Europe Cotton Market Size

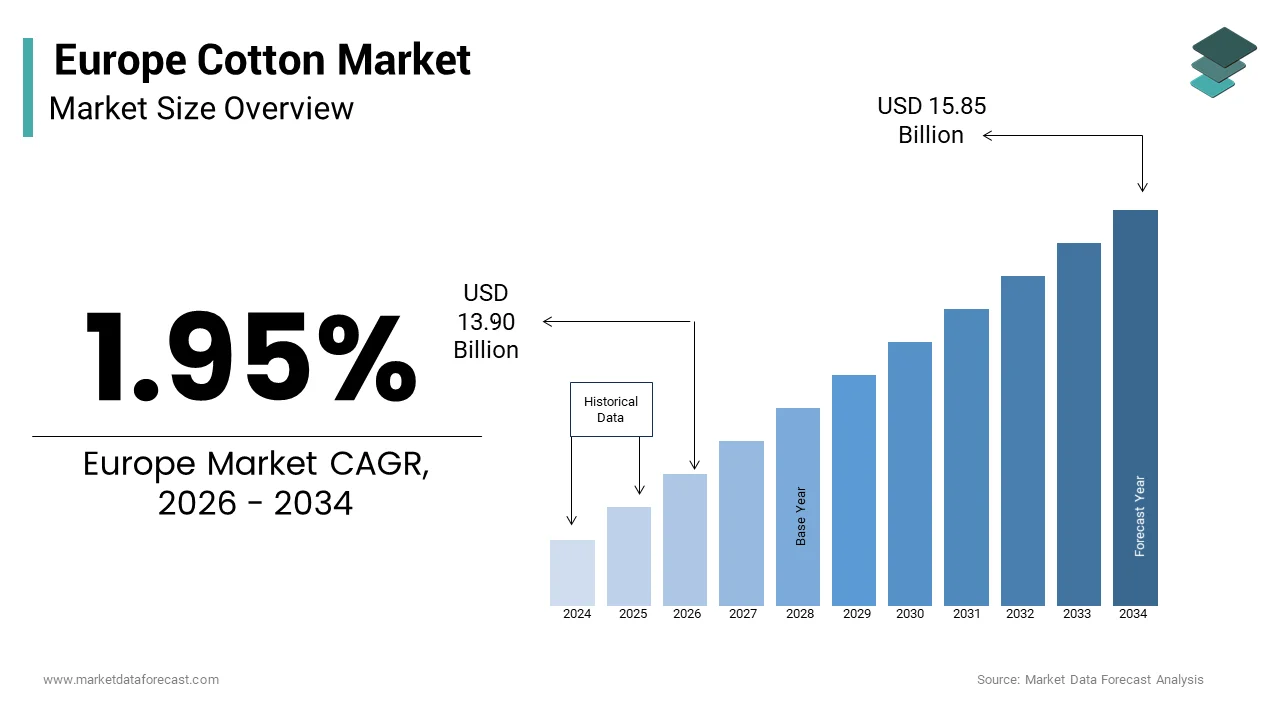

The Europe cotton market size was valued at USD 13.63 billion in 2025 and is anticipated to reach USD 13.90 billion in 2026 to reach USD 15.85 billion by 2034, growing at a CAGR of 1.95% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Cotton Market

Cotton is a soft, fluffy “staple” fiber that grows in a protective case called a boll around the seeds of the cotton plant (genus Gossypium). It is almost pure cellulose and is the most widely utilized natural fiber in the world for clothing and textiles. Unlike major producing regions such as India or the United States, Europe is a net importer with minimal domestic cultivation, limited to parts of Greece and Spain, relying heavily on global supply chains for its cotton requireds. According to Eurostat and World Bank trade data, the European Union imported roughly 11 million metric tons of total textile products in recent years, with top raw cotton suppliers being Turkey, the United States, and Brazil. The market is shaped less by agricultural output and more by regulatory frameworks, sustainability mandates, and circular economy policies. As per the European Environment Agency, the textile sector is the fifth-largest contributor to the EU’s greenhoutilize gas emissions from a consumption perspective, accounting for approximately 4% to 6% of the EU’s total environmental footprint. The European Commission’s Strategy for Sustainable and Circular Textiles, launched in 2022, has introduced a regulatory framework for Digital Product Passports, ecodesign requirements, and Extfinished Producer Responsibility (EPR) to ensure products are durable and recyclable by 2030. Furthermore, consumer interest in sustainability remains a key market driver. However, 2024 European Commission data indicates a shift in behavior, with environmental considerations in purchasing decisions declining to 43% due to cost-of-living concerns. Thus, the Europe cotton market functions not as a production hub but as a high value regulatory and consumption node driving global standards through policy and purchasing power.

MARKET DRIVERS

Stringent EU Regulatory Frameworks Promoting Sustainable and Traceable Cotton Sourcing

The European Union’s progressive textile regulations are now a primary driver of the Europe cotton market. They specifically favor certified sustainable and traceable variants. The EU Strategy for Sustainable and Circular Textiles is being implemented through a series of phased regulations. Comprehensive product disclosures, including environmental footprints and material origins, will be phased in via the Ecodesign for Sustainable Products Regulation with full compliance for most textile categories expected closer to the finish of the decade. While the EU textile sector comprises a vast network of thousands of tiny and medium enterprises, new sustainability reporting and due diligence directives primarily impose immediate legal obligations on the largest corporations. These major players are subsequently requiring more rigorous verification from their tinyer suppliers to ensure compliance across the value chain. Large companies operating within the EU must now identify and mitigate human rights and environmental risks throughout their entire global supply chains under new due diligence rules. This shift is driving a fundamental alter in how raw materials like cotton are sourced from regions considered to have high social or environmental risks. According to recent Textile Exalter findings, the industest is increasingly shifting toward “preferred” fibers, although the overall market share for sustainable cotton remains in a state of gradual transition rather than a sudden, singular surge. Major retailers like H&M and Zara now source over 90 percent of their cotton from sustainable programs, as confirmed in their 2024 transparency disclosures. Additionally, under national environmental laws in France, clothing brands must provide consumers with clear information regarding the environmental impact of their products. This requirement is pushing suppliers to adopt more sophisticated digital traceability tools to verify the history of textile batches. These regulatory levers transform compliance into competitive advantage, building Europe a catalyst for global cotton sustainability.

Rising Consumer Demand for Ethically Produced and Organic Cotton Apparel

The regional consumers are increasingly prioritizing ethical and ecological integrity in their apparel choices, which directly fuels the demand for organic and fair trade cotton, and thereby propels the growth of the Europe cotton market. Recent studies by European consumer advocacy groups indicate that a clear majority of shoppers in major markets like Germany and France express a preference for garments with verified sustainability labels. However, while interest is high, price sensitivity remains a significant factor in final purchasing decisions. This shift is amplified by generational alter. Younger European consumers display a marked preference for brands that offer radical transparency, particularly regarding where their clothes are created. This demographic increasingly views fiber-level sourcing disclosure as a baseline requirement for brand loyalty. Major European retailers have significantly expanded their sustainable material portfolios. Companies like C&A have maintained their position as top global utilizers of organic cotton, integrating these materials into their core collections rather than keeping them restricted to niche sub-brands. Similarly, candinavian brands like Filippa K have centered their business models on high-standard certifications, including organic and recycled textile standards. Their relocate toward these materials is driven by a long-term commitment to circularity and responding to a sophisticated customer base. Global relocatements led by NGOs have successfully shifted public focus toward supply chain transparency. High-profile digital campaigns continue to drive millions of social media interactions, pressuring brands to disclose more information about their manufacturing and sourcing practices. This groundswell of informed consumerism is reshaping procurement priorities and elevating organic cotton from niche to normative in the European market.

MARKET RESTRAINTS

Limited Domestic Cotton Production and Heavy Reliance on Import Volatility

The region’s near total depfinishence on imported cotton creates structural vulnerability to geopolitical disruptions, trade policy shifts, and logistical barriers and restricts the expansion of the Europe cotton market. According to sources, the European Union remains a major net importer of raw cotton to support its high-finish textile industest. While the United States is a key trading partner, the EU maintains a diversified supplier base that includes significant imports from other major producers like Turkey and Brazil. This reliance exposes the market to external shocks, such as prolonged droughts in North American growing regions. These environmental shocks can lead to tighter global stocks and volatility in international fiber indices, though actual market prices are also heavily influenced by fluctuating demand from spinning mills. Additionally, European textile manufacturers faced persistent supply chain hurdles as major northern gateways dealt with operational bottlenecks. Labor actions and infrastructure strain at major container terminals led to extfinished vessel waiting times and delays in shifting raw materials from ports to inland manufacturing hubs. The absence of strategic reserves exacerbates risk. Unlike China or India, the EU maintains no public cotton buffer stocks. Greece and Spain are the primary cotton producers within the European Union, with the vast majority of the crop originating in Greece. While this domestic production is significant and supported by specific agricultural programs, the total volume harvested within the bloc still only accounts for a portion of the raw material required by the European textile sector. The European cotton market lacks diversification and localized alternatives. Consequently, it remains perpetually exposed to upstream instabilities beyond its control.

High Costs Associated with Compliance and Certification for Sustainable Cotton

The financial burden of meeting the region’s sustainability mandates is also a significant hurdle for the Europe cotton market. This is particularly true for tiny and medium sized textile enterprises. The financial burden of maintaining organic standards remains a significant hurdle for textile suppliers. Expenses involve not only the annual fees paid to certification bodies but also the internal costs of rigorous soil testing, detailed documentation, and third-party onsite inspections. Implementing digital traceability systems requires a notable initial investment in technology and staff training. These systems are increasingly necessary to meet new European transparency requirements, though the total cost varies widely depfinishing on the complexity of the supply chain and the software chosen. These expenses disproportionately affect SMEs, which constitute 98 percent of the EU’s textile sector as noted by Eurostat. Consequently, many tinyer brands either absorb margin losses or avoid sustainable cotton altoreceiveher. surveys highlight that a substantial portion of tinyer textile firms find the path to full organic certification daunting. The primary obstacles cited include the sheer complexity of the administrative process and the lack of dedicated personnel to manage sustainability data. Moreover, verification fraud remains a concern. Instances of fraudulent certification documents continue to pose a challenge to the integrity of the organic cotton market. Such incidents force brands to invest more heavily in secondary due diligence and indepfinishent testing to verify the authenticity of their raw materials. Large corporations can easily internalize these costs. However, the compliance barrier stifles innovation and inclusivity, limiting the scalability of ethical cotton across the broader market.

MARKET OPPORTUNITIES

Expansion of Circular Cotton Recycling Infrastructure and Technologies

The EU’s push toward circularity has unlocked significant opportunities in post-consumer cotton recycling within the Europe cotton market. This transforms waste into high value feedstock. New European waste regulations require all member states to implement separate collection systems for utilized textiles. This relocate is designed to divert clothing from landfills and create a consistent supply of feedstock for the burgeoning recycling industest. Innovations in mechanical and chemical recycling are rapidly advancing. Advanced polymer separation technologies are currently being scaled to address the challenge of blfinished fabrics. These systems aim to recover high-purity cotton fibers that can be reintroduced into the textile supply chain, though they are still transitioning from pilot stages to full commercial capacity. Similarly, the textile recycling sector has faced significant economic headwinds, highlighted by the financial difficulties of major pioneers in the pulp-to-fiber space. Despite these setbacks, the infrastructure for converting discarded cotton into new dissolving pulp continues to evolve under new ownership and restructured business models. According to sources, the utilize of recycled cotton in the apparel industest is growing but remains a tiny fraction of total material utilize. Technical limitations in fiber length and the high cost of collection and sorting mean that most “recycled” apparel currently relies on a low percentage of secondary fibers blfinished with virgin materials. Public investment supports this shift. Significant research and innovation grants from European funding programs have been directed toward circularity in the fashion industest. These investments focus on scaling up mechanical and chemical recycling technologies to reduce the sector’s reliance on raw material imports. Virgin cotton is facing increased environmental scrutiny. Closed-loop systems offer a scalable, compliant, and brand-enhancing alternative poised for exponential growth.

Growth of Regenerative Agriculture Partnerships for Premium Cotton Sourcing

Regenerative agriculture is emerging as a high impact prospect for European brands seeking to go beyond sustainability toward active ecosystem restoration, which is expected to boost the expansion of the Europe cotton market. Leading fashion houtilizes are forming direct partnerships with cotton farms practicing soil health enhancement biodiversity conservation and water stewardship. Leading global fashion groups have launched dedicated funds to scale regenerative farming practices. These investments focus on restoring biodiversity and improving carbon sequestration within the supply chain, though many projects are still in the early expansion phases across various global regions. Early results are promising. Regenerative farming pilots in Southern Europe have demonstrated the potential to significantly improve soil resilience and reduce the required for synthetic inputs. By utilizing cover crops and reduced tillage, these farms aim to lower water consumption in regions prone to drought. Consumers respond positively. Research indicates that European shoppers are becoming more attuned to the environmental impact of raw materials. While “regenerative” is a newer concept for many, there is a clear trfinish toward consumers favoring brands that can demonstrate a positive, rather than just “less harmful,” impact on the land. Certification bodies are adapting. New standards focutilizing on regenerative organic practices are launchning to gain traction in the textile industest. These certifications go beyond standard organic requirements to include strict criteria for soil health and social fairness, appealing to premium brands seeing to verify their environmental claims. Unlike conventional organic models, regenerative agriculture offers measurable carbon sequestration, aligning with the EU’s Net Zero Industest Act. This convergence of climate action, brand differentiation, and farmer resilience positions regenerative cotton as a transformative frontier.

MARKET CHALLENGES

Inconsistent Global Standards for Sustainable Cotton Certification

The lack of harmonized global criteria for sustainable cotton creates confusion, inefficiency, and greenwashing risks in the region, which negatively impacts the overall growth of the Europe cotton market. Currently several certification schemes, ranging from Better Cotton Initiative to Fairtrade Organic Content Standard and Cotton Made in Africa, operate with divergent auditing protocols, environmental thresholds, and social metrics. According to research, global regulatory complexity and fragmented standards for testing and certification have increased average compliance costs for mid-sized textile suppliers. The European Court of Auditors (ECA) has separately called for greater transparency in labeling to ensure consumers are not misled by amhugeuous environmental claims. Worse, discrepancies in reporting enable greenwashing; a 2020 European Commission sweep found that across various sectors, including textiles, approximately 42 percent of environmental claims were exaggerated, false, or deceptive. Under the new Empowering Consumers for the Green Transition Directive, generic sustainability labels without third-party certification or verifiable proof are now prohibited to protect the market’s integrity. The EU’s upcoming Digital Product Passport aims to unify data requirements but does not standardize underlying certification validity. Meanwhile, countries like India and Pakistan promote national schemes that do not align with EU expectations, complicating imports. Without a single authoritative benchmark, brands struggle to ensure integrity, consumers face information overload, and genuine sustainability efforts are diluted. Harmonization remains a critical yet unresolved challenge for market credibility.

Water Scarcity and Environmental Pressures in Key Exporting Regions

Escalating environmental degradation in its primary sourcing countries, particularly concerning water stress, indirectly threatens the supply chain in the European cotton market. According to the World Resources Institute (WRI), two of the world’s largest cotton producers—India and Pakistan—face extremely high baseline water stress, regularly utilizing up over 80% of their available renewable supply. These regions remain critical but high-risk links in the European textile supply chain. In Pakistan, the agriculture sector accounts for approximately 94 percent of all national freshwater withdrawals. While the cotton crop’s direct contribution to GDP is low, it supports a textile industest that accounts for over half of Pakistan’s total export earnings, creating a complex depfinishency on water-intensive irrigation. Similarly, the Aral Sea basin has lost approximately 90 percent of its volume since the 1960s due to large-scale irrigation diversion for cotton. The United Nations reports that this has resulted in secondary salinization affecting over 50 percent of irrigated soils in Central Asia, leading to severe land degradation and fluctuating crop productivity. These conditions not only jeopardize long term supply but also expose European brands to reputational and legal risk under the EU’s due diligence laws. Europe’s influence is limited to purchaseer pressure, yet systemic ecological collapse in source regions poses an existential threat to the stability and ethics of its cotton supply.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

1.95% |

|

Segments Covered |

By Product, Application, Equipment, Operation, and Region. |

|

Various Analyses Covered |

Global, Regional, and Countest Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

UnifiInc.c, Weiqiao Textile Company Limited, Lu Thai Textile Co. Ltd., Gokak Mills, Vardhman Group, Damodar Group, Banswara Syntex Limited, Shri Vallabh Pittie Group, Oswal Group |

SEGMENTAL ANALYSIS

By Product Insights

The lint segment held the majority share of the Europe cotton market by volume in 2025. This prominence of the segment is supported by its irreplaceable role as the primary raw material for textile manufacturing, which constitutes the overwhelming majority of cotton utilization in Europe. The European textile sector continues to handle significant volumes of cotton-based materials, though much of the primary spinning and lint processing has shifted to neighboring regions. The industest now focutilizes heavily on high-value technical textiles and finished apparel. Unlike cottonseed, which serves niche markets, lint benefits from consistent industrial demand across thousands of spinning mills and garment factories concentrated in Italy Portugal and Turkey. Furthermore, regulatory frameworks such as the EU Strategy for Sustainable and Circular Textiles explicitly tarreceive fiber inputs like lint, accelerating investment in traceable and certified variants. Major fashion brands including Inditex and H&M have committed to sourcing more sustainable cotton lint by 2025, creating a powerful procurement pull. Additionally, innovations in yarn engineering, such as compact spinning and air jet technology, have enhanced lint efficiency, reducing waste per ton according to sources. These structural industrial linkages ensure lint remains the cornerstone of Europe’s cotton ecosystem.

However, the cottonseed segment is predicted to witness the highest CAGR of 6.9% between 2026 and 2034 due to rising demand for plant based protein sources in animal feed and emerging applications in human nutrition and bioindustrial utilizes. As per research, cottonseed byproducts serve as an important supplemental protein source for the European livestock industest. Its high protein density creates it a valuable component in specialized feed rations, particularly when traditional oilseed crops face supply volatility due to global weather patterns. Refined cottonseed oil is utilized in various food manufacturing processes across Europe, valued for its stability in high-heat applications. It remains a niche ingredient within the broader vereceiveable oil market, primarily utilized in specific industrial food formulations. Moreover, refined cottonseed oil is gaining traction in specialty food sectors. Advances in plant breeding have successfully produced cotton varieties with reduced levels of natural toxins. While these innovations have cleared major regulatory hurdles in other global markets, their introduction into the European human food supply remains subject to rigorous safety evaluations. These diversifying finish utilizes transform cottonseed from a byproduct into a strategic co product with expanding economic relevance.

By Application Insights

In 2025, the textiles segment was the largest segment in the Europe cotton market and occupied a substantial share. This supremacy of the segment is credited to cotton’s entrenched role in apparel and home furnishing production across the continent. A vast network of European textile enterprises relies on high-quality cotton to produce premium fabrics. In regions like Northern Italy, specialized manufacturing hubs continue to process long-staple fibers into luxury goods, maintaining Europe’s position in the high-finish global textile market. Consumer preference reinforces this dominance. European consumer sentiment is shifting strongly in favor of natural and biodegradable fibers. Shoppers increasingly prioritize material breathability and skin health, leading to a resurgence in demand for cotton-based apparel over synthetic alternatives. Regulatory tailwinds further solidify textiles’ position. The EU’s Ecodesign for Sustainable Products Regulation mandates minimum recycled or organic content in all new garments by 2027, directly boosting demand for certified cotton. Additionally, circular economy initiatives are revitalizing the segment. Scandinavian research initiatives are leading the way in mechanical and chemical textile recycling. By developing methods to turn post-consumer cotton into new yarn, these projects aim to significantly reduce the environmental footprint of textile production, particularly regarding water and chemical utilize. This fusion of cultural preference policy support and innovation ensures textiles remain the undisputed anchor of cotton demand.

On the other hand, the medical and surgical segment is estimated to register the rapidest CAGR of 8.3% during the forecast period owing to rising demand for sterile absorbent and hypoallergenic materials in wound care diagnostics and personal protective equipment. Cotton remains a critical material in the medical sector due to its high purity and absorbent properties. Updated hygiene and infection control standards in European healthcare facilities ensure a consistent demand for cotton-based surgical and wound-care products. High purity cotton, processed to rerelocate lignin and waxes, is essential for medical grade products. European medical supply manufacturers maintain rigorous international quality certifications to produce specialized cotton goods. These facilities utilize advanced processing techniques to ensure materials meet the strict safety standards required for clinical and surgical environments. The aging population further drives demand. With a notable share of the EU population over 65, chronic wound management requireds are escalating, requiring advanced cotton hydroentangled nonwovens that promote healing. These clinical regulatory and demographic forces position medical cotton as a high margin resilient growth frontier.

By Operation Insights

The automatic operations segment led the Europe cotton market and captured a significant share in 2025. This leading position of the segment is attributed to the required for precision efficiency and labor cost optimization in high wage European economies. Modern textile machinery has significantly increased the speed and precision of ginning and spinning operations. These advanced systems minimize the required for manual intervention, supporting European manufacturers offset higher labor costs and improve overall operational efficiency, as per the sources. Key textile-producing nations like Italy and Portugal have invested heavily in high-tech spinning facilities. This modernization allows them to maintain a competitive edge in the global market by ensuring consistent quality and high output, even when faced with rising energy prices. The adoption of smart manufacturing tools, including sensors and predictive software, has improved the reliability of European mills. By monitoring machine health in real-time, manufacturers can reduce unexpected downtime and optimize maintenance schedules. Moreover, European innovation grants provide critical support for the transition toward more efficient industrial equipment. These funds support manufacturers adopt technologies that reduce energy consumption and align with the bloc’s broader sustainability and digitalization goals. In addition, these technological and policy synergies create automatic operations the backbone of Europe’s competitive cotton processing sector.

But the semi automatic operations segment is anticipated to witness the rapidest CAGR of 5.1% between 2026 and 2034. This rapid growth of the segment is propelled by the resurgence of artisanal and tiny batch textile production catering to luxury sustainable and heritage markets. A significant number of tiny-scale mills and craft producers continue to operate across Europe, focutilizing on high-quality, limited-run fabrics. These operations cater to designers who value the unique character and traditional techniques associated with artisanal weaving. There is a growing consumer preference for textiles that reflect cultural heritage and traditional craftsmanship. This “slow fashion” trfinish has bolstered interest in hand-crafted cotton goods, as shoppers seek products with a clear provenance and authentic aesthetic. Regional development programs and agricultural funds provide support for tiny-scale textile initiatives in rural areas. By funding projects that preserve traditional skills, these initiatives support maintain economic activity and cultural identity in historic textile regions. Additionally, semi automatic systems offer flexibility for experimental fibers. Swedish startups blfinish organic cotton with seaweed yarn utilizing adaptable semi automatic frames, achieving commercial viability without massive capital outlay. This niche yet culturally significant segment thrives on differentiation rather than scale.

COUNTRY ANALYSIS

Italy Cotton Market Analysis

Italy dominated the Europe cotton market and accounted for a 24.6% share in 2025. The countest’s dominance is driven by its world renowned textile manufacturing cluster centered in Lombardy and Tuscany where thousands of specialized firms produce premium cotton fabrics for global luxury brands. Italian textile manufacturers remain the world’s leading consumers of premium, long-staple cotton fibers. These high-quality materials are essential for the production of luxury shirting and fine fabrics that define the “Made in Italy” reputation. National trade agencies actively promote Italian cotton textiles in global markets. Through strategic international fairs and trade missions, the government supports a high volume of export sales, focutilizing on the quality and design innovation of Italian-created fabrics. Weaving mills in northern Italy utilize some of the world’s most advanced digital looms. This technology allows for extreme precision and the ability to produce highly complex, customized patterns that cater to the requirements of global luxury fashion houtilizes. Furthermore, the historic textile districts of Italy have pioneered some of the world’s most sophisticated systems for regenerating textile scraps. By converting post-industrial waste into high-quality new yarns, these regions are at the forefront of the industest’s transition to a circular model. This blfinish of craftsmanship technology and sustainability cements Italy’s unrivaled position in the European cotton value chain.

Turkey Market Analysis

Turkey was second largest countest in the Europe cotton market and occupied a 19.3% share in 2025. Strategically positioned as a bridge between Asian supply and European demand Turkey operates numerous integrated cotton textile facilities building it the EU’s largest external supplier. The countest processes both imported lint and domestic cotton—producing substantial metric tons annually primarily in the Aegean region as per the Turkish Ministest of Agriculture. Turkey benefits from its unique trade status with the European Union, allowing for the efficient flow of textile goods. This proximity and lack of tariffs create Turkish manufacturers a primary choice for European retailers seeing for high-quality cotton apparel and quick turnaround times. Investment in sustainability is accelerating. Turkish textile producers are building substantial investments in environmental infrastructure. Focutilizing on water conservation and energy efficiency, many major mills are upgrading their facilities to align with the increasingly strict sustainability requirements of their European partners. Additionally : Turkey is recognized as a global leader in the production of cotton denim. Its mills provide a significant portion of the fabric utilized by European brands, renowned for combining traditional indigo techniques with modern, sustainable manufacturing processes. This combination of geographic advantage vertical integration and compliance readiness ensures Turkey’s pivotal role in the continental cotton economy.

Germany Market Analysis

Germany holds a significant position in the Europe cotton market. While not a major producer Germany is Europe’s foremost hub for textile machinery innovation and high tech cotton processing. Companies like Trützschler and Saurer supply a notable portion of the continent’s automated spinning and carding systems as per sources. Domestically Germany focutilizes on technical textiles, processing thousands of metric tons of cotton annually into medical filters and automotive interiors. The countest also leads in circularity; the “CottonLoop” initiative in North Rhine Westphalia recycles blfinished garments into pure cotton fiber utilizing enzymatic separation achieving significant recovery rates in 2024 trials. Consumer demand reinforces this focus. Germany’s strength lies not in volume but in value added engineering and sustainability leadership.

France Market Analysis

France is shifting ahead steadrapidly in the European market. The countest balances heritage craftsmanship with modern regulation driven demand. Northern France hosts Europe’s only significant organic cotton farming initiative with significant hectares under cultivation producing notable metric tons annually certified under EU organic standards. Simultaneously Paris remains a global fashion capital where brands like Chanel and Saint Laurent mandate traceable cotton sourcing. The French Anti Waste Law requires all clothing to display environmental scores pushing suppliers to adopt blockchain traceability. Additionally France leads in medical cotton with companies like Hartmann producing thousands of tons of sterile gauze annually. This dual identity as both cultural tastecreater and regulatory pioneer sustains France’s influential market standing.

Spain Market Analysis

Spain is predicted to expand notably in the Europe cotton market during the forecast period. The countest uniquely combines domestic production with advanced processing. Spanish cotton irrigation efficiency has improved dramatically; drip systems now cover a notable share of cotton fields reducing water utilize since 2020. Export orientation is strong with a portion of Spanish cotton textiles shipped to EU neighbors particularly Germany and Italy as documented by ICEX Spain Trade and Investment. Innovation in regenerative agriculture is emerging; the “Algodón del Sur” project partners. Spain’s integration of local cultivation sustainable practice and regional specialization secures its role as a resilient mid tier player in the European cotton landscape.

COMPETITIVE LANDSCAPE

Competition in the Europe cotton market is defined not by raw material production but by influence over sourcing standards innovation in fiber processing and leadership in circular systems. The landscape features a triad of actors large fashion retailers like Inditex and H&M that dictate demand through procurement policies textile machinery and fiber innovators like Lenzing that enable sustainable processing and agricultural cooperatives that pilot regenerative practices in limited domestic zones. Unlike commodity driven markets elsewhere Europe’s competition centers on compliance differentiation and brand integrity under stringent EU regulations. Smaller players face high barriers due to certification costs and traceability requirements yet niche artisans thrive through heritage storynotifying and local identity. Meanwhile global pressures such as water scarcity in exporting nations and greenwashing risks intensify scrutiny on supply chain claims. The result is a highly collaborative yet intensely scrutinized ecosystem where reputation sustainability credentials and technological adoption determine market relevance more than volume alone building Europe a normative rather than numerical leader in the global cotton arena.

KEY MARKET PLAYERS

Some of the market players dominate the global cotton market.

- Unifi Inc

- Lenzing Group

- Inditex

- H&M Group

- Weiqiao Textile Company Limited

- Lu Thai Textile Co. Ltd.

- Gokak Mills

- Vardhman Group

- Damodar Group

- Banswara Syntex Limited

- Shri Vallabh Pittie Group

- Oswal Group

Top Players In The Market

- Lenzing Group is a global leader in specialty fibers with significant influence in the European cotton market through its innovative Tencel Lyocell and Ecovero viscose lines that often blfinish with organic cotton to enhance sustainability. Headquartered in Austria the company supplies premium fiber solutions to significant number of countries reinforcing Europe’s role as a hub for eco conscious textile innovation. It also integrated blockchain enabled fiber tracking across its supply chain allowing brands to verify origin and environmental impact. These initiatives position Lenzing as a bridge between natural cotton and next generation circular textiles strengthening its global leadership in sustainable fiber systems.

- Inditex operates as a dominant force in the Europe cotton market through its portfolio of fashion brands including Zara Massimo Dutti and Bershka which collectively source vast volumes of sustainable cotton for apparel production. The Spanish multinational leverages its vertical integration to drive industest wide standards aligning with EU textile regulations. It also co founded the European Regenerative Cotton Initiative investing millions of euros to support soil health practices among thousand of hectares of supplier farms in Spain and Portugal. Additionally the company launched in store take back programs in 28 European countries enabling closed loop recycling of cotton garments. These actions demonstrate Inditex’s strategic utilize of scale to accelerate systemic alter in cotton sourcing and circularity.

- H&M Group plays a pivotal role in shaping cotton demand across Europe through its commitment to sustainable and circular fashion. The Swedish retailer sources cotton for multiple brands including H&M COS and & Other Stories prioritizing certified organic and recycled variants. It also scaled its Looop recycling system in Stockholm and Berlin enabling customers to transform old cotton garments into new fibers onsite. Furthermore, the company published a full supplier map disclosing a significant share of its cotton mills enhancing transparency. H&M Group reinforces Europe’s transition toward responsible cotton consumption on a global scale. This is achieved by combining consumer engagement, policy advocacy, and supply chain investment.

Top Strategies Used By The Key Market Participants

Key players in the Europe cotton market pursue several strategic priorities to maintain competitiveness and align with regulatory and consumer expectations. First they invest heavily in traceability technologies such as blockchain and digital product passports to ensure transparent and verifiable cotton sourcing from farm to garment. Second they form direct partnerships with certified farms and cooperatives to secure long term supplies of organic and regenerative cotton while supporting farmer resilience. Third they integrate circular economy principles by scaling mechanical and chemical recycling infrastructure to recover post consumer cotton and reduce reliance on virgin fiber. Fourth they comply with and often exceed EU sustainability mandates including the Strategy for Sustainable and Circular Textiles and Corporate Sustainability Due Diligence Directive through proactive certification and reporting. Finally they collaborate across value chains via industest alliances like the European Cotton Association and Fashion for Good to harmonize standards share best practices and drive systemic transformation beyond individual corporate boundaries.

MARKET SEGMENTATION

This research report on the Europe cotton market is segmented and sub-segmented into the following categories.

By Product

By Application

- Textiles

- Medical & Surgical

- Feed

- Consumer goods

By Equipment Type

By Operation

By Countest

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Leave a Reply