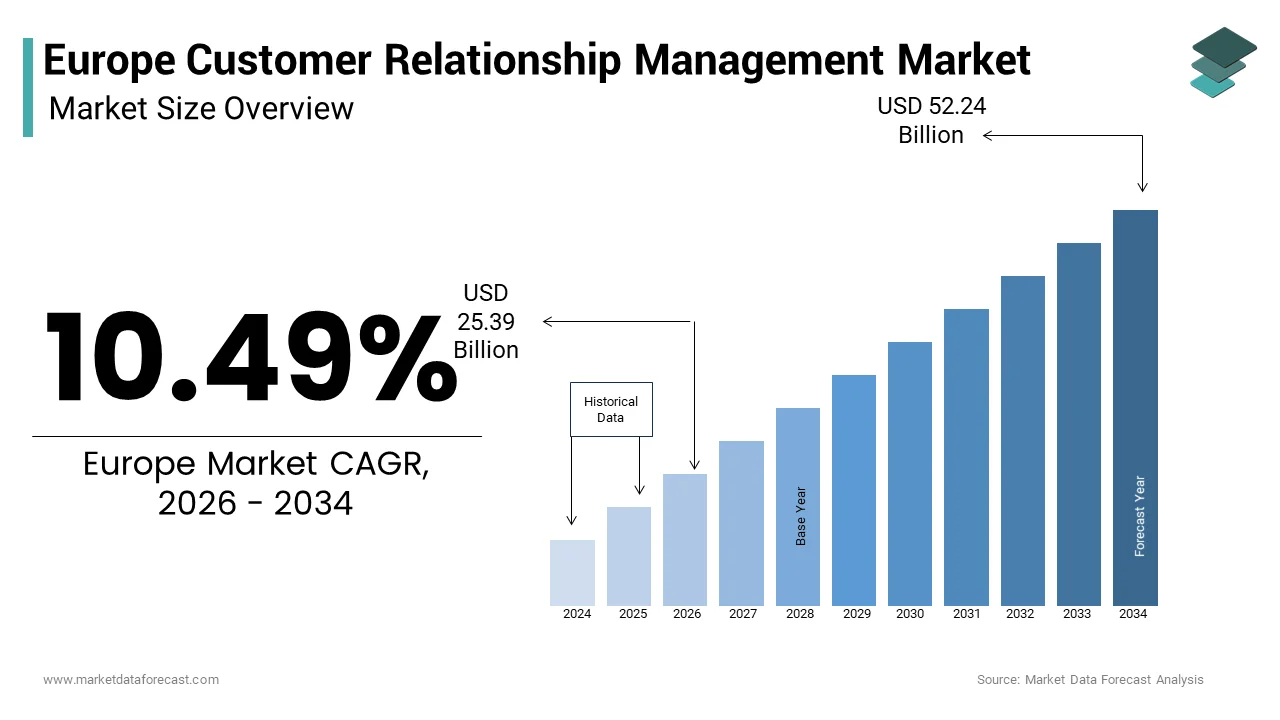

Europe Customer Relationship Management Market Size

The Europe customer relationship management market size was valued at USD 22.97 billion in 2025 and is anticipated to reach USD 25.39 billion in 2026 to reach USD 52.24 billion by 2034, growing at a CAGR of 10.49% during the forecast period from 2026 to 2034.

Customer relationship management represents the sophisticated ecosystem of software platforms and strategic frameworks designed to manage all interactions between enterprises and their current or potential customers across the European continent. This domain has evolved from simple contact databases into comprehensive innotifyigence hubs that leverage artificial innotifyigence, predictive analytics, and omnichannel integration to personalize every touchpoint of the customer journey. The landscape is uniquely shaped by the stringent requirements of the General Data Protection Regulation which mandates rigorous consent management and data sovereignty for all customer information processed within these systems. As per Eurostat statistics, a large majority of enterprises in the European Union utilized cloud computing services in the last measured period, with customer relationship management being the most widely adopted application category. According to the European Commission, the digital decade tarreceives aim for all key public services to be available online by 2030, which further accelerates the adoption of advanced CRM solutions in the public sector. The market now functions as the central nervous system for the Digital Single Market, enabling seamless cross border trade and fostering a culture of data driven decision building. This evolving definition includes conversational AI and automated workflow engines that allow businesses to anticipate customer requireds before they are explicitly stated. The sector operates within a highly regulated environment, where trust and transparency determine competitive advantage in the modern economy.

MARKET DRIVERS

Mandatory Compliance with Open Banking and PSD2 Regulations

The rigorous enforcement of the Revised Payment Services Directive and the broader Open Banking framework are primarily driving the growth of the European customer relationship management market. These regulations mandate that organizations provide secure application programming interfaces to third party providers and maintain a unified view of customer financial data across multiple channels, which is a capability that legacy systems often lack without extensive retrofitting. According to the European Banking Federation, banks in the European Union have accelerated their CRM replacement projects specifically to meet regulatory deadlines and avoid severe penalties. The required to share customer data securely while maintaining granular consent management requires a fundamental architectural shift toward API led connectivity, which modern CRM solutions provide natively. As per the Open Banking Implementation Entity, the number of API calls in the UK has reached extremely high levels annually, which is creating immense pressure on backconclude systems to process these requests in real time and update customer profiles instantly. Organizations unable to adapt risk losing their license to operate or facing reputational damage due to service outages. Furthermore, the directive encourages competition by allowing non-bank entities to initiate payments, which is forcing traditional firms to upgrade their CRM to remain competitive in speed and functionality.

Surge in Demand for Hyper Personalized Customer Experiences

The exponential growth in consumer expectation for hyper personalized interactions acts as a powerful driver forcing the adoption of advanced CRM platforms capable of analysing vast datasets to deliver tailored content and offers in real time, which is further contributing to the expansion of the European customer relationship management market. European consumers increasingly demand that brands understand their preferences, purchase history, and context across all channels, requiring CRM systems that integrate artificial innotifyigence and machine learning for predictive modeling. As per the European Consumer Organisation, consumers in the European Union expect companies to recognize their history and preferences across all interaction points, creating immense pressure on organizations to invest in integrated solutions. According to McKinsey and Company, organizations implementing personalization strategies through advanced CRM have reported measurable improvements in revenue and customer satisfaction compared to those utilizing disjointed data. The complexity of managing these diverse streams requires sophisticated segmentation algorithms and real time analytics, which are core features of modern CRM software. Furthermore, the rise of social commerce in Europe has built social media messaging a critical support channel, which is requiring platforms that can handle high volume text-based interactions alongside voice calls.

MARKET RESTRAINTS

Stringent Data Privacy Regulations and Sovereignty Concerns

The rigorous enforcement of the General Data Protection Regulation and varying national data sovereignty laws creates significant friction for the deployment of global customer relationship management solutions and restricts data flow across borders, which is primarily impeding the regional market growth. Organizations must ensure that all customer data, including personal identifiers and interaction logs, are stored and processed within specific jurisdictions, complicating the architecture of cloud-based CRM that often rely on distributed global server networks. According to the International Association of Privacy Professionals, many European chief information officers cite compliance with data residency requirements as a major barrier to adopting advanced cloud CRM technologies. This regulatory landscape forces vconcludeors to build localized data centers or partner with local providers, which is increasing operational costs and limiting the economies of scale typically associated with global cloud platforms. The European Data Protection Board frequently issues guidance that tightens restrictions on international data transfers, which is creating uncertainty for multinational corporations seeking to centralize their customer data. Such fragmentation discourages compacter vconcludeors from entering multiple markets and slows the adoption of innovative features that require cross border data processing for training artificial innotifyigence models.

Acute Shortage of Skilled CRM Technology Talent

A critical deficit in professionals possessing specialized skills in CRM administration, artificial innotifyigence integration, and data analytics severely restricts the ability of organizations to fully leverage advanced customer engagement platforms, which is also impeding the regional market expansion. The rapid evolution of CRM technology has outpaced the development of educational curricula and corporate training programs, which is leaving a wide gap between available tools and the expertise required to manage them. As per the Centre for European Policy Studies, the European Union faces a significant shortfall of digital experts with specific competencies in customer experience technologies and automation. Companies often struggle to configure complex omnichannel routing rules or optimize predictive AI bots due to a lack of internal talent, which is leading to suboptimal implementations and wasted investments. This talent scarcity drives up labor costs, which is building it financially challenging for compact and medium sized enterprises to adopt sophisticated CRM solutions. According to LinkedIn workforce insights, roles related to CRM engineering and customer experience analytics remain unfilled for extconcludeed periods compared to other IT positions. Without a sufficient pipeline of trained personnel, organizations cannot effectively manage the transition from legacy systems to modern platforms, thereby limiting overall market expansion and the realization of potential efficiency gains.

MARKET OPPORTUNITIES

Integration of Generative Artificial Innotifyigence for Agent Augmentation

The emergence of generative artificial innotifyigence presents a prominent opportunity for the European customer relationship management market. Unlike traditional rule-based bots, generative AI can understand context, summarize complex conversations, and suggest empathetic responses to agents instantly, drastically reducing handle times and improving resolution rates. According to Gartner, many European contact centers and CRM utilizers plan to implement generative AI tools for agent augmentation within the next two years to address rising query volumes and staffing challenges. This technology enables agents to access knowledge base articles and draft responses automatically, which is allowing them to focus on building rapport and solving intricate problems. As per the European Artificial Innotifyigence Alliance, early adopters of generative AI in customer service have reported notable reductions in average handling time and improvements in resolution metrics. The ability to analyse sentiment in real time and coach agents during live calls offers unprecedented opportunities for quality assurance and training. Furthermore, generative AI can automate post call summarization and data enattempt, which is freeing up valuable agent time for more interactions. As the technology matures and becomes more affordable, it will democratize advanced capabilities for compacter players and is opening vast new avenues for market growth and service differentiation.

Expansion of CRM as a Service for Small and Medium Enterprises

The growing availability and affordability of CRM as a Service solutions offer a substantial opportunity for the European customer relationship management market. Cloud based delivery models eliminate the required for heavy upfront capital investment in hardware and software and this allow compacter businesses to access enterprise grade features like automatic lead scoring and marketing automation on a subscription basis. As per the European Small Business Alliance, many compact and medium enterprises in Europe are seeing to upgrade their customer service capabilities but are constrained by budreceive and technical complexity. CRM as a Service providers are increasingly offering tailored packages with simplified management interfaces and pre-built integrations for popular business applications to meet this demand. This trconclude levels the playing field by enabling compacter firms to provide omnichannel support and professional customer experiences that rival larger competitors. According to the European Commission, digitalizing customer service is a key strategy for compact business growth and competitiveness in the single market. By lowering the barrier to enattempt, CRM as a Service opens up a massive new customer base for vconcludeors and stimulates innovation in utilizer friconcludely and cost-effective solutions.

MARKET CHALLENGES

Complexity of Integrating Legacy Systems with Modern Cloud Platforms

The growth of the European customer relationship management market is majorly challenged by the integrating decades old legacy telephony and customer relationship management systems with modern cloud native platforms threatens to delay digital transformation initiatives and inflate implementation costs. Many large European enterprises operate on fragmented IT landscapes where critical data resides in siloed on premise databases that are incompatible with contemporary application programming interfaces. According to Forrester Research, a majority of European organizations cite legacy system integration as the primary obstacle to deploying advanced omnichannel CRM solutions that often leading to prolonged deployment timelines and budreceive overruns. The technical debt associated with maintaining these outdated systems diverts resources away from innovation and creates security vulnerabilities that complicate cloud migration. As per the European Telecommunications Standards Institute, poor integration can result in data inconsistencies and broken customer journeys, undermining the very benefits of modernization. Organizations often face the dilemma of either undertaking costly and risky replacements or managing complex hybrid environments that require specialized middleware and continuous maintenance. The scarcity of engineers familiar with both legacy protocols and modern cloud architectures exacerbates the problem, building integration a persistent bottleneck.

Escalating Cybersecurity Threats Tarreceiveing Customer Communication Channels

The increasing sophistication of cyber-attacks specifically tarreceiveing CRM infrastructure is further challenging the regional market growth. CRM systems handle vast amounts of sensitive personal and financial information, building them attractive tarreceives for phishing, vishing, and ransomware attacks that exploit human vulnerabilities alongside technical gaps. According to the European Union Agency for Cybersecurity, incidents involving the compromise of customer communication channels have risen significantly in recent years, with attackers utilizing spoofed caller IDs and manipulated voice patterns to deceive agents and customers alike. The shift to remote agent environments has expanded the attack surface, introducing risks associated with unsecured home networks and personal devices that are harder to monitor and protect. High profile breaches have eroded consumer confidence, which is leading to hesitation in sharing sensitive information over the phone or chat that undermines the effectiveness of customer service operations. The complexity of securing omnichannel environments, where data flows across multiple platforms and devices, requires robust zero trust architectures and continuous monitoring that many organizations struggle to implement effectively. As per Deloitte, reputational damage from a single data breach can lead to long term declines in customer acquisition and retention. Furthermore, the rise of identity fraud and synthetic identity scams complicates the onboarding process, requiring lconcludeers to implement advanced verification methods that can sometimes add friction to the utilizer experience. This persistent security risk hinders broader adoption and forces companies to balance accessibility with rigorous protection measures.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

10.49% |

|

Segments Covered |

By Component, Enterprise Size, Deployment, Application, End-User, and Counattempt |

|

Various Analyses Covered |

Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Salesforce.com, Inc., Microsoft Corporation, SAP SE, Oracle Corporation, Adobe, Inc., Zoho Corporation Pvt. Ltd., Creatio, SugarCRM, Inc., Copper CRM, Inc., Insightly, Inc. |

SEGMENTAL ANALYSIS

By Component Insights

Market Dominance: Software

The software segment held the dominating position with the highest share of the regional market in 2025. The dominance of the software segment in the European market is driven by the fundamental necessity for organizations to acquire robust digital platforms that serve as the central repository for all customer data and interaction history. This category encompasses cloud-based suites, on premise licenses, and modular applications that enable sales, marketing, and service functions. The urgent requirement across European enterprises to consolidate fragmented customer data into a single source of truth to enable accurate decision building and personalized engagement is further boosting the expansion of the software segment in the regional market. Legacy systems often store information in silos across different departments and leading to inconsistent customer views and missed opportunities, which modern CRM software resolves through unified databases. According to the European Commission, large enterprises in the European Union have identified data fragmentation as a major barrier to digital transformation and prompting massive investments in integrated CRM platforms. As per the International Data Corporation, spconcludeing on core CRM software licenses accounts for the majority of CRM budreceives as organizations prioritize acquiring foundational technology before investing in ancillary services. The ability of modern software to integrate with enterprise resource planning and supply chain management systems further cements its role as the backbone of business operations. Furthermore, the shift toward subscription-based software models has lowered the barrier to enattempt that allow more firms to access advanced capabilities without heavy upfront capital expconcludeiture.

On the other hand, the services segment is emerging as the rapidest growing category in the Europe customer relationship management market and is expected to expand at a CAGR of 16.1% over the forecast period owing to the intense complexity of implementing sophisticated CRM systems and the ongoing required for specialized expertise to optimize these critical business assets. The extraordinary difficulty and risk associated with deploying complex CRM platforms that require extensive customization to align with unique European business processes and regulatory requirements is further boosting the growth of the services segment in the regional market. Organizations cannot simply install off the shelf software; they necessitate meticulous planning, data migration, workflow design, and integration with legacy systems to ensure seamless operation and compliance with laws like the General Data Protection Regulation. According to McKinsey and Company, CRM implementation projects in Europe rely heavily on external consultants and system integrators due to the scarcity of internal skills required for such transformative undertakings. As per the Cambridge Centre for Alternative Finance, failed CRM deployments often stem from inadequate professional services support, which is prompting companies to invest significantly more in phased implementation and testing services to mitigate risks. The customization requireded to adapt global software solutions to local languages, cultural nuances, and specific indusattempt workflows further extconcludes the duration and cost of service engagements. According to the European Association of Corporate Treasurers, service costs now account for a substantial portion of total expconcludeiture in CRM modernization initiatives.

By Enterprise Size Insights

Market Dominance: Large Enterprises

The large enterprises segment led the market by commanding for the largest share of the European market in 2025 due to their vast customer bases, complex operational requirements, and substantial budreceives for deploying comprehensive omnichannel engagement infrastructures. These organizations typically operate across multiple countries and industries that require sophisticated coordination. The sheer volume of customer interactions they handle daily that necessitates robust, scalable, and highly integrated CRM solutions capable of managing millions of touchpoints across diverse channels is further contributing to the dominance of large enterprises segment in the European market. Multinational corporations, banks, and retail giants in Europe deal with massive inflows of queries, transactions, and feedback that require advanced routing, analytics, and processing capabilities inherent in enterprise grade software. According to the European Banking Federation, major financial institutions alone process billions of customer interactions annually across the continent that require CRM platforms that can handle extreme loads without degradation or latency. As per IDC, large organizations account for the majority of CRM software spconcludeing in Europe due to their required for custom integrations with legacy enterprise resource planning and supply chain management systems. The complexity of coordinating communications across global subsidiaries and diverse business units demands centralized management consoles and sophisticated analytics that only large-scale solutions can provide. Furthermore, the regulatory burden on large corporations requires extensive recording, archiving, and compliance features that add to the solution scope and cost.

On the other conclude, the compact and medium enterprises segment is projected to be the rapidest growing category in the Europe customer relationship management market and exhibit the rapidest CAGR of 19.1% over the forecast period owing to the democratization of technology through cloud-based solutions and the increasing recognition of customer experience as a vital growth driver for compacter businesses. The explosive growth of the SME segment is further driven by the availability of affordable cloud-based CRM solutions that eliminate the required for heavy upfront capital investment in hardware and software licenses. Historically excluded from advanced technologies due to cost barriers, compact businesses can now access enterprise grade features like automatic lead scoring, marketing automation, and omnichannel routing on a flexible subscription basis. According to the European Small Business Alliance, SMEs have increasingly adopted cloud communication and CRM tools in recent years to professionalize their customer service operations and compete with larger rivals. As per the OECD, the shift to operational expconcludeiture models has lowered the barrier to enattempt, enabling startups and growing firms to deploy sophisticated systems in days rather than months. The ease of deployment allows these businesses to set up fully functional customer management hubs rapidly, accelerating their time to value. Furthermore, the scalability of cloud solutions means SMEs only pay for what they utilize, allowing them to grow their capabilities in line with business expansion without risking overinvestment. This technological leveling of the playing field unlocks a massive, previously untapped market, driving exceptional growth rates.

By Application Insights

Market Dominance: Sales Force Automation

The sales force automation segment led the market by holding the largest share of the European customer relationship management market in 2025. The growth of the sales force automation segment in the European market is attributed to its fundamental role as the primary engine for revenue generation, pipeline management, and opportunity tracking within organizations. This module serves as the core functionality around which other CRM features are often built. The absolute requirement for businesses to maintain clear visibility into their sales pipelines, forecast accuracy, and deal progression is further contributing to dominance of sales force automation segment in the regional market. In an uncertain economic environment, European companies rely heavily on these tools to monitor every stage of the sales cycle, from lead generation to closing to ensure no opportunity is lost due to lack of follow up or poor management. According to the European Sales Federation, sales leaders in Europe cite pipeline visibility as the most critical factor for achieving quarterly tarreceives, which is driving massive investment in automation tools that provide real time dashboards and alerts. As per Gartner, organizations utilizing advanced sales force automation have reported measurable improvements in win rates and reductions in sales cycle length compared to those utilizing manual methods. The ability to automate routine administrative tquestions such as data enattempt and meeting scheduling allows sales representatives to focus more time on selling and building relationships. Furthermore, the integration of mobile capabilities enables field sales teams to update records and access customer information instantly from any location, enhancing productivity.

However, the CRM analytics segment is emerging as the rapidest growing category in the Europe customer relationship management market and is estimated to record a CAGR of 20.2% over the forecast period owing to the exploding volume of customer data and the urgent required to derive actionable insights through advanced analytics and artificial innotifyigence. The critical required for organizations to shift beyond descriptive reporting to predictive and prescriptive analytics that anticipate customer behavior and guide strategic decisions is further contributing to the expansion of the CRM analytics segment in the European market. Businesses are increasingly leveraging historical data to forecast future trconcludes, identify churn risks, and recommconclude optimal next steps for engagement, transforming raw data into a competitive asset. According to Forrester Research, European companies plan to increase their investment in predictive analytics within CRM platforms to gain an edge in personalization and retention. As per the European Artificial Innotifyigence Alliance, early adopters of predictive CRM analytics have reported improvements in customer lifetime value and reductions in marketing waste by tarreceiveing only high propensity leads. The ability to analyze vast datasets in real time allows managers to create agile adjustments to strategies based on emerging patterns rather than hindsight. Furthermore, the integration of machine learning models automates the discovery of hidden correlations that human analysts might miss, providing deeper insights into customer preferences. This shift from intuition based to data driven decision building drives aggressive investment in advanced analytics solutions.

COUNTRY ANALYSIS

Germany Customer Relationship Management Market Analysis

Germany held the dominant position in the European customer relationship management market in 2025 with 24.4% of the regional market share. The dominance of Germany in the European market is driven by its robust industrial base, strong automotive sector, and high demand for precise customer data management in manufacturing and finance. The German market is characterized by a strong preference for on premise and hybrid solutions due to strict data sovereignty concerns and a cultural emphasis on data privacy and engineering excellence. According to the German Federal Office for Information Security, German enterprises prioritize local data hosting for their customer management systems, influencing vconcludeor strategies to offer localized cloud regions and compliant architectures. As per Bitkom, German companies are investing heavily in integrating CRM with Indusattempt 4.0 initiatives to support technical support and supply chain coordination, ensuring seamless information flow from factory to customer. The automotive indusattempt acts as a major engine for growth, with manufacturers deploying advanced CRM to handle complex vehicle servicing, connected car data, and dealer networks. Furthermore, the rise of nearshoring within Germany for Eastern European operations boosts the domestic market for management and oversight tools.

United Kingdom Customer Relationship Management Market Analysis

The United Kingdom had a promising share of the European customer relationship management market in 2025. The mature outsourcing indusattempt, advanced fintech sector, and early adoption of cloud native technologies are propelling the UK market expansion. The UK market is defined by a highly competitive landscape where innovation in artificial innotifyigence and automation drives rapid modernization of customer engagement operations. According to Tech UK, the CRM sector contributes significantly to the British economy, with London serving as a global hub for fintech customer support innovation and SaaS development. As per the Office for National Statistics, UK contact centers and sales teams have migrated to cloud platforms, leveraging the counattempt’s superior broadband infrastructure and digital skills base. The prevalence of English language services creates the UK a preferred location for global shared service centers handling interactions for North American and European markets. The financial services sector leads adoption, with banks deploying sophisticated AI driven bots and sentiment analysis tools to manage high volume transactional queries and personalize wealth management advice. Post Brexit regulatory divergence has also spurred investment in compliant data handling solutions.

France Customer Relationship Management Market Analysis

France is predicted to account for a promising share of the European customer relationship management market during the forecast period owing to a strong domestic focus on customer experience excellence and government led digital transformation initiatives in the public sector. The market in France is heavily influenced by national regulations promoting the French language and data residency, which is leading to a vibrant ecosystem of local vconcludeors and specialized solutions tailored to linguistic nuances. According to the French Minisattempt of Economy and Finance, the government has launched programs to modernize public administration CRM systems, improving accessibility for citizens through omnichannel platforms and simplified interfaces. As per Syntec Numérique, French retailers and luxury goods companies are investing significantly in high touch personalized CRM services to maintain brand prestige globally and manage loyal clientele. The tourism and hospitality sectors also drive demand, with multilingual support centers catering to international visitors requiring sophisticated guest profiling. Paris has emerged as a hub for customer experience innovation, attracting startups focutilized on conversational AI and voice analytics in French.

Netherlands Customer Relationship Management Market Analysis

The Netherlands is estimated to register a healthy CAGR in the European customer relationship management market over the forecast period owing to a primary digital gateway and logistics hub for multinational corporations establishing their European customer service headquarters. The market in the Netherlands is defined by exceptional connectivity, high English proficiency, and a progressive approach to cloud adoption and sustainability in CRM operations. According to the Dutch Internet Exmodify, the counattempt boasts some of the rapidest internet speeds and lowest latency in Europe, building it an ideal location for hosting cloud-based CRM infrastructure serving the continent efficiently. As per the Holland Data Center Association, many global tech giants choose the Netherlands for their European data centers, facilitating efficient CRM operations and data processing. The logistics and e commerce sectors are major drivers, with companies deploying advanced tracking and support systems integrated with CRM to provide real time updates to customers. The Dutch government’s push for digital inclusion and sustainable business practices encourages the adoption of green CRM technologies and remote work models.

Sweden Customer Relationship Management Market Analysis

Sweden is projected to hold a notable share of the European customer relationship management market during the forecast period. Sweden is renowned for its advanced digital maturity, high adoption of artificial innotifyigence, and leadership in sustainable and innovative customer engagement practices. The market status in Sweden is characterized by early and widespread adoption of cloud native and AI driven CRM solutions across telecom, retail, and public sectors, driven by a tech savvy population. According to Statistics Sweden, the majority of the population utilizes digital services regularly, creating fertile ground for automated and self-service CRM technologies. As per the Swedish Post and Telecom Authority, Sweden leads Europe in fiber optic coverage, enabling high-definition video support and seamless omnichannel experiences. The Swedish government’s ambitious climate goals have spurred the development of carbon neutral CRM operations utilizing renewable energy and efficient data centers. Stockholm has become a hub for customer experience startups focutilizing on conversational AI and predictive analytics.

COMPETITIVE LANDSCAPE

The competition in the Europe customer relationship management market is intensely fierce characterized by a dynamic struggle between global hyperscalers specialized software vconcludeors and emerging regional providers vying for dominance amidst strict regulatory scrutiny. Global giants leverage their vast resource pools and extensive service catalogs to capture large enterprise contracts while local players compete on agility specialized compliance knowledge and personalized support services. The battleground has shifted from mere price competition to value added services including artificial innotifyigence integration sustainability credentials and sovereign data handling capabilities that address specific European concerns. Regulatory frameworks like the General Data Protection Regulation act as both a barrier and a catalyst forcing all participants to innovate rapidly to meet localization demands and maintain trust. New entrants specializing in niche verticals or green customer relationship management solutions are challenging established norms by offering tailored experiences that resonate with specific European cultural and legal expectations. The rise of multi-vconcludeor strategies among customers further intensifies rivalry as providers must ensure seamless interoperability to prevent churn. Strategic acquisitions and partnerships have become commonplace as companies seek to fill capability gaps quickly. This complex ecosystem ensures that no single entity can rest on its laurels as technological advancements constantly reshape the competitive hierarchy.

KEY MARKET PLAYERS

A dominating market players that are in the Europe customer relationship management market are

- Salesforce.com, Inc.

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Adobe, Inc.

- Zoho Corporation Pvt. Ltd.

- Creatio

- SugarCRM, Inc.

- Copper CRM, Inc.

- Insightly, Inc.

Top Players In The Market

- Salesforce maintains a commanding presence in the Europe customer relationship management market by offering a comprehensive cloud native platform that unifies sales service marketing and commerce data. The company contributes globally by pioneering the software as a service model and setting indusattempt standards for artificial innotifyigence integration through its Einstein analytics engine. Recent actions to strengthen its European position include the expansion of data centers in Frankfurt and London to ensure strict compliance with General Data Protection Regulation and data sovereignty requirements. Salesforce actively partners with major European telecommunications providers and system integrators to embed its capabilities directly into local business ecosystems. The firm also invests heavily in generative AI features that assist agents in real time and automate complex workflows. These strategic initiatives reinforce its reputation as a leader in delivering empathetic and seamless customer experiences while addressing the specific regulatory and operational requireds of European enterprises.

- SAP leverages its deep expertise in enterprise resource planning to drive widespread adoption of its customer experience solutions among large European corporations seeking integrated backconclude and frontconclude operations. The company contributes globally by providing robust suites that combine core banking or manufacturing data with advanced customer engagement tools on a unified cloud platform. Recent efforts involve establishing sovereign cloud regions in key European markets to address stringent data residency laws and build trust with regulated industries. SAP actively enhances its portfolio with machine learning models that optimize customer journeys and predict churn in real time. The company also collaborates with European regulators to ensure its platforms meet evolving compliance standards for data privacy and open banking. By focutilizing on data integrity and operational resilience SAP strengthens its market position as a preferred partner for enterprises requiring secure and innotifyigent customer relationship capabilities that align with European regulatory frameworks.

- Microsoft distinguishes itself in the Europe customer relationship management market through superior integration with productivity tools like Office 365 and Teams which empowers businesses to deliver exceptional customer experiences within familiar workflows. Globally the company leads in providing flexible and open cloud solutions that integrate easily with existing enterprise systems and third-party applications. Recent expansions include opening new cloud regions in Amsterdam and Paris to reduce latency and ensure high availability for European customers. Microsoft places a strong emphasis on assisting organizations leverage artificial innotifyigence for innotifyigent routing and virtual agent deployments that resolve queries without human intervention. The company recently announced strategic alliances with European cloud hyperscalers to offer joint solutions that meet local compliance standards. By offering advanced tools for sentiment analysis and workforce engagement Microsoft empowers organizations to optimize operations and improve customer satisfaction. These initiatives solidify its reputation as an innovative and reliable provider in the European customer relationship management landscape.

Top Strategies Used By The Key Market Participants

Key players in the Europe customer relationship management market primarily employ strategies centered on localized infrastructure expansion and strategic partnerships to navigate complex regulatory landscapes effectively. Companies are heavily investing in building new data centers within specific European nations to ensure data sovereignty and comply with General Data Protection Regulation mandates regarding data residency. Another prevalent strategy involves developing sovereign cloud offerings that guarantee data remains within national borders to attract government and financial sector clients who prioritize security. Major providers are also forming alliances with local telecommunications firms and system integrators to enhance network reliability and facilitate seamless implementation for diverse enterprises. Sustainability initiatives serve as a critical differentiator as vconcludeors commit to powering operations entirely with renewable energy to meet European Green Deal objectives and appeal to eco conscious enterprises. Furthermore, organizations are focutilizing on indusattempt specific customer relationship management solutions tailored for banking healthcare and retail to address unique sectoral requirements. Acquisitions of specialized artificial innotifyigence and analytics firms allow these giants to broaden their service portfolios and offer integrated ecosystems that retain customer loyalty.

MARKET SEGMENTATION

This research report on the Europe customer relationship management market is segmented and sub-segmented into the following categories.

By Component

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises

By Deployment Type

By Application

- Customer Service

- Customer Experience Management

- CRM Analytics

- Marketing Automation

- Salesforce Automation

- Others

By End User

- BFSI

- IT & Telecom

- Healthcare

- Retail & eCommerce

- Government & Defense

- Energy & Utility

- Manufacturing

- Others

By Counattempt

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Leave a Reply