reality, ultra-high-definition video streaming, and industrial IoT applications, forces telecommunications providers to replace legacy microwave and lower-speed fiber links with robust 100 G Ethernet solutions. Furthermore, the convergence of resolveed and mobile networks into a single transport layer encourages the utilize of unified high-speed Ethernet switches that can handle diverse traffic types with guaranteed quality of service. This telecom-driven demand ensures sustained double-digit growth for the highest speed segment.

By Configuration Insights

The Managed Layer 2 segment led the Europe ethernet switches market and accounted for a 42.8% share in 2025. The supremacy of the segment is driven by the optimal balance these switches offer between functionality, security, and cost, building them the preferred choice for access layer deployments in enterprises, camputilizes, and industrial settings. Unlike unmanaged switches, Managed L2 devices provide essential features such as Virtual Local Area Network segmentation, Quality of Service prioritization, and Simple Network Management Protocol monitoring, which are crucial for maintaining network stability and security. The widespread adoption of Bring Your Own Device policies and the proliferation of Internet of Things sensors in smart buildings further amplify the necessary for L2 management capabilities to control device access and prevent broadcast storms. Furthermore, the ability to remotely configure and monitor these switches reduces operational overhead for IT teams managing distributed branches across the continent. The critical necessary for robust network segmentation and enhanced security protocols serves as the fundamental force driving the dominance of the Managed Layer 2 segment in the European market. With the increasing frequency of cyberattacks and the implementation of strict data protection laws like GDPR, organizations must isolate different types of traffic to prevent lateral relocatement of threats within their networks. Managed L2 switches enable the creation of Virtual Local Area Networks, which logically separate departments, guest utilizers, and IoT devices, ensuring that a breach in one segment does not compromise the entire infrastructure. The ability to enforce port security and disable unutilized ports on Managed L2 switches also mitigates the risk of unauthorized physical access, a key concern for facilities with open floor plans. Additionally, compliance with indusattempt standards such as PCI DSS for payment processing requires strict network isolation that only managed switches can provide. This regulatory and security imperative ensures that Managed L2 switches remain the most widely deployed configuration type across all verticals. The drive for operational efficiency through remote management capabilities acts as a powerful driver sustaining the leadership of the Managed Layer 2 segment in the European Ethernet switches market. Organizations are expanding their footprint with multiple branch offices and remote working sites. In this environment, the ability to monitor, configure, and troubleshoot network devices without physical presence is essential for reducing travel costs and downtime. Managed L2 switches support protocols like Simple Network Management Protocol and cloud-based management platforms that allow central IT teams to visualize network health and push configuration updates instantly. The integration of these switches with software-defined networking controllers further enhances automation, enabling dynamic policy enforcement and resource allocation based on real-time conditions. The scalability of remote management allows businesses to grow their network infrastructure without proportionally increasing their IT staff, offering a compelling return on investment. This operational advantage creates Managed L2 switches the default choice for organizations seeking to optimize their network operations while maintaining tight control over their distributed assets.

The Managed Layer 3 segment is predicted to witness the highest CAGR of 14.8% between 2026 and 2034, owing to the increasing complexity of enterprise networks and the necessary for innotifyigent routing capabilities at the distribution and core layers to handle heavy traffic loads. Also, this segment is boosted by the convergence of voice, video, and data onto single IP networks, which requires advanced routing protocols, access control lists, and quality of service mechanisms that only L3 switches can provide. Furthermore, the trconclude toward flattening network architectures to reduce latency and simplify management drives the deployment of L3 switches closer to the edge, replacing traditional router-switch hierarchies. The rise of software-defined networking also boosts this segment, as L3 switches serve as the programmable underlay fabric that enables flexible overlay networks. The shift toward innotifyigent, routed access networks positions the Managed L3 segment for the highest growth rate in the coming years. The accelerating convergence of Information Technology and Operational Technology networks in industrial settings serves as the main engine driving the rapid growth of the Managed Layer 3 segment. Modern smart factories require seamless communication between enterprise resource planning systems and factory floor machinery, necessitating switches that can route traffic between different subnets and apply complex security policies at the boundary. L3 switches provide the necessary routing innotifyigence to manage diverse protocols and ensure deterministic delivery of critical control messages without interfering with business traffic. The implementation of Time Sensitive Networking standards often requires L3 capabilities to coordinate timing information across larger network domains, enhancing the precision of automated processes. Industries are relocating towards fully connected ecosystems, caapplying a surge in demand for switches that bridge office and factory floors. Consequently, the Managed L3 market is experiencing significant expansion. The widespread adoption of Software Defined Networking architectures acts as a major accelerator for the surging growth of the Managed Layer 3 segment in the Europe ethernet switches market. SDN decouples the control plane from the data plane, requiring underlying hardware that supports open flow protocols and programmable forwarding tables, features inherent to advanced L3 switches. Managed L3 switches serve as the innotifyigent fabric that executes the centralized controller’s instructions, enabling dynamic path selection, load balancing, and rapid failover mechanisms that traditional L2 switches cannot support. The ability to program these switches via APIs allows organizations to integrate network management with their broader IT orchestration tools, streamlining operations and reducing human error. Furthermore, the flexibility of L3 switches to support various overlay technologies like VXLAN creates them indispensable for building scalable multi-tenant cloud environments. This architectural shift towards software-defined infrastructure ensures that Managed L3 switches will experience sustained high growth as networks become more agile and responsive.

COUNTRY LEVEL ANALYSIS

Germany Ethernet Switches Market Analysis

Germany dominated the European Ethernet switches market and accounted for a 26.6% share in 2025. The leading position of the German market is attributed to the “Industrie 4.0” strategy, which has led to the digitization of over 40 percent of German manufacturing plants, each requiring sophisticated Ethernet infrastructure to connect robots, sensors, and control systems. The counattempt has a highly advanced industrial base that drives immense demand for ruggedized and high-performance switching solutions for manufacturing automation and Indusattempt 4.0 applications. The presence of major global switch manufacturers and a strong ecosystem of system integrators further solidifies Germany’s position as a hub for innovation and deployment. Additionally, the government’s push for gigabit connectivity in rural areas has spurred investments in access layer switches to bridge the digital divide. The combination of industrial strength, technological leadership, and supportive policies ensures Germany remains the largest and most influential market for Ethernet switches in Europe.

United Kingdom Ethernet Switches Market Analysis

The United Kingdom was the next prominent player in the European Ethernet switches market and captured a 19.7% share in 2025 by serving as a major financial and technology hub that drives demand for high-speed data center and enterprise networking. The market status in the UK reveals a mature cloud computing sector and aggressive investments in artificial innotifyigence infrastructure, necessitating upgrades to 100 G and 400 G switching fabrics. A key driver for the UK market is the concentration of hyperscale data centers in London and surrounding regions, which account for a notable share of Europe’s total colocation capacity, creating a relentless demand for high-density core switches. The financial services sector, a cornerstone of the British economy, also contributes significantly by requiring low-latency, highly secure switching solutions for high-frequency trading and real-time transaction processing. Furthermore, the government’s Project Gigabit initiative aims to deliver rapid and reliable broadband to hard-to-reach areas, driving procurement of access switches for last-mile connectivity. The post-Brexit focus on digital sovereignty has also encouraged domestic organizations to upgrade their network infrastructure to ensure resilience and security. This blconclude of financial power, data center density, and strategic initiatives secures the UK’s position as a critical market for Ethernet switches.

France Ethernet Switches Market Analysis

France holds a key position in the Europe ethernet switches market, and is driven by strong state-led initiatives to modernize public sector infrastructure and promote digital sovereignty. The market is heavily fuelled by the “France 2030” investment plan, which allocates substantial funds for the development of trusted cloud services and the modernization of healthcare and education networks. The counattempt’s vibrant aerospace and automotive industries also contribute to demand, particularly for specialized switches capable of handling real-time data in design and production environments. The push for energy-efficient networking solutions aligns with France’s ambitious climate goals, encouraging the replacement of legacy hardware with green-certified switches. Additionally, the expansion of submarine cable landing stations in France enhances its role as a gateway for international data traffic, boosting demand for high-capacity core switches. This combination of public investment, industrial, and strategic positioning drives the steady growth of the Ethernet switch market in France.

Italy Ethernet Switches Market Analysis

Italy expanded its presence in the Europe ethernet switches market due to a growing focus on modernizing its SME sector and tourism infrastructure through digital technologies. The market status is evolving as Italian businesses increasingly adopt cloud services and IoT solutions to improve competitiveness and operational efficiency. A major driving factor is the National Recovery and Resilience Plan, which includes significant funding for digital innovation and broadband expansion, stimulating demand for Ethernet switches in both private and public sectors. The tourism indusattempt, a vital part of the Italian economy, is investing in smart hotel solutions and connected visitor experiences, driving the installation of PoE switches for lighting, security, and entertainment systems. Furthermore, the manufacturing hubs in Northern Italy are embracing automation, leading to increased purchases of industrial-grade switches for factory floors. The government’s incentives for energy efficiency also encourage the replacement of old networking equipment with newer, low-power models. This gradual but steady digital transformation ensures a consistent demand for Ethernet switches across the Italian market.

Netherlands Ethernet Switches Market Analysis

The Netherlands is likely to grow in the European Ethernet switches market during the forecast period, owing to its status as a premier data center hub and logistics gateway for Europe. The market status is robust, supported by the presence of major internet exmodify points and a high concentration of colocation facilities that serve as the digital enattempt point for the continent. A key growth factor for the Dutch market is the Amsterdam Metropolitan Area, which hosts one of the largest clusters of data centers in the world, generating immense demand for high-speed core and aggregation switches. The logistics and port of Rotterdam also drive demand for ruggedized switches to support automated terminal operations and supply chain visibility systems. The Netherlands’ proactive approach to sustainability has led to early adoption of energy-efficient switching technologies, with many organizations tarobtaining carbon-neutral data centers by 2030. Additionally, the strong presence of multinational corporations headquartered in the Netherlands fosters a culture of early technology adoption, building it a key testbed for new switching innovations. This strategic importance as a digital nexus ensures the Netherlands remains a vital and high-value market for Ethernet switches.

COMPETITIVE LANDSCAPE

The competition in the Europe ethernet switches market is intense and characterized by the presence of established global giants alongside specialized regional vconcludeors who compete on technology innovation and service quality. Large multinational corporations leverage their extensive product portfolios and strong brand recognition to offer conclude-to-conclude networking solutions that lock in enterprise customers through ecosystem integration. In contrast, niche players differentiate themselves by providing highly customized industrial switches or superior price-performance ratios for tiny and medium-sized businesses. The market sees frequent product launches featuring advanced capabilities like Time Sensitive Networking and Power over Ethernet to address emerging utilize cases in automation and smart buildings. Price competition remains moderate as acquireers prioritize reliability, security, ty and energy efficiency over initial cost savings, given the critical nature of network infrastructure. Regulatory compliance with European standards acts as a significant barrier to enattempt for non-compliant foreign vconcludeors, favoring local or well-adapted global providers. Innovation speed and the ability to demonstrate tangible return on investment through sustainability metrics are becoming key differentiators in this evolving competitive arena.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe ethernet switches market include

- Cisco Systems, Inc.

- Arista Networks, Inc.

- Hewlett-Packard Enterprise Company

- Juniper Networks, Inc.

- Huawei Technologies Co., Ltd.

- Dell Technologies, Inc.

- Allied Telesis Holdings Co., Ltd.

- Siemens AG

- Advantech Co., Ltd.

- Black Box Limited

- D-Link Corporation

- TP-Link Corporation

TOP LEADING PLAYERS IN THE MARKET

- Cisco Systems Inc stands as a preeminent force in the Europe ethernet switches market by delivering comprehensive networking solutions that span enterprise, industrial, and service provider segments globally. The company contributes to the worldwide ecosystem through its Catalyst and Nexus portfolios, which set indusattempt standards for security and automation. Cisco recently strengthened its European market position by launching new AI-ready switching platforms designed to handle massive data flows from generative artificial innotifyigence workloads. Their strategic focus includes expanding silicon photonics technology to reduce energy consumption in data centers while enhancing throughput. Cisco continues to invest heavily in software-defined networking capabilities that allow European customers to manage complex hybrid cloud environments seamlessly. These innovations reinforce their leadership by addressing critical necessarys for sustainability and operational agility across diverse verticals.

- Huawei Technologies Co Ltd maintains a significant presence in the Europe ethernet switches market despite regulatory challenges by offering high-performance and cost-effective networking hardware for various sectors. The company influences the global market through its CloudEngine series, which provides ultra-high density and low-latency switching for modern data centers. Huawei has recently focutilized on strengthening its position by introducing advanced energy-saving features that align with strict European Union environmental regulations. Their strategy involves deepening partnerships with local enterprises to deploy smart campus solutions that integrate artificial innotifyigence for predictive maintenance. Huawei also emphasizes research and development in silicon technologies to ensure supply chain resilience and product innovation. Huawei provides robust and scalable switching infrastructure to European organizations. This support assists them achieve digital transformation goals while navigating complex geopolitical landscapes.

- Hewlett Packard Enterprise operates as a key player in the Europe ethernet switches market by leveraging its Aruba Networks division to deliver innotifyigent edge solutions tailored for dynamic business environments. The firm contributes globally by pioneering cloud-native management platforms that simplify network operations and enhance security posture for distributed enterprises. HPE recently strengthened its European footprint by expanding its GreenLake edge-to-cloud platform to include automated switching services that optimize performance and reduce costs. Their commitment to sustainability is evident in new switch models designed with recycled materials and superior power efficiency ratings. HPE actively collaborates with European channel partners to accelerate the adoption of Wi-Fi 7 and multi-gigabit switching technologies. HPE drives continuous innovation in edge computing and secure access. This empowers organizations to build resilient networks that support next-generation applications and workflows.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe ethernet switches market primarily focus on developing energy-efficient hardware architectures that comply with stringent European Union environmental regulations and reduce the total cost of ownership for customers. Companies are increasingly integrating artificial innotifyigence and machine learning capabilities into their switching platforms to enable predictive maintenance and automated traffic optimization. Strategic acquisitions of specialized software firms are essential to enhance cloud management interfaces and provide unified visibility across hybrid network environments. Vconcludeors are also prioritizing the expansion of industrial-grade product lines to capture growth opportunities in manufacturing automation and smart city initiatives. Furthermore, market participants are investing heavily in silicon innovation to deliver higher port densities and rapider speeds, such as 400 Gigabit Ethernet,t while maintaining thermal efficiency. These collective strategies aim to drive technological leadership and customer loyalty in a highly competitive landscape.

MARKET SEGMENTATION

This research report on the europe ethernet switches market is segmented and sub-segmented into the following categories.

By Speed

- 1 G (Gigabit Ethernet)

- 10 G (10 Gigabit Ethernet)

- 25 G

- 40 G

- 100 G and Above

By Configuration

- Unmanaged Switches

- Managed Layer 2 Switches

- Managed Layer 3 Switches

By Counattempt

- Germany

- United Kingdom

- France

- Italy

- Netherlands

- Spain

- Sweden

- Rest of Europe\

Leave a Reply