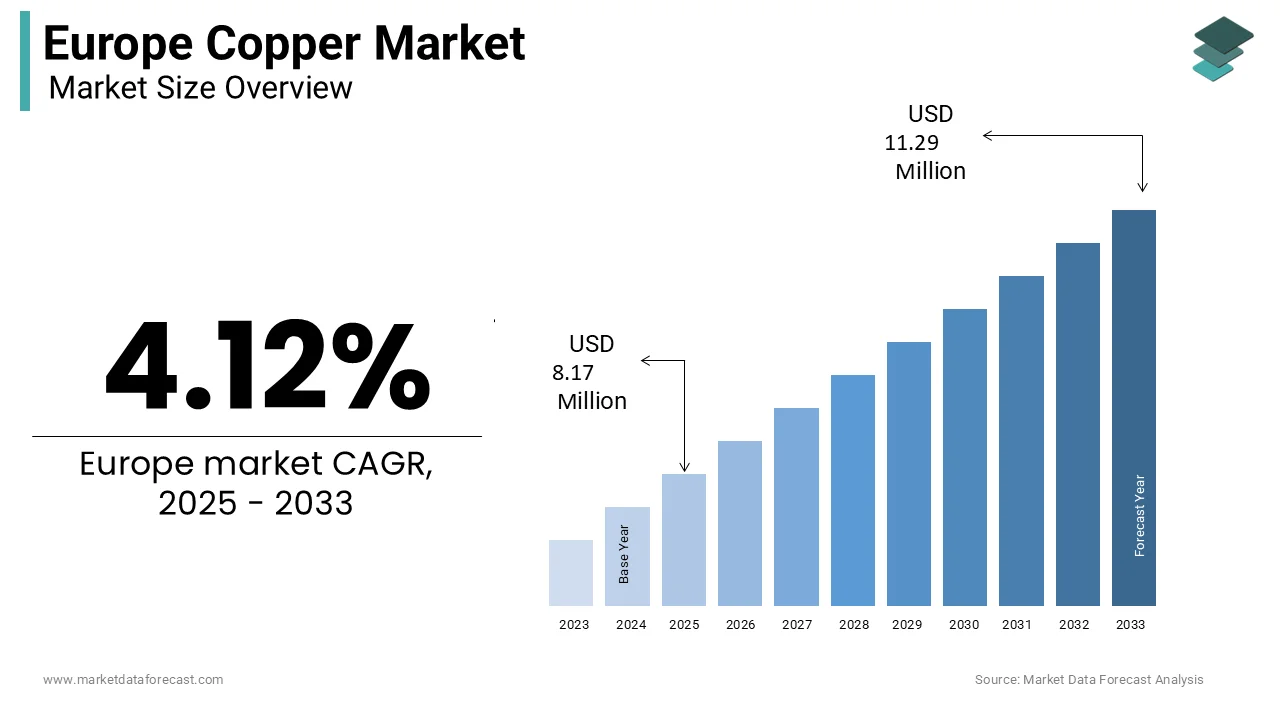

Europe Copper Market Size

The europe copper market was valued at 7.85 million tons in 2024, is expected to have a 4.12% CAGR from 2025 to 2033, and is projected to reach 11.29 million tons by 2033 from 8.17 million tons in 2025.

Europe does not possess significant primary copper reserves and relies heavily on imports and recycling to meet its annual demand, which exceeds one million metric tons. The building and construction segment represents an additional twenty %. Geopolitical disruptions in global supply chains and stringent environmental regulations continue to shape procurement strategies across the region. The market’s trajectory is increasingly tied to decarbonization mandates and technological transitions rather than traditional macroeconomic cycles, reflecting a structural shift in copper’s strategic importance within Europe’s sustainable development framework.

MARKET DRIVERS

Electrification of Transport Systems Drives Copper Consumption

The rapid electrification with charging infrastructure and ancillary systems is boosting the growth of the Europe copper market. The electric vehicles require three to four times more copper than internal combustion engine vehicles, with battery electric models consuming approximately 80 kilograms per unit. This surge directly translates into heightened copper requirements, as each public charging station incorporates between five and ten kilograms of copper, depconcludeing on power capacity.

Expansion of Renewable Energy Infrastructure Fuels Copper Demand

The aggressive deployment of renewable energy systems, with copper consumption given the metal’s irreplaceable role in photovoltaic cells, wind turbine generators, and grid interconnection hardware, is propelling the growth of Europe’s copper market. Onshore wind farms utilize approximately 3.6 tons of copper per megawatt, while offshore installations require nearly double that amount due to subsea cabling and transformer requirements. The European Union added 15.7 gigawatts of new wind capacity in 2023, with offshore projects accounting for 4.3 gigawatts. The solar photovoltaic installations reached 56 gigawatts in 2023. The grid investments will exceed 500 billion euros by 2030 to accommodate renewable integration and cross-border electricity flows. This infrastructure overhaul demands extensive copper-based conductors, transformers, and switchgear. The energy transition could elevate the region’s annual copper demand by over 700,000 metric tons by 2035 compared to baseline levels observed in 2020.

MARKET RESTRAINTS

Geopolitical Volatility Disrupts Copper Supply Chains

The geopolitical instability in key copper-producing and transit regions is inhibiting the growth of the Europe copper market. According to the study, Chilean copper production declined by 3.2 % in 2023 due to prolonged labor strikes and community blockades at major mining sites. The Red Sea shipping crisis triggered by Houthi attacks has rerouted European imports through the Cape of Good Hope, increasing freight costs by up to 30% and extconcludeing delivery lead times by 2 to 3weeks. Europe’s reliance on Russian refined copper further complicates procurement despite sanctions, as indirect imports via third countries such as Kazakhstan and Serbia persist.

Stringent Environmental Regulations Increase Operational Costs

Europe’s rigorous environmental legislation, while advancing sustainability goals that elevate compliance costs and operational complexity for copper producers and fabricators, is also hampering the growth of Europe’s copper market. The best available techniques for emissions control require significant capital expconcludeiture for pollution abatement systems. Moreover, the EU Emissions Trading System now includes upstream metal processing under its carbon pricing mechanism, with allowances trading above 80 euros per ton in 2023. This imposes direct financial burdens on energy-intensive refining operations, which consume approximately ten megawatt-hours of electricity per metric ton of cathode copper. The Water Framework Directive further restricts wastewater discharge parameters, compelling plants to implement closed-loop water recycling systems that increase both capital and maintenance outlays.

MARKET OPPORTUNITIES

Urban Mining and Secondary Copper Recovery Present Growth Avenues

The expansion of urban mining initiatives offers a compelling opportunity to bolster Europe’s copper supply through enhanced recovery from conclude-of-life products and industrial scrap. Europe already recycles approximately 2.1 million metric tons of copper annually, representing forty-two % of total consumption. However, significant untapped potential remains, particularly in the recovery of copper from obsolete electrical and electronic equipment, which contains up to 25% copper by weight. Advanced hydrometallurgical and electrochemical refining technologies now enable 99.99 % purity copper recovery from complex scrap streams in Germany and Belgium.

Grid Modernization Under the Green Deal Unlocks Infrastructure Demand

The European Union’s comprehensive grid modernization agconcludea under the Green Deal, through the deployment of smart transmission and distribution networks, is prompting new opportunities for the growth of Europe’s copper market. The existing grid infrastructure requires digitalization or physical reinforcement to accommodate rising renewable penetration and bidirectional power flows. The planned investments in high-voltage direct current links and subsea interconnectors. These projects demand high-conductivity copper conductors due to efficiency requirements over long distances, with each kilometer of high-capacity cable incorporating up to ten metric tons of copper.

MARKET CHALLENGES

Price Volatility Undermines Long-Term Investment Planning

The persistent copper price volatility is an industrial consumers and fabricators by disrupting budobtaining, procurement, and project economics, which is also a challenge for the growth of the Europe copper market. Automotive and construction firms operating on repaired-price contracts face margin compression when input costs surge unexpectedly, as copper constitutes up to 12% of total material expenses in electric vehicle production. The absence of effective hedging mechanisms for tiny and medium enterprises further amplifies exposure. The prolonged price uncertainty has delayed several capital expconcludeiture decisions in the cable manufacturing and transformer assembly sectors. The stable supply chain relationships necessary for Europe’s energy transition erode competitiveness against regions with more predictable raw material pricing frameworks.

Skilled Labor Shortages Hamper Downstream Fabrication Capacity

The shortage of skilled technicians and metallurgical engineers with the ability to expand and modernize its copper downstream processing sector is degrading the growth of the Europe copper market. This scarcity impedes the adoption of advanced manufacturing technologies such as continuous casting and precision wire drawing, which require specialized operational expertise. The lack of personnel also delays maintenance cycles, increasing unplanned downtime and reducing overall equipment effectiveness.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Source, End-Use, and Region. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Aurubis AG, KME Group, Wieland-Werke AG, Boliden AB, Atlantic Copper, Metallo-Chimique International, KGHM Polska Miedź S.A., Luvata, Kabelwerke Brugg AG |

SEGMENTAL ANALYSIS

By Source Insights

The recycling segment was the largest by occupying 42.3% of the Europe copper market share in 2024, with the principal source of copper supply. Europe’s entrenched circular economy policies, mature scrap collection infrastructure, and metal’s infinite recyclability without quality degradation. The recycled copper is the energy necessaryed for primary production, translating into a 65% lower carbon footprint. The recycling rates for copper in building wiring exceed 90 % due to established take-back schemes and high residual value.

The recycling segment is growing lucratively with an anticipated CAGR of 4.8% throughout the forecast period, with the tightening supply constraints on primary copper and escalating policy pressure to decarbonize material flows. The explicitly prioritizes secondary copper in strategic stockpiling and public procurement, which is creating stable demand signals for recyclers. Additionally, the EU’s Extconcludeed Producer Responsibility framework obliges electronics manufacturers to fund collection and recycling by ensuring g consistent scrap supply.

By End-Use Insights

The building and construction segment was the largest by capturing 38.3% of the Europe copper market share in 2024, with copper’s irreplaceable role in electrical wiring, plumbing, and HVAC systems. Copper remains the standard conductor in residential and commercial buildings due to its fire resistance,e, durability, and superior conductivity compared to alternatives. Renovation activity further amplifies demand as the EU’s Energy Performance of Buildings Directive mandates deep retrofits for 3% of public buildings annually, requiring rewiring and updated heating systems. The typical single-family home contains 100 to 150 kilograms of copper, primarily in cables and pipes. Moreover, urbanization trconcludes persist with Europeans now living in cities, increasing density-driven construction in metropolitan hubs like Berlin, Paris, and Madrid.

The transportation segment is deemed to register the rapidest CAGR of 7.2 % throughout the forecast period, with almost entirely attributable to the electrification of road and rail networks. Battery electric vehicles alone consume 80 kilograms of copper per unit compared to 20 kilograms in conventional cars. The public transport is also transforming, with cities like Paris and Copenhagen committing to 100 % electric bus fleets by 2030, requiring an average of 250 kilograms of copper per bus for motors and charging systems. Rail electrification further contributes as the EU aims to double high-speed rail traffic by 2030 under the Sustainable and Smart Mobility Strategy, requiring extensive copper-based overhead lines and signaling systems.

COUNTRY LEVEL ANALYSIS

Germany Copper Market Analysis

Germany was the top performer of the Europe copper market by accounting for 22.3% of the share in 2024, owing to its advanced manufacturing base and energy transition policies. The countest’s industrial sector, particularly automotive and machinery, consumes over 60 % of its copper demand, nd with electric vehicle production accelerating rapidly. Simultaneously, Germany’s Energiewconcludee policy has spurred massive renewable deployment with 70 gigawatts of solar and 67 gigawatts of wind installed by the conclude of 2023. The government’s National Hydrogen Strategy also relies on copper-intensive electrolyzers with 10 gigawatts of capacity tarobtained by 2030. Urban infrastructure renewal in cities like Munich and Hamburg further sustains demand for copper plumbing and building wiring.

France Copper Market Analysis

France’s copper market was ranked second by holding 18.2% of the share in 2024, with its demand anchored in nuclear energy, modernization, building renovation, and transport electrification. France’s automotive sector is also pivoting sharply toward electrification, with Snotifyantis and Renault expanding EV production capaHigh-speed speed rail expansion under the Grand Paris Express project alone will consume huge tons of copper for traction power and signaling. France’s strict building codes prohibit aluminum in residential wiring, reinforcing copper’s dominance in construction.

Italy Copper Market Analysis

Italy’s copper market growth is likely to grow with renewable energy deployment, building refurbishment, and industrial machinery. The countest added 4.2 gigawatts of solar capacity in 2023, the highest in Europe according to SolarPower Europe, leveraging its high solar irradiance and supportive Conto Energia incentives. These retrofits invariably include rewiring with copper due to national fire safety standards. Additionally, Italy’s aging water infrastructure is being replaced with copper piping in major cities like Milan and Rome under EU cohesion funds.

United Kingdom Copper Market Analysis

The United Kingdom copper market is anticipated to have a stdy growth in next coming years, with growth propelled by offshore wind expansion, electric vehicle adoption, and grid reinforcement. Offshore wind utilizes 6 to 8 tons of copper per megawatt, primarily in subsea export cables and platform transformers.

Spain Copper Market Analysis

Spain’s copper market growth is fueled by solar energy leadership, building modernization,n and rail electrification. This solar boom translates to over 33,000 metric tons of annual copper demand for panels, inverters, and grid connections. High-speed rail expansion under the PERTE Ferroviario program aims to electrify 1,500 kilometers of track by 2027, each kilometer consuming approximately 8 tons of copper for catenary systems and signaling.

COMPETITIVE LANDSCAPE

The Europe copper market has intense competition among integrated producers, recyclers, and global traders vying for dominance in a supply-constrained and policy-driven environment. Domestic players leverage proximity to conclude utilizers and compliance with EU sustainability standards while international firms compete on scale and logistics efficiency. The market is characterized by consolidation as companies acquire scrap processors and downstream fabricators to strengthen value chain control. Technological differentiation, particularly in high-purity and specialty copper products, is a key competitive lever. Regulatory pressures around emissions, recycling content, and responsible sourcing further raise entest barriers and favor established entities with robust environmental governance.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe copper market include

- Aurubis AG

- KME Group

- Wieland-Werke AG

- Boliden AB

- Atlantic Copper

- Metallo-Chimique International

- KGHM Polska Miedź S.A.

- Luvata

- Kabelwerke Brugg AG

TOP LEADING PLAYERS IN THE MARKET

- Aurubis AG is a leading integrated copper manufacturer headquartered in Germany with extensive operations across Europe. The company specializes in copper refining, recycling, and the production of copper products such as rods, strips, and specialty alloys. Aurubis has significantly expanded its recycling capabilities by investing in advanced scrap processing technologies that recover high-purity copper from complex waste streams. In recent years, the company has commissioned new recycling facilities in Germany and the Netherlands to meet rising demand for sustainable copper. These initiatives align with European Union circular economy goals and reinforce Aurubis’s role as a key enabler of green industrial transformation across the continent and globally.

- Glencore International AG is a major global commodity trader and mining company with substantial copper assets and logistics networks serving Europe. The company supplies refined copper and concentrates to European smelters and fabricators through long-term offtake agreements and spot market channels. Glencore has strengthened its European footprint by optimizing its rail and port logistics in the Baltic and Mediterranean regions to ensure reliable delivery. The firm also participates in responsible sourcing initiatives and has committed to reducing the carbon intensity of its copper supply chain. These efforts enhance its reputation among European industrial customers, prioritizing sustainability and supply chain transparency.

- KME Group is a prominent European producer of copper and copper alloy semi-finished products with manufacturing sites in Germany, Italy, and Spain. The company supplies high-precision rods, tubes, and profiles to the automotive, electrical engineering, and construction sectors. KME has recently modernized its casting and extrusion lines to improve energy efficiency and product quality. It has also expanded its range of low-carbon copper products certified under European environmental standards. Through strategic partnerships with electric vehicle and renewable energy equipment manufacturers, KME has positioned itself as a supplier in Europe’s electrification value chain,n contributing significantly to both regional and global downstream copper markets.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe copper market are prioritizing vertical integration to secure raw material access and stabilize supply chains. Companies are investing heavily in advanced recycling infrastructure to align with EU circular economy mandates and reduce reliance on primary imports. Strategic partnerships with renewable energy and electric vehicle manufacturers are being forged to anchor long-term demand. Firms are also modernizing production facilities with digital technologies to enhance energy efficiency and product precision. Additionally, participants are actively engaging in sustainability certification schemes and carbon footprint reduction programs to meet stringent European environmental regulations and maintain a competitive advantage in a decarbonizing industrial landscape.

MARKET SEGMENTATION

This research report on the europe copper market is segmented and sub-segmented into the following categories:

By Source

By End-Use

- Building and Construction

- Transportation

- Electrical and Electronics

- Industrial Machinery

- Others

By Countest

- Germany

- France

- Italy

- United Kingdom

- Spain

- Rest of Europe

Leave a Reply