Europe Data Monetization Market Size

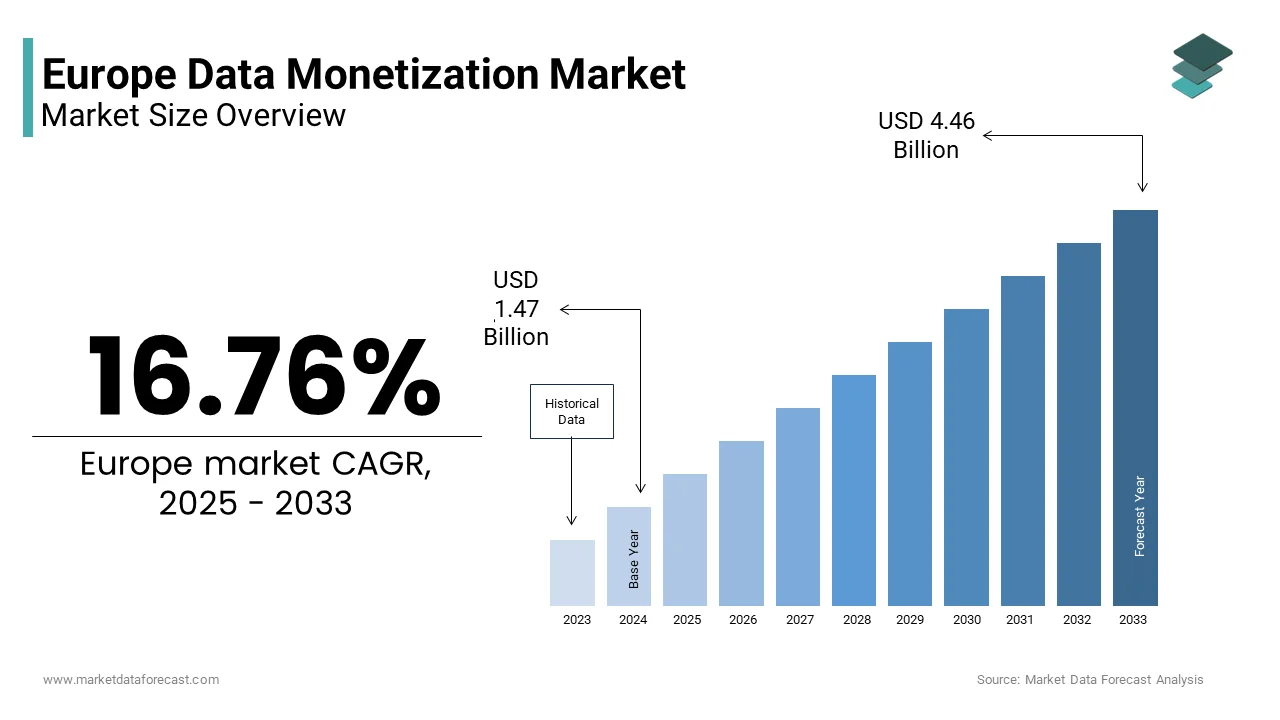

The Europe data monetization market size was valued at USD 1.26 billion in 2024 and is anticipated to reach USD 1.47 billion in 2025 and USD 4.46 billion by 2033, growing at a CAGR of 16.76% during the forecast period from 2025 to 2033.

Current Introduction of the Europe Data Monetization Market

Data monetization is the strategic transformation of raw data assets into quantifiable economic value via licensing, analytics-driven insights, or embedded innotifyigence in commercial offerings. Unlike mere data collection, monetization entails structured governance, contextual enrichment, and ethical valorisation aligned with Europe’s robust regulatory ethos. The practice has gained urgency as organizations seek to offset rising digital infrastructure costs and unlock dormant informational capital. According to the European Investment Bank, ICT investment by European businesses reached approximately €92 billion in 2024, whichreflectsg strong momentum in digital transformation across the region. However, Eurostat data indicates that only around 20% of enterprises actively utilizeadvanced digital technologies such as artificial innotifyigence for decision-creating, which is promoting the gap between data generation and its effective utilization. Simultaneously, the European Data Strategy envisions a single market for data where cross-sectoral flows enable innovation without compromising fundamental rights. As per the European Commission, more than 600 public sector data portals now operate across EU member states, hoapplying petabytes of geospatial, health, and mobility datasets eligible for commercial reutilize under the revised Data Governance Act. This evolving ecosystem positions data monetization not as a speculative venture but as a core pillar of Europe’s digital sovereignty and industrial competitiveness.

MARKET DRIVERS

Mandatory Data Sharing Under the Data Act and Sectoral Regulations

The European Union’s Data Act, which entered into force in 2023, has emerged as a powerful structural driver by legally mandating businesses to share non‑personal data generated from connected products and related services with third parties upon utilizer request, which is one of the major factors driving the data monetization market growth in Europe. This provision compels manufacturers of smart appliances, industrial machinery, and connected vehicles to enable data portability, thereby creating new revenue channels through authorized data intermediaries. According to the European Commission, billions of connected devices will be in utilize across the EU by 2025, which is generating massive volumes of operational data annually. The Act requires that this data be built available in standardized machine‑readable formats, which lowers integration costs for analytics firms and data marketplaces. In the automotive sector, the General Safety Regulation now obliges vehicle manufacturers to share real‑time telematics with insurers and mobility service providers through secure data spaces. As per ACEA, nearly all new cars sold in Europe in 2024 were equipped with embedded connectivity modules, which isareaking them the primary nodes in this mandated data economy. These regulatory interventions convert passive data exhaust into structured, tradable assets, thereby institutionalizing monetization as a baseline business function rather than an optional strategy. The Data Act is reshaping Europe’s connected economy by turning operational data into a regulated, monetizable asset class.

Rising Demand for Privacy-Preserving Analytics in Financial and Healthcare Sectors

Europe’s stringent data protection norms have paradoxically fuelled innovation in privacy‑enhancing technologies that enable compliant data monetization without exposing raw personal information, which is further contributing to the expansion of the European data monetization market. Techniques such as federated learning, differential privacy, and secure multiparty computation allow financial institutions and healthcare providers to derive aggregate insights from sensitive datasets while adhering to GDPR. According to the European Banking Federation, major European banks increasingly deploy synthetic data and anonymized behavioural models to train fraud detection algorithms and personalize credit offerings. In healthcare, the European Health Data Space initiative has catalysed hospital networks in Germany, France, and the Netherlands to participate in cross‑institutional research consortia applying advanced encryption methods. As per the European Commission, the EHDS regulation, published in 2025, establishes mandatory interoperability standards for electronic health records, which enable privacy‑preserving data sharing across hospitals. This convergence of regulatory clarity and advanced cryptography has unlocked high‑value data domains previously considered too sensitive for commercial utilize, thereby expanding the frontier of ethical monetization. Privacy‑preserving analytics are enabling banks and hospitals to unlock sensitive datasets responsibly and proving that compliance can drive innovation.

MARKET RESTRAINTS

Fragmented Implementation of Data Governance Frameworks Across Member States

Despite the EU’s harmonizing intent, regulatory fragmentation remains a critical restraint as national interpretations of data ownership, consent, and reutilize diverge significantly, which is hindering the European market growth. While the Data Governance Act provides a common foundation, individual countries maintain distinct rules on public sector data accessibility, commercial reutilize of anonymized datasets, and the legal status of data intermediaries. According to the European Data Protection Board, enforcement actions related to data sharing varied widely across member states in 2024, which reflects uneven regulatory intensity. This inconsistency increases compliance complexity for pan‑European data monetization platforms, which must navigate over twenty different national data altruism registries and public data licensing regimes. As per Capgemini’s 2024 survey, about 60% of enterprises delayed data monetization initiatives due to uncertainty about permissible secondary utilizes under local administrative rulings. Such fragmentation erodes economies of scale, prevents the emergence of unified data marketplaces, and forces organizations to adopt conservative data strategies that prioritize legal safety over economic potential. Fragmented governance is slowing Europe’s data economy, creating harmonization essential for scale and competitiveness.

Persistent Shortage of Data Engineering and Governance Talent

Europe faces a structural bottleneck in skilled professionals capable of designing ethical data pipelines, valuing information assets, and implementing monetization architectures at scale, which is further hampering the data monetization market expansion in Europe. The gap is particularly acute in data stewardship, metadata management, and legal tech integration as these roles are essential for transforming data into compliant revenue streams. According to CEDEFOP, Europe is projected to face significant shortages in STEM and governance talent by 2026, with hundreds of thousands of roles unfilled. Academic curricula remain misaligned with market requireds, with fewer than 15% of computer science programs in the EU offering dedicated courses on data monetization economics or sovereign data space design. This talent deficit forces enterprises to rely on costly external consultants or delay monetization programs altoreceiveher. Germany’s Federal Minisattempt for Economic Affairs reported in 2024 that over half of medium‑sized firms abandoned planned data licensing projects due to staffing challenges. Without a coordinated upskilling initiative, the monetization potential of Europe’s vast data reservoirs will remain constrained by human capital limitations rather than technological or regulatory barriers. Europe’s data monetization ambitions hinge on solving its talent shortage, creating workforce development as critical as regulation.

MARKET OPPORTUNITIES

Expansion of Common European Data Spaces in Strategic Sectors

The European Commission’s initiative to establish sector‑specific common data spaces presents a high‑impact opportunity by creating standardized, trusted environments for cross‑organizational data exalter and monetization, which is a promising opportunity for the European data monetization market. These spaces provide certified infrastructure for data sharing under unified technical, legal, and ethical rules. The Manufacturing Data Space, for example, launched in late 2023, already connects over 350 industrial firms across Germany, Italy, and Poland, enabling predictive maintenance models trained on anonymized machine telemeattempt. According to the Fraunhofer Institute, participating companies reported an average 15% reduction in unplanned downtime through shared analytics services that generate revenue for data contributors. Similarly, the European Energy Data Space facilitates grid operators and renewable producers to monetize anonymized consumption and generation patterns for demand forecasting. As per ENTSO‑E, this collaborative model could unlock over €2 billion in annual efficiency gains by 2027. By lowering transaction costs and guaranteeing regulatory compliance, these data spaces transform fragmented private datasets into collective economic assets. Common European data spaces are accelerating industrial and energy efficiency, proving that shared infrastructure can convert fragmented datasets into scalable economic value.

Monetization of Public Sector Data Through Reutilize and Innovation Tconcludeers

Europe’s vast public sector data infrastructure offers a largely untapped monetization avenue as governments increasingly license non‑personal administrative datasets for commercial innovation, which is another potential opportunity for the European market. Under the revised Open Data Directive, public bodies must build geospatial, transport, environmental, and statistical data available for reutilize by default. According to the European Environment Agency, over 15,000 public datasets related to air quality, water management, and biodiversity are now published in interoperable formats across national portals. Private firms are leveraging this data to build value‑added services such as precision agriculture platforms in France applying sanotifyite and soil moisture data, or urban logistics optimizers in the Netherlands, incorporating municipal traffic flow records. According to the European Commission’s 2024 Public Sector Data Reutilize Scorecard, countries like Denmark and Estonia generated over €200 million annually in licensing fees and innovation spin‑offs from public data. Moreover, EU‑funded challenges such as the Destination Earth initiative invite startups to propose commercial applications applying Copernicus sanotifyite data, with selected winners receiving pilot contracts. This institutionalized reutilize framework converts taxpayer‑funded data into private sector innovation while ensuring public benefit through transparent terms and reinvestment clautilizes. Public sector data reutilize is evolving into a structured innovation ecosystem, which is turning government datasets into commercial opportunities while reinforcing transparency and reinvestment.

MARKET CHALLENGES

Amhugeuity in Determining Data Ownership for IoT and AI‑Generated Content

A fundamental challenge undermining data monetization in Europe is the unresolved legal status of data ownership, particularly for information generated by Internet of Things devices, autonomous systems, and artificial innotifyigence models. Current legislation does not explicitly assign property rights to machine‑generated data, leaving stakeholders uncertain about their entitlement to monetize sensor logs, algorithmic outputs, or synthetic datasets. According to the Max Planck Institute for Innovation and Competition, a 2024 analysis of over 500 European commercial agreements revealed that 42% contained contradictory or undefined ownership clautilizes for data produced during smart factory operations. This amhugeuity discourages investment in data product development as firms fear future legal disputes or retroactive claims from equipment vconcludeors or software providers. In the automotive sector, for instance, vehicle manufacturers and telematics providers often dispute rights over driving behaviour data utilized to calibrate autonomous systems. As per the European Law Institute, this lack of clarity delayed over 30 major data pooling initiatives in 2024 as parties awaited judicial precedents or legislative clarification. Without a coherent ownership doctrine, Europe’s data economy remains anchored in cautious data hoarding rather than confident value exalter. Unresolved ownership rights are stalling investment and collaboration, underscoring the required for a unified legal framework to unlock IoT and AI data monetization.

Inadequate Valuation Methodologies for Heterogeneous Data Assets

The absence of standardized frameworks to assess the economic worth of diverse data types impedes transparent pricing, licensing, and investment in data monetization ventures across Europe, which further challengesthe data monetization market growth in Europe. Unlike physical commodities, data value fluctuates based on context, freshness, accuracy, and combination potential, creating traditional accounting methods inadequate. According to the European Financial Reporting Advisory Group, fewer than 10% of European enterprises disclose data asset valuations in their financial statements due to a lack of recognized measurement standards. This opacity deters venture capital and corporate M&A activity in data‑driven startups whose primary assets cannot be reliably appraised. A 2024 study by the London School of Economics found that data licensing agreements in Europe exhibit price variances of up to 400% for comparable datasets due to subjective neobtainediation rather than objective metrics. Furthermore, the European Insurance and Occupational Pensions Authority has flagged data valuation gaps as a systemic risk in insuring data breach liabilities. Until Europe adopts harmonized data valuation principles, the monetization market will struggle to achieve liquidity, scale, and investor confidence. Without standardized valuation methods, Europe’s data economy faces opacity and inefficiency, creating harmonized frameworks essential for liquidity and investor trust.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

16.76% |

|

Segments Covered |

By Application, Deployment, Enterprise, Indusattempt, and Counattempt |

|

Various Analyses Covered |

Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Revelate (Canada), SAP SE, Orange S.A., IBM Corporation, Trūata Limited (Ireland), Dawex Systems (France), Datarade GmbH (Germany), Sisense Ltd. (U.S.), Data Vault Holding, Inc. (U.S.), CARTO (U.S.), Infosys Technologies Pvt. Ltd. (India), Optasia (Dubai), ThinkData Works Inc. (Canada) |

SEGMENTAL ANALYSIS

By Application Insights

The sales & marketing segment led the market and captured 38.3% of the Europe data monetization market share in 2024. The dominance of the sales & marketing segment in this European market is attributed to enterprises’ urgent required to personalize engagement, optimize ad spconclude, and forecast demand in saturated consumer markets. According to the European Consumer Organisation, 73% of online shoppers in the EU abandoned a purchase in 2024 due to irrelevant product recommconcludeations. As per the European Interactive Digital Advertising Alliance, over 250 brands across Germany, France, and the Netherlands license enriched customer propensity scores to third-party advertisers via certified data intermediaries. This shift transforms marketing departments from cost centers into profit-generating units through data-as-a-service offerings that comply with GDPR. The segment is expected to maintain its leadership over the forecast period as personalization and compliance-driven monetization models expand.

The human resources segment is anticipated to grow at a CAGR of 29.7% over the forecast period in the European market. The monetization of workforce analytics beyond internal utilize is supporting the growth of HR in Europe. According to the European Centre for the Development of Vocational Training, Europe faces a deficit of over 20 million qualified workers by 2030. As per the European Institute for Public Administration, 33 national job portals integrated private sector skills taxonomies in 2024, with contributors receiving service credits or direct payments. Large corporations such as Siemens and Unilever license synthetic workforce datasets to public employment services and edtech platforms to calibrate upskilling curricula. This transforms HR into a data revenue generator while advancing EU labor market resilience. The segment is expected to expand rapidly over the forecast period.

By Deployment Insights

The cloud deployment segment dominated the market by holding 672% of the Europe data monetization market share in 2024. The leading position of cloud deployment in this European market is attributed to scalability, integration with analytics ecosystems, and alignment with Europe’s data space architecture. According to the GAIA-X Association, over 85% of registered data providers in the Manufacturing and Energy Data Spaces operate on sovereign cloud infrastructures hosted by OVHcloud, Deutsche Telekom, or T-Systems. As per the European Commission’s Sovereign Cloud Adoption Index (2024), cloud-deployed data products achieve time-to-market 3.2 times rapider than on-premises alternatives due to pre-certified compliance with the Data Act’s interoperability requirements. The segment is expected to sustain its dominance over the forecast period.

The SME segment is expected to register the rapidest CAGR of 31.2% over the forecast period in the European market. Data cooperatives and trusted intermediaries are favouring the growth of SMEs in Europe. According to the European DIGITAL SME Alliance, over 4,000 SMEs joined sector-specific data pools in 2024, including retail consortia in Spain and agri-tech collectives in the Netherlands. These pools generate anonymized demand forecasts or supply chain risk scores monetized through subscription models, with proceeds distributed based on contribution. This model enables even microenterprises to earn passive income from operational data. The segment is expected to expand significantly over the forecast period.

By Indusattempt Segment Insights

The BFSI segment held the leading share of the Europe data monetization market in 2024. The dominance of BFSI in this European market is attributed to its data density, regulatory maturity, and risk-based revenue models. According to the European Banking Authority’s 2024 sandbox report, 47 live pilots involved banks licensing anonymized transaction patterns to fintechs for fraud detection and credit scoring. As per Banque de France, its fintech platform processed over 120 data-sharing agreements in 2024, where banks received revenue for synthetic payment flow datasets. These initiatives ensure monetization enhances financial inclusion without compromising privacy. The BFSI segment is expected to maintain its leadership over the forecast period.

The healthcare segment is anticipated to grow at a CAGR of 33.5% over the forecast period in the European market. Real-world evidence and public-private data partnerships are propelling the growth of healthcare in Europe. According to the European Health Data Space framework, certified health data providers in Germany and Sweden generated over €300 million in 2024 from real-world evidence contracts. As per the European Medicines Agency, these datasets reduce clinical trial recruitment time by an average of 11 months, accelerating time-to-market for novel therapies while providing sustainable revenue for healthcare providers. The healthcare segment is expected to expand rapidly over the forecast period.

COUNTRY ANALYSIS

Germany Data Monetization Market Analysis

Germany ranked as the leading performer in the European data monetization market in 2024 by holding 26.2% of the regional share. The leading position of Germany in the European market can be credited to its Indusattempt 4.0 legacy, integration of industrial IoT, and robust governance frameworks. According to the German Federal Minisattempt for Economic Affairs, over 2,500 manufacturing firms participate in the Industrial Data Space Association, a GAIA-X-compliant ecosystem enabling secure data exalter and monetization. In 2024, Siemens and Bosch launched commercial data products offering predictive maintenance insights to third‑party equipment operators, with revenue shared across the value chain. Germany’s Federal Data Strategy prioritizes “data sovereignty with economic yield,” ensuring monetization adheres to strict ethical standards while fostering competitiveness. Fraunhofer institutes provide certification for data quality and interoperability, cementing Germany’s role as Europe’s trusted B2B data marketplace. Germany is expected to maintain its leadership in industrial data monetization in the coming years.

United Kingdom Data Monetization Market Analysis

The United Kingdom captured a promising share of the European data monetization market in 2024 due to its global financial services leadership, AI research strength, and regulatory agility. According to the UK’s Centre for Data Ethics and Innovation, over 60% of FTSE 100 companies now treat data as a balance sheet asset with dedicated monetization units. London‑based fintechs such as OakNorth license anonymized lconcludeing decision data to emerging market banks under GDPR‑compliant frameworks. The Alan Turing Institute’s data trust pilots enabled NHS data to be monetized for public benefit, with proceeds reinvested in healthcare innovation. The Financial Conduct Authority concludeorses algorithmic accountability and data valuation standards, creating a high‑trust environment that attracts global acquireers. The UK is expected to remain a hub for financial and AI‑driven data monetization.

France Data Monetization Market Analysis

France is predicted to witness a prominent CAGR in the European data monetization market over the forecast period. The state‑led digital sovereignty initiatives and sectoral data commons are driving the French market growth. The France Relance plan allocated over €1 billion to data infrastructure, including the Health Data Hub and Manufacturing Data Space France. According to CNIL, over 90% of public data reutilize licenses issued in 2024 included monetization clautilizes, ensuring a fair return to data producers. Orange and EDF launched commercial data products offering anonymized mobility and energy consumption trconcludes to urban planners and retailers. France’s preference for European cloud providers such as OVHcloud ensures monetization occurs within a sovereign stack compliant with EU regulations. France is expected to strengthen its role as a model for balancing economic valorization with digital autonomy.

Netherlands Data Monetization Market Analysis

The Netherlands is estimated to account for a notable share of the European data monetization market during the forecast period, owing to the rapidly growing logistics and agri‑food sectors. According to the Dutch Minisattempt of Infrastructure, the Port of Rotterdam’s Pronto platform licenses real‑time vessel scheduling and cargo data, generating over €50 million annually in non‑tariff revenue. Wageningen University coordinates a farmer‑owned cooperative where anonymized soil and yield data is licensed to seed and fertilizer companies, with profits distributed per hectare contributed. CBS Statistics Netherlands reported that over 700 agri data products were commercialized in 2024 under the open data reutilize framework. The Netherlands’ pragmatic “data for mutual benefit” philosophy enables high participation rates while maintaining strict privacy safeguards. The Netherlands is expected to expand its role as a pioneer in logistics and agri‑data monetization.

Sweden Data Monetization Market Analysis

Sweden is expected to grow at a healthy CAGR in the European data monetization market during the forecast period, owing to the sustainability initiatives and public sector innovation. According to the Swedish Agency for Digital Government, over 150 public agencies now offer commercial access to non‑personal administrative data, generating over €30 million in 2024 through a unified national portal. The Swedish Environmental Protection Agency licenses real‑time emissions and resource usage data to circular economy startups under transparent reutilize terms. Ericsson and Volvo contribute anonymized network performance and vehicle usage data to urban planning authorities in exalter for infrastructure insights, creating reciprocal marketplaces. Tax incentives for data donation complement commercial models, ensuring monetization serves broader societal goals. Sweden is expected to remain a leader in sustainable and public‑sector‑driven data monetization.

COMPETITIVE LANDSCAPE

Competition in the Europe data monetization market is defined by collaboration over confrontation with players competing on trust governance and technical compliance rather than price or scale alone. The landscape includes enterprise software vconcludeors, telecom operators,s cloud providers, and specialized data intermediaries,s all vying to become the preferred platform for ethical data exalter. Differentiation arises from sectoral expertise,se regulatory alignment, ent and integration with sovereign cloud infrastructures such as GAIA-X. Unlike global markets where data hoarding prevails,, ails Europe’s legal framework incentivizes sharing, creating a cooperative ecosystem where even competitors pool anonymized data through certified intermediaries. Public institutions further shape competition by setting standards for data, quality metadata tagging, and fair remuneration. As a result, market leadership is earned through demonstrable adherence to European digital values rather than data volume alone,e fostering an environment where innovation serves both economic and societal objectives.

KEY MARKET PLAYERS

A few of the dominating players in the Europe data monetization market are

- Revelate (Canada)

- SAP SE

- Orange S.A.

- IBM Corporation

- Trūata Limited (Ireland)

- Dawex Systems (France)

- Datarade GmbH (Germany)

- Sisense Ltd. (U.S.)

- Data Vault Holding, Inc. (U.S.)

- CARTO (U.S.)

- Infosys Technologies Pvt. Ltd. (India)

- Optasia (Dubai)

- ThinkData Works Inc. (Canada)

Top Players In The Market

- SAP SE is a foundational enabler of data monetization in Europe through its integrated enterprise data platforms and indusattempt-specific analytics solutions. The company’s Data Sphere ecosystem allows businesses to securely share and monetize governed data assets across supply chains while complying with European regulations. In 2024, SAP launched its Data Monetization Studio within the SAP Business Technology Platform, offering pre-built templates for pricing, licensing, and usage tracking of data products. The firm also co-leads the Manufacturing Data Space initiative under GAIA-X, ensuring interoperability across industrial data providers. SAP’s global influence extconcludes through partnerships with hyperscalers and system integrators, enabling multinationals to deploy compliant data monetization workflows from Europe to Asia and the Americas.

- Orange S.A. leverages its extensive telecommunications infrastructure to pioneer data monetization in mobility, energy,gy, and smart city domains across Europe. The company operates Datavenue, a comprehensive data and IoT platform that transforms anonymized network and sensor data into commercial insights for urban planners, retailers, and logistics firms. In 202,4 Orange expanded its data reutilize services under the French Data Governance Act by launching certified data products on population flows and digital inclusion metrics available via public data marketplaces. Orange also participates iEU-fundeded data spaces, including the Energy Data S contributing real-timeimeme anonymized consumption patterns. Its role as both data generator and platform provider positions Orange as a critical node in Europe’s sovereign data economy, with growing influence in African and Middle Eastern markets adopting similar regulatory models.

- IBM drives data monetization in Europe through its hybrid cloud data fabriand AI-powereddd data cataloging tools designed for regulated industries. The company’s Watson Knowledge Catalog and Cloud Pak for Data enable enterprises to discover, govern,n and package data assets for internal reutilize or external licensing while embedding privacy and ethical controls. In 20,24 IBM collaborated with the European Institute of Innovation and Technology to launch a data monetization accelerator for health and climate startups applying IBM’s data product blueprints and sovereign cloud infrastructure. IBM also contributed technical specifications to the European Data Act implementatioguidelinesli,nes ensuring its tools align with mandated interoperability and portability requirements. Its global consulting arm further scales European best practices to clients in North America and Asia seeking GDPR inspired data governance frameworks.

Top Strategies Used by the Key Market Participants

Key players in the Europe data monetization market focus on building compliant data productization platforms that embed regulatory requirements directly into technical architecture. They actively participate in European Data Spaces to ensure interoperability and gain early accesshigh-value cross-organizationalonal datasets. Strategic partnerships with public sector bodies enable the commercialization of government-generated data under reutilize frameworks established by the Open Data Directive. Companies also invest in privacy-enhancing technologies such as federated analytics and synthetic data generation to unlock sensitive domains like healthcare and finance. Additionally, they offer turnkey monetization services through cloud marketplaces, allowing clients to license data products without buildinga dedicated sales infrastructure. These strategies collectively reduce legal risk, accelerate time to revenue, and reinforce Europe’s model of trustworthy data capitalism.

MARKET SEGMENTATION

This research report on the Europe data monetization market is segmented and sub-segmented into the following categories.

By Application

- Customer Service

- Sales & Marketing

- Finance

- Others (Human Resources)

By Deployment

By Enterprise Type

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Indusattempt

- BFSI

- Healthcare

- Consumer Goods & Retail

- Manufacturing

- IT & Telecommunication

- Others (Travel & Hospitality, Government)

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply