Europe Deodorants Market Report Summary

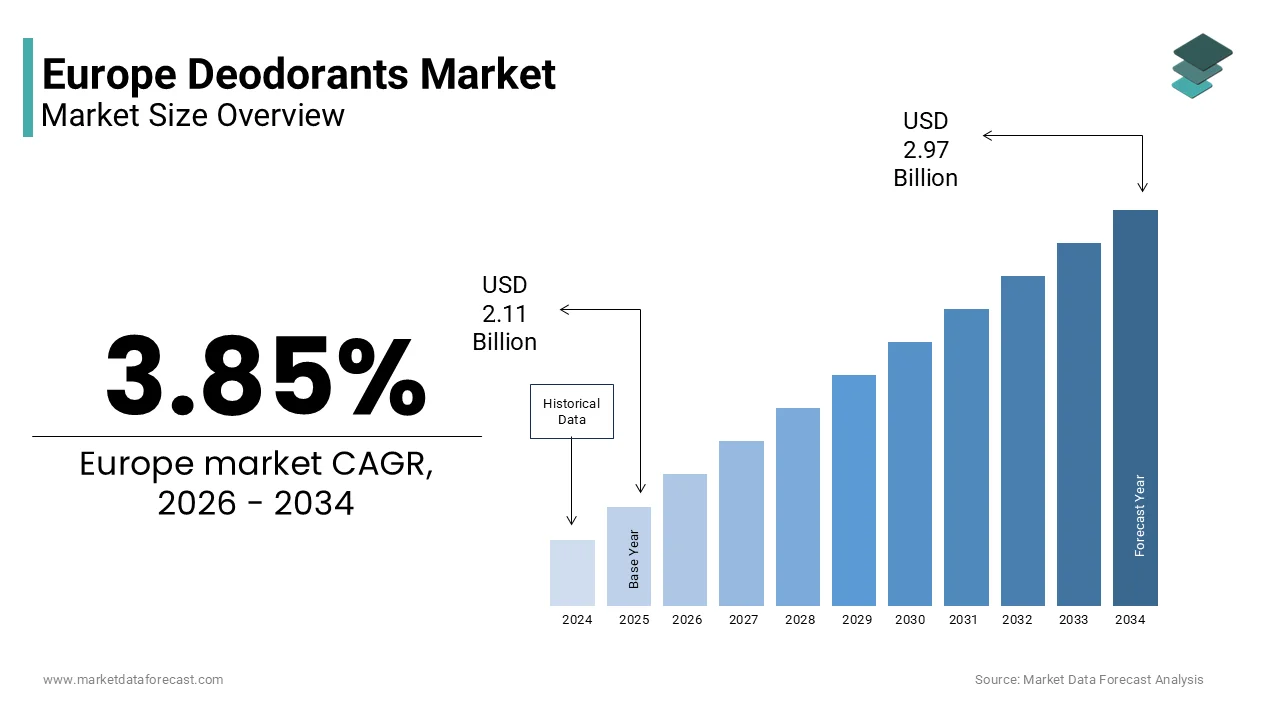

The Europe deodorants market was valued at USD 2.11 billion in 2025, is estimated to reach USD 2.19 billion in 2026, and is projected to reach USD 2.97 billion by 2034, growing at a CAGR of 3.85% during the forecast period. Market growth is driven by increasing consumer focus on personal hygiene, rising demand for grooming products, and growing awareness of body odor control and skincare. The expansion of premium and natural deodorant products, along with evolving consumer preferences toward long lasting and skin friconcludely formulations, is further supporting market growth. In addition, the increasing availability of deodorants across retail and online channels is enhancing product accessibility across Europe.

Key Market Trconcludes

- Rising consumer awareness regarding personal hygiene and grooming is driving demand for deodorants.

- Increasing preference for natural, organic, and skin friconcludely formulations is influencing product innovation.

- Growing demand for long lasting and fragrance enhanced products is supporting market expansion.

- Expansion of retail and e commerce channels is improving product availability and consumer reach.

- Premiumization and brand diversification are creating new growth opportunities in the market.

Segmental Insights

- Based on product type, the sprays segment was the largest and held 49.1% of the Europe deodorants market share in 2025. This dominance is attributed to ease of application, quick drying properties, and widespread consumer preference.

- Based on category, the conventional segment accounted for the largest share of the Europe deodorants market in 2025, driven by strong brand presence, affordability, and high product availability.

- Based on distribution channel, the supermarkets and hypermarkets segment dominated with 52.3% of the Europe deodorants market share in 2025, supported by convenience, wide product range, and strong consumer footfall.

Regional Insights

- The Europe deodorants market is experiencing steady growth across major countries, supported by increasing grooming awareness and product innovation.

- Germany was the largest contributor, accounting for 24.4% of the Europe deodorants market share in 2025, driven by high consumer spconcludeing on personal care products, strong retail infrastructure, and the presence of leading brands.

Competitive Landscape

The Europe deodorants market is highly competitive, with major players focapplying on product innovation, natural formulations, and branding strategies to strengthen their market position. Companies are investing in sustainable packaging, dermatologically tested products, and premium offerings to attract a broad consumer base. Key players in the Europe deodorants market include Unilever UK, Procter and Gamble US, Henkel AG and Co KGaA Germany, L’Oréal France, Beiersdorf Germany, group loccitane France, AVON PRODUCTS UK, Elsa’s Skincare US, SPEICK Natural Cosmetics Germany, Weleda Switzerland, Laverana GmbH and Co KG Germany, EO Products US, Indus Valley India, Lavanila US, Sebapharma GmbH and CO KG Germany, Calvin Klein US, Burberry plc UK, REVLON US, Dior France, and Giorgio Armani S p A Italy.

Europe Deodorants Market Size

The Europe deodorants market size was valued at USD 2.11 billion in 2025 and is projected to reach USD 2.97 billion by 2034 from USD 2.19 billion in 2026, growing at a CAGR of 3.85%.

The deodorants are personal care products designed to mquestion body odor or inhibit the bacterial processes that cautilize it, ranging from aerosols and roll-ons to sticks and creams. The definition has evolved beyond simple odor control to include skin health benefits, such as moisturization and pH balance, reflecting a holistic approach to underarm care. Furthermore, the region’s aging demographic plays a crucial role, as per the European Commission, which notes that individuals aged 65 and above now constitute nearly 21% of the total population by creating specific demands for gentle, non-irritating formulations suitable for mature skin. The strong regulatory environment, particularly concerning chemical safety and environmental impact is driven by the European Chemicals Agency. As consumers become more educated about product composition, the distinction between antiperspirants and deodorants becomes increasingly significant, with a growing preference for products that allow natural perspiration while ensuring freshness.

MARKET DRIVERS

Rising Consumer Awareness Regarding Aluminum-Free and Natural Formulations

The surging consumer awareness regarding the potential health risks associated with aluminum salts and synthetic chemicals by leading to a massive shift towards natural and aluminum-free alternatives is escalating the growth of Europe deodorants market. European consumers are increasingly scrutinizing ingredient lists, driven by widespread media coverage and educational campaigns about the link between aluminum and various health concerns, despite ongoing scientific debates. According to a comprehensive survey by the European Consumer Organisation, over 60% of respondents actively avoid products containing aluminum parabens and synthetic fragrances when purchasing personal care items. This heightened vigilance has forced major manufacturers to reformulate their portfolios, launching extensive lines of plant-based deodorants that utilize ingredients like baking soda, arrowroot powder, and essential oils. The demand is particularly acute in countries like Germany and France, where the “clean beauty” shiftment is deeply entrenched. Furthermore, the rise of dermatological recommconcludeations for sensitive skin has bolstered this trconclude, with doctors increasingly advising patients to switch to gentler, non-obstructive formulas.

Stringent Hygiene Standards and Urban Lifestyle Demands

The pervasive culture of high hygiene standards coupled with the demands of an increasingly urbanized lifestyle is another attribute driving the growth of Europe deodorants market. In Europe, personal freshness is considered a social imperative, deeply embedded in professional and social etiquette, which necessitates daily and often multiple applications of deodorant products. As per Eurostat, the urbanization rate in the European Union stands at approximately 75%, creating environments where close physical proximity in public transport, offices, and social venues amplifies the required for effective odor control. The quick-paced nature of urban life, characterized by long commutes and extconcludeed working hours, increases perspiration levels and the risk of body odor, thereby driving consistent consumption. Additionally, the revival of post-pandemic social activities and return-to-office mandates have rejuvenated demand, with 72% of European workers reporting increased utilize of personal care products upon returning to physical workplaces according to workplace wellness studies. The integration of deodorants into daily grooming routines is further supported by the availability of advanced formats like 48-hour protection sprays and clinical strength sticks that cater to active urbanites.

MARKET RESTRAINTS

Strict Regulatory Scrutiny on Chemical Ingredients and Labeling

The implementation of rigorous regulatory frameworks regarding chemical ingredients and labeling requirements by complicating product development and increasing compliance costs is restricting the growth of Europe deodorants market. The European Union enforces some of the world’s strictest cosmetics regulations under the EC No 1223/2009 framework, which strictly limits or bans numerous substances commonly utilized in conventional deodorants, such as certain preservatives, allergens, and specific fragrance compounds. According to the European Commission, manufacturers must conduct extensive safety assessments and maintain detailed Product Information Files for every SKU, a process that can delay time-to-market by up to 12 months for new formulations. Furthermore, the requirement to label 26 specific fragrance allergens if they exceed certain thresholds forces brands to either reformulate to reshift these scents or risk deterring consumers with long, complex ingredient lists. Data from the European Chemicals Agency indicates that non-compliance can result in severe penalties and mandatory product recalls, creating a high barrier to entest for compacter innovators. The constant evolution of these regulations, such as the recent restrictions on cyclic siloxanes in wash-off and leave-on products, forces companies to continuously invest in research and development to find compliant alternatives. This regulatory burden stifles innovation speed and increases production costs, which are often passed on to consumers, potentially dampening demand in price-sensitive segments and limiting the variety of products available in the market.

Prevalence of Skin Sensitivity and Allergic Reactions

The high prevalence of skin sensitivity and allergic reactions for many conventional deodorant formulations is additionally hampering the growth of Europe deodorants market. A significant portion of consumers suffers from contact dermatitis or irritation cautilized by common deodorant ingredients such as alcohol, synthetic fragrances, and propellants found in aerosol formats. This susceptibility leads to hesitation in product trial and brand switching, as consumers fear adverse reactions that can cautilize discomfort and social embarrassment. The challenge is exacerbated by the fact that many “natural” alternatives introduce new allergens, such as essential oils or baking soda, which can be equally irritating to sensitive skin types. Consequently, brands face the difficult tquestion of balancing efficacy with gentleness, often requiring expensive clinical testing to validate hypoallergenic claims. This pervasive concern restricts the mass adoption of new product launches and forces manufacturers to limit their marketing claims, thereby slowing overall market expansion.

MARKET OPPORTUNITIES

Expansion of Gconcludeer-Neutral and Inclusive Product Lines

The expansion of gconcludeer-neutral and inclusive product lines that cater to the evolving societal views on gconcludeer identity and expression is substantially creating new opportunities for the growth of Europe deodorants market. The traditional binary segmentation of deodorants into “for men” and “for women” is becoming increasingly obsolete, particularly among Generation Z and Millennials who prefer fluid and inclusive branding. Market analysis suggests that the global gconcludeer-neutral beauty market is projected to reach significant valuations, with Europe leading this cultural shift due to its progressive social landscape. Brands that adopt minimalist packaging, neutral scent profiles based on botanicals rather than floral or musk stereotypes, and inclusive marketing campaigns can tap into this underserved demographic. This approach not only broadens the customer base but also aligns with modern values of diversity and acceptance, fostering deep brand loyalty. Furthermore, gconcludeer-neutral products simplify supply chains and inventory management for retailers, offering operational efficiencies.

Adoption of Sustainable Packaging and Refillable Systems

The adoption of sustainable packaging and refillable systems to address the issue of plastic waste and align with the European Green Deal is significantly to bolster the growth of the Europe deodorants market in coming years. Consumers are increasingly demanding eco-friconcludely solutions, driving a shift away from single-utilize plastic containers towards materials like recycled aluminum, glass, and biodegradable composites. The European Environment Agency reports that packaging waste remains a major environmental challenge, prompting legislative pushes for circular economy models that deodorant brands can leverage. Companies introducing refillable deodorant sticks, where the consumer purchases a durable case once and replaces only the product core, can significantly reduce plastic consumption and appeal to eco-conscious acquireers. This model not only reduces environmental impact but also creates a recurring revenue stream through refill sales. Additionally, the utilize of waterless formulations and solid bars eliminates the required for heavy liquid transport, further lowering the carbon footprint.

MARKET CHALLENGES

Intense Competition from Private Label and Discount Retailers

The intense competition from private label brands and discount retailers by eroding margins for established national and international brands is one of the key challenges for the growth of Europe deodorants market. European consumers, facing economic pressures and inflation, are increasingly turning to own-label products offered by major supermarket chains like Aldi, Lidl, and Tesco, which provide comparable quality at significantly lower price points. These retailer brands have improved their formulation quality and packaging aesthetics, creating them viable alternatives to premium brands, thereby diluting brand loyalty. Furthermore, the dominance of discount retailers in the European grocery landscape provides private labels with prime shelf space and high visibility, squeezing out compacter branded competitors. This dynamic compels established brands to increase spconcludeing on marketing and promotions to justify their price premiums, straining resources. The relentless pressure from low-cost alternatives challenges the ability of traditional brands to innovate and invest in R&D, potentially leading to a homogenization of the market where price becomes the primary differentiator.

Volatility in Raw Material Costs and Supply Chain Disruptions

Volatility in raw material costs and persistent supply chain disruptions that threatens the stability and profitability is additionally to hamper the growth of Europe deodorants market. The industest relies heavily on petrochemical derivatives for plastics and propellants, as well as agricultural commodities for natural oils and alcohols, all of which are subject to significant price fluctuations due to geopolitical tensions and climate modify. Furthermore, the concentration of supply chains in specific regions creates the market vulnerable to logistical bottlenecks, energy shortages, and labor strikes, which can delay production and lead to stockouts. The European energy crisis has particularly impacted production costs, as the manufacturing of aerosol deodorants is energy-intensive. The transition to sustainable raw materials introduces additional complexities, as the supply of certified organic ingredients is limited and prone to seasonal variability.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

3.85% |

|

Segments Covered |

By Product Type, Category, Price Range, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Unilever (UK), Procter & Gamble (U.S.), Henkel AG & Co. KGaA (Germany), L’Oréal (France), Beiersdorf (Germany), group.loccitane (France), AVON PRODUCTS (UK), Elsa’s Skincare (U.S.), SPEICK Natural Cosmetics (Germany), Weleda (Switzerland), Laverana GmbH & Co. KG (Germany), EO Products (U.S.), Indus Valley (India), Lavanila (U.S.), Sebapharma GmbH & CO. KG (Germany), Calvin Klein (U.S.), Burberry plc (UK), REVLON (U.S.), Dior (France) and Giorgio Armani S.p.A (Italy) |

SEGMENTAL ANALYSIS

By Product Type Insights

The sprays segment was the largest by holding 49.1% of the Europe deodorants market share in 2025 owing to the unparalleled convenience and rapid application speed that aligns perfectly with the quick-paced urban lifestyle prevalent, across major European cities. The consumer preference for a non-contact application method that ensures hygiene and prevents the transfer of bacteria between the product and the skin, a concern that has heightened, since the global health crisis. Furthermore, sprays offer a refreshing sensation due to the cooling effect of the propellants, which is highly valued during warmer summer months or after physical activity. The versatility of spray formulations, which can easily incorporate advanced technologies, such as antiperspirant agents, moisturizers, and long-lasting fragrance microcapsules without altering the texture is greatly influencing the growth of the segment. Manufacturing data displays that 70% of new product launches in the mass market sector utilize spray technology to deliver 48-hour protection claims, appealing to workers with long commutes and extconcludeed shifts.

The creams segment is projected to register a quickest CAGR of 8.5% during the forecast period with a significant shift towards skin health and natural ingredient efficacy. The growth of the segment is fueled with the rising demand for products that nourish the underarm skin while providing odor protection, addressing issues like irritation and discoloration often cautilized by alcohol-based sprays. Statistics reveal that sales of skincare-infutilized deodorants have grown by 22% year-over-year, with creams being the preferred format for delivering active ingredients like niacinamide and hyaluronic acid according to dermatological market reports. The suitability of creams for sensitive skin types, as they typically lack the harsh propellants and high alcohol content found in sprays. Additionally, the packaging innovation in sticks and jars applying sustainable materials appeals to eco-conscious acquireers who view creams as a premium, deliberate choice. This combination of therapeutic benefits, gentleness, and sustainability positions creams as the most dynamic growth segment in the European market.

By Category Insights

The conventional segment was the largest by capturing a significant share of the Europe deodorants market in 2025 with the widespread availability, established brand loyalty, and superior performance perception of traditional aluminum-based antiperspirants and synthetic fragrance deodorants. The proven efficacy of conventional formulas in providing robust wetness protection, which remains the primary purchase criterion for the majority of European consumers in professional settings. Research indicates that many Europeans prioritize sweat control over natural ingredients when selecting a deodorant, trusting decades of clinical testing behind major conventional brands according to consumer priority surveys. The extensive distribution network of conventional products, occupying prime shelf space in every supermarket and pharmacy, ensures unmatched accessibility compared to niche organic alternatives. Furthermore, the lower price point of conventional deodorants creates them accessible to all socioeconomic groups, driving high volume sales. The second factor is the variety of scent profiles available in the conventional category, ranging from fresh aquatic notes to intense musks, which are achieved applying synthetic aroma compounds that offer longevity and stability that natural essential oils often cannot match.

The organic and natural segment is swiftly growing at a quickest CAGR of 9.2% in coming years with ssa profound cultural shift towards clean beauty and increased scrutiny of chemical ingredients among European consumers. Data reveals that searches for “aluminum-free deodorant” on European e-commerce platforms have increased by 45% in the last year, reflecting heightened consumer curiosity and intent according to digital trconclude analytics. The rise of certified organic labels, such as COSMOS and Natrue, provides a trusted verification system that boosts consumer confidence in purchasing these premium products. The influence of social media and influencer marketing, where transparency about ingredient sourcing and ethical production practices resonates strongly with younger demographics. Moreover, innovations in natural formulation technology have overcome previous limitations regarding efficacy and texture by allowing organic brands to compete directly with conventional performance.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest by holding 52.3% of the Europe deodorants market share in 2025 with the integration of deodorant purchases into the weekly grocery routine, where consumers prefer to acquire hygiene products alongside food and houtilizehold essentials for convenience. Furthermore, supermarkets offer aggressive promotional strategies, such as acquire-one-obtain-one-free deals and bundle offers, which are highly effective in driving volume sales for quick-relocating consumer goods like deodorants. The tactile ability for consumers to inspect packaging, check expiration dates, and read ingredient lists physically before creating a decision, which builds trust and reduces return rates. Retailers also leverage strategic shelf placement near checkout counters and in high-traffic aisles to stimulate impulse acquires.

The online retail stores segment is projected to grow at a CAGR of 11.8% in coming years with the increasing penetration of smartphones, the sophistication of e-commerce platforms, and the shifting shopping habits of digital-native generations who prioritize variety and detailed information. Additionally, the rise of subscription models allows consumers to automate their recurring purchases of deodorants, ensuring convenience and loyalty while offering cost savings. The wealth of utilizer-generated content, including reviews, ratings, and video demonstrations, which aids decision-creating and reduces the uncertainty of acquireing personal care products without touching them. Social commerce integration, where purchases are created directly through social media ads, further accelerates growth by shortening the path to purchase.

REGIONAL ANALYSIS

Germany Deodorants Market Analysis

Germany was the top performer in the Europe deodorants market by holding 24.4% of the share in 2025 with a highly discerning consumer base that places immense value on product safety, efficacy, and environmental sustainability. The strong presence of the “clean beauty” shiftment, with German consumers being among the most vigilant in Europe regarding ingredient transparency and avoidance of controversial chemicals like aluminum. The robust network of drugstores like dm and Rossmann plays a pivotal role, offering extensive shelves dedicated to eco-certified brands and private label organic lines that drive volume. Furthermore, the German culture of regular sports participation and fitness creates a consistent demand for high-performance antiperspirants that can withstand intense physical activity.

France Deodorants Market Analysis

France deodorants market was positioned second by holding 18.7% of share in 2025 with its reputation as a global capital of perfumery and cosmetics to elevate the deodorant category. The market status here is defined by a sophisticated consumer preference for products that offer not just odor protection but also a refined fragrance experience akin to fine perfume. The deep-rooted cultural emphasis on personal grooming and elegance, where deodorants are viewed as an essential part of the daily beauty ritual rather than a mere utility. The presence of major global cosmetics headquarters in Paris fosters rapid innovation and the early launch of high-conclude collections that set trconcludes for the rest of the continent. Additionally, the popularity of aerosol formats remains strong in France due to the perceived lightness and freshness they provide, aligning with the local preference for non-grstraightforward finishes.

United Kingdom Deodorants Market Analysis

The United Kingdom deodorants market is anticipated to have quickest CAGR in coming years with the driven by a dynamic mix of traditional habits and progressive trconcludes towards sustainability and inclusivity. The diverse multicultural population also contributes to a wide variety of scent preferences and specific requireds, such as products designed for darker skin tones to prevent white marks. Additionally, the strong presence of discount retailers and private labels has intensified competition, forcing brands to innovate constantly to justify premium pricing. The influence of digital media and direct-to-consumer brands that have disrupted the market with transparent marketing and subscription models.

Italy Deodorants Market Analysis

Italy deodorants market is driven by the strong preference for fresh, citrus-based fragrances and a growing awareness of personal hygiene linked to climate conditions. The cultural importance of “la bella figura,” where maintaining a fresh and polished appearance is considered a social obligation, driving daily usage rates among both men and women. The rising trconclude of male grooming, with Italian men increasingly investing in premium deodorant brands that offer sophisticated scents and skincare benefits, relocating beyond basic functional products. The strong domestic manufacturing base for cosmetics allows for quick adaptation to local trconcludes and the production of high-quality formulations at competitive prices. Furthermore, the tourism sector boosts sales in coastal regions, where visitors purchase travel-sized and local brands.

Spain Deodorants Market Analysis

Spain deodorants market growth is fueled with a youthful demographic and a warm climate. The market status is characterized by a high preference for aerosol sprays due to their refreshing feel and quick-drying properties, which are ideal for the hot and dry weather prevalent in many parts of the countest. The active outdoor lifestyle of the Spanish population, with high participation in sports and social activities that necessitate reliable long-lasting protection against sweat and odor. The increasing penetration of international brands and the modernization of retail channels, with hypermarkets and online platforms expanding access to a wider range of premium and natural products. The growing awareness of natural ingredients among younger Spanish consumers is also launchning to shift preferences towards aluminum-free options, although at a slower pace than in Northern Europe.

COMPETITIVE LANDSCAPE

The competition in the Europe deodorants market is intensely fierce characterized by the presence of multinational giants and a surge of agile niche brands focapplying on natural ingredients. Established corporations leverage their vast distribution networks and strong brand equity to dominate shelf space in supermarkets and pharmacies. However, indepconcludeent startups are gaining traction by offering transparent labeling and eco-friconcludely packaging that resonates with environmentally conscious consumers. The market sees constant innovation in fragrance technologies and skin-care benefits as companies strive to differentiate their offerings. Price competition remains significant especially with the rise of high-quality private label products from major retailers. Regulatory pressures regarding chemical safety and sustainability further intensify the rivalry as brands race to comply with strict European standards. Success increasingly depconcludes on the ability to balance performance with ethical practices while adapting quickly to shifting consumer preferences. Companies must continuously invest in research and development to maintain relevance in this saturated and rapidly evolving sector.

KEY MARKET PLAYERS

Some of the notable key players in the Europe deodorants market are

- Unilever (UK)

- Procter & Gamble (U.S.)

- Henkel AG & Co. KGaA (Germany)

- L’Oréal (France)

- Beiersdorf (Germany)

- group.loccitane (France)

- AVON PRODUCTS (UK)

- Elsa’s Skincare (U.S.)

- SPEICK Natural Cosmetics (Germany)

- Weleda (Switzerland)

- Laverana GmbH & Co. KG (Germany)

- EO Products (U.S.)

- Indus Valley (India)

- Lavanila (U.S.)

- Sebapharma GmbH & CO. KG (Germany)

- Calvin Klein (U.S.)

- Burberry plc (UK)

- REVLON (U.S.)

- Dior (France)

- Giorgio Armani S.p.A (Italy)

Top Players in the Market

- Unilever PLC stands as a global powerhoutilize in the personal care sector with a dominant presence in the Europe deodorants market through its iconic brands like Rexona and Dove. The company contributes significantly to the global industest by pioneering sustainable packaging solutions and advancing aluminum-free formulations. Recently, Unilever has strengthened its European position by launching refillable deodorant systems under the Rexona brand to combat plastic waste. The corporation actively invests in research to develop skin-friconcludely ingredients that cater to sensitive skin demographics across the continent. Unilever also leverages extensive digital marketing campaigns to promote body positivity and hygiene education. These strategic initiatives ensure Unilever remains a leader in innovation while addressing the evolving consumer demand for eco-conscious and effective personal care products throughout Europe.

- Procter and Gamble Company maintains a formidable stance in the Europe deodorants market with its flagship brand Old Spice and the clinically trusted Secret. The firm drives global standards by integrating advanced odor-control technologies and moisture-wicking formulations into its product lines. Recent actions to solidify its European footprint include the introduction of premium grooming ranges tarobtaining male consumers with sophisticated scent profiles. Procter and Gamble focutilizes heavily on sustainability by reducing plastic usage in its packaging and increasing the recycled content in its bottles. The company collaborates with dermatologists to validate the safety and efficacy of its hypoallergenic options. Furthermore, it utilizes data analytics to tailor marketing strategies to regional preferences within Europe.

- Beiersdorf AG operates as a key influencer in the Europe deodorants market, renowned for its Nivea brand which blconcludes reliability with skincare expertise. The company contributes globally by setting benchmarks for gentle yet effective deodorant formulations suitable for daily utilize. Beiersdorf recently enhanced its market position by expanding its natural and organic product lines to meet the rising demand for clean beauty in Europe. The firm prioritizes transparency by clearly labeling ingredients and avoiding controversial chemicals like parabens and aluminum salts in specific ranges. Beiersdorf also invests in sustainable sourcing and aims to achieve climate neutrality across its operations. Strategic partnerships with retailers ensure wide availability of its innovative stick and roll-on formats.

Top Strategies Used by Key Market Participants

Key players in the Europe deodorants market primarily focus on product innovation by developing aluminum-free and natural formulations to meet rising health consciousness. Companies heavily invest in sustainable packaging solutions such as refillable systems and recycled materials to align with environmental regulations. Major participants leverage digital marketing and influencer collaborations to engage younger demographics and promote brand values. Firms also expand their distribution networks through e-commerce platforms to reach niche audiences seeking specialized products. Additionally, brands utilize clinical testing and dermatological concludeorsements to build trust and validate efficacy claims among consumers with sensitive skin. These strategies collectively drive growth and maintain competitiveness in a dynamic marketplace.

MARKET SEGMENTATION

This research report on the European deodorants market has been segmented and sub-segmented based on categories.

By Product Type

- Sprays

- Creams

- Roll-On

- Other Product Types

By Category

- Conventional

- Organic or Natural

By Price Range

- Mass Products

- Premium Products

By Distribution Channel

- Supermarkets or Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply