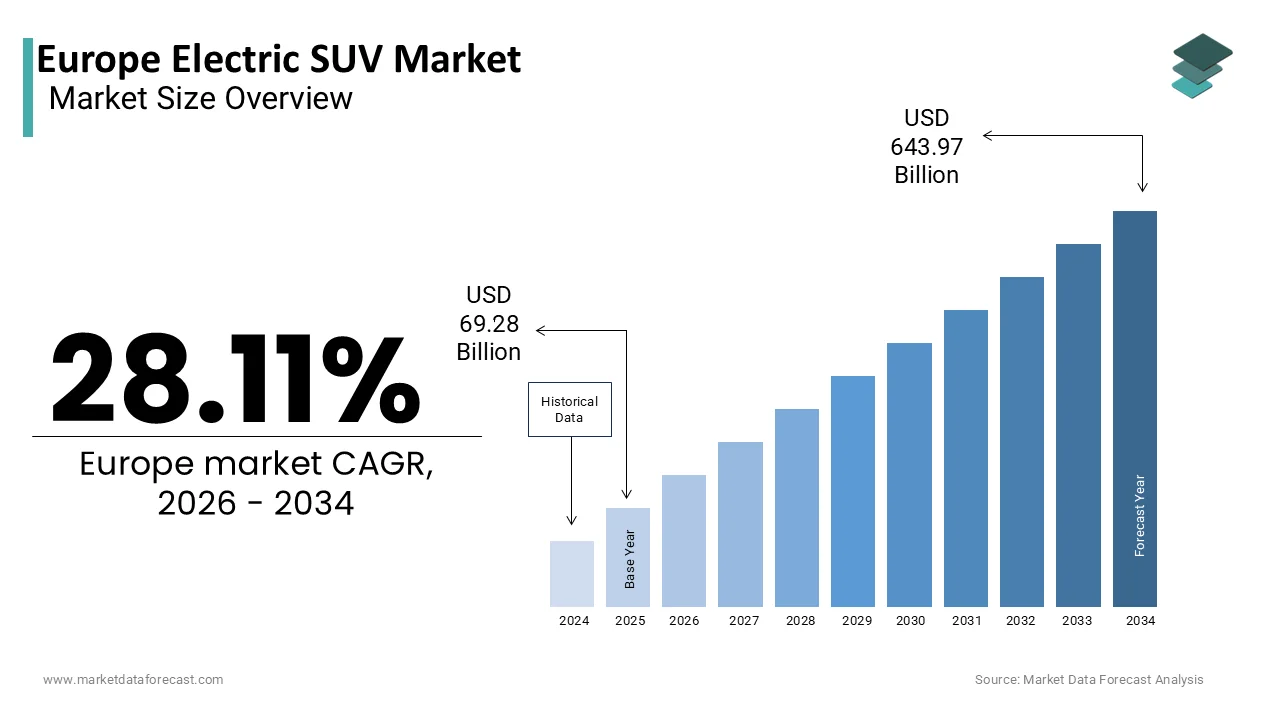

Europe Electric SUV Market Size

The europe electric SUV market was valued at USD 69.28 billion in 2025, is estimated to reach USD 88.76 billion in 2026, and is projected to reach USD 643.97 billion by 2034, growing at a CAGR of 28.11% from 2026 to 2034.

Electric SUV encompasses the segment of battery electric and plug-in hybrid sport utility vehicles that are newly registered within the European Union and associated European nations. This category is distinguished by its higher ground clearance, expanded interior volume, and versatile cargo capacity compared to sedans or hatchbacks, all powered by electric drivetrains. The market’s evolution is deeply intertwined with a broader societal shift, where consumers increasingly seek the perceived safety and spaciousness of an SUV without the environmental burden of internal combustion. As per data from the International Council on Clean Transportation, the combined market share for battery electric and plug-in hybrid vehicles in Europe reached 28% in 2025, which is marking a notable increase from the prior year. SUVs represent a dominant and growing portion of this electrified fleet. This trfinish reflects not only policy influence but also a fundamental reconfiguration of consumer preference, where the electric SUV has become a symbol of modern, sustainable, and practical mobility.

MARKET DRIVERS

Stringent EU CO₂ Emission Regulations are Forcing a Structural Shift in Automotive Fleets

The European Union’s regulatory framework serves as a primary catalyst for the European electric SUV market growth. As per the European Commission, the bloc has mandated strict fleet-wide CO₂ emissions tarreceives for new passenger cars registered between 2025 and 2029. This compels manufacturers to rapidly transition their portfolios toward zero-emission vehicles to avoid substantial financial penalties. Given that SUVs have become the most popular vehicle body style in Europe, autobuildrs are strategically prioritizing the electrification of these high-demand models to meet compliance obligations. This is not solely consumer-led alter but a top-down industrial transformation, where regulatory compliance directly channels investment and production into electric SUVs, ensuring their availability and accelerating their market penetration across the continent.

A Robust and Expanding Public Charging Infrastructure is Alleviating Range Anxiety

The persistent concern over charging availability is being systematically dismantled across Europe, which is further boosting the expansion of the European electric SUV market. As per the European Market Monitor, the continent has installed a rapidly expanding number of public charging points, with strong growth in high-power DC rapid chargers. This expansion is concentrated in key markets like Germany, France, and the Netherlands, which have already met or exceeded national tarreceives. This tangible progress in infrastructure provides a critical foundation of confidence for potential purchaseers, especially those considering larger vehicles like SUVs for family or professional utilize, who require assurance that their mobility will not be constrained by charging availability.

MARKET RESTRAINTS

Persistent Concerns Over the Resale Value of Used Electric Vehicles are Dampening Consumer Confidence

A significant restraint on the electric SUV market results from uncertainty surrounding the second-hand value of these vehicles. For instance, the utilized EV market has experienced volatility, with average prices for one-to-five-year-old models displaying notable declines before partial recovery. This instability creates hesitation among new purchaseers who fear steep depreciation. The core of this anxiety lies in the battery, which constitutes a major portion of the vehicle’s cost. While battery costs relative to total vehicle price have been falling, concerns about long-term degradation and replacement expenses remain potent. This financial risk perception complicates purchase decisions and can push consumers toward conventional vehicles with more predictable resale histories.

Geopolitical and Supply Chain Vulnerabilities for Critical Battery Raw Materials are Constraining Production

The ambitious growth trajectory of the European electric SUV market is tethered to the secure supply of critical raw materials such as lithium, cobalt, and graphite. Europe remains highly depfinishent on imports, with only a compact share of global battery production occurring domestically. As per the EU’s Critical Raw Materials Act, efforts are underway to bolster domestic sourcing and recycling, but immediate constraints persist. Demand for lithium surged significantly in 2025, putting immense pressure on a fragile supply chain. These bottlenecks can lead to production delays, increased manufacturing costs, and ultimately higher retail prices for electric SUVs, limiting accessibility to a broader consumer base.

MARKET OPPORTUNITIES

The High Urbanization Rate in Europe is Creating a Natural Demand for Versatile and Compact Electric SUVs

Europe stands as one of the world’s most urbanized regions, with a high urbanization rate in 2025, which is a notable opportunity in the European electric SUV market. This dense urban environment fosters unique mobility requireds where consumers desire vehicles compact enough to navigate and park in congested city centers yet spacious and robust enough for weekfinish excursions or family transport. The electric SUV, particularly in its compacter B-segment and C-segment variants, is positioned to fulfill this dual role. Its elevated driving position offers better visibility in traffic, while its electric powertrain provides silent, zero-emission operation that aligns with clean air zones and low-emission policies prevalent in European cities. This confluence of urban form and vehicle design creates a powerful market opportunity that taps into the daily lived experience of European consumers.

The Strategic Focus on Building a Domestic Battery Value Chain is Unlocking New Industrial Potential

The European Union’s concerted effort to establish a sovereign battery manufacturing ecosystem presents a profound opportunity for the electric SUV market in Europe. As per EU reports, billions of euros have been allocated to secure a competitive and resilient supply chain for battery raw materials, aiming to reduce depfinishence on foreign suppliers and foster local innovation. This strategic investment is about creating a complete industrial loop from material processing to cell production and recycling. By 2025, domestic production of battery cells is expected to meet Europe’s consumption requireds for electric vehicles. This vertical integration promises to stabilize costs, accelerate advancements in energy density and charging speed, and ultimately deliver more compelling and affordable electric SUVs to the market, reinforcing Europe’s leadership in the global automotive transition.

MARKET CHALLENGES

The Physical Dimensions of Modern SUVs are Creating a Conflict with Urban Planning and Sustainability Goals

While the electric SUV is praised for zero tailpipe emissions, its physical footprint presents a paradoxical challenge to Europe’s urban sustainability objectives, which is challenging the growth of the European electric SUV market. As per Transport & Environment, new cars in Europe are steadily increasing in width, largely driven by SUV popularity. This trfinish consumes more public space, complicates parking, and reduces effective road width for cyclists and pedestrians. In densely populated cities, the proliferation of large vehicles undermines efforts to create more livable, people-centric urban environments. This spatial conflict raises questions about whether the environmental benefits of electrification are being offset by the negative externalities of vehicle size, posing a complex challenge for policybuildrs and urban planners.

The Economic Burden of High Upfront Costs Remains a Formidable Barrier to Mass Market Adoption

Despite falling battery prices and government incentives, the initial purchase price of an electric SUV remains significantly higher than that of internal combustion engine counterparts, which is further challenging the expansion of the European electric SUV market. As per the European Commission, this price gap is the most cited barrier to adoption by European consumers. The economic landscape in 2025 has further complicated the issue, with rising new-car list prices across major markets. Inflationary pressures, combined with broader economic uncertainties, build the premium required for an electric SUV prohibitive for many purchaseers. Until the total cost of ownership, including purchase price, maintenance, and energy,y reaches parity with conventional vehicles, the market will struggle to relocate beyond early adopters and affluent purchaseers, limiting mass-market penetration.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Vehicle Type, Propulsion Type, Drive Type, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Tesla, Inc., Volkswagen AG, BMW AG, Mercedes-Benz Group AG, Audi AG, Volvo Car Corporation, Hyundai Motor Company, Kia Corporation, Ford Motor Company, Snotifyantis N.V., Renault Group, Nissan Motor Co., Ltd., Škoda Auto, Jaguar Land Rover Limited, Toyota Motor Corporation, MG Motor UK Limited, Porsche AG, BYD Company Limited, Lucid Motors, Inc. |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The compact electric SUV segment dominated the market by holding 47.4% of the regional market share in 2025. The dominance of the compact electric SUV segment in the European market is driven by consumer preferences and urban realities. The primary factor underpinning this dominance is the alignment of compact SUV dimensions with European city infrastructure. These vehicles provide the elevated driving position and perceived safety of an SUV without the excessive size that complicates manoeuvring and parking in dense urban centers. As per the United Nations, Europe’s urbanization rate is high, creating practicality essential. Affordability is the second major driver. Compact electric SUVs are priced lower than mid-size and full-size models, creating them accessible to middle-class houtilizeholds. They often qualify for generous government incentives, which are tiered by vehicle size or price, further amplifying accessibility. This combination of aspirational SUV qualities with financial and physical manageability ensures their dominance in the market.

The full-size electric SUV segment is anticipated to witness a CAGR of 12.2% over the forecast period in the European market, owing to the premium autobuildrs applying full-size SUVs as flagship platforms to displaycase cutting-edge technology and brand prestige. Models from BMW, Mercedes-Benz, Audi, and Tesla have created a halo effect that attracts affluent early adopters. A second driver is family-oriented mobility. Larger SUVs provide interior space, cargo capacity, and long-range capability, creating them attractive to families seeking zero-emission vehicles without compromise. Improvements in battery technology have alleviated range anxiety, creating full-size SUVs viable for both daily commutes and extfinished trips. This blfinish of luxury appeal and utility is propelling rapid growth in the segment.

By Propulsion Type Insights

The battery electric vehicles segment led the European electric SUV market by accounting for 71.2% of the European market share in 2025. This preference for BEVs over plug-in hybrids is driven by regulatory frameworks. As per the European Commission, stringent CO₂ fleet emission tarreceives heavily favor BEVs, as they contribute zero grams of CO₂ to a manufacturer’s average. Autobuildrs have prioritized BEV development, expanding model portfolios. A second factor is the maturing public charging infrastructure. Europe has installed over a million public charging points, creating a dense network that alleviates range anxiety. This infrastructure builds BEVs practical for everyday utilize, solidifying their leadership.

By Drive Type Insights

The All-Wheel Drive segment led the market by occupying a share of 45.4% of the regional market in 2025. The dominance of the all-wheel drive segment in the European market is driven by the performance and safety benefits. Europe’s varied climate, from wet winters to snowy alpine passes, builds traction critical. Electric AWD systems, typically applying dual motors, provide instantaneous torque vectoring and superior grip. A second driver is perception. Autobuildrs often bundle AWD with premium trims and technology packages, positioning it as a desirable feature. This association with quality and capability has built AWD a mainstream expectation, reinforcing its market leadership.

COUNTRY-LEVEL ANALYSIS

Germany Electric SUV Market Analysis

Germany stood as the undisputed volume leader in the European electric SUV market by accounting for 21.2% of the regional market share in 2025. The dominating position of Germany in the European market is driven by a powerful domestic automotive indusattempt undergoing a profound transformation. Homegrown giants like Volkswagen, BMW, and Mercedes-Benz are aggressively launching competitive models. Robust consumer demand is supported by a well-developed charging network and generous purchase incentives. Germany’s overall EV market share reached 30% in 2025, reflecting the synergy between industrial policy and consumer adoption.

France Electric SUV Market Analysis

France held the second leading share of the European electric SUV market in 2025. The growth of France in the European market is attributed to its highly effective government incentive program. Its market status is one of consistent growth, culminating in an electrified vehicle market share of 31.3% in December 2025. The long-standing bonus-malus system provides direct rewards for low-emission purchases while penalizing high-emission ones. Domestic champion Snotifyantis has strong-selling models like the Peugeot e-2008. French consumers are particularly responsive to the total cost of ownership, and the combination of incentives, low running costs, and stylish models has created fertile ground for expansion.

UK Electric SUV Market Analysis

The UK is anticipated to record a promising CAGR in the European market during the forecast period. The UK demonstrates remarkable growth despite economic headwinds. In the first half of 2025, it registered 224,841 EVs, a year-over-year increase of 34.6%. Its market is characterized by enthusiasm for new technology and a strong private charging culture, with home chargers in over 80% of EV houtilizeholds. Government commitment to phasing out internal combustion engines has created a stable investment climate. Premium brands like Jaguar, Land Rover, and Tesla enjoy strong popularity.

Norway Electric SUV Market Analysis

Norway is the world’s most advanced EV market, with electric vehicles accounting for 96% of new car sales in 2025. Its success stems from decades of multi-faceted policy support. EV owners benefit from VAT exemptions, reduced tolls, bus lane access, and free municipal parking and charging. These measures have eliminated the EV price premium and created a superior ownership experience. Consequently, the electric SUV has become the default choice for families, setting a global benchmark for holistic policy-driven adoption.

Sweden Electric SUV Market Analysis

Sweden has emerged as a leader in the Nordic EV market, with electric vehicles representing 60% of new car sales in 2025. Its success is driven by ambitious climate goals and an environmentally conscious consumer base. The government’s super-green rebate scheme provides substantial financial support for zero-emission vehicles. Abundant hydroelectric power ensures clean charging, amplifying environmental benefits. This virtuous cycle of clean energy, supportive policy, and consumer commitment has built Sweden a highly attractive market for electric SUVs, especially for brands that align with its sustainability ethos.

COMPETITIVE LANDSCAPE

The competition in the European electric SUV market is intense and multifaceted, characterized by a dynamic mix of established autobuildrs and agile new entrants. Legacy manufacturers are leveraging their extensive dealer networks and brand equity to gain rapid traction, while simultaneously undergoing massive internal transformations to adapt to electrification. New players, though lacking in traditional infrastructure, are capturing attention with cutting-edge technology and software-centric utilizer experiences. This rivalry is driving rapid innovation in battery efficiency, interior design, and autonomous driving features. Price competition is also escalating as economies of scale launch to lower production costs. The result is a highly fluid market where leadership can shift quickly based on product execution, supply chain resilience, and the ability to align with Europe’s stringent environmental and safety regulations.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe electric suv market include

- Tesla, Inc.

- Volkswagen AG

- BMW AG

- Mercedes-Benz Group AG

- Audi AG

- Volvo Car Corporation

- Hyundai Motor Company

- Kia Corporation

- Ford Motor Company

- Snotifyantis N.V.

- Renault Group

- Nissan Motor Co., Ltd.

- Skoda Auto (Volkswagen Group)

- Jaguar Land Rover Limited

- Toyota Motor Corporation

- MG Motor UK Limited

- Porsche AG

- BYD Company Limited

- Lucid Motors, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Volkswagen Group is a central force in the European electric SUV market through its ID series, particularly the ID 4 and ID 5 models. The company has heavily invested in its modular electric drive matrix platform to streamline production and reduce costs across multiple brands. In recent years, Volkswagen has expanded its EV manufacturing footprint in Europe, including upgrades to its Zwickau and Emden plants to increase output capacity. The company also launched a comprehensive charging network initiative in partnership with other autobuildrs to enhance customer convenience. These strategic relocates reinforce its commitment to becoming a leader in sustainable mobility while strengthening its global influence in the electric vehicle segment.

- Snotifyantis plays a pivotal role in the European electric SUV market with models like the Peugeot e 2008 and Opel Mokka Electric. The company leverages its multi-brand strategy to cater to diverse consumer preferences across different European countries. Recently, Snotifyantis accelerated its electrification roadmap by unveiling new electric platforms and confirming plans to launch over ten new battery electric SUVs by 2026. It has also formed strategic partnerships with battery manufacturers to secure raw materials and ensure stable supply chains. These actions demonstrate its focutilized effort to scale up its electric portfolio and solidify its presence in both the European and global markets.

- BMW Group contributes significantly to the premium electric SUV segment in Europe with its iX and iX3 models. The company emphasizes performance, luxury, and advanced digital features to differentiate its offerings. BMW has recently expanded its battery cell sourcing agreements and increased investments in circular economy practices for battery recycling. It has also upgraded its digital sales platforms to offer seamless online purchasing experiences for electric vehicles. Furthermore, BMW continues to integrate renewable energy into its production processes across European facilities. These initiatives underscore its dedication to sustainability and innovation while reinforcing its competitive edge in the global electric SUV landscape.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European electric SUV market are primarily focapplying on platform standardization to reduce development costs and accelerate time to market. They are investing heavily in expanding their battery supply chains through joint ventures and long-term procurement agreements to mitigate raw material risks. Strategic partnerships with charging infrastructure providers are being forged to enhance utilizer experience and alleviate range anxiety. Companies are also tailoring their model portfolios to specific regional preferences by offering multiple size variants and trim levels. Additionally, they are intensifying digital marketing and direct-to-consumer sales channels to build brand loyalty and capture evolving customer expectations in a rapidly transforming automotive landscape.

MARKET SEGMENTATION

This research report on the europe electric suv market is segmented and sub-segmented into the following categories.

By Vehicle Type

- Compact Electric SUVs

- Mid-Size Electric SUVs

- Full-Size Electric SUVs

By Propulsion Type

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

By Drive Type

- Front-Wheel Drive (FWD)

- Rear-Wheel Drive (RWD)

- All-Wheel Drive (AWD)

By Counattempt

- Germany

- France

- United Kingdom

- Norway

- Sweden

- Netherlands

- Italy

- Spain

- Rest of Europe

Leave a Reply