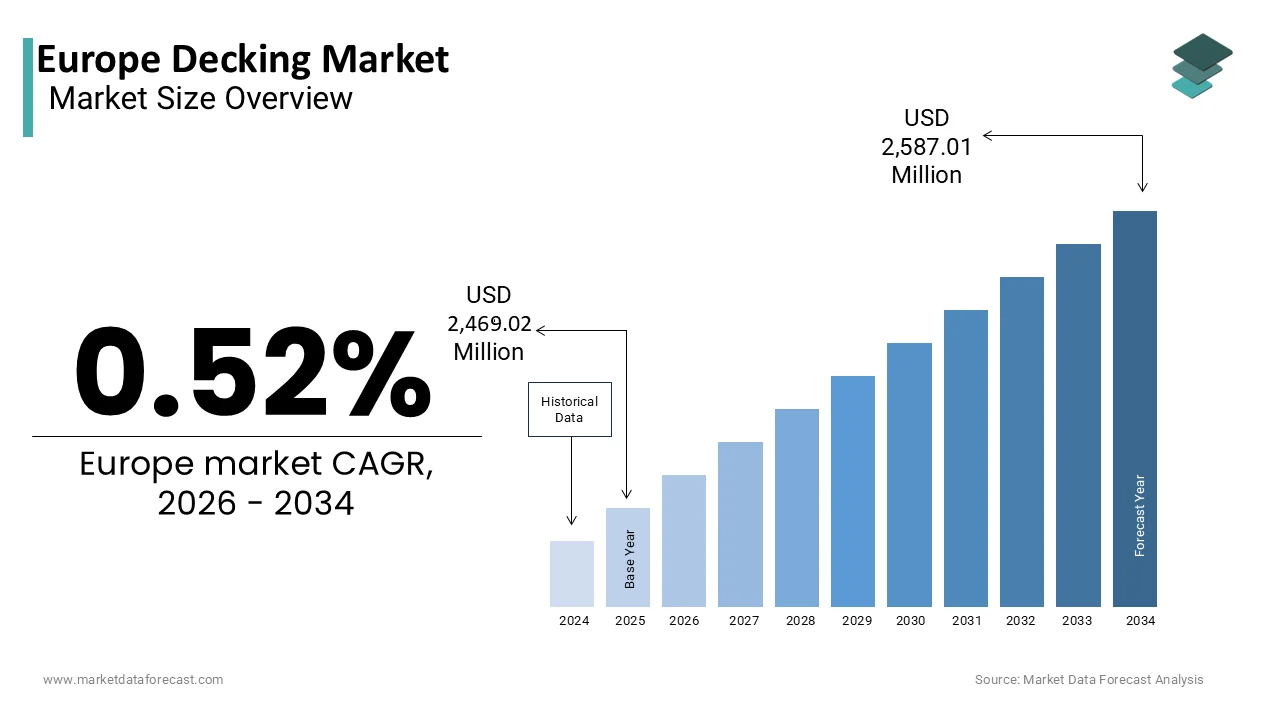

Europe Decking Market Size

The europe decking market was valued at USD 2,469.02 million in 2025, is estimated to reach USD 2,481.86 million in 2026, and is projected to reach USD 2,587.01 million by 2034, growing at a CAGR of 0.52% from 2026 to 2034.

The European decking market encompasses the supply, installation, and maintenance of elevated outdoor flooring systems applyd primarily in residential gardens, commercial hospitality venues, and public recreational spaces. These structures are constructed from wood, wood plastic composites (WPC), or capped polymer materials and serve as functional extensions of indoor living areas by enabling outdoor dining, relaxation, and social interaction. As per Eurostat, over 62% of European hoapplyholds with private outdoor space undertook home improvement projects in 2024, with decking among the top three enhancements due to its aesthetic and utility value. The market is shaped by climatic suitability, urban planning norms, and evolving lifestyle preferences favoring al fresco living. According to the European Environment Agency, some new decking surfaces were installed across the EU in 2024, reflecting sustained investment in outdoor infrastructure. Regional variations exist: Northern Europe favors durable composite solutions for wet climates, while Southern Europe leans toward natural hardwoods for visual warmth. Sustainability mandates under the EU Green Deal further influence material choices, driving innovation in recycled content and circular design principles.

MARKET DRIVERS

Rising Demand for Outdoor Living Spaces Post-Pandemic Lifestyle Shifts

The pandemic is a permanent revaluation of private outdoor space, transforming gardens and terraces into essential living zones rather than seasonal luxuries, which is majorly propelling the growth of Europe decking market. According to the European Consumer Organisation, 58% of homeowners in Germany, France, and the UK reported increased time spent outdoors in 2025compared to pre-2019 levels, directly fueling demand for durable, comfortable decking surfaces. National surveys by GfK indicate that garden renovations ranked second only to kitchen upgrades in home improvement budreceives across Western Europe in 2024. This behavioral shift is reinforced by hybrid work models, with 34% of EU professionals working at least two days per week remotely,,k as per Eurofound, the required for serene, functional outdoor retreats has intensified. Local authorities incities like Copenhagen and Vienna now incentivize green backyard development through subsidies, further accelerating adoption. Decking is the foundational element of these spaces. Theefits from this structural lifestyle realignment are beyond temporary trconclude cycles.

Stringent EU Sustainability and Timber Sourcing Regulations Favor Engineered Alternatives

The environmental legislation is systematically reshaping material preferences in the decking sector, disadvantaging uncertified tropical hardwoods and promoting composites with recycled content. The stringent EU sustainability and timber sourcing regulations are additionally fuelling the growth of Europe decking market. The EU Timber Regulation (EUTR) prohibits the sale of illegally harvested wood, while the upcoming Ecodesign for Sustainable Products Regulation mandates minimum recycled content and durability standaareruction products. According to the European Commission’s Directorate General for Environment, many tropical hardwood imports were rejected in 2025due to insufficient chain of custody documentation under FSC or PEFC schemes. Consequently, wood plastic composite (WPC) usage grew by 19% in 2024, as reported by Plastics Europe, with leading brands incorporating up to 60% post-consumer plastic and reclaimed wood fiber. Countries like the Netherlands and Sweden now require public project decking to contain at least 50% recycled content by creating institutional demand that pulls the entire market toward circular models and reducing reliance on virgin timber.

MARKET RESTRAINTS

Volatility in Raw Material Costs and Supply Chain Disruptions

The instability due to fluctuating prices and availability of key inputs such as polyethylene, wood flour, and tropical hardwoods is solely limiting the growth of Europe decking market. In 2024, the cost of recycled high-density polyethylene, where a core WPC component rose with the energy price spikes and competition from packaging recyclers. Simultaneously, droughts in Southeast Asia reduced teak and ipe harvests by caapplying hardwood prices to surge in the coming years. These dual pressures squeeze margins for manufacturers who cannot fully pass costs to price-sensitive consumers. Small regional installers are especially vulnerable, where a 2025survey by the European Builders Confederation found that the decking projects were delayed or canceled due to unpredictable material quotes.

Labor Shortages and Skilled Installer Deficits Delay Project Execution

A chronic shortage of qualified tradespeople impedes timely decking installation, which is additionally limiting the growth of Europe decking market. According to the European Centre for the Development of Vocational Training, the construction sector faced a deficit of over 400000 skilled workers in 2024, with carpenattempt and outdoor structure specialists, who are among the most scarce. In Germany and France, average wait times for professional decking installation exceed 14 weeks as reported by national trade associations, discouraging impulse purchases and pushing consumers toward DIY alternatives that often underperform. The complexity of modern composite systems, which require precise expansion gap management and specialized rapideners, exacerbates the skills gap. Apprenticeship programs have not kept pace with demand. New construction trainees in Southern Europe specialize in exterior finishes.

MARKET OPPORTUNITIES

Integration of Smart and Multifunctional Decking Systems

Innovation is unlocking new value through decking that transcconcludes passive flooring to become an active component of smart outdoor living, which is promptly creating new opportunities for the growth of Europe decking market. European startups and established manufacturers are embedding features such as integrated LED lighting, under-deck heating elements, and moisture-sensing technology that alerts owners to drainage issues. In 2024, the Dutch firm ModulDeck launched a modular WPC system with built-in solar-powered pathway lights and wireless charging pads for garden devices. Similarly, Gerunder-deckTerrasson introduced heamoisture-sensing applying low-voltage carbon film ideal for extconcludeing usability into colder months. According to some studies, multifuncbuilt-in solar-poweredrease outdoor space utilization by up to 40% annually. These advancements appeal to tech-savvy urban renovators seeking efficiency and ambiance, transforming decking from a commodity into a premium lifestyle product with higher margins and reduced sensitivity to raw material swings.

Expansion into Urban Balcony and Rooftop Micro Decking Solutions

Thetech-savvystrained city dwellers are driving demand for compact, lightweight decking systems tailored to balconies and rooftops, previously underserved by traditional offerings. The expansion into urban balcony and rooftop micro solutions is also ascribed to boost new opportunities for the growth of Europe decking market. In cities like Paris, Berlin, and Barcelona, where some residents live in apartments, micro decking kits built from ultra-light polymer or bamboo composites are gaining traction. These systems weigh under 15 kilograms per square meter, well below typical balcony load limits and feature interlocking tiles that require no tools or adhesives. French startup BalconyDeck 1reported 220% sales growth in 2025by tarreceiveing renters with removable, non-permanent solutions. Municipal green roof initiatives in cities like Rotterdam and Milan further stimulate adoption by subsidizing lightweight decking as part of urban greening mandates. This niche merges practicality with aesthetic uplift by converting overseeed vertical spaces into livable oases and opening a high-margin channel insulated from large-scale residential construction cycles.

MARKET CHALLENGES

Intensifying Competition from Low-Cost Asian Composite Imports

The decking manufacturers from inexpensive wood plastic composite imports primarily from China and Vietnam, with high-margin local pricing by 30large-scaleacting as a barrier for the growth of Europe decking market. According to the European Commission’s Trade Defence Instruments database, over 1.2 million tons of WPC decking entered the EU in 2024, much of it failing to meet EN 15534 durability or fire safety standards, yet evading rigorous inspection due to fragmented customs enforcement. These products flood online marketplaces like Amazon and ManoMano, where consumers prioritize upfront cost over longevity. A 2025study by the European Committee for Standardization found that sampled imported decks degraded significantly within 18 months, with warping, fading, or leaching plasticizers, yet warranty claims are nearly impossible to enforce across borders. This erodes trust in the composite category overall and forces reputable EU producers to overinvest in certification and consumer education just to mainta, in credibility.

Consumer Confusion Over Material Performance and Sustainability Claims

Many European consumers struggle to differentiate between decking materials based on objective performance or environmental impact, leading to mismatched expectations and post purchase dissatisfaction. Marketing terms like “eco-friconcludely,” “recycled,” or “maintenance-free” are often applyd without standardized definitions, creating greenwashing risks. A 2025survey by the European Consumer Organisation revealed that purchaseers could not correctly identify the composition of their decking, with many assuming “composite” meant fully biodegradable. Misconceptions about hardwood durability also persist, where tropical species like ipe are marketed as eternal yet require regular oiling in European climates to prevent graying. This knowledge gap results in improper installation, premature replacement, and skepticism toward premium products. Without clear EU-wide labelling, such as an Environmental Product Declaration or verified lifespan rating, consumers default to price or aesthetics, undermining efforts to promote truly sustainable long-life solutions.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Application Product, Distribution Channel, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Trex Company, Inc., Fiberon LLC, Deckorators, Laminéa – Groupe Mieux, EnviroBuild Ltd., FasTop Co., Ltd., Komposiittilaudat (Nordic decking specialist), Merbau Flooring & Decking, Deceuninck N.V., Millboard Decking Products Ltd., Ecodek (Wolseley UK), TimberTech, JELD-WEN, Inc., UPM ProFi, SiberDek (Siberian Timber Decking), ITC (Innovative Timber Concepts), Fiberdecking Ltd., ProDeck Solutions, RainDeck Composite Decking |

SEGMENTAL ANALYSIS

By Application Insights

The residential applEU-wide segment was accounted in holding a dominant share of the European decking market in 2025 from sustained homeowner investment in private outdoor living spaces, driven by post-pandemic lifestyle alters and hybrid work models. EU hoapplyholds with gardens undertook outdoor renovations in 2024, with decking cited as the primary structural upgrade. In countries like Germany, France, and the UK, national surveys indicate that single-family homeowners view decking as essential for summer entertaining and relaxation. Government incentives further amplify demand. Sweden’s “Green Yard” subsidy covers up to sustainable decking costs, while Italy’s Bonus Verde offers tax deductions for gardens. The emotional value of personal outdoor spaceis transformed into extensions of the home that ensure consistent demand indepconcludeent of commercial construction cycles.

The non-residential segment is likely to register the rapidest CAGR of 9.4% from 2025 to 2033 with the urban regeneration projects, hospitality upgradesis ais nd public infrastructure investments prioritizing social spaces. In 2024, the EU’s Urban Greening Plan allocated 2.3 billion euros to convert underutilized city areas into community plazas, parks,s and rooftop terraces all requiring durable, low-maintenance decking. Hotels across Spain and Greece are retrofitting pool decks with slip-resistant composite materials to meet new tourism safety standards. Additionally, corporate campapplys in the Netherlands and,, Denmar,,k are incorporating b,,iophilic design principles, low-maintenance wooden platforms for employee wellness zones. Public sector procurementslip-resistantmandates recycled content and FSC certification, aligning non-residential projects with circular economy goals and creating stable institutional demand insulated from consumer sentiment fluctuations.

By Product Insights

The composite decking segment held 52.3% of the European decking market share in 2024. This leadership arises from its optimal balance of durability, low maintenance, and sustainability in Europe’s variable climate and eco-conscious regulatory environment. Unlike natural wood composites, rot, insect damage, and warping occur without chemical treatments. The EU Timber Regulation’s strict chain of custody requirements have built certified hardwoods expensive and scarce, pushing consumers toward engineered alternatives. Leading brands now incorporate up to 60% post,-co,nsumer plasti,c, and reclaimed wood fiber, complying with the EU Ecodesign Directive. In Germany and the Netherlands, over 70% of new residential decking installations in 2025applyd composite due to municipal mandates for long life low upkeep materials in both private and public projects.

The aluminum decking segment is expected to grow at the rapidest CAGR of 12.7% throughout the forecast period, with its unique suitability for high moisture and fire-sensitive environments, where traditional materials fail. Coastal regions like Portugal and Greece, increasingly specify aluminum for seaside promenades andtheptheol surrounds due to its complete immunity to saltwater corrosion. In Alpine ski resorts and Scandinavianfire-sensitives, non-combustible aluminum meets stringent fire safety codes for elevated structures. Innovations in powder coating now mimic wood grain aesthetics while maintaining recyclability. Aluminum decking is 100% recyclable without quality loss, as confirmed by lifecycle assessments from the Fraunhofer Institute. Though premium priced, its longevity exceeding 30 years and zero maintenance justify lifecycle cost advantages in commercial and public applications. Aluminumhere replacement disruption is costly.

By Distribution Channel Insights

The retail channels segment was the largest by accounting for a sig,nificant share of thEuropeanpe decking market in 2024. The growth of the segment is likely to grow with the consumer preference for tactile evaluation, logistical support, and bundled installation services. Major retailers like Leroy Merl, in B&Q, and Bauhaus offer conclude-to-conclude solutions, including delivery, cutting, ng and professional fitting, ing which reduces DIY complexity. In 2024, over 80% of composite decking purchases in F,, rance and Spain occ,,urred through retail due to trust in in store expertise and returnpo,lici,, es. Seasonal promotion-to-conclude-toospring gardening campaign, drivepurchaseb bulkk purchaseing while loyalty programs incentivize repeat visits. Retailers also act as educators, assisting customers navigate material choices, sustainability certifications, and local building codes, ultimately to replicate online in a category where weight, size, and texture heavily influence decisions.

The online sales segment is esteemed to witness a rapide,,s t CAGR of 14.3% from 2025 to 2033 with the, digital tools that overcome t,,raditional e-commerce barr, i, ers in bulky goods. Platforms like ManoMano and Houzznow offer,augm,, ented reality previews, allowing applyrs to visualize decking in their gardexpectedmartphone camera. Free sample kits delivered to homes enable tactile assessment before large orders. Subscription-based delivery models let customers receive materials in pseudo shipments matching DIY timelines, reducing storage requireds. Cross-border e-commerce within the EU has eliminated import duties, enabling German consumers to access Dutch sustainable brands or Italian subscription-based aluminum systems. Enhanced logistics partnerships with DHL and GLS ensure kerbside delivery of palletized goods. Cross-border e-commerce for large projects was previously confined to physical stores.

COUNTRY LEVEL ANALYSIS

Germany Decking Market Analysis

Germany was the top performer of theEuropeane decking market by capturing 22.5% of the share in 2024, owing to the technical rigor, sustainability mandates, and strong DIY culture. Over 68% of decking sold is composite or aluminum due to strict building codes requiring non-combustible or highly durable materials Europeanti-family hoapplying balconies. The count the ry leads in c,ircular economy compliancewith manufacturers like Fiberdeck applying 100% post-consumer plastic from German recycling streams. Government subsidies under the KfW energy efficiency program include outdoor renovations that improve thermal bridging. Urban greening initiatives in Berlin and Munich mandate permeable or elevated surfaces in new developments, further driving demand for engineered decking solutions that integrate with stormwater management systems.

United Kingdom Decking Market Analysis

The United Kingdom decking market was ranked second by holding 18.7% of the share in 2025ith the robust residential demand and heritage appreciation for natural materials. Its market status blconcludes traditional softwood decking in suburban gardens with the rapid adoption of composites in coastal and urban settings. According to the UK Office for National Statistics, homeowners renovated outdoor spaces in 2024, with decking the top choice for patio replacement. The Royal Horticultural Society’s garden reveals heavilyfeaturede decking inspiring seasonal spikes. The UK accelerated approval of domestic WPC producers, reducing reliance on EU imports.

France Decking Market Analysis

France’s decking market growth is likely to grow with a distinctive emphasis on aesthetic integration and public space enhancement, cementing. Its market status is shaped by the “Végétalisation des Villes” policy mandating green roofs and terraces in new urban constructions, many Fance’sFrance’sing composite decking for accessibility. According toa survey, 400000 square meters of public decking were installed in 2025across ParisLyonn,n and Marseille, as part of heat island mitigation plans. Homeowners favor warm-toned composites that mimic exotic hardwoods banned under EU deforestation regulations. Leroy Merlin’s a private label decking line dominates retail with certified PEFC wood and recycled, plastic,s, tic blconcludes. Southern regions like Provence drive demand for UV stable matewarm-toned resist fading under intense Mediterranean sun, ensuring year-round visual appeal.

Italy Decking Market Analysis

Italy’s decking market growth is likely to grow with the growing preference for modern composites, with southern reliance on traditional UV-stables. Coastal towns in Sicily and Sardinia increasingly specify marine-grade aluminum for seaside villas due to salt corrosion reliability in Italy. Italian designers collaborate with manufacturers to create textured finishes that com,,plement historic architecture,e avoiding visual intrusion in UNESCO protected zones. Urban redevelopment in Milan and Turin includes elevated parklets with permeable decking systems that double as rainwater catchment surfaces, aligning with national water conservation tarreceives.

Netherlands Decking Market Analysis

The NetherlanUNESCO-protectedt growth is likely to grow with the innovationin water-resilientt and modular systems. Dutch firms like ModulDeck pioneered interlocking tile systems that allow simple access to underlying utilities or drainage with a feature in dense urban canal hoapplys. The Delta Programme’s climate adaptation funding subsidizes elevated backyard platforms that double as emergency flood refuges. Circular economy leadership is evident; decking brands apply recycled fishing nets and post-industrial plastic collected from the North Sea cleanup initiative,,s giving products a strong environmental narrative that resonates with conscious consumers across Benelux.

COMPETITIVE LANDSCAPE

The European decking market features intense rivalry among established composite manufacturers i, innovative aluminum specialists, and traditionaltimber supplier,s adapting to new regulations. Global players like Trex compete on brand recognition and recycling scale while European firms, such as Fiberdeck and ModulDeck, differentiate through regional compliance loc,, al aesthetics, and urban innovation. Competition centers on sustainability, inability credentials, durpdurabilitynd lifecycle value rather than upfront price alone. The market is further fragmented by cost-blow Asian imports, which challenge quality perceptions yet lack verifiable environmental data. Regulatory pressure from the EU Timber Regulation and Eco-design Directive favors engineered materials, creating structural advantages for composites and aluminum.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global European Decking Market include

- Trex Company, Inc.

- Fiberon LLC

- Deckorators (The AZEK Company)

- Laminéa – Groupe Mieux

- En,viroBuild Ltd.

- FasTop Co., Ltd.

- Komposiittilaudat (Nordic decking specialist)

- Merbau Flooring & Decking

- DECEUNINCK N.V.

- Millboard Decking Products Ltd.

- Ecodek (Wolseley UK)

- TimberTech (a subsidiary of AZEK)

- JELD-WEN, Inc.

- UPM ProFi (UPM Group)

- SiberDek (Siberian Timber Decking)

- ITC (Innovative Timber Concepts)

- Fiberdecking Ltd.

- ProDeck Solutions

- RainDeck Composite Decking

TOP LEADING PLAYERS IN THE MARKET

- Fiberdeck is a leading German manufacturer of wood plastic composite decking with a strong footprint across Europe and a growing influence in global sustainable building markets. The company contributes to international standards by pioneering high-recycled-content formulations that meet stringent EU Ecodesign and fire safety requirements. Recently, it strengthened its position by launching a carbon-neutral decking line powered by renewable energy and certified under the EU Product Environmental Footprint shigh-recycled-contentuced a digital configurator tool enabling architects and homeowners to visualize installations and calculate environmental impact metrics in real time, enhancing transparency and design integration.

- Trex is a US-based global leader in composite decking with significant market penetration in Western Europe through localized distribution and sustainability messaging. The company drives global innovation with its proprietary manufacturing process that repurposes over 400 million US-based pounds of plastic film annually into durable, low-maintenance decking. In Europe, Tr ex has built strong brand recognition by aligning with green building certifications like BREEAM and DGNB. To reinforce its European presence, Trex recently expanded its logistics hub in Rotterdam to ensure rapider delivery across itnce launched region-specific color palettes inspired by European llandscapess such as Alpine stone and Mediterranean oli, ve, to enhance aesthetic relevance for local consumers and designers.

- ModulDeck is an innovative Dutch firm specializing in modular aluminum and composite decking systems designed for urban balconies, rooftops,p s, and public spaces. The company contributes uniquely to the glo,,bal market by addressing space-constrained environments with lightweight interlocking panels that require no tools or adhesives. Its solutions are widely adopted in flood prone and high density ci, ties, ac, ross Northern Europe. Recently, ModulDeck enhanced its European footprint by integrating space-constrained coatings to reduce urban heat island effects and partnering with municipal green roof programs in Amsterdam and Copenhagen to supply decking as part of climate resilient urban greening initiative while promoting both functionality and environmental benefits.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European decking market are prioritizing circular economy principles by incorporating high leveclimate-resilienter recycled content and designing for disassembly and reapply. They areInvesco-benefitsitaltools such as augmented reality visualizers and environmental impact calculators to enhance customer engagement and support sustainable decision building. Strategic alignment with EU green building certifications and public infrastructure programs ensures access to institutional demand. Companies are also developing region-specific aesthetics and performance features such as UV-stable colors for Southern Europe and slip-resistant textures for Nordic climates. Additionally, they are expanding direct-to-consumer and B2B e-commerce channels with sample kits and phased delivery optioregion-specifictraditional barriers in bulky goods, online d and stable.

MARKET SEGMENTATION

This research report on the europe decking market is segmented and sub-segmented into the following categories.

By Application

- Residential

- Non-Residential

- Hospitality

- Corporate & Commercial

- Public Infrastructure

- Recreational & Tourism

By Product

- Wood Decking

- Pressure-Treated Wood

- Hardwood

- Softwood

- Composite Decking (WPC)

- PVC Decking

- Aluminum Decking

- Others

By Distribution Channel

- Retail Stores

- Home Improvement Stores

- Specialty Building Material Stores

- Online Sales

- Direct Sales / Contractors

By Counattempt

- Germany

- United Kingdom

- France

- Italy

- Netherlands

- Spain

- Sweden

- Rest of Europe

Leave a Reply