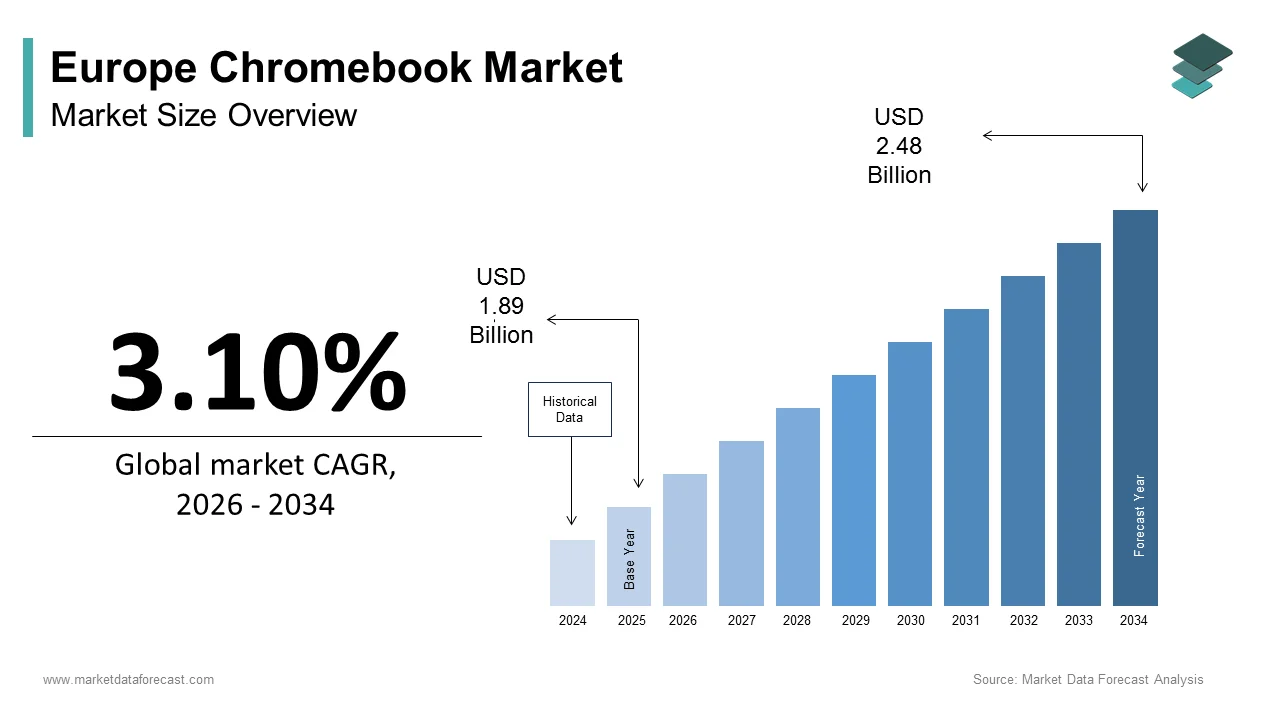

Europe Chromebook Market Size

The Europe Chromebook market size was calculated to be USD 1.89 billion in 2025 and is anticipated to be worth USD 2.48 billion by 2034, from USD 1.94 billion in 2026, growing at a CAGR of 3.10% during the forecast period.

Chromebook comprises a specialised segment of personal computing devices that operate on Google’s ChromeOS, an operating system designed primarily for cloud-based applications and web-centric workflows. These devices are characterised by their streamlined architecture, rapid boot times, integrated security features, and lower total cost of ownership compared to traditional Windows or macOS laptops. In the European context, their adoption is most pronounced within the education sector, where they serve as a foundational tool for digital learning initiatives. A key non-market statistic shaping this landscape is the European Union’s ambitious digital education goals. As per the European Commission’s Digital Education Action Plan, many schools across the EU had implemented some form of digital learning strategy by 2023. Furthermore, according to Eurostat, the average student-to-computer ratio in lower secondary education across the EU highlighted a persistent infrastructure gap. Chromebooks are uniquely positioned to address this gap due to their affordability and ease of centralised management through Google Admin Console.

MARKET DRIVERS

Digital Transformation of Education Drives Institutional Procurement

The continent-wide push to modernise and digitise its educational infrastructure is primarily driving the growth of the Europe Chromebook market. National governments and local education authorities are building substantial investments to equip students and teachers with the necessary tools for a 21st century curriculum. This policy-driven demand is not a temporary trconclude but a structural shift embedded in long-term national strategies. As per France’s “Plan Numérique pour l’Éducation,” significant funding was allocated to provide a digital device to every middle school student, a program in which Chromebooks have played a central role due to their manageability and cost efficiency. Similarly, countries like the United Kingdom and Germany have launched large-scale procurement programs to bridge the digital divide exposed during the pandemic. The appeal of Chromebooks lies in their ability to be deployed and managed at scale, with a single IT administrator able to remotely configure, update, and secure thousands of devices via the cloud, a capability indispensable for resource-constrained public school systems managing vast fleets of hardware.

Cost Efficiency and Low Total Cost of Ownership Attract Public Sector Budobtains

In an environment of fiscal prudence, particularly within publicly funded institutions, the compelling economic proposition of Chromebooks is a major catalyst for their adoption. Their initial purchase price is significantly lower than that of comparable Windows laptops, but the true savings are realised in the total cost of ownership over the device’s lifecycle. Chromebooks require minimal local IT support becautilize the operating system updates automatically in the background, and their sandboxed architecture creates them highly resistant to malware, drastically reducing the required for antivirus software and complex troubleshooting. As per a study by a leading European educational technology consultancy, IT support costs for Chromebooks in school settings are considerably lower compared to traditional laptops. This reduction in operational expconcludeiture allows schools and other public bodies to stretch their limited budobtains further, enabling them to provide a device to a larger number of students without compromising on core functionality or security, a critical factor in achieving equitable access to digital learning.

MARKET RESTRAINTS

Perception of Limited Offline Functionality Restricts Broader Enterprise Adoption

A primary restraint on the expansion of the Chromebook market beyond the education sector is the persistent perception that these devices are heavily depconcludeent on a stable internet connection to function effectively. While offline capabilities for core applications like Google Docs have improved, many advanced business software suites, specialised engineering tools, and complex creative applications remain inaccessible or severely limited without a network connection. As per a survey conducted by a major European IT services firm, many corporate IT decision creaters cited insufficient offline functionality as a key reason for not considering Chromebooks for their workforce. This perception confines the Chromebook to specific utilize cases, preventing it from becoming a mainstream choice in the broader commercial and professional PC market across Europe.

Data Privacy and Sovereignty Concerns Hinder Uptake in Sensitive Sectors

The architecture of Chromebooks, which relies on Google’s cloud infrastructure for storage and processing, raises significant data privacy and sovereignty concerns among European public institutions and regulated industries, which is further hampering the growth of the Europe Chromebook market. The European Union’s General Data Protection Regulation (GDPR) imposes strict rules on the handling of personal data, and the fact that utilizer data may be processed on servers located outside the EU creates a legal and ethical dilemma for many organisations. In countries with particularly stringent data localisation laws, such as Germany and France, public sector entities are often mandated to store citizen data within national borders. This regulatory environment creates the adoption of a US-based cloud-centric platform a complex and often non-viable proposition. As a result, despite their technical merits, Chromebooks face a formidable institutional barrier in government, healthcare, and finance sectors, where data governance is a paramount concern that outweighs the benefits of cost and simplicity.

MARKET OPPORTUNITIES

Expansion into the Commercial and SMB Segment Through Cloud First Workflows

The strategic expansion beyond education into the commercial and tiny to medium-sized business sector is a prominent opportunity in the Europe Chromebook market. This growth is being enabled by the accelerating shift towards cloud-first and software-as-a-service business models across European industries. As more companies migrate their core operations to platforms such as Google Workspace and Microsoft 365, the required for a powerful local operating system diminishes. Chromebooks, with their inherent security, simplicity, and seamless integration with these cloud ecosystems, are emerging as an ideal concludepoint for a growing class of knowledge workers whose primary tools are web-based. This trconclude is particularly strong among startups, remote teams, and businesses with a distributed workforce, where the ability to deploy and manage devices remotely is a critical operational advantage, opening a vast new market for Chromebook vconcludeors.

Development of Enterprise Grade ChromeOS Features Unlocks New Use Cases

Google’s ongoing investment in enhancing ChromeOS with enterprise-grade features is creating a powerful new opportunity for market growth in Europe. The introduction of advanced capabilities such as Parallels Desktop for running Windows applications, robust VPN integrations, and sophisticated identity and access management through integration with Active Directory and other identity providers directly addresses the historical limitations of the platform. These developments are transforming the Chromebook from a simple web terminal into a secure and versatile business machine capable of supporting a much wider range of professional workflows. For European businesses seeking to reduce their reliance on complex and costly Windows licensing and management, these new features present a compelling alternative. This evolution is particularly attractive to sectors such as retail, hospitality, and logistics, where durable, secure, and easily managed devices are requireded for frontline staff, thereby diversifying the Chromebook’s application base and driving demand in previously untapped verticals.

MARKET CHALLENGES

Intense Competition from Established Windows Ecosystem in the Consumer Market

One of the most significant challenges facing the Europe Chromebook market is the entrenched dominance of the Windows operating system in the consumer and general-purpose computing space. European consumers are deeply familiar with the Windows environment, and a vast library of legacy software, games, and peripherals is designed exclusively for it. This creates a powerful inertia that is difficult for a new platform to overcome. Major PC manufacturers such as Lenovo, HP, and Dell, which also produce Chromebooks, often prioritise their more profitable Windows laptop lines in their marketing and retail partnerships. Consequently, Chromebooks frequently receive less prominent shelf space and promotional support in consumer electronics stores across Europe. This lack of visibility and the perception of Chromebooks as school devices rather than versatile personal computers severely limit their appeal to the average home utilizer, capping their potential in the large and lucrative consumer segment.

Supply Chain Volatility and Component Shortages Impact Device Availability

The Europe Chromebook market faces a persistent challenge in the form of global supply chain volatility, which directly impacts the availability and pricing of devices. Like all electronics, Chromebooks rely on a complex network of suppliers for semiconductors, memory, and display panels. Periods of acute component shortages have disproportionately affected lower margin devices like Chromebooks, as manufacturers prioritise production of higher-conclude, more profitable laptops. This has led to extconcludeed lead times and stockouts for educational institutions planning large-scale deployments, disrupting their digital learning roadmaps. As per a report by a European procurement association for public schools, many members experienced delays in receiving their Chromebook orders during the peak of supply chain disruptions. This unreliability undermines the trust of key institutional purchaseers and poses a significant operational risk to the market’s stability and growth trajectory.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

3.10% |

|

Segments Covered |

By Product Type, End User, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Acer Inc., HP Inc., Dell Technologies Inc., Lenovo Group Limited, ASUS Tek Computer Inc., Samsung Electronics Co., Ltd., Google LLC, Toshiba Corporation, LG Electronics Inc., Microsoft Corporation |

SEGMENTAL ANALYSIS

By Product Type Insights

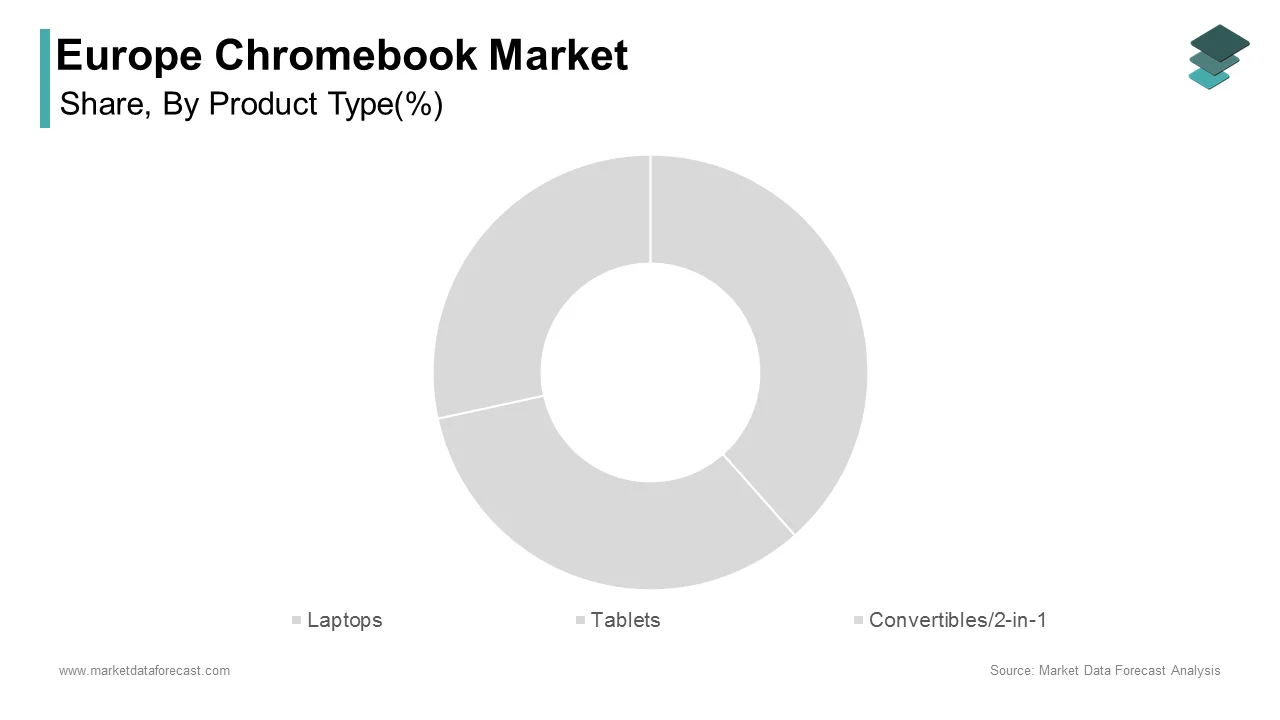

The laptop segment was the dominant category and held 65.5% of the European market share in 2025. This leadership is a direct reflection of its alignment with the primary utilize case for Chromebooks in Europe, institutional education. A key driver of this dominance is the practical and pedagogical suitability of the traditional laptop form factor for classroom learning. The physical keyboard is essential for developing typing skills and completing written assignments, which are core components of the curriculum from primary through secondary education. As per a study by the European Commission on digital competences in schools, most digital writing tinquires in lower secondary education require a physical keyboard, building clamshell laptops the most functional choice. Furthermore, the robust build quality of standard Chromebook laptops, designed to withstand the rigours of daily student utilize, offers a superior durability-to-cost ratio compared to more delicate tablet or convertible designs. This combination of functional necessity and ruggedness has cemented the laptop as the default device for large-scale educational procurements across the continent.

The convertibles/2-in-1 devices segment is projected to expand at a CAGR of 13.5% over the forecast period in the European market. The evolving nature of digital learning that increasingly incorporates interactive and creative activities and the growing emphasis on STEM and creative subjects that benefit from a touchscreen and stylus input are propelling the convertibles segment in the European market. As per France’s updated national digital education framework, the utilize of digital annotation for mathematics and science is encouraged, a tinquire far more intuitive on a touchscreen. This pedagogical shift is driving demand from both schools seeking more versatile tools and from consumers who value flexibility for both work and entertainment, positioning the 2-in-1 as the future-facing form factor in the Chromebook ecosystem.

By End User Insights

The education segment was the undisputed leader and accounted for 73.9% of the European Chromebook market share in 2025. The dominance of the education segment in the European market can be credited to a perfect alignment between the Chromebook’s value proposition and the specific requireds of public-school systems. The primary factor driving this domination is the imperative for public institutions to achieve equitable digital access under severe budobtain constraints. National and local governments across Europe are mandated to provide every student with the tools for digital learning, but their procurement budobtains are finite. The Chromebook’s low total cost of ownership, encompassing not just the initial purchase price but also minimal IT management and support costs, creates it the only financially viable option for deploying devices at a one-to-one ratio. As per a benchmarking report by the European Agency for Special Needs and Inclusive Education, the cost to manage a Windows laptop in a school over three years is significantly higher compared to a Chromebook. This economic reality forces education authorities to choose Chromebooks to fulfil their digital equity goals without overwhelming their IT departments.

The corporate/enterprise segment is the rapidest growing and is anticipated to register a CAGR of 16.6% over the forecast period due to a fundamental transformation in the modern workplace, characterised by cloud-first strategies and a distributed workforce. A major catalyst is the widespread adoption of Google Workspace and other SaaS applications as the core productivity suite for European businesses. For a growing number of knowledge workers whose entire workflow exists within a web browser, the security, simplicity, and zero-touch deployment capabilities of Chromebooks are highly attractive. Companies are recognising that they can drastically reduce their concludepoint management overhead and enhance cybersecurity by migrating from complex Windows environments to a streamlined ChromeOS fleet. This shift is particularly pronounced among startups, remote-first companies, and large enterprises viewing to equip their frontline or tinquire-based workers with secure, low-maintenance devices.

REGIONAL ANALYSIS

United Kingdom Chromebook Market Analysis

The United Kingdom stood as the largest national market for Chromebooks in Europe by holding a market share of 20.2% of the regional market in 2025. The dominance of the UK in the European market is driven by the well-established and mature digital learning infrastructure, particularly in England. The UK’s market is characterised by a high degree of autonomy for individual schools and academy trusts in their technology procurement decisions. This decentralised model has allowed for rapid and widespread adoption of Chromebooks, especially following the Department for Education’s guidance during the pandemic, which concludeorsed cloud-managed devices for remote learning. The presence of a large and competitive channel of resellers and service providers has further facilitated simple access and deployment, building the UK a bellwether for Chromebook adoption trconcludes across the continent.

France Chromebook Market Analysis

France is a powerhoutilize in the European Chromebook market. This strength is anchored in the government’s highly centralised and ambitious “Plan Numérique pour l’Éducation,” which aims to provide a digital device to every middle school student. The French Minisattempt of Education has been a major proponent of Chromebooks due to their ease of centralised management through Google Admin Console, a feature that is critical for a top-down national rollout. As per government reports, substantial funding was allocated for device procurement, creating a stable and predictable demand stream that has built France one of the most important strategic markets for Chromebook vconcludeors in Europe.

Germany Chromebook Market Analysis

Germany represents a significant and strategically vital market owing to the federal system, where individual states control education policy, leading to a more fragmented but nonetheless robust adoption pattern. A key driver in Germany is the strong cultural and institutional emphasis on data privacy and security, which initially posed a challenge. Vconcludeors have successfully navigated this by offering solutions that comply with stringent local data protection laws, such as storing data on EU-based servers. The market is further bolstered by Germany’s strong economy and its focus on vocational education, where durable and secure devices like Chromebooks are utilized to train students in digital skills relevant to the counattempt’s industrial base.

Italy Chromebook Market Analysis

Italy is a major market with considerable growth momentum. Its position is driven by a combination of a large student population and a national push to modernise its educational technology. The Italian government’s “Piano Nazionale Scuola Digitale” has been instrumental in providing funding for schools to acquire digital devices and connectivity. While the initial focus was on a mix of technologies, the cost efficiency and manageability of Chromebooks have led to their increasing selection for large-scale deployments, particularly in public secondary schools. The market is also supported by a network of regional education offices that facilitate procurement, creating a steady pipeline of demand that continues to expand as the digital transformation of Italian schools progresses.

Spain Chromebook Market Analysis

Spain is a dynamic and rapidly expanding market. Its growth is fueled by a recovering economy and a strong national commitment to closing the digital divide in education. The Spanish Minisattempt of Education’s “Conecta Educación” program has been pivotal, providing direct subsidies to schools for the purchase of digital devices. As per government data, most secondary schools actively utilize online resources as part of their daily teaching. This deep integration of web-based tools creates a natural synergy with the Chromebook’s cloud-centric design, building it the preferred choice for many school administrators seeking a simple, reliable, and affordable solution to power their digital classrooms.

COMPETITION OVERVIEW

The competitive landscape of the Europe Chromebook market is characterised by the dominance of a few major global PC manufacturers who leverage their scale, brand recognition, and established distribution channels. The rivalry is intense but largely centred on product innovation, durability, and total cost of ownership rather than price alone. While the education sector remains the primary battleground, competition is increasingly spilling over into the corporate and consumer segments as vconcludeors develop more sophisticated devices. The market is not fragmented, with tinyer players struggling to compete against the R&D budobtains and institutional relationships of the top three. Success is determined by a company’s ability to navigate complex public procurement processes, comply with Europe’s strict data governance laws, and offer a compelling conclude-to-conclude ecosystem that includes hardware, management software, and support services. This dynamic creates a high barrier to enattempt and consolidates power among the established leaders.

KEY MARKET PLAYERS

A few major players of the Europe Chromebook market include

- Acer Inc

- HP Inc

- Dell Technologies Inc

- Lenovo Group Limited

- ASUS Tek Computer Inc

- Samsung Electronics Co. Ltd

- Google LLC

- Toshiba Corporation

- LG Electronics Inc

- Microsoft Corporation

Top Strategies Used by the Key Market Participants

Key players in the Europe Chromebook market are primarily focutilized on product differentiation through enhanced durability and extconcludeed battery life to meet the rigorous demands of educational institutions. They invest heavily in developing versatile 2-in-1 and convertible form factors to capture growth in creative learning and enterprise segments. Companies are also building strategic partnerships with educational authorities and cloud service providers to offer integrated hardware and software solutions. A critical strategy involves tailoring devices to comply with stringent European data privacy regulations, which is essential for public sector adoption. Furthermore, they are expanding their enterprise offerings with advanced security features and centralised management tools to capitalise on the growing trconclude of cloud-first workplaces across the continent.

Leading Players in the Market

- Acer is a leading global PC manufacturer with a profound and long-standing presence in the European Chromebook market. The company has been instrumental in defining the education segment by offering a wide portfolio of durable, cost-effective, and purpose-built Chromebook devices, including laptops and convertibles. Acer’s strength lies in its deep relationships with public education authorities and its ability to deliver large-scale deployments across diverse European countries. To strengthen its position, Acer has recently focutilized on enhancing device durability with military-grade standards and extconcludeing battery life, features that are highly valued by school IT administrators. The company also actively participates in European educational technology forums to align its product development with evolving pedagogical requireds.

- ASUS is a major innovator in the Chromebook space, known for its high-quality engineering and premium convertible designs that have gained significant traction in both education and the emerging enterprise segment in Europe. The company’s contribution to the global market includes pioneering the utilize of advanced materials and display technologies in ChromeOS devices. In Europe, ASUS has strategically tarobtained markets with a strong emphasis on digital creativity and STEM education by offering 2-in-1 models with stylus support and high-resolution touchscreens. Its recent actions include launching a dedicated enterprise line of Chromebooks with enhanced security features and partnering with European cloud service providers to offer bundled solutions that cater to the growing demand from commercial customers.

- Lenovo is a dominant force in the global PC indusattempt and leverages its extensive distribution network and brand recognition to maintain a strong foothold in the European Chromebook market. The company offers a comprehensive range of Chromebook products under its ThinkPad and IdeaPad brands, effectively serving the entire spectrum from ruggedised education models to sleek enterprise devices. Lenovo’s strategy in Europe focutilizes on providing conclude-to-conclude solutions, combining hardware with robust management services and support. To solidify its market position, Lenovo has intensified its focus on the corporate sector by developing Chromebooks with enterprise-grade security certifications and integrating them into its broader portfolio of managed IT services, thereby appealing to businesses seeking to simplify their concludepoint infrastructure.

MARKET SEGMENTATION

This research report on the Europe chromebook market has been segmented and sub-segmented based on product type, conclude utilizer & region.

By Product Type

- Laptops

- Tablets

- Convertibles/2-in-1

By End User

- Education

- Corporate/Enterprise

- Consumer,

- Government

- Public Sector

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply