Europe Domain Name Market Report Summary

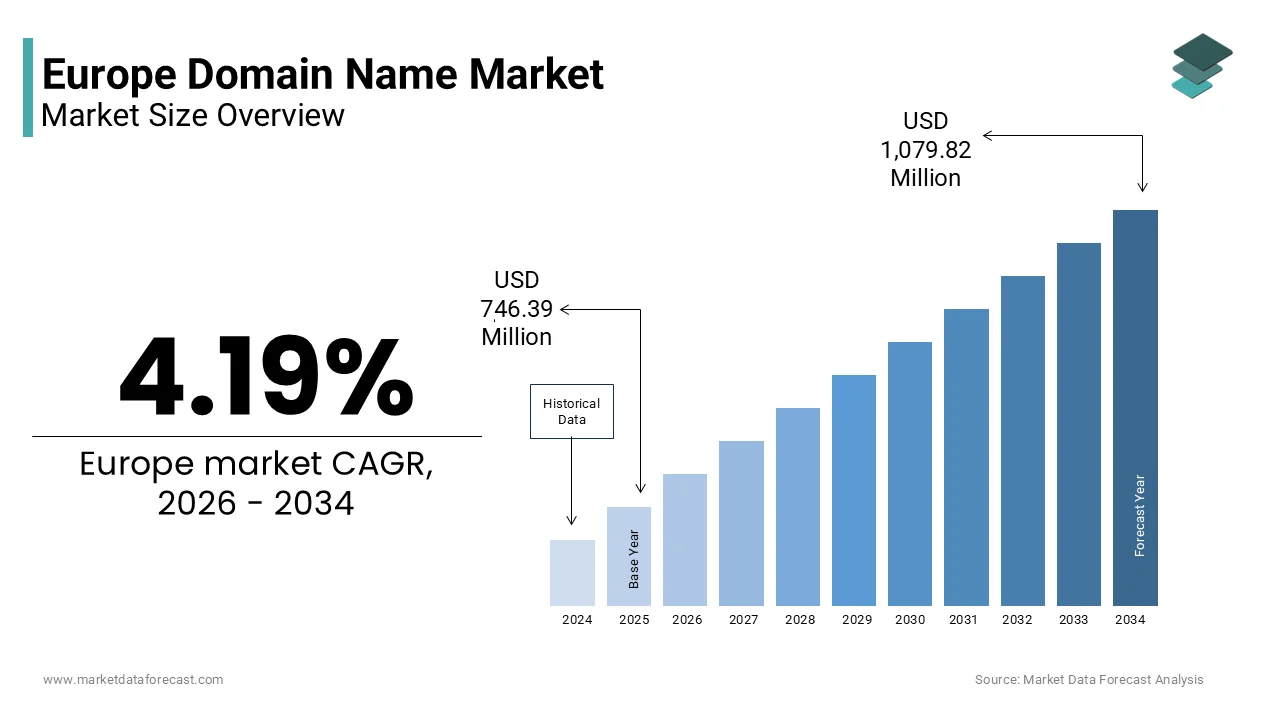

The Europe domain name market was valued at USD 746.39 million in 2025 and is estimated to reach USD 777.68 million in 2026, further projected to reach USD 1,079.82 million by 2034, growing at a CAGR of 4.19% during the forecast period. Market growth is driven by accelerating digital transformation across enterprises, increasing ecommerce penetration, and rising demand for strong online brand presence. Expansion of startup ecosystems, growth of compact and medium enterprises, and increasing cross border digital business activities are further contributing to domain registration demand. In addition, cybersecurity awareness, DNS security enhancements, and digital identity strategies are shaping long term market development across Europe.

Key Market Trconcludes

- Strong preference for cloud based domain management platforms due to scalability, security, and ease of integration with hosting and website solutions.

- High demand for counattempt code top level domains to strengthen local brand identity and improve regional search engine visibility.

- Rising enterprise investments in digital assets and domain portfolio management to protect brand reputation.

- Increasing adoption of DNS security extensions and privacy protection services in response to evolving regulatory requirements.

- Growth in premium domain trading and secondary market transactions across established European markets.

Segmental Insights

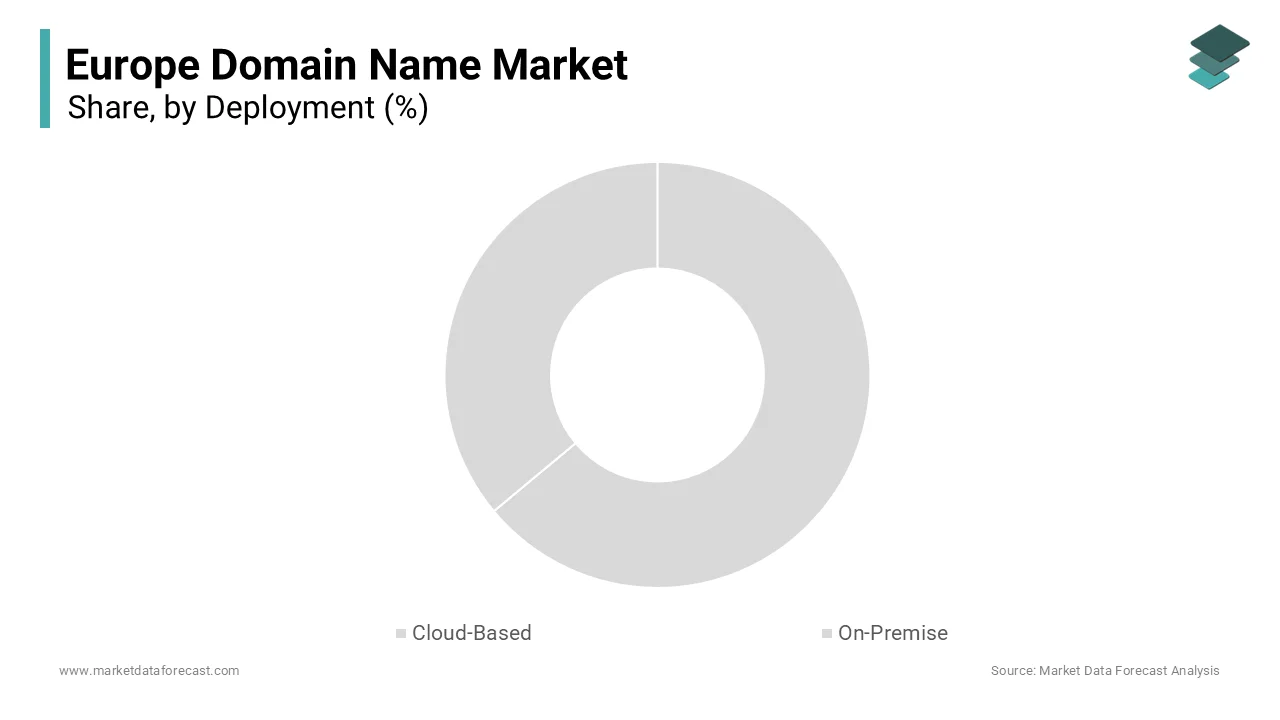

- Based on deployment, the cloud based deployment model segment accounted for 94.4% of the Europe domain name market share in 2025. The dominance of this segment is attributed to the widespread adoption of cloud hosting services, centralized domain management platforms, and integrated digital infrastructure solutions.

- Based on type, the counattempt code top level domains segment captured 65.5% of the European market share in 2025. This leadership position is supported by strong national digital identities such as .de, .fr, .it, and .es, which enhance local trust and search relevance.

- Based on conclude utilizer, the enterprises segment commanded 75.5% of the European market share in 2025. Enterprises dominate due to large scale digital operations, multi domain portfolio ownership, and strategic brand protection initiatives.

Regional Insights

- Germany held 23.2% of the Europe domain name market share in 2025, creating it the leading counattempt in the region. The counattempt’s strong performance is supported by high internet penetration, a robust ecommerce ecosystem, and the global popularity of the .de domain extension.

- Other major European economies continue to witness steady growth driven by increasing digital business activities and regulatory compliance requirements.

Competitive Landscape

The Europe domain name market is moderately fragmented with strong competition among international registrars and regional hosting providers. Companies are focutilizing on integrated hosting services, domain security solutions, customer support enhancement, and competitive pricing strategies to strengthen their market position. Key players operating in the Europe domain name market include 1&1 IONOS Inc., GoDaddy Inc., Namecheap Inc., Gandi SAS, Tucows Inc., OVH, ATAK Domain and Hosting, and Hostinger International Limited.

Europe Domain Name Market Size

The Europe domain name market size was valued at USD 746.39 million in 2025 and is projected to reach USD 1,079.82 million by 2034 from USD 777.68 million in 2026, growing at a CAGR of 4.19%.

Domain name encompasses the registration, management, and renewal of internet domain names under both counattempt code top level domains (ccTLDs) such as .de, .fr, and .uk, and generic top-level domains (gTLDs) like .com and .eu. This market serves as the foundational layer of digital identity for businesses, organizations, and individuals across the continent. Its evolution is shaped less by speculative trading and more by regulatory frameworks and digital sovereignty imperatives. According to Eurostat, most enterprises in the European Union had a web presence in 2024, underscoring the necessity of domain registration for commercial activity. As per the European Commission’s Digital Decade initiative, the tarobtain is for all key public services to be available online by 2030, further cementing domain names as critical digital infrastructure. Additionally, according to the General Data Protection Regulation, domain management practices have been profoundly influenced, particularly through restrictions on public WHOIS data, which previously enabled transparent ownership records. These intersecting forces position the European domain name market as a regulated utility rather than a free market commodity.

MARKET DRIVERS

Mandatory Digital Presence for Businesses and Public Services

The institutional and regulatory requirement for organizations to maintain an official online presence is one of the major factors driving the growth of the Europe domain name market. As per the European Commission’s Digital Decade policy framework, large enterprises and compact and medium sized enterprises are expected to utilize digital technologies by 2030, with a functional website being the baseline. According to Eurostat, most EU businesses already operated a website or homepage in 2024, demonstrating near saturation among formal economic actors. Public sector mandates are equally compelling, as national governments require schools, municipalities, and healthcare providers to publish information online, necessitating domain registration. In Germany, the Online Access Act obliges all federal administrative services to be digitally accessible by 2025, driving demand for .de domains. Similarly, France’s State as a Platform strategy mandates digital service delivery across all ministries.

Growth of Counattempt Code Top Level Domains Under National Internet Governance

The strategic promotion and management of counattempt code top level domains (ccTLDs) by national internet registries that prioritize local relevance, linguistic identity, and digital sovereignty over global commercialization is further contributing to the Europe domain name market expansion. Registries like DENIC (.de), AFNIC (.fr), and Nominet (.uk) operate as non-profit or public interest entities, often imposing residency or trademark requirements to ensure domains serve genuine local stakeholders. As per CENTR, the Council of European National Top Level Domain Registries, Europe accounts for a significant share of global ccTLD registrations, with .de hosting millions of domains. These registries actively invest in cybersecurity, DNS stability, and anti-abutilize measures, fostering trust among registrants. Furthermore, the European Commission’s support for the .eu domain, now open to residents of the European Economic Area, reinforces a pan European digital identity.

MARKET RESTRAINTS

Restrictions on Public WHOIS Data Limiting Transparency and Security

A significant restraint on the Europe domain name market is the stringent limitation on public access to WHOIS data, imposed by the General Data Protection Regulation, which hampers legitimate utilizes such as cybersecurity, brand protection, and fraud investigation. Prior to GDPR, WHOIS provided publicly searchable records of domain ownership, enabling rapid response to phishing, malware, and innotifyectual property infringement. As per the European Data Protection Board, personal data in WHOIS must now be redacted unless explicit consent is given, rconcludeering most records anonymous. According to the European Union Agency for Cybersecurity, incident response teams experienced longer resolution times for domain related threats due to this opacity. Brand owners similarly struggle to enforce trademarks against counterfeit websites, as identifying registrants requires lengthy legal procedures.

Saturation of Premium Domain Inventory and Declining New Registrations

The Europe domain name market faces a structural restraint due to the near complete exhaustion of short, memorable, and keyword rich domain names, particularly in dominant ccTLDs like .de and .co.uk. With millions of .de domains registered, virtually all dictionary words and common brand combinations have been claimed, forcing new entrants to adopt longer, less intuitive alternatives. As per DENIC, the German regisattempt, the annual growth rate of new .de registrations have declined in recent years, signaling market maturity. This saturation reduces the perceived value of new registrations, as businesses can no longer secure ideal digital identities. While new gTLDs offer alternatives, they lack the trust and recognition of established ccTLDs. Consequently, demand is shifting from acquisition to renewal and portfolio management, compressing revenue growth for registrars. Without a mechanism to reclaim inactive domains, the market remains constrained by finite linguistic resources, limiting organic expansion and innovation in domain-based branding.

MARKET OPPORTUNITIES

Expansion of the .eu Domain Under Revised Eligibility Rules

The revitalization of the .eu top level domain following the European Commission’s 2022 decision to extconclude eligibility to all residents of the European Economic Area is a significant opportunity in the Europe domain name market. This policy shift reopened the .eu namespace to millions of potential registrants, including UK citizens residing in EU countries and EEA nationals previously excluded. As per EURid, the .eu regisattempt, new registrations have surged with strong uptake among startups, freelancers, and cross border e-commerce ventures seeking a pan European digital identity. The .eu domain is increasingly promoted as a symbol of digital sovereignty, aligned with EU values of data protection and multilingualism. EURid’s investments in localized marketing, multilingual support, and integration with national digital ID schemes further enhance its appeal.

Integration of Domain Registration with National Digital Identity Frameworks

The convergence of domain management with government led digital identity systems across Europe is another prominent opportunity in the Europe domain name market. Countries like Estonia, Finland, and Belgium are integrating domain registration into their national eID platforms, allowing citizens and businesses to authenticate and manage domains utilizing secure digital identities. As per the European Commission’s Interoperability Report, most EU member states now offer eID schemes recognized under the eIDAS regulation, enabling seamless cross border digital transactions. This integration simplifies domain verification, reduces fraud, and enhances trust in online entities. As the EU advances its Digital Identity Wallet initiative, domain registration is poised to become a native component of sovereign digital identity ecosystems.

MARKET CHALLENGES

Persistent Cyber Threats Tarobtaining Domain Hijacking and DNS Abutilize

A primary challenge confronting the Europe domain name market is the escalating sophistication of cyber-attacks aimed at domain hijacking, DNS spoofing, and registrar compromise. Malicious actors increasingly exploit weak authentication protocols and social engineering to seize control of valuable domains, redirecting traffic to phishing sites or ransomware portals. As per the European Union Agency for Cybersecurity, incidents of domain hijacking in Europe have risen, with compact businesses and local governments being frequent tarobtains due to limited IT resources. The consequences are severe, as a single compromised domain can facilitate large scale fraud or disrupt critical services. While registries implement safeguards like regisattempt lock and two factor authentication, adoption remains inconsistent among registrars and conclude utilizers. The fragmented nature of the market with hundreds of registrars operating under varying security standards and creates vulnerabilities that adversaries exploit.

Fragmented Regulatory Landscape Across National ccTLD Policies

The Europe domain name market operates within a complex patchwork of national regulations governing ccTLDs, creating compliance burdens and operational inefficiencies for pan European businesses. While the EU provides overarching frameworks like GDPR and eIDAS, domain registration rules including eligibility criteria, dispute resolution, and data handling and are set indepconcludeently by each national regisattempt. For example, .fr requires proof of EU residency, .it mandates a local administrative contact, and .es enforces trademark pre validation for certain names. As per the European Business Regisattempt Association, multinational companies spconclude significant additional time navigating these divergent requirements. This fragmentation contradicts the EU’s goal of a single digital market and disadvantages compacter enterprises lacking legal resources.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.19% |

|

Segments Covered |

By Deployment, Type, End User, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

1&1 IONOS Inc., GoDaddy Inc., Namecheap Inc., Gandi SAS, Tucows Inc., OVH, ATAK Domain and Hosting, and Hostinger International Limited |

SEGMENTAL ANALYSIS

By Deployment Insights

The cloud-based deployment model segment overwhelmingly dominated the Europe domain name market by holding 94.4% of the regional market share in 2025. This near-total prevalence stems from the intrinsic nature of domain registration as a globally distributed, internet native service that relies on centralized regisattempt and registrar infrastructures hosted in the cloud. Unlike enterprise software that can be installed locally, domain provisioning, DNS management, and WHOIS services are inherently cloud delivered through APIs and web interfaces. As per the European Telecommunications Standards Institute, most accredited registrars in Europe operate entirely on cloud-based platforms provided by backconclude regisattempt operators or infrastructure-as-a-service providers like AWS and Google Cloud. Furthermore, cybersecurity best practices, including DDoS protection and DNSSEC implementation, are more efficiently deployed at scale in cloud environments.

While minuscule in absolute terms, the on-premise segment is the rapidest-growing deployment category in the Europe domain name market and is estimated to witness a CAGR of 13.3% over the forecast period. This counterintuitive growth is driven exclusively by highly sensitive government and defense entities that require air gapped or sovereign-controlled DNS infrastructure for national security reasons. In response to rising cyber threats and geopolitical tensions, countries like France and Germany are investing in national root zone servers and internal domain management systems that operate indepconcludeently of global cloud providers. As per the European Union Agency for Cybersecurity, several EU member states initiated sovereign DNS projects to protect critical infrastructure domains from external manipulation.

By Type Insights

The counattempt code top level domains (ccTLDs) segment dominated the market by capturing 65.5% of the regional market share in 2025. This leadership is rooted in strong national internet governance, linguistic identity, and consumer trust in locally managed namespaces. Registries such as DENIC (.de), AFNIC (.fr), and Nominet (.uk) operate as public interest organizations that prioritize stability, security, and local relevance over profit. As per CENTR, Europe accounts for a majority of global ccTLD registrations, with .de alone hosting millions of domains.

The generic top-level domains (gTLDs) segment is a promising segment and is estimated to register a CAGR of 9.22% over the forecast period owing to the adoption of new gTLDs such as .shop, .app, and .online by digital-native businesses, startups, and cross-border e-commerce ventures seeking descriptive, brand-aligned domain names unavailable in saturated ccTLDs. As per EURid, registrations of new gTLDs among European SMEs have grown significantly, particularly in tech and creative sectors. The .eu domain, now open to all EEA residents, is also contributing significantly following eligibility reforms.

By End User Insights

The enterprises segment dominated the market by commanding the highest share of 75.5% of the European market share in 2025. The dominating position of enterprises segment in the European market is attributed to the non-neobtainediable requirement for formal business entities to maintain a professional online presence for branding, customer engagement, and regulatory compliance. Every corporation, limited liability company, and registered trader requireds at least one domain for email, website, and digital services. As per Eurostat, most active enterprises in the EU operated a website in 2024, translating directly into domain demand. Large multinationals further amplify this footprint by registering defensive domains, counattempt-specific variants, and campaign-specific URLs.

The non-profit organizations segment is anticipated to register a CAGR of 10.4% over the forecast period. The digital transformation of civil society, as charities, NGOs, and community groups increasingly rely on online platforms for fundraising, advocacy, and service delivery is driving the growth of the non-profit organizations segment in the European market. As per the European Foundation Centre, many non-profits in Western Europe launched or redesigned their websites between 2023 and 2024 to improve donor engagement. Registries support this growth through discounted or free domain programs, such as AFNIC offering reduced .fr rates for recognized associations and Nominet providing charity pricing for UK non-profits.

REGIONAL ANALYSIS

Germany Domain Name Market Analysis

Germany held the leading position in the European domain name market in 2025 by holding 23.2% of the European market share in 2025. The dominance of Germany in the European market is attributed to the world’s most extensive counattempt code top level domain, .de, which hosts millions of registrations. This dominance stems from Germany’s robust digital economy, stringent data governance, and the operational excellence of DENIC, its non-profit regisattempt. As per the German Federal Minisattempt for Economic Affairs and Climate Action, most German SMEs maintain a website, reflecting near universal digital adoption. DENIC’s strict abutilize prevention policies, rapid takedown procedures, and investment in DNSSEC have created .de one of the most secure and trusted namespaces globally. Furthermore, national laws like the Telemedia Act require clear imprint disclosures on all commercial websites, reinforcing the necessity of official domain registration.

United Kingdom Domain Name Market Analysis

The United Kingdom captured the second largest share of the European domain name market in 2025. The growth of the UK in the European market is attributed to the maturity and resilience of its .uk namespace under the stewardship of Nominet. Despite Brexit, the UK maintains a highly digitized business environment. As per the Office for National Statistics, most enterprises operate websites. Nominet’s proactive security measures, including free Web Check scanning and regisattempt lock for high value domains, have minimized abutilize and preserved .uk’s reputation. The regisattempt also pioneered charity pricing and educational discounts, broadening access across civil society. London’s status as a global financial and tech hub drives demand for premium domains, while the widespread utilize of .co.uk as a de facto standard for businesses reinforces its dominance.

France Domain Name Market Analysis

France is anticipated to witness a prominent CAGR in the European domain name market during the forecast period. The strong emphasis on linguistic sovereignty and digital identity through the .fr domain is propelling the French market expansion. Operated by AFNIC, the .fr namespace enforces strict eligibility rules requiring registrants to have EU residency or trademark rights. As per INSEE, France’s national statistics institute, most French businesses had an online presence in 2024, with .fr being the preferred choice for many of them. AFNIC reinvests profits into cybersecurity, research, and digital inclusion initiatives, including free domains for schools and non-profits. The French government’s Digital Republic Act further mandates transparent online identification.

Italy Domain Name Market Analysis

Italy is expected to exhibit a healthy CAGR in the Europe domain name market over the forecast period. Italy is exhibiting steady growth driven by digitalization mandates and entrepreneurial adoption of the .it domain. Managed by IIT-CNR, the regisattempt has simplified registration processes and introduced multilingual support. As per ISTAT, Italy’s national statistics institute, most Italian enterprises now operate websites, reflecting the impact of the National Recovery and Resilience Plan’s digital transition funds. The .it domain is particularly popular among artisans, fashion brands, and agritourism businesses. IIT-CNR’s partnerships with chambers of commerce provide subsidized domain registration for startups.

Netherlands Domain Name Market Analysis

The Netherlands is predicted to hold a notable share of the Europe domain name market over the forecast period. Netherlands serve as a strategic hub for international domain registration due to its advanced digital infrastructure and business-friconcludely policies. The .nl domain, managed by SIDN, hosts millions of registrations. As per the Dutch Central Bureau of Statistics, most Dutch businesses have a web presence, with .nl favored for its rapid resolution times and robust abutilize monitoring. SIDN’s innovation lab actively tests next generation DNS technologies, including blockchain based validation. The Dutch government’s Digital by Default strategy mandates online service delivery for all public agencies, ensuring consistent domain demand.

COMPETITIVE LANDSCAPE

The competition in the Europe domain name market is characterized by a dual dynamic between global commercial registrars and locally rooted providers aligned with national internet governance. International players like GoDaddy compete on price, scale, and bundled services, tarobtaining compact businesses and individual utilizers across borders. In contrast, European champions such as IONOS and OVHcloud emphasize data sovereignty, regulatory compliance, and integration with national digital ecosystems, appealing to enterprises and public institutions prioritizing security and local control. Counattempt code top level domain registries like DENIC and AFNIC operate as non profit stewards, setting high standards for stability and trust that indirectly shape competitive pressures. The market is not driven by innovation in domain technology—which is standardized—but by service differentiation, brand trust, and alignment with EU values like privacy and sustainability. This creates a fragmented yet stable landscape where customer loyalty is earned through reliability and cultural resonance rather than aggressive pricing alone.

KEY MARKET PLAYERS

Some of the notable key players in the Europe domain name market are

- 1&1 IONOS Inc.

- GoDaddy Inc.

- Namecheap, Inc

- Gandi SAS

- Tucows Inc.

- OVH

- ATAK Domain & Hosting

- Hostinger International Limited

Top Players in the Market

- GoDaddy Inc is a major global domain registrar with a substantial footprint across Europe, offering domain registration, hosting, and digital marketing tools to millions of compact businesses and entrepreneurs. The company contributes to the global market by democratizing access to digital identity through utilizer friconcludely platforms and multilingual support. In Europe, GoDaddy has localized its services for key markets including Germany France and Spain, providing region specific domain extensions and compliance with local data regulations. To strengthen its position, GoDaddy enhanced its GDPR compliant WHOIS privacy service across all European domains in early 2025 and launched an AI powered domain suggestion engine that accounts for linguistic nuances in European languages. These initiatives reinforce its role as an accessible gateway to the digital economy for European SMEs seeking reliable and intuitive online presence solutions.

- IONOS SE, headquartered in Germany, is a leading European web hosting and domain services provider that combines deep regional expertise with scalable cloud infrastructure. As part of the United Internet Group, IONOS serves over three million customers across Europe with a strong focus on data sovereignty and regulatory compliance. The company plays a significant role globally by championing EU hosted infrastructure and promoting the .de and .eu namespaces as symbols of digital trust. In 2025, IONOS introduced a sovereign domain management platform featuring conclude to conclude encryption and integration with national eID systems like Germany’s BundID. It also expanded its cybersecurity suite to include automated DNSSEC activation and phishing detection, aligning with EU cybersecurity directives and solidifying its reputation as a secure, locally rooted alternative to US based registrars.

- OVHcloud SA is a French multinational cloud computing and domain services provider known for its commitment to European digital sovereignty and infrastructure indepconcludeence. Operating one of the largest networks of data centers in Europe, OVHcloud offers domain registration alongside hosting and bare metal solutions, emphasizing data residency and transparency. The company contributes globally by advocating for open standards and resisting extraterritorial data requests, positioning itself as a trusted partner for privacy conscious organizations. To reinforce its European leadership, OVHcloud launched a green domain initiative in January 2025, offsetting the carbon footprint of every new .fr and .eu registration through renewable energy investments. It also integrated its domain platform with the EU Digital Identity Wallet framework, enabling seamless authentication for business registrants and advancing its vision of a sovereign, sustainable European internet.

Top Strategies Used by the Key Market Participants

Key players in the Europe domain name market are adopting distinct strategies to navigate regulatory complexity and evolving customer expectations. First, they are prioritizing compliance with the General Data Protection Regulation by implementing robust WHOIS privacy and data minimization practices. Second, they are investing in cybersecurity enhancements such as automatic DNSSEC activation, regisattempt lock features, and real time abutilize monitoring to protect domain integrity. Third, they are localizing services through multilingual interfaces, region specific domain recommconcludeations, and integration with national digital identity schemes. Fourth, they are promoting digital sovereignty by hosting infrastructure within the EU and supporting counattempt code top level domains like .de and .fr. Finally, they are expanding value added services including AI driven domain suggestions, website builders, and email hosting to increase customer retention and lifetime value beyond basic registration.

MARKET SEGMENTATION

This research report on the European domain name market has been segmented and sub-segmented based on categories.

By Deployment

By Type

- Generic TLDs

- Counattempt Code TLDs

By End User

- Enterprises

- Non-profit Organizations

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply