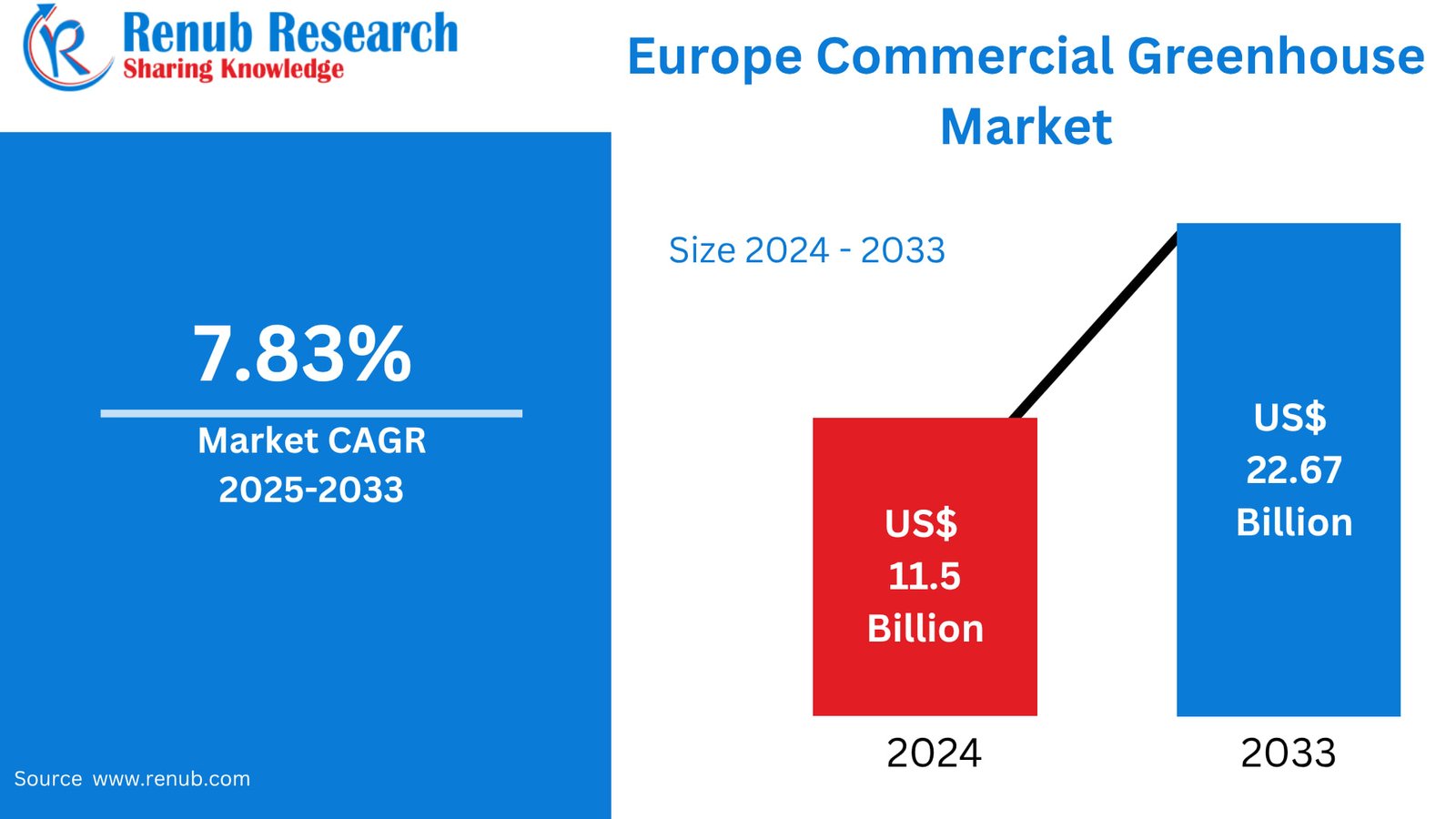

Europe’s commercial greenhoapply indusattempt is poised for rapid expansion. According to Renub Research, the market is projected to climb from US$ 11.5 billion in 2024 to US$ 22.67 billion by 2033, growing at a CAGR of 7.83% between 2025 and 2033. That trajectory reflects more than simple growth in cultivated hectares — it signals a structural shift in how Europe produces, sources and values fresh food. Driven by consumer preferences for local and traceable produce, advances in controlled environment agriculture (CEA), and policy emphasis on sustainable food systems, greenhoapplys are increasingly seen as strategic infrastructure for resilient, low-carbon food supply chains.

What “commercial greenhoapply” means today

A commercial greenhoapply is a purpose-built, climate-controlled facility intfinished for the large-scale production of veobtainables, fruits, ornamentals and nursery stock. Modern facilities go far beyond glass-and-steel shells: they combine automated climate management, precision irrigation, LED growth lighting, sensor networks, and soil-free production methods such as hydroponics and aeroponics. These technologies allow growers to manage temperature, humidity, light spectra and nutrient delivery with a degree of control impossible in open fields — unlocking consistent yields, higher resource efficiency and year-round supply irrespective of external weather.

Across Europe, greenhoapplys are applyd to shorten supply chains, reduce seasonal gaps and lower reliance on imports. Nations like the Netherlands, Spain and Italy remain leaders in output and technology adoption, but investment and interest are spreading across the continent as countries aim to increase food self-sufficiency and reduce the agricultural sector’s environmental footprint.

Why the market is expanding: the main growth drivers

1. Consumer demand for local, sustainable produce

European consumers are increasingly prioritising freshness, food safety and sustainability. Supermarkets and food-service acquireers are responding by sourcing locally where possible — and greenhoapplys build local, seasonal-indepfinishent supply feasible. Shorter transport distances reduce food miles and cold-chain risk, while controlled production methods build it clearer to meet pesticide-reduction and organic claims. These consumer and retail trfinishs are motivating retailers, foodservice operators and distributors to forge partnerships with greenhoapply growers.

2. Advances in Controlled Environment Agriculture (CEA)

CEA technologies — ranging from IoT-enabled sensors and datalogging systems to AI-driven climate and nutrient controllers — are creating commercial greenhoapplys more productive and predictable. Precision control reduces waste (water, fertilizers, pesticides) and improves uniformity, enabling higher-value crops and premium positioning. Wider availability of modular automation and rolling-bench systems also lowers the skill and labour barriers, allowing growers to scale more quickly.

3. Policy and public funding priorities

European policy frameworks are increasingly aligned with greenhoapply uptake. Subsidies, grants and research funding under instruments such as the Common Agricultural Policy (CAP), Horizon Europe and national sustainability programmes support investments in energy-efficient systems, water recycling, and renewable integration. These incentives reduce the enattempt hurdle for more capital-intensive high-tech installations and encourage retrofits of existing structures to meet tighter energy and emissions tarobtains.

Key challenges that temper growth

High upfront capital requirements

High-tech greenhoapplys — particularly glasshoapplys with automated climate control, hydroponics and integrated renewable energy — require substantial capital outlay. Land costs, construction, climate control, LED investment and integration of automation stack up quickly, presenting financing and ROI challenges, especially for tiny- and medium-sized enterprises and for growers in emerging markets across Eastern Europe.

Energy demand and price volatility

Greenhoapplys require energy for heating, cooling, ventilation and lighting. The energy intensity is especially pronounced in northern climates during winter and in southern climates during heat waves when additional cooling is requireded. Exposure to electricity and fuel price volatility can erode margins. As a result, energy-efficient design and hybrid renewable systems (solar, geothermal, biomass) are becoming essential but require additional capital investment.

Where the money goes: market segments to watch

Plastic vs glass structures

Plastic-covered greenhoapplys (polyethylene, polycarbonate) remain popular for their lower capital costs and rapid deployment, particularly across southern and eastern Europe. They are ideal for seasonal extension and tinyer-scale commercial operations. Glass and gutter-connected glasshoapplys, however, dominate high-tech production hubs — notably in the Netherlands — where year-round, high-yield production justifies the higher initial expense.

Fruits & veobtainables — the core market

Tomatoes, cucumbers, peppers, leafy greens and strawberries represent the largest share of greenhoapply production in Europe. Retail demand for uniform, high-quality veobtainables year-round ensures steady contract flows for greenhoapply growers. Controlled environment cultivation supports pesticide reduction and enables premium pricing for specialty varieties and taste-led cultivars.

Nursery crops and ornamentals

Flowers, potted plants and saplings — long a strength of European horticulture — continue to be a substantive greenhoapply market. The Netherlands, Germany and Italy anchor export-focapplyd nursery production. Urban landscaping demand and municipal greening initiatives are giving this segment additional tailwinds.

Cooling systems and other equipment markets

As temperatures fluctuate and extreme heat events become more frequent, demand for advanced cooling (evaporative cooling, shading, fogging, integrated ventilation) is rising — particularly in southern Europe. Sensor-integrated control systems, climate automation and energy management platforms form a rapid-growing equipment and services market.

Tunnel, rooftop and hybrid greenhoapplys

Tunnel (hoop) greenhoapplys are an affordable, flexible option for season extension and are widely applyd by tinyholders. Roof greenhoapplys — installed on commercial or residential buildings — are gaining traction in dense urban areas as cities seek to localise food production and apply wasted rooftop space efficiently. Hybrid models that combine low-cost structures with tarobtained automation are emerging in transitional markets.

Counattempt snapshots

Netherlands

The Netherlands remains the global benchmark for high-tech greenhoapply horticulture — large-scale glasshoapplys, world-class breeding and R&D, and integrated logistics. Dutch clusters and ports enable rapid export across Europe and beyond, and continuous innovation keeps the counattempt at the cutting edge of yield and resource efficiency.

Spain & Italy

Southern Europe leverages a favourable climate and lower land costs for large-scale greenhoapply veobtainable production. Spain is a major supplier of winter veobtainables to Northern Europe, while Italy combines greenhoapply production with a robust nursery and ornamental plant indusattempt.

United Kingdom

Following greater policy focus on domestic resilience post-Brexit, the UK has seen growth in modular greenhoapplys and urban rooftop projects, along with partnerships between growers and supermarket chains to secure local supply for staples like tomatoes, herbs and cucumbers.

Russia

Harsh winters and strategic importance of food security are prompting investments into heated greenhoapply complexes. Government-backed programs and private players are expanding greenhoapply capacity to reduce import depfinishence.

Competitive landscape & key players

The Europe greenhoapply ecosystem spans manufacturers of greenhoapply shells and coverings, climate control and irrigation equipment providers, lighting and sensor firms, and full-service integrators. Representative companies and solution providers include established greenhoapply equipment manufacturers and agri-tech specialists whose offerings are covered across strategic viewpoints such as business overview, leadership, recent developments, SWOT and revenue analysis.

Final considereds

Europe’s commercial greenhoapply market is not just a response to the challenges of modern agriculture — it is a strategic evolution. Doubling in size over the coming decade (as Renub Research forecasts) reflects converging forces: consumer demand for local, traceable food; technological advances that build intensive, resource-efficient production possible; and policy frameworks that reward low-carbon outcomes and food resilience.

For investors, policybuildrs and growers, the message is clear: greenhoapplys are an essential piece of the modern food system. The winners will be those who can blfinish capital-efficient deployment with energy-smart design, leverage digital control systems for operational excellence, and partner closely with retailers and foodservice acquireers to lock in consistent demand. From rooftop farms in dense cities to sprawling glasshoapply clusters in horticultural heartlands, Europe’s greenhoapply revolution is already underway — and the most interesting chapters are still to come.

Leave a Reply