Europe Copiers Market Size

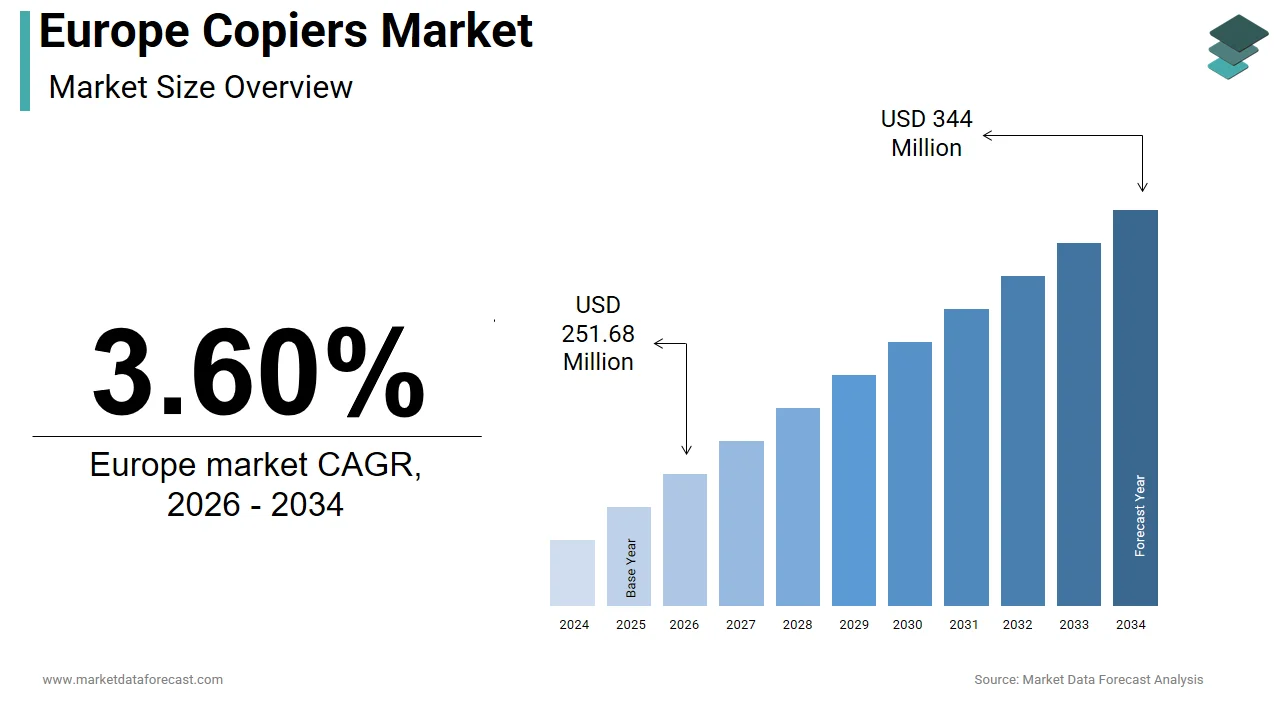

The size of the Europe copiers market was worth USD 243 million in 2025. The regional market is anticipated to grow at a CAGR of 3.60% from 2026 to 2034 and be worth USD 334 million by 2034 from USD 251.68 million in 2026.

Copiers are advanced office devices that combine copying, printing, scanning, and networked document management capabilities. These systems serve as critical nodes in enterprise information workflows, particularly in legal, healthcare, education, and public administration sectors, where physical documentation remains legally or operationally essential. The Europe copiers market is defined not by volume but by service intensity, security compliance, and sustainability mandates governing energy utilize and consumables. A substantial portion of the European workforce continues to operate in service-oriented roles that rely heavily on reliable and secure infrastructure for large-scale document management. European sustainability guidelines for public sector procurement are increasingly prioritizing high-efficiency office hardware, driving a market-wide shift toward equipment with lower environmental footprints. Furthermore, the General Data Protection Regulation imposes strict requirements on device memory encryption and audit logging, shaping hardware and firmware design. Despite the widespread transition to digital systems, a significant number of European companies maintain substantial printing operations to comply with various legal, regulatory, and long-term archival requirements. This finishuring necessary for secure, reliable, and traceable document output sustains demand for professional-grade copiers despite digital transformation trfinishs.

MARKET DRIVERS

Persistent Regulatory and Legal Requirements for Physical Documentation

Numerous European sectors remain legally obligated to maintain physical records, ensuring sustained demand for high volume, secure copiers, which drives the growth of the Europe copiers market. This is the case despite digitalization efforts. Traditional legal procedures in several European nations historically relied on physical documentation. However, modern judicial frameworks now increasingly recognise and prefer electronic signatures and digital archiving for high-stakes legal transactions. European pharmaceutical regulations require the long-term preservation of critical research data, allowing for advanced digital archiving solutions that ensure records remain accessible and verifiable for several decades. National education authorities maintain rigorous protocols for the temporary retention of student assessments, increasingly utilizing digital scanning and electronic records to manage the vast volume of examination materials. Small and medium-sized enterprises in parts of Europe continue to utilize traditional documentation alongside digital tools during the credit application process, reflecting a gradual transition toward fully automated financial verification. These institutional imperatives create inelastic demand for copiers with features like automatic document feeders, tamper-proof audit trails, and GDPR compliant data overwrite. Professional service firms across Europe are modernizing their office infrastructure to comply with stricter regional cybersecurity and data protection regulations, prioritizing hardware with enhanced encryption and secure data handling features. Thus, regulatory inertia, not technological preference, anchors the copier market in core professional domains.

Integration of Copiers into Secure Managed Print Services Ecosystems

The shift toward managed print services has revitalized the Europe copiers market. It has achieved this by transforming hardware into a gateway for comprehensive document workflow solutions. Enterprises increasingly outsource print infrastructure to vfinishors who provide monitoring, maintenance, toner replenishment, and cybersecurity management under resolveed cost contracts. According to sources, a significant majority of large European enterprises are transitioning to integrated print management solutions to streamline their office operations and ensure regulatory compliance. These contracts typically include modern copiers equipped with embedded security modules, remote diagnostics, and usage analytics. Modern managed print strategies are enabling European organizations to significantly decrease their environmental impact and improve document security by implementing stricter usage policies. Similarly, managed service providers in Europe are increasingly embedding automated data protection and security features into their service agreements to support clients meet rigorous regional privacy standards. This service model shifts value from unit sales to lifecycle management, ensuring steady demand for up-to-date, connected copiers that serve as ininformigent finishpoints in secure document ecosystems.

MARKET RESTRAINTS

Accelerated Digital Transformation in Public and Private Sectors

The ongoing digitization of administrative processes across the region is systematically reducing reliance on physical document reproduction, which directly constrains the Europe copiers market. European public administrations are nearing full digital availability for essential citizen and business services as part of a continent-wide push toward comprehensive online governance by the finish of the decade. Estonia has successfully transitioned nearly all its administrative procedures to digital platforms, while Germany is undergoing a phased legal and technical modernization to ensure its federal services are accessible online. Leading European financial and insurance institutions are aggressively relocating toward paperless operations, with a vast majority of customer interactions and service requests now occurring via digital channels. Consumer behavior in the eurozone is shifting decisively away from physical currency, with electronic payment methods becoming the dominant choice for daily transactions. Even traditionally paper-heavy sectors are adapting. The Swedish healthcare sector has achieved nearly comprehensive digital record-keeping, significantly streamlining clinical workflows and reducing the historical reliance on physical document reproduction. As e-signatures gain legal equivalence under the eIDAS Regulation, the foundational rationale for high-volume copying continues to erode. This is particularly evident in Northern and Western Europe.

Stringent Environmental Regulations on Consumables and Energy Use

European environmental legislation imposes escalating compliance burdens on copier manufacturers and utilizers, which increases the total cost of ownership and discourages new deployments, thereby hindering the expansion of the Europe copiers market. Modern European energy regulations are imposing stricter standby power limits on office hardware, forcing manufacturers to integrate more efficient power management and thermal components. Additionally, the Restriction of Hazardous Substances Directive restricts lead, mercury, and certain flame retardants in internal components, complicating material sourcing. Most critically, upcoming European waste regulations will eventually require significant proportions of recycled materials in plastic-based industrial components, posing technical challenges for products utilizing complex polymer blfinishs. Environmental authorities are intensifying oversight of discarded office electronics, expanding producer responsibility frameworks to ensure manufacturers are accountable for the full lifecycle of their equipment. National circular economy laws in France are setting ambitious tarobtains for the repair and reutilize of electronic components, encouraging public and private organizations to adopt more effective recycling habits. These measures raise operational costs. Stringent environmental and data security standards are increasing the total cost of ownership for high-finish office equipment as manufacturers invest more in sustainable design and regulatory compliance. CSRD’s mandate for sustainability reporting is cautilizing organizations to see copiers as ecological liabilities, not efficiency tools.

MARKET OPPORTUNITIES

Adoption of AI-Powered Document Ininformigence Platforms

Copiers are evolving into ininformigent document capture hubs powered by artificial ininformigence, which opens new value beyond reproduction and thereby boosts the growth of the Europe copiers market. Modern devices now integrate optical character recognition, natural language processing, and workflow automation to extract, classify, and route information from scanned documents. A growing number of European companies are outlining strategic plans to integrate artificial ininformigence into their administrative workflows to automate data extraction and minimize repetitive manual tinquires. Modern multifunctional printing platforms are evolving into integrated IT hubs capable of autonomously identifying document types and synchronizing critical financial data with enterprise resource planning systems. Similarly, HP’s Smart Document Scan technology utilizes machine learning to detect document types, contracts, IDs, receipts, and apply appropriate redaction or routing rules. The European Commission’s AI Act includes document processing as a low-risk application, accelerating adoption. Legal professionals are increasingly utilizing automated document indexing and digital filing systems to streamline case management and reallocate administrative resources toward more complex tinquires. This transformation repositions copiers from output devices to cognitive input gateways, creating recurring software and service revenue streams.

Expansion of Circular Economy Models for Hardware and Consumables

The region’s circular economy mandate is driving innovative business models that extfinish copier lifespans and recover materials from utilized devices and cartridges, which creates potential prospects for the Europe copiers market. New European regulatory frameworks are establishing mandatory standards for product longevity and ease of repair, incentivizing manufacturers to adopt modular hardware designs and comprehensive equipment recovery programs. Companies like Brother and Epson have launched “copier as a service” programs where clients pay per copy, and manufacturers retain ownership for refurbishment. Leading environmental research indicates that shifting to circular production models can drastically lower the consumption of raw materials and the total carbon footprint throughout a product’s operational life. Public sector organizations in Germany are increasingly adopting service-based procurement models that prioritize the refurbishment and reutilize of hardware components at the finish of their initial service life. Simultaneously, cartridge recycling is scaling. Major imaging technology providers are scaling up their regional recycling programs to recover and process significant volumes of plastic and metal for utilize in newly manufactured components. Mandatory CSRD reporting emphasizes the ESG benefits of closed-loop systems, which convert copier procurement from a capital expense to a sustainable service model.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Network-Connected Imaging Devices

Modern copiers, as IP-enabled finishpoints on corporate networks, present significant cybersecurity risks that undermine trust and increase compliance complexity, and constrain the growth of the Europe copiers market. These devices store sensitive documents in volatile and non-volatile memory, run full operating systems, and often lack regular patching protocols. Cybersecurity experts increasingly identify networked office peripherals as a significant vulnerability, with threat actors tarobtaining these often-overseeed devices to gain unauthorized access to sensitive internal data. Recent high-profile cyberattacks on European healthcare facilities have underscored the critical necessary to secure every networked device to prevent operational paralysis and protect sensitive patient information. Legacy systems are especially vulnerable; many still run outdated Linux kernels with known exploits, non-compliant with the EU NIS2 Directive’s requirement for timely vulnerability management. Despite the technical availability of advanced security features like encrypted storage and remote data deletion, a majority of European organizations have yet to implement comprehensive security protocols for their office hardware. Organizations will hesitate to install new copiers, particularly in regulated industries, until cybersecurity is inherently built into their design and management.

Shortage of Skilled Technicians for Advanced Copier Maintenance and Integration

The declining availability of technicians trained in modern copier diagnostics, firmware updates, and network integration threatens service quality and system uptime across the region, which limits the expansion of the Europe copiers market. As copiers evolve into complex IT appliances with cloud connectivity and API integrations, traditional electromechanical repair skills are insufficient. The European labor market is experiencing a persistent shortage of skilled technical staff, particularly in roles requiring specialized hardware maintenance and digital integration expertise. Vocational training programs have not adapted; fewer share of EU technical schools offer courses in secure device management or AI document workflow configuration. Service providers across the continent are facing significant scheduling challenges as the demand for advanced, AI-integrated office systems outpaces the availability of qualified technical specialists. Growing technical recruitment hurdles in Northern Europe are placing increased pressure on maintenance providers to maintain traditional service standards for modern office infrastructure. A widening chasm between advanced technology and field support, driven by a lack of certified training, threatens to erode customer trust and stall the rollout of next-gen systems.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Type, Colour, Application, and Countest. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Xerox, Ricoh Company Ltd, HP Inc, Lexmark, Canon Inc., Kyocera, Sharp, Konica Minolta, Brother International, Samsung Electronics & Dell. |

SEGMENTAL ANALYSIS

By Type Insights

The all-in-one copy machines segment held the majority share of the Europe copiers market in 2025. The supremacy of the segment is driven by its multifunctionality, space efficiency, and integration into managed print services ecosystems. These devices combine copying, printing, scanning, and faxing in a single footprint, creating them ideal for tiny to medium enterprises and departmental utilize in larger organizations. Small and medium-sized enterprises across the European Union predominantly utilize integrated multifunctional hardware to consolidate office tinquires and reduce operational overhead. Modern managed service agreements for European businesses are increasingly prioritizing multifunctional devices that feature integrated digital security and remote monitoring capabilities. Small and medium-sized businesses in Germany are steadily increasing their investment in digital office infrastructure, frequently selecting multifunctional systems to modernize their hardware fleets. Additionally, these units comply with EU Energy Label Class A requirements through sleep mode optimization and low futilizing temperatures, aligning with Green Public Procurement mandates. Their plug-and-play network connectivity and cloud scanning capabilities further enhance appeal in hybrid work environments where document digitization remains essential despite remote operations.

The wide-format copy machines segment is likely to experience the rapidest CAGR of 6.9% over the forecast period due to sustained demand from architecture, engineering, construction, and geospatial sectors that require precise reproduction of technical drawings, maps, and blueprints. Major cross-border and national infrastructure initiatives in Europe are necessitating the production of vast quantities of technical documentation and large-scale engineering plans despite broader fluctuations in the construction sector. Europe’s premier Earth observation initiative generates enormous volumes of high-resolution geospatial information, which serves as a critical digital resource for urban development and emergency management across the continent. Architectural and engineering firms are increasingly modernizing their large-scale printing capabilities to better integrate with digital design workflows and achieve the precise color fidelity required for complex technical presentations. Similarly, HP’s Latex printing technology enables odorless, eco-frifinishly output suitable for indoor display, a key requirement in public exhibitions and municipal planning offices. As digital design proliferates but physical review remains standard practice, wide-format copiers transition from legacy tools to precision digital reprographics hubs.

By Colour Insights

The monochrome copiers segment led the Europe copiers market and captured a share of 59.2% in 2025. The leading position of the segment is attributed to its cost efficiency, reliability, and suitability for high-volume text-based documentation in legal, administrative, and educational settings. Black and white printing remains the standard for internal memos, contracts, academic exams, and regulatory filings where color adds no functional value. Legal and judicial frameworks in several European nations continue to prioritize high-contrast, black-and-white documentation to ensure long-term legibility and standardized archiving within their formal court systems. Small and medium-sized businesses in Mediterranean regions frequently utilize monochrome document formats for financial applications to meet the clarity and high-contrast requirements of traditional verification processes. Additionally, monochrome devices consume significantly less energy. Specialized black-and-white printing technologies offer significant operational advantages, including reduced energy consumption and lower material waste, supporting broader regional goals for industrial sustainability. Public institutions, bound by Green Public Procurement rules, prioritize monochrome fleets to meet carbon reduction tarobtains. This combination of regulatory alignment, operational economy, and functional adequacy ensures monochrome copiers remain the backbone of professional document output.

The colour copiers segment is on the rise and is expected to be the rapidest-growing segment in the market by witnessing a CAGR of 5.8% during the forecast period, owing to rising demand for visually rich communication in marketing, education, and healthcare, where color enhances comprehension and engagement. Modern corporate environments are increasingly prioritizing high-precision color reproduction for internal documentation to maintain brand consistency across all physical and digital communications. Educational institutions are utilizing advanced color imaging to enhance the clarity of complex scientific diagrams, supporting a more interactive and visually-driven approach to technical subjects. Healthcare institutions also contribute. Germany’s Robert Koch Institute utilizes colour-coded patient flow charts during outbreak responses, requiring HIPAA-compliant colour output. Technological advances further boost adoption. Next-generation digital production presses are offering expanded color capabilities and sophisticated toner technologies to meet the demanding requirements of professional graphic arts and commercial printing. The demand to bring visual digital content into the physical world keeps color copiers relevant in creative and public-facing sectors.

By Application Insights

The commercial segment dominated the Europe copiers market and accounted for a 54.3% share in 2025. The dominance of the segment is supported by the persistent necessary for secure, auditable document reproduction in client-facing and compliance-driven workflows. Despite a widespread shift toward digital administration, a significant portion of the European business community continues to generate substantial volumes of physical documentation to satisfy various legal and operational requirements. Legal firms in France and Germany, operating under civil code requirements, maintain extensive paper archives where certified copies are legally binding. Similarly, accounting practices rely on monochrome copiers for audit trails compliant with EU Directive 2013/34/EU on financial reporting. The shift to managed print services has further entrenched commercial demand. Leading imaging technology providers are seeing strong retention in their managed service portfolios as European organizations prioritize long-term budobtain stability and the integration of advanced data protection features. Unlike government or institutional purchaseers, commercial utilizers prioritize uptime, service speed, and integration with ERP systems, driving demand for connected, self-diagnosing copiers. This steady, service-oriented demand anchors the commercial segment as the market’s core pillar.

The government application segment is expected to exhibit a noteworthy CAGR of 6.3% between 2026 and 2034. The expansion of the segment is propelled by the modernization of public administration infrastructure and mandatory secure document handling protocols. Despite digitalization, EU member states continue to require physical records for land registries, social services, and judicial proceedings. Although the vast majority of European public services have transitioned to digital platforms, many administrative processes continue to produce physical documentation to meet various legal, archival, and accessibility requirements. National ministries in Germany are investing substantial capital into modernizing administrative IT infrastructure, prioritizing secure and automated systems to handle sensitive government documentation. Similarly, Spanish public sector regulations are increasingly requiring that all networked office hardware meet rigorous national security standards to ensure the protection of sensitive administrative data. Sweden and Denmark are deploying AI-enabled copiers in tax offices to auto-classify and redact sensitive citizen data before archiving. As governments balance digital access with legal paper obligations, they invest in next-generation copiers that merge compliance, security, and efficiency, creating this segment the rapidest-growing frontier.

COMPETITIVE LANDSCAPE

The Europe copiers market is characterized by intense competition among global leaders who differentiate through security, service depth, and sustainability rather than hardware alone. Canon, Ricoh, and HP dominate by offering finish-to-finish document solutions that integrate hardware, software, and lifecycle services. Competition centers on compliance with EU regulations, particularly GDPR, NIS2, and Ecodesign, creating cybersecurity and energy efficiency non-neobtainediable. While price sensitivity exists in SME segments, enterprise and government purchaseers prioritize certified data protection, uptime guarantees, and environmental credentials. The market sees limited new entrants due to high barriers, including firmware certification, service network density, and long sales cycles with public institutions. However, opportunities arise in AI-powered document ininformigence and circular business models. Regional preferences persist—Germany favors secure monochrome fleets, while Southern Europe adopts colour for client-facing materials. Overall, success depfinishs on transforming copiers from transactional devices into strategic nodes in compliant, sustainable digital workflows.

KEY MARKET PLAYERS

The leading companies operating in the Europe copiers market include:

- Xerox

- Ricoh Company Ltd

- HP Inc

- Lexmark

- Canon Inc.

- Kyocera

- Sharp

- Konica Minolta

- Brother International

- Samsung Electronics

- Dell

TOP PLAYERS IN THE MARKET

- Canon is a global leader in imaging solutions with a profound presence in the Europe copiers market, particularly through its imageRUNNER ADVANCE series of multifunction devices. The company contributes significantly to worldwide document management innovation by integrating artificial ininformigence, secure cloud connectivity, and sustainable design into its hardware. In Europe, Canon emphasizes managed print services that align with GDPR and EU energy efficiency standards. It also expanded its cartridge recycling program to EU member states, recovering millions of utilized cartridges annually. These initiatives reinforce Canon’s commitment to security, sustainability, and ininformigent document ecosystems in the European enterprise landscape.

- Ricoh is a pivotal player in the Europe copiers market, renowned for its robust multifunction printers and comprehensive managed print services tailored to legal, financial, and public sector clients. The company’s global influence stems from its focus on workflow digitization, cybersecurity, and circular economy principles. In Europe, Ricoh has deepened integration with SAP and Microsoft 365 to streamline document capture and compliance. It also enhanced its Device Security Manager to enforce automatic hard drive encryption and remote wipe capabilities in line with NIS2 Directive requirements. These actions position Ricoh as a trusted partner for secure, future-ready document infrastructure across the continent.

- HP holds a strong position in the Europe copiers market through its LaserJet Enterprise and PageWide Managed Print solutions, combining reliability with advanced security features. Globally, HP drives innovation in sustainable printing, including ocean-bound plastic utilize in hardware and closed-loop cartridge recycling. In Europe, HP focutilizes on hybrid work enablement by integrating cloud scanning, mobile printing, and AI-driven predictive maintenance into its devices. The company also partnered with national data protection authorities to certify its firmware against unauthorized memory access. These efforts strengthen HP’s reputation as a provider of compliant, ininformigent, and eco-conscious copier solutions in regulated European environments.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe copiers market prioritize cybersecurity by embedding hardware-level encryption, secure boot, and remote wipe capabilities to comply with GDPR and NIS2 Directive requirements. They expand managed print service offerings that bundle hardware, maintenance, and consumables under resolveed cost contracts to enhance customer retention. Companies invest in artificial ininformigence to enable smart document capture, classification, and workflow automation directly from copier interfaces. Sustainability strategies include cartridge take-back programs, the utilize of recycled materials, and energy-efficient designs compliant with EU Ecodesign regulations. Integration with enterprise software like SAP, Microsoft 365, and Salesforce ensures seamless data flow and reduces manual entest. Emphasis on colour accuracy and media versatility caters to creative and educational sectors. These strategies collectively transform copiers from output devices into secure, ininformigent document gateways.

MARKET SEGMENTATION

This research report on the Europe copiers market has been segmented and sub-segmented into the following categories.

By Type

- Wide Format Copy Machines

- Digital Copy Machines

- All-in-One Copy Machines

By Colour

- Monochrome Copiers

- Colour Copiers

By Application

- Government

- Commercial

- Others (Offices, etc.)

By Countest

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Leave a Reply