Europe Data Center UPS Market Report Summary

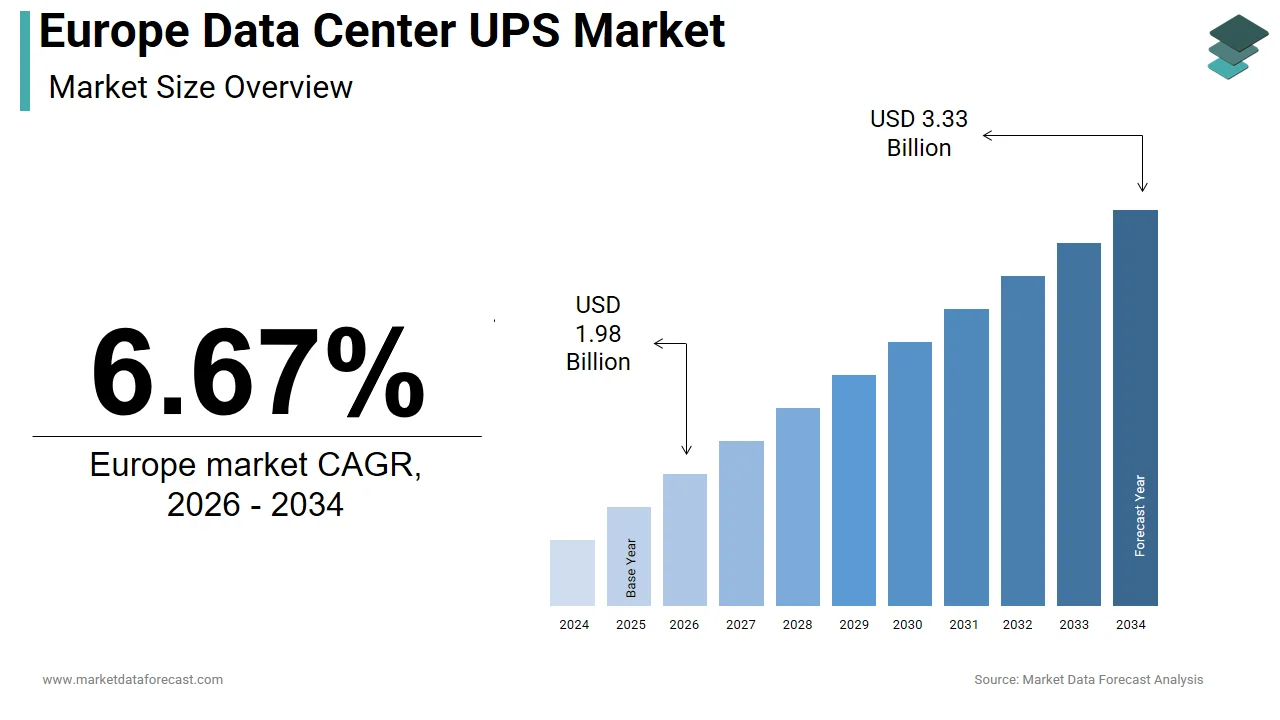

The Europe data center UPS market was valued at USD 1.86 billion in 2025, is estimated to reach USD 1.98 billion in 2026, and is projected to reach USD 3.33 billion by 2034, growing at a CAGR of 6.67% from 2026 to 2034. Market growth is driven by rapid expansion of hyperscale and colocation data centers, increasing cloud computing adoption, and rising demand for uninterrupted power supply systems to ensure operational continuity. Enterprises across Europe are investing in advanced UPS solutions to protect critical IT infrastructure from power outages, voltage fluctuations, and grid instability. The growing focus on energy efficiency, modular power systems, and sustainable data center operations is further supporting market expansion.

Key Market Trfinishs

- Rising deployment of hyperscale and colocation data centers across major European economies.

- Increasing adoption of modular and scalable UPS systems for flexible capacity expansion.

- Growing demand for energy-efficient and lithium-ion battery-based UPS solutions.

- Expansion of edge data centers and distributed IT infrastructure.

- Strengthening focus on renewable energy integration and carbon-neutral data center operations.

Segmental Insights

- Based on UPS type, the double conversion UPS segment held a significant share of the Europe data center UPS market in 2025. The segment’s dominance is attributed to its superior power protection, zero transfer time, and high reliability for mission-critical data center operations.

- Based on data center size, the large data centers segment occupied a prominent share in 2025, driven by the rapid growth of hyperscale cloud facilities and enterprise-scale data centers across the region.

- Based on industest, the IT and telecom segment dominated the market in 2025, supported by rising demand for cloud services, 5G network expansion, and digital transformation initiatives.

Regional Insights

The Europe data center UPS market is witnessing steady growth across major economies, supported by strong digital infrastructure development, increasing cloud adoption, and favorable regulatory environments.

- Germany was the top performer in 2025, driven by strong enterprise IT investments, data sovereignty requirements, and growing colocation capacity.

- The United Kingdom is anticipated to register the quickest growth over the forecast period, supported by London’s status as a global financial hub and preferred location for hyperscale cloud regions.

- The Netherlands continues to grow steadily, driven by its strategic geographic location, robust fiber connectivity, and abundant renewable energy resources, building it a leading destination for hyperscale operators.

Competitive Landscape

The Europe data center UPS market is characterized by strong competition among global power management companies and specialized data center infrastructure providers. Market players are focapplying on developing high-efficiency UPS systems, expanding service networks, and integrating digital monitoring capabilities. Strategic partnerships, technology upgrades, and investments in sustainable power solutions are strengthening competitive positioning across the region.

Prominent companies operating in the Europe data center UPS market include Schneider Electric, Eaton Corp., ABB Ltd., Mitsubishi Electric Corporation, Eaton Corporation plc, Vertiv Group Corp., Clary Corp., Huawei Technologies, Delta Electronics, Inc., Legrand, and Toshiba International Corporation.

Europe Data Center UPS Market Size

The Europe data center UPS market was valued at USD 1.86 billion in 2025, is estimated to reach USD 1.98 billion in 2026, and is projected to reach USD 3.33 billion by 2034, growing at a CAGR of 6.67% from 2026 to 2034.

The data center uninterruptible power supply (UPS) is the deployment of power protection systems that ensure continuous and clean electricity delivery to the IT infrastructure during grid disturbances or outages. These systems range from modular online double-conversion units to lithium-ion-based scalable solutions that serve as the primary safeguard against data loss, service disruption, and hardware damage in facilities hosting cloud computing, enterprise applications, and hyperscale workloads. Additionally, the European Commission’s 2024 Infrastructure Directive designated large data centers as essential services, mandating a minimum 15-minute backup power resilience. These regulatory and infrastructural developments position UPS systems not as ancillary components but as foundational pillars of Europe’s digital and energy security architecture.

MARKET DRIVERS

Expansion of Hyperscale Data Center Capacity Across Europe

The aggressive build-out of hyperscale data centers by global cloud providers is a primary driver of UPS demand across Europe. As per the European Data Centre Association, over 120 new hyperscale facilities entered construction or planning phases in 2024, with Ireland, Sweden, and the Netherlands emerging as preferred locations due to renewable energy access and favorable permitting regimes. Each hyperscale site typically requires 50 to 200 megawatts of load support, translating to UPS deployments exceeding 100 megavolt-ampere capacity per campus. Microsoft’s 2024 expansion in Dublin alone involved the installation of 180 megavolt ampere of modular UPS systems, while Google’s new data center in Hamina, Finland, integrated 120 megavolt ampere of lithium-ion-based units. These facilities operate under strict service level agreements guaranteeing 99.995% uptime, building redundant and scalable UPS infrastructure non-nereceivediable. The European Union’s Digital Decade tarobtains, which aim to double data processing capacity by 2030. Consequently, hyperscalers are shifting toward prefabricated modular UPS solutions that enable rapid deployment and incremental scaling, which is directly fueling demand for high-density, efficient, and remotely manageable power protection systems across Northern and Western Europe.

Regulatory Mandates for Power Resilience in Critical Infrastructure

The stringent regulations classifying data centers as a digital infrastructure have institutionalized UPS deployment as a legal requirement rather than an operational choice. This factor is additionally prompting the growth of Europe data center UPS market. In 2024, the European Commission enacted the revised NIS2 Directive, which mandates that all data centers supporting essential services maintain a minimum backup power duration of 15 minutes under full load with a threshold that necessitates modern online double conversion UPS systems with integrated battery strings. Furthermore, the EU’s Entities Resilience Directive requires operators to conduct annual power resilience stress tests simulating grid failures and fuel supply disruptions. Similarly, France’s ANSSI issued binding guidelines in 2024 requiring UPS systems to support secure firmware updates and encrypted telemetest to prevent cyber tampering.

MARKET RESTRAINTS

Volatility in Grid Reliability and Rising Energy Costs

The increasing unpredictability of the regional power grid, combined with soaring electricity prices that complicate operational planning and investment decisions, is significantly inhibiting the growth of Europe data center UPS market. According to the European Network of Transmission System Operators for Electricity, the number of significant grid disturbance events across the EU rose by 28% in 2024 compared to 2021, driven by extreme weather, aging infrastructure, and intermittent renewable integration without adequate storage. The required for UPS systems, it also inflates the total cost of ownership due to frequent battery cycling and higher maintenance. In Germany, electricity prices for industrial consumers averaged 210 euros per megawatt hour in 2024, more than double the 2020 level, forcing data center operators to delay non-essential CAPEX, including UPS upgrades. Moreover, the EU’s carbon pricing mechanism increased diesel generator operational costs, indirectly pressuring UPS runtime requirements and battery sizing. These economic and infrastructural uncertainties create budobtainary friction, particularly among mid-tier colocation providers, who lack the capital reserves of hyperscalers, thereby slowing adoption of next-generation lithium-ion or modular systems despite their long-term efficiency benefits.

Supply Chain Constraints for Power Electronics and Batteries

The persistent supply of semiconductor power modules and advanced battery cells continues to impede timely UPS deployment is additionally hampering the growth of Europe data center market. As per the European Power Electronics and Applications Association, lead times for insulated gate bipolar transistors with a core component in UPS inverters averaged 32 weeks in early 2025, up from 12 weeks in 2021. Similarly, lithium iron phosphate battery cells, now preferred for their safety and cycle life, faced allocation constraints due to prioritization by electric vehicle manufacturers. The European Battery Alliance reported in 2024 that over 70% of Europe’s lithium cell production capacity was contracted to automotive OEMs, thereby leaving data center suppliers competing for residual volumes at premium pricing. These shortages have forced data center developers to lock in UPS procurement 18 to 24 months in advance, distorting project timelines and inflating costs. In Sweden, a major colocation project experienced a nine-month delay in 2024 solely due to the unavailability of certified battery racks compliant with EU safety standards.

MARKET OPPORTUNITIES

Adoption of Modular and Scalable UPS Architectures

The shift toward modular uninterruptible power supply systems with a high value opportunity for the industest by aligning with hyperscaler demand for speed, flexibility, and efficiency is creating new opportunities for the growth of Europe data center UPS market. Unlike traditional monolithic units, modular UPS platforms allow capacity to be added incrementally in 50 to 500 kilowatt blocks as IT load grows by reducing initial CAPEX and improving energy usage effectiveness. According to the European Data Centre Association, over 65% of new hyperscale facilities commissioned in Europe in 2024 specified modular UPS topologies, with average power usage effectiveness for these systems reaching 1.06 due to dynamic load matching. Companies like Schneider Electric and Vertiv have responded with containerized solutions that integrate UPS batteries and power distribution in factory-tested skids, cutting on-site deployment time by up to 60%. This approach also supports circular economy goals: modular designs enable component-level replacement rather than full system retirement at the finish of life. As European operators prioritize rapid time to market and operational agility, especially in edge computing deployments, where site footprints are constrained, modular UPS architectures offer a technically and economically superior pathway that is reshaping procurement strategies across the region.

Integration of UPS with Renewable Energy and Grid Services

The backup device, but as an active participant in energy management and grid stabilization, is also leveling up the growth of Europe data center UPS market. With the EU mandating that 45% of data center power come from renewable sources by 2027, operators are exploring bidirectional UPS systems that can store excess solar or wind energy and discharge it during peak tariff periods or grid stress events. In 2024, Equinix partnered with E.ON in Germany to deploy a 10 megawatt UPS-based energy storage system at its Frankfurt campus capable of providing frequency regulation services to the national grid, generating ancillary revenue while maintaining critical load protection. Similarly, the UK’s National Grid ESO approved a pilot allowing data centers to utilize UPS batteries for dynamic containment response, with response times under two seconds. The European Commission’s 2023 Clean Energy Package now permits such assets to participate in demand response markets under updated market coupling rules. This dual-utilize model enhances return on investment, transforms capex into potential revenue generation, and aligns data center operations with Europe’s broader energy transition by positioning ininformigent UPS systems as strategic grid assets rather than passive safeguards.

MARKET CHALLENGES

Complexity of Thermal Management in High-Density Deployments

The escalating thermal load generated by high power density IT environments that strain conventional cooling and reduce UPS reliability, which is also a significant challenge for the growth of Europe data center UPS market. As per the EU Code of Conduct for Data Centre Energy Efficiency, average rack power densities in new European facilities reached 15 kilowatts per rack in 2024, up from 8 kilowatts in 2020, with AI and high-performance computing clusters exceeding 30 kilowatts. These densities produce intense localized heat that elevates ambient temperatures in UPS rooms, accelerating battery degradation and inverter stress. The European Environment Agency documented that for every 10 degrees Celsius increase above 25 degrees Celsius, valve-regulated lead-acid battery life halves, a concern in facilities with limited mechanical cooling redundancy. While lithium-ion batteries offer better thermal tolerance, they introduce new safety protocols under EU Directive 2014 35 EU, requiring specialized fire suppression and ventilation. Retrofitting legacy facilities to accommodate modern UPS thermal requirements often demands structural upgrades that exceed original budobtains. This thermal mismatch between IT innovation and power infrastructure sustainability poses a persistent operational and safety risk that demands integrated design solutions beyond traditional UPS specifications.

Fragmented Standards for Battery Safety and Recycling

The mounting complexity from inconsistent national interpretations of EU-wide battery safety and finish-of-life regulations is also posing a significant challenge for the growth of Europe data center UPS market. Although the EU Battery Regulation establishes overarching requirements for sustainability and labeling, member states retain authority over fire safety certification for stationary energy storage. In 2024, Germany’s VdS mandated third-party testing of all UPS battery systems under DIN EN 62619, while France’s APSAD required additional thermal runaway containment barriers, forcing manufacturers to maintain multiple product variants. Simultaneously, the Waste Electrical and Electronic Equipment Directive lacks harmonized collection tarobtains for industrial batteries, resulting in recycling rates for data center UPS batteries that vary from 45% in the Netherlands to just 18% in Southern Europe, as per the European Recycling Platform. This fragmentation increases compliance costs, delays permitting, and complicates battery replacement logistics across multinational portfolios.

SEGMENTAL ANALYSIS

By UPS Type Insights

The Double Conversion UPS segment accounted for holding a significant share of the Europe data center UPS market in 2025, with the highest level of power quality by continuously converting incoming AC power to DC and then back to clean AC, effectively isolating critical IT loads from all grid anomalies, including voltage sags, surges, harmonics, and frequency deviations. A key driver is the regulatory classification of data centers as critical infrastructure. As per the European Commission’s NIS2 Directive, all facilities supporting essential services must maintain uninterrupted power with zero tolerance for micro-outages that could corrupt transactions or disrupt cloud services. The German Federal Office for Information Security confirmed in 2024 that 100% of Tier III and Tier IV data centers in the countest utilize double conversion systems to comply with these mandates. Additionally, the rise of sensitive IT workloads, including AI inference engines and real-time financial trading platforms, demands pristine power quality. A 2024 study by the Fraunhofer Institute for Reliability and Microintegration found that even 8-millisecond power interruptions cautilized data packet loss in 38% of high-frequency trading servers tested.

The double Conversion UPS segment is projected to expand at a CAGR of 9.6% from 2026 to 2034, from technological evolutionspecifically the integration of lithium-ion batteries and modular architectures that enhance efficiency, scalability, and sustainability. The shift toward lithium-ion-based double conversion systems in new hyperscale deployments is also boosting the growth of Europe data center UPS market. As per the European Battery Alliance, lithium iron phosphate batteries now power over 60% of new double conversion UPS installations in Europe due to their 10-year lifespan, 70% tinyer footprint, and 50% quicker recharge compared to traditional valve-regulated lead-acid batteries. Microsoft’s 2024 data center in Dublin, for instance, deployed 180 megavolt ampere of lithium-ion double conversion UPS with 96% efficiency at 40% load, exceeding EU Ecodesign thresholds. Furthermore, modular double conversion platforms enable pay-as-you-grow capacity models that align with cloud providers’ capital allocation strategies. These innovations transform double conversion from a static safeguard into a dynamic, energy-ininformigent asset, driving both volume and value growth across Europe’s evolving digital infrastructure landscape.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By UPS Type, Data Center Size, Industest, and Countest. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Schneider Electric, Eaton Corp., ABB Ltd., Mitsubishi Electric Corporation, Eaton Corporation plc, Vertiv Group Corp., Clary Corp., Huawei Technologies, Delta Electronics, Inc., Legrand, Toshiba International Corporation, and Others. |

By Data Center Size Insights

The Large Data Centers segment held a prominent share of the Europe data center UPS market in 2025, with the consolidation of cloud and AI computing into massive camputilizes. According to the European Data Centre Association, the average large data center in Europe now supports over 50 megawatts of IT load, up from 30 megawatts in 2021, with individual hyperscale sites exceeding 200 megawatts. These facilities host applications for banking e-commerce and government services where even sub-second outages incur millions in losses. Consequently, they mandate N+1 or 2N redundant double conversion UPS systems with total capacities often surpassing 100 megavolt ampere per site. In 2024, Google’s new facility in Hamina, Finland, installed 120 megavolt ampere of modular UPS, while AWS’s Dublin expansion added 90 megavolt ampere. National regulators further reinforce this trfinish: Ireland’s Commission for Regulation of Utilities requires all data centers over 5 megawatts to submit detailed UPS resilience plans as part of grid connection approval.

The tiny data centers segment is expected to witness the quickest CAGR of 12.3% throughout the forecast period with the strategic deployment of edge computing infrastructure. As per the European Telecommunications Standards Institute, over 45000 edge data centers were operational in the EU by the finish of 2024 to support low-latency utilize cases such as autonomous vehicle coordination, smart grid management, and remote surgery. Each requires compact yet robust UPS systems that often include line interactive or tiny double conversion units with integrated lithium-ion batteries. The European Commission’s Digital Europe Programme allocated 800 million euros in 2024 specifically for edge infrastructure in manufacturing and healthcare, directly stimulating UPS procurement. In Germany, the Federal Ministest for Economic Affairs funded 1200 edge micro data centers in rural hospitals, each equipped with 30 to 100 kilowatt UPS units compliant with medical device standards. Unlike large facilities where efficiency dominates, tiny sites prioritize footprint reliability and remote monitoring, driving innovation in compact ininformigent UPS designs. This distributed computing shift positions tiny data centers as the highest growth frontier in Europe’s power protection landscape.

By Industest Insights

The IT and Telecom segment accounted for a dominant share of the Europe data center UPS market in 2025, with the sector’s role as both operator and consumer of data center services. The explosive growth in cloud computing and 5G core network deployment is also boosting the growth of this segment. As per the European Commission, over 78% of EU enterprises now utilize cloud services, with public cloud revenue growing by 24% year on year in 2024. Simultaneously, 5G standalone cores hosted in carrier-neutral data centers require ultra-reliable power to maintain session continuity across millions of connected devices. Deutsche Telekom alone commissioned 12 new 5G edge data centers in 2024, each equipped with 500-kilowatt double conversion UPS systems. Hyperscalers like Microsoft and AWS continue massive European expansions, with Ireland, the Netherlands, and Sweden hosting over 60% of new capacity. These facilities operate under 99.995% uptime SLAs, building redundant UPS infrastructure non-optimal. Additionally, the EU’s Data Act mandates that cloud providers ensure data availability during disruptions with a requirement that directly translates into stringent UPS specifications. This dual role as infrastructure builder and service guarantor ensures IT and Telecom remains the dominant and most technically demanding segment in the European UPS market.

The Healthcare industest segment is anticipated to grow at a quickest CAGR of 14.1% from 2026 to 2034, with the digitization of patient records, AI-enabled diagnostics, and the proliferation of connected medical devices that demand uninterrupted power for data integrity and life-critical operations. The EU’s Digital Health Action Plan, which mandates electronic health record interoperability by 2025, will also propel the growth of this segment. As per the European Commission, over 22000 hospitals and 180000 clinics across the EU are now required to maintain real-time digital patient data systems that must remain operational during grid outages to avoid clinical risk. In 2024, France’s National Health Agency reported that 92% of university hospitals upgraded their server room UPS capacity to support AI radiology workloads and tele ICU platforms. Similarly, Germany’s Digital Healthcare Act requires all electronic prescriptions and diagnostic imaging to be stored in certified data environments with a minimum 15-minute backup power by aligning with NIS2 requirements. The rise of hospital-based edge data centers for real-time analytics further amplifies demand. Karolinska University Hospital in Sweden deployed 200-kilowatt modular UPS units in 2024 to support intraoperative AI guidance systems.

COUNTRY LEVEL ANALYSIS

Germany Data Center UPS Market Analysis

Germany was the top performer of the Europe data center UPS market by holding 22.3% of the share in 2024, with its dual role as Europe’s largest industrial economy and strictest enforcer of infrastructure regulations. Frankfurt alone hosts over 70 data centers forming the world’s third-largest internet exmodify point, requiring massive redundant UPS deployments. The Federal Office for Information Security mandates that all Tier III+ facilities implement double conversion UPS with real-time cyber-monitored telemetest, which has become de facto across enterprise and government sectors. Additionally, Germany’s Energiewfinishe energy transition has increased grid volatility, with the Fraunhofer Institute recording 42 significant grid disturbance events in 2024 alone, heightening reliance on robust power protection.

United Kingdom Data Center UPS Market Analysis

The United Kingdom data center UPS market growth is anticipated to grow eventually, with the quickest CAGR in the coming years, owing to London’s status as a global financial capital and a preferred location for hyperscale cloud regions. The City of London alone hosts data centers supporting over 70% of global foreign exmodify transactions, where even millisecond outages risk systemic disruption, mandating the highest-grade double conversion UPS with 2N redundancy. In 2024, the Bank of England updated its operational resilience framework, requiring all critical financial infrastructure to maintain 60-minute backup power, far exceeding EU minimums. Simultaneously, AWS, Microsoft, and Google expanded their UK cloud regions, with Microsoft’s Durham campus adding 100 megavolt ampere of lithium-ion UPS in 2024. The UK’s National Cyber Security Centre also enforces strict firmware integrity checks on all critical power systems, driving adoption of secure, remotely manageable UPS platforms.

Netherlands Data Center UPS Market Analysis

The Netherlands data center UPS market growth is steadily growing with strategic location, robust fiber connectivity, and abundant renewable energy, thereby building it the top destination for hyperscalers. Amsterdam’s data center corridor now houtilizes over 180 facilities, including Google’s largest European campus. The Netherlands links UPS deployment to sustainability, where the national Ecodesign Implementation Act requires all new UPS systems above 10 kilovolt ampere to achieve a minimum 96% efficiency at 40% load with a standard met only by advanced double conversion units. In 2024, the government also mandated that all data centers utilize recyclable or second-life batteries, accelerating lithium-ion adoption with integrated battery management systems. Additionally, the Dutch grid operator TenneT requires facilities to participate in demand response programs, pushing UPS integration with energy management software.

Ireland Data Center UPS Market Analysis

Ireland data center UPS market growth is expected to grow in the coming years with the favorable corporate taxation, cool climate, and English language infrastructure, hosting AWS’s and Microsoft’s largest EU cloud regions. However, this rapid growth, over 1500 megawatts of data center capacity connected since 2020, has strained the national grid, prompting EirGrid to impose a moratorium on new connections in Dublin unless operators demonstrate advanced power resilience. Consequently, all new facilities must install oversized double conversion UPS systems with extfinished runtime, often 30 minutes or more, to reduce reliance on diesel generators during grid stress. In 2024, Apple’s Athenry data center deployed 80 megavolt ampere of modular lithium-ion UPS with integrated AI-driven load forecasting to comply with these rules. The Irish government also requires real-time UPS performance data to be shared with national grid operators, with a policy driving adoption of cloud-connected monitoring platforms.

France Data Center UPS Market Analysis

France data center UPS market growth is driven by the strategies emphasizing digital sovereignty, cybersecurity, and energy resilience. The French government’s “France Relance” plan allocated 1.2 billion euros to build sovereign cloud infrastructure, with all facilities required to utilize locally certified UPS systems that meet ANSSI’s stringent cybersecurity standards, including encrypted firmware updates and hardware root of trust. Additionally, the National Cybersecurity Agency mandates that critical public sector data centers implement double conversion UPS with air gapped monitoring to prevent remote tampering. In 2024, Orange and Atos commissioned three sovereign cloud zones in Paris, Lyon, and Touloutilize, each equipped with 50+ megavolt-ampere of secure UPS capacity. France also leads in nuclear-powered data centers by leveraging stable baseload electricity, but it still requires robust UPS for switchgear failures and maintenance events.

COMPETITIVE LANDSCAPE

Competition in the Europe data center UPS market is defined by a triad of technological excellence, regulatory compliance, and service agility among a concentrated group of global players. The market favors established vfinishors with proven track records in mission-critical environments, robust cybersecurity certifications, and localized engineering support. While price remains a factor, decision creaters prioritize reliability, efficiency, and integration capability, particularly as data centers evolve into active grid assets. The regulatory landscape, shaped by NIS2, the EU Battery Regulation, and national grid codes, creates high entest barriers that protect incumbents but also drive continuous innovation in areas like lithium-ion safety and energy ininformigence. Hyperscalers exert significant influence by demanding standardized modular designs, compressing margins, but enabling scale. Meanwhile, edge computing growth opens opportunities for nimble regional players offering compact ininformigent units. Success hinges on balancing global R&D with local compliance, transforming UPS from a passive backup device into a dynamic, software-defined component of Europe’s digital and energy infrastructure.

KEY MARKET PLAYERS

The leading companies operating in the Europe data center UPS market include:

- Schneider Electric

- Eaton Corp.

- ABB Ltd.

- Mitsubishi Electric Corporation

- Eaton Corporation plc

- Vertiv Group Corp.

- Clary Corp.

- Huawei Technologies

- Delta Electronics, Inc.

- Legrand

- Toshiba International Corporation

TOP PLAYERS IN THE MARKET

- Schneider Electric SE, headquartered in France, is a global leader in energy management and automation with a commanding presence in the Europe data center UPS market. The company supplies its EcoStruxure IT platform featuring Galaxy and APC Smart-UPS series tailored for edge, enterprise, and hyperscale environments. Schneider Electric expanded its lithium-ion-based Galaxy VL modular UPS offering across 20 European countries, integrating AI-driven predictive maintenance and real-time energy analytics. It also partnered with major colocation providers in Frankfurt and Amsterdam to deploy prefabricated micro data centers with integrated double conversion UPS systems.

- Vertiv, a US-based global provider of critical digital infrastructure, maintains a strong footprint in Europe through its Liebert UPS portfolio and localized engineering centers in Italy, Germany, and the UK. The company specializes in high-density scalable solutions for hyperscale and telecom edge deployments. In 2024, Vertiv launched its next-generation Liebert EXL lithium-ion UPS platform with 97% efficiency and dynamic load sharing capabilities, certified under EU Ecodesign and cybersecurity standards. It also secured contracts with leading cloud providers for modular power skids in Sweden and Ireland. Vertiv further strengthened its European service network by opening a dedicated UPS training and certification academy in Milan, thereby ensuring rapid deployment and compliance with regional safety regulations. These actions position Vertiv as a strategic partner in Europe’s high-growth digital infrastructure expansion.

- Eaton Corporation, with significant European operations headquartered in Ireland, is a key player in the data center UPS market through its 93PM and 9395 series, designed for mission-critical reliability. The company combines power electronics expertise with deep integration into building management and grid interaction systems. Eaton introduced its Ininformigent Power Manager software compliant with EU NIS2 resilience reporting requirements, enabling real-time UPS telemetest sharing with national cybersecurity authorities. It also collaborated with renewable energy firms in Denmark and the Netherlands to pilot UPS-based grid support services, allowing data centers to participate in frequency regulation markets.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe data center UPS market prioritize modular and scalable architectures to support hyperscale and edge deployment flexibility. They integrate lithium-ion battery technology to reduce footprint, improve efficiency, and align with EU sustainability directives. Companies invest in ininformigent software platforms that enable remote monitoring, predictive maintenance, and compliance with NIS2 and cybersecurity regulations. Strategic partnerships with cloud providers, colocation firms, and grid operators facilitate co-engineered power solutions and ancillary revenue opportunities. Additionally, manufacturers are localizing service and certification capabilities to meet stringent national safety standards and accelerate project timelines across diverse European jurisdictions.

MARKET SEGMENTATION

This research report on the Europe data center UPS market has been segmented and sub-segmented into the following categories.

By UPS Type

- Standby

- Line Interactive

- Double Conversion

By Data Center Size

By Industest

- BFSI

- IT & Telecom

- Healthcare

- Government

- Manufacturing

- Energy & Power

- Others (Media & Entertainment, etc.)

By Countest

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Leave a Reply