Europe Chlor Alkali Market Report Summary

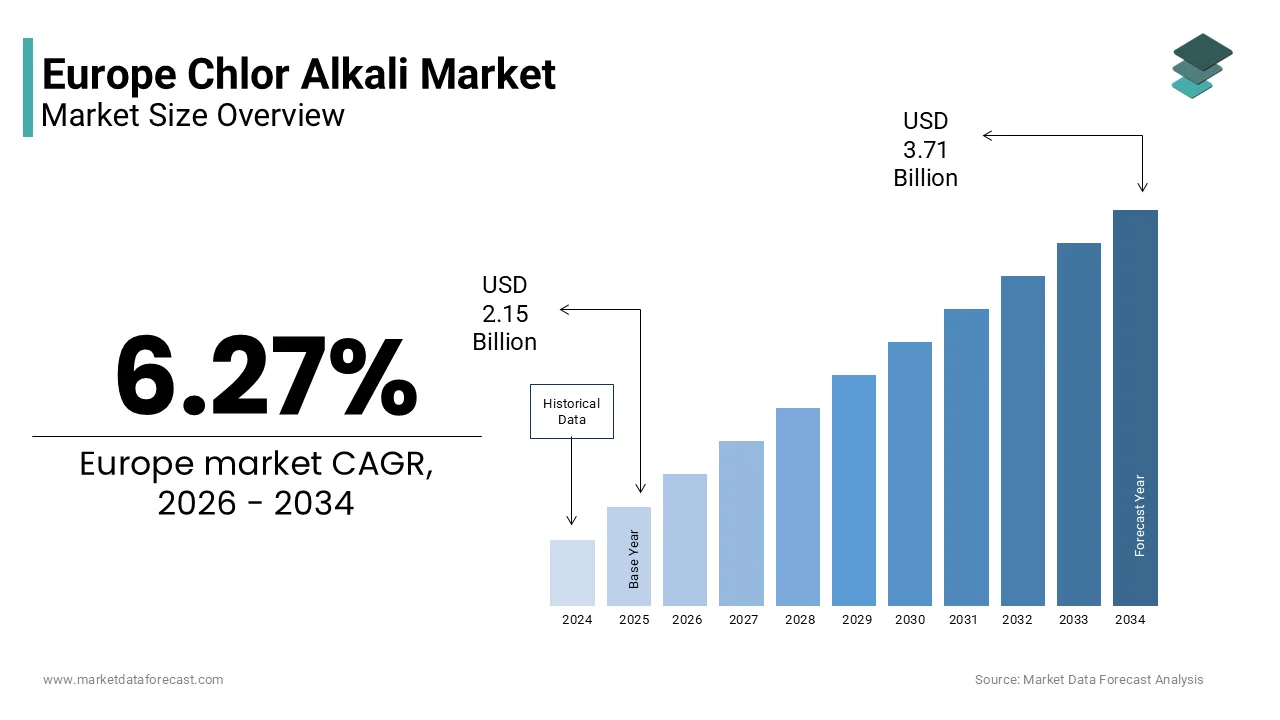

The Europe chlor alkali market was valued at USD 2.15 billion in 2025, is estimated to reach USD 2.28 billion in 2026, and is projected to reach USD 3.71 billion by 2034, growing at a CAGR of 6.27% during the forecast period. Market growth is driven by increasing demand for chlorine and caustic soda across key industries such as construction, chemicals, water treatment, and manufacturing. The expanding utilize of PVC in infrastructure development, along with rising investments in industrial and urban construction projects, is further supporting market growth. In addition, growing demand for water purification and sanitation solutions is contributing to steady market expansion across Europe.

Key Market Trfinishs

- Rising demand for PVC in construction applications is driving growth in the chlor alkali market.

- Increasing utilize of chlorine in water treatment and sanitation is supporting market expansion.

- Growing industrial and infrastructure development is boosting demand for chlor alkali products.

- Expansion of chemical manufacturing industries is enhancing market growth.

- Technological advancements in production processes are improving efficiency and sustainability.

Segmental Insights

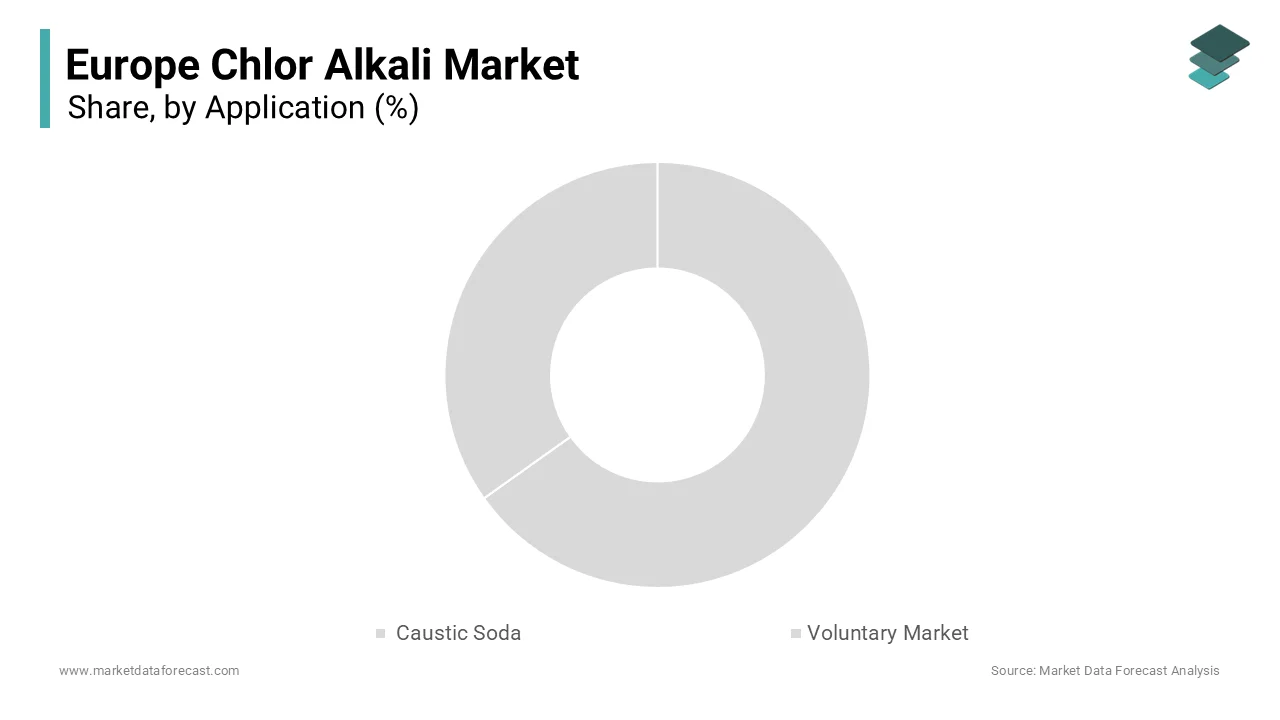

- Based on application, the vinyls segment was the largest and held 36.3% of the Europe chlor alkali market share in 2025. This dominance is attributed to the extensive utilize of PVC in construction applications such as pipes, window profiles, flooring, and cable insulation, driving consistent demand for chlor alkali products.

Regional Insights

- The Europe chlor alkali market is experiencing steady growth across key countries, supported by industrial expansion and infrastructure development.

- Germany was the largest contributor, accounting for 26.1% of the Europe chlor alkali market share in 2025, driven by a strong chemical manufacturing base, advanced industrial infrastructure, and high demand for PVC and related products.

Competitive Landscape

The Europe chlor alkali market is highly competitive, with key players focutilizing on capacity expansion, process optimization, and sustainability initiatives to strengthen their market position. Companies are investing in energy efficient production technologies and strategic collaborations to meet growing demand. Prominent players in the Europe chlor alkali market include INEOS Group, Solvay SA, Akzo Nobel N V, Olin Corporation, Kemira, Occidental Petroleum Corporation, Tata Chemicals Limited, Formosa Plastics Corporation, Tosoh Corporation, Covestro, Vynova Group, and Nobian.

Europe Chlor Alkali Market Size

The Europe chlor alkali market size was valued at USD 2.15 billion in 2025 and is projected to reach USD 3.71 billion by 2034 from USD 2.28 billion in 2026, growing at a CAGR of 6.27%.

Chlor alkali represents a foundational pillar of the continent’s chemical indusattempt characterized by the electrochemical production of chlorine caustic soda and hydrogen from brine. This sector is intrinsically linked to the health of downstream industries including polyvinyl chloride manufacturing, water treatment, pharmaceuticals, and pulp and paper production. The operational landscape is defined by the membrane cell technology which has largely replaced older mercury and diaphragm methods due to environmental regulations. As per Eurostat, the chemical indusattempt remains one of the largest manufacturing sectors in the European Union, contributing significantly to industrial output and employment. The production process is highly energy intensive, creating it sensitive to electricity prices and availability. According to the European Chemical Indusattempt Council, the sector is undergoing a strategic transformation towards sustainability and circular economy principles. The integration of chlor alkali plants with renewable energy sources is becoming a priority to reduce carbon footprints. According to the International Energy Agency, industrial electrification is a key component of Europe’s decarbonization strategy. The market operates within a strict regulatory framework governed by the Industrial Emissions Directive and REACH regulations. These frameworks mandate rigorous control over hazardous substances and emissions. The interdepfinishence between chlorine and caustic soda production creates a unique market dynamic where demand for one product often influences the supply of the other. This balance is critical for maintaining operational efficiency and economic viability. The region’s focus on green chemisattempt and resource efficiency continues to shape investment decisions and technological advancements in chlor alkali production facilities across Europe.

MARKET DRIVERS

Sustained Demand from Polyvinyl Chloride Manufacturing

The robust demand for chlorine as a key feedstock in the production of polyvinyl chloride is majorly driving the growth of the Europe chlor alkali market. PVC is a versatile plastic widely utilized in construction, automotive, healthcare, and packaging sectors due to its durability and cost effectiveness. As per Plastics Europe, the construction indusattempt is a major consumer of PVC in Europe, driven by applications in pipes, window profiles, and flooring. The ongoing renovation wave initiated by the European Commission to improve energy efficiency in buildings has spurred demand for PVC based insulation and resolvetures. As per the European Construction Indusattempt Federation, significant investments are created annually in building refurbishment projects which require substantial amounts of PVC materials. The lightweight and corrosion resistant properties of PVC build it an ideal substitute for traditional materials like metal and wood. Furthermore, the recyclability of PVC aligns with the European Union’s circular economy action plan, encouraging its continued utilize in sustainable construction practices. The automotive sector also contributes to demand through the utilize of PVC in interior components and underbody coatings. The stability of the construction sector provides a consistent baseline for chlorine consumption. Manufacturers of chlor alkali benefit from long term contracts with PVC producers, ensuring steady revenue streams. The expansion of infrastructure projects across emerging European markets further supports this demand. This structural reliance on PVC ensures that chlorine production remains central to the chemical value chain.

Critical Role in Water Treatment and Hygiene Applications

The essential role of caustic soda and chlorine in water treatment and hygiene applications is further boosting the Europe chlor alkali market expansion. Caustic soda is extensively utilized for pH adjustment and neutralization in municipal and industrial wastewater treatment processes. According to the European Environment Agency, strict regulations on water quality necessitate advanced treatment technologies to rerelocate contaminants and ensure safe discharge. The Urban Wastewater Treatment Directive mandates high standards for sewage treatment, leading to increased consumption of chemicals like caustic soda. Chlorine derivatives such as sodium hypochlorite are vital for disinfection purposes in drinking water supplies and swimming pools. As per the World Health Organization guidelines adopted by European health authorities, chlorination remains the most effective method for preventing waterborne diseases. The heightened awareness of hygiene following recent global health crises has further amplified demand for disinfectants and cleaning agents containing chlor alkali derivatives. The pharmaceutical indusattempt also relies on high purity caustic soda for various synthesis processes. The food and beverage sector utilizes these chemicals for cleaning and sanitizing equipment to meet safety standards. The growing population and urbanization in Europe increase the volume of wastewater requiring treatment. Government investments in upgrading water infrastructure support sustained demand. The non-discretionary nature of water treatment ensures resilience against economic fluctuations. This essential service aspect provides a stable and growing market for chlor alkali products.

MARKET RESTRAINTS

High Energy Intensity and Volatile Electricity Costs

The Europe chlor alkali market faces a major restraint due to its high energy intensity and exposure to volatile electricity prices. The electrolysis process required to split brine into chlorine and caustic soda consumes substantial amounts of electrical power. According to the International Energy Agency, the chemical indusattempt is one of the largest industrial consumers of electricity in Europe. Recent geopolitical tensions and supply disruptions have led to significant spikes in energy costs affecting the competitiveness of European producers. As per the European Chemical Indusattempt Council, energy costs constitute a large portion of production expenses for chlor alkali manufacturers, creating them vulnerable to market fluctuations. High electricity prices erode profit margins and can force temporary plant closures or production cuts. This volatility builds it difficult for producers to offer stable pricing to customers, leading to uncertainty in supply chains. Compared to regions with cheaper energy resources such as North America or the Middle East, European producers face a structural disadvantage. The transition to renewable energy sources, while environmentally necessary, involves high upfront investment and potential intermittency issues. Manufacturers must invest in energy efficiency measures and power purchase agreements to mitigate risks, but these strategies require capital. The burden of high energy costs limits the ability of companies to expand capacity or invest in innovation. It also encourages the relocation of energy intensive processes to lower cost regions. This economic pressure acts as a persistent brake on market growth and profitability.

Stringent Environmental Regulations and Compliance Burdens

Stringent environmental regulations and the associated compliance burdens pose a significant restraint to the Europe chlor alkali market. The production process involves hazardous materials and generates byproducts that are strictly regulated under European law. According to the European Environment Agency, the Industrial Emissions Directive imposes strict limits on pollutants released from chemical installations including chlor alkali plants. Compliance with these standards requires significant investment in advanced emission control technologies and monitoring systems. As per the European Commission, the REACH regulation restricts the utilize of certain substances and requires extensive documentation for chemical safety assessments. The phase out of mercury cell technology, although largely complete, has left a legacy of environmental remediation costs for some operators. New regulations aimed at reducing carbon emissions further complicate operations by imposing additional reporting and reduction tarobtains. The Best Available Techniques reference documents for chlor alkali production are regularly updated, requiring continuous adaptation. Small and medium sized enterprises may struggle to meet these financial and regulatory demands, leading to market consolidation. The administrative burden of compliance diverts resources from potential growth initiatives. Any failure to comply can result in heavy fines and operational shutdowns. The constant evolution of environmental laws creates an uncertain operating environment. This regulatory intensity increases the overall cost structure of production. It acts as a barrier to enattempt for new players and limits the flexibility of existing manufacturers.

MARKET OPPORTUNITIES

Integration with Renewable Hydrogen Production

The integration of chlor alkali production with renewable hydrogen generation is a significant opportunity for the Europe chlor alkali market. The electrolysis process naturally produces hydrogen as a byproduct which can be captured and purified for utilize as a clean energy carrier. According to the European Clean Hydrogen Partnership, hydrogen is considered a key vector for decarbonizing hard to abate sectors including heavy indusattempt and transport. Chlor alkali plants are well positioned to become suppliers of low carbon hydrogen due to their existing electrolysis infrastructure. As per the Joint Research Centre of the European Commission, the potential for coupling chlor alkali production with hydrogen networks is substantial. Producers can invest in purification and compression technologies to sell hydrogen to nearby industries or inject it into gas grids. This diversification creates a new revenue stream and enhances the economic viability of chlor alkali plants. The European Union hydrogen strategy aims to install electrolyzer capacity by 2030, providing a favorable policy environment. Partnerships with energy companies and logistics providers can facilitate the distribution of hydrogen. The utilize of renewable electricity for chlor alkali production further reduces the carbon footprint of the resulting hydrogen. This alignment with green energy goals attracts investment and support from government bodies. The development of hydrogen valleys and clusters offers opportunities for collaboration. By leveraging their hydrogen byproduct, chlor alkali producers can play a crucial role in the energy transition. This strategic shift transforms a waste product into a valuable commodity.

Expansion in Pharmaceutical and Specialty Chemical Synthesis

The expanding pharmaceutical and specialty chemical sectors offer a promising opportunity for the Europe chlor alkali market through increased demand for high purity caustic soda and chlorine derivatives. Caustic soda is a critical reagent in the synthesis of active pharmaceutical ingredients and intermediates. According to the European Federation of Pharmaceutical Industries and Associations, the pharmaceutical indusattempt is a key driver of innovation and economic growth in Europe. The aging population and increasing healthcare spfinishing drive demand for medicines requiring complex chemical synthesis. As per indusattempt analysis from specialized chemical consultancies, the trfinish towards personalized medicine and biologics requires precise and high quality chemical inputs. Chlorine derivatives are utilized in the production of solvents, epichlorohydrin, and other intermediates essential for drug manufacturing. The specialty chemicals sector also utilizes chlor alkali products in the production of agrochemicals, dyes, and adhesives. The shift towards sustainable chemisattempt encourages the utilize of efficient and clean reagents. Producers can differentiate themselves by offering high purity grades tailored to specific pharmaceutical applications. Investment in quality assurance and certification enhances trust with sensitive finish utilizers. The resilience of the healthcare sector provides stable demand regardless of economic cycles. Collaborations with research institutions can lead to new applications for chlor alkali derivatives. This segment offers higher margins compared to commodity applications. The focus on innovation and quality supports long term growth.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Availability

The Europe chlor alkali market faces substantial challenges from supply chain disruptions and the availability of raw materials particularly salt and energy. While salt is abundant, the logistics of transporting bulk brine or solid salt can be affected by infrastructure constraints and labor issues. According to the European Logistics Association, transport bottlenecks and port congestion have impacted the timely delivery of industrial goods. Geopolitical tensions can also affect the supply of energy and other critical inputs. As per the International Energy Agency, energy security remains a top concern for European industries relying on imported fuels. The depfinishence on specific suppliers for membrane cells and other specialized equipment adds another layer of vulnerability. Any disruption in the supply of these components can delay maintenance and expansion projects. The just in time inventory models adopted by many manufacturers leave little room for error. Currency fluctuations impact the cost of imported raw materials and equipment, adding financial uncertainty. The complexity of global supply chains builds them susceptible to shocks from natural disasters or political instability. Ensuring supply security requires diversifying sources and holding larger inventories which increases costs. The lack of local alternatives for certain specialized inputs limits flexibility. Manufacturers must invest in robust risk management strategies to mitigate these risks. However, these measures require significant resources and planning. The unpredictability of supply chains poses a continuous threat to operational stability.

Competition from Alternative Materials and Technologies

The Europe chlor alkali market faces intense competition from alternative materials and technologies that threaten to reduce demand for chlorine and caustic soda. In the plastics sector, bio based polymers and recycled materials are gaining traction as sustainable alternatives to PVC. According to Plastics Europe, recycling rates for plastics are increasing, driven by regulatory tarobtains and consumer preference. The development of non chlorinated polymers for construction and packaging applications reduces the necessary for chlorine. In water treatment, alternative disinfection methods such as ultraviolet light and ozone are being adopted to avoid the formation of harmful byproducts. As per the European Water Association, these technologies are becoming more cost effective and efficient. The pharmaceutical indusattempt is exploring greener synthesis routes that minimize the utilize of hazardous chemicals. The shift towards digitalization and automation in manufacturing also drives demand for different types of chemicals. The emergence of new materials with superior properties challenges the dominance of traditional chlor alkali derivatives. Manufacturers must continuously innovate to maintain relevance and competitiveness. The pace of technological alter requires significant investment in research and development. Failure to adapt could result in loss of market share. The competitive landscape is dynamic and requires strategic agility. Companies must monitor trfinishs and adjust their product portfolios accordingly. This pressure to innovate adds to the operational complexity.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

6.27% |

|

Segments Covered |

By Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

INEOS Group, Solvay SA, Akzo Nobel N.V., Olin Corporation, Kemira, Occidental Petroleum Corporation, Tata Chemicals Limited, Formosa Plastics Corporation, Tosoh Corporation, Covestro, Vynova Group, and Nobian |

SEGMENTAL ANALYSIS

By Application Insights

The vinyls segment dominated the market by holding 36.3% of the European market share in 2025. The growth of the vinyls segment in the European market is attributed to the extensive utilize of PVC in the construction indusattempt for pipes, window profiles, flooring, and cable insulation. As per Plastics Europe, the construction sector is a major consumer of PVC in Europe, highlighting its critical role in infrastructure development. The European Commission’s Renovation Wave strategy aims to increase annual energy renovation rates of buildings by 2030 which directly boosts the demand for PVC based insulation and resolvetures due to their thermal efficiency and durability. As per the European Construction Indusattempt Federation, significant investments are created annually in building refurbishment projects across the EU creating a sustained necessary for construction materials. PVC is favored for its longevity, resistance to corrosion, and low maintenance requirements creating it ideal for both new builds and renovations. The material’s recyclability also aligns with circular economy goals further supporting its adoption. Major chemical producers in Europe have integrated PVC production with chlor alkali plants ensuring a stable supply chain. The automotive indusattempt also contributes to demand through the utilize of PVC in interior components and underbody coatings. The established infrastructure for PVC manufacturing and recycling in Europe reinforces its market leadership. This structural depfinishence on PVC for essential construction and industrial applications ensures that the vinyls segment remains the primary driver of chlorine demand in the region.

However, the water treatment segment is projected to witness a promising CAGR of 5.1% over the forecast period in the European market owing to the stringent environmental regulations and increasing investments in municipal and industrial wastewater infrastructure. Chlorine and caustic soda are indispensable for disinfection, pH adjustment, and neutralization processes in water treatment facilities. According to the European Environment Agency, the Urban Wastewater Treatment Directive requires member states to ensure that all agglomerations above a certain population size have adequate collection and treatment systems. As per the World Health Organization guidelines adopted by European health authorities, chlorination remains the most reliable method for preventing waterborne diseases in drinking water supplies. The growing awareness of water scarcity and quality issues has prompted governments to invest in advanced treatment technologies. The industrial sector also contributes to growth as manufacturers strive to meet stricter discharge limits. The pharmaceutical and food and beverage industries require high purity water necessitating rigorous treatment protocols. Population growth and urbanization increase the volume of wastewater requiring processing. Government initiatives to improve public health and environmental protection support steady demand. The non-discretionary nature of water treatment ensures resilience against economic fluctuations. This segment benefits from long term infrastructure projects and regulatory compliance requirements driving consistent growth.

REGIONAL ANALYSIS

Germany Chlor Alkali Market Analysis

Germany held the leading position in the Europe chlor alkali market by capturing 26.1% of the European market share in 2025. The counattempt’s robust chemical indusattempt particularly its large scale production of polyvinyl chloride and specialty chemicals drives substantial demand for chlorine and caustic soda. According to the German Chemical Indusattempt Association, the chemical sector is one of the largest industries in the counattempt contributing significantly to national exports and employment. Germany is home to major chlor alkali producers who operate integrated facilities ensuring efficient supply to downstream industries. The construction sector’s demand for PVC pipes and profiles supports chlorine consumption. As per the Federal Statistical Office of Germany, industrial production levels remain steady in basic chemicals. The pharmaceutical and water treatment sectors also contribute to demand for high purity caustic soda and chlorine derivatives. Germany’s commitment to environmental sustainability has led to investments in advanced emission control technologies ensuring compliant production. The counattempt’s strategic location and well developed logistics infrastructure facilitate efficient distribution across Europe. Additionally, the push towards renewable energy integration in chemical production enhances competitiveness. The strong research and development ecosystem supports innovation in process efficiency. These factors collectively sustain Germany’s dominance in the regional market. The market status is characterized by high technological standards and strict regulatory compliance.

France Chlor Alkali Market Analysis

France had the second largegest share of the European chlor alkali market in 2025. The counattempt’s diverse industrial base including chemicals, pharmaceuticals, and water treatment drives demand for chlor alkali products. According to the French Minisattempt of Economy, the chemical indusattempt is a strategic sector with significant investment in sustainable production methods. France has a well developed water infrastructure network requiring consistent supplies of chlorine and caustic soda for disinfection and pH control. As per the French Water Agencies, wastewater treatment requires substantial chemical inputs. The pulp and paper indusattempt although compacter than in Nordic countries still contributes to demand for bleaching agents. The pharmaceutical sector in France is a major consumer of high purity caustic soda for synthesis processes. The government’s focus on environmental protection and public health ensures steady demand for water treatment chemicals. France’s energy mix which includes a significant share of nuclear power provides relatively stable electricity costs for energy intensive chlor alkali production. The presence of major chemical companies facilitates local production and supply security. The market status is defined by strong regulatory frameworks and a focus on sustainability. Investment in modernizing production facilities supports continued growth.

Italy Chlor Alkali Market Analysis

Italy is estimated to account for a promising share of the European chlor alkali market during the forecast period. The counattempt’s chemical and construction industries are the primary drivers of demand for chlorine and caustic soda. According to the Italian National Institute of Statistics, the manufacturing sector remains a cornerstone of the Italian economy with significant output in chemicals and plastics. The construction indusattempt’s reliance on PVC for pipes and fittings supports chlorine consumption. As per the Italian Chemical Indusattempt Federation, the sector is characterized by specialization and innovation catering to global markets. The water treatment sector in Italy faces challenges related to infrastructure modernization driving investment in treatment facilities and chemical usage. The textile and soap and detergent industries utilize caustic soda in various processing steps. Italy’s strategic Mediterranean location facilitates trade and access to raw materials. The counattempt’s focus on environmental compliance has led to upgrades in production technologies. The presence of integrated chemical parks enhances supply chain efficiency. The market status is characterized by a mix of domestic production and imports. Regulatory pressures drive the adoption of cleaner technologies. Investment in sustainable practices supports long term viability. The diversity of finish utilize applications provides stability to demand.

Netherlands Chlor Alkali Market Analysis

The Netherlands is predicted to displaycase a healthy CAGR in the European chlor alkali market over the forecast period. The counattempt’s position as a major chemical hub in Europe drives significant demand for chlor alkali products. According to the Netherlands Chemical Indusattempt Association, the sector is a key contributor to the national economy with strong export orientation. The Port of Rotterdam serves as a critical logistics node for the import and export of chemicals facilitating efficient supply chains. The Netherlands hosts several large scale chlor alkali production facilities that serve both domestic and international markets. As per Statistics Netherlands, industrial production in the chemical sector remains robust. The water management sector in the Netherlands is highly advanced requiring substantial amounts of chemicals for treatment and purification. The agricultural sector also contributes to demand through the utilize of chlorinated intermediates in agrochemicals. The counattempt’s commitment to sustainability drives innovation in green chemisattempt and circular economy practices. The integration of renewable energy sources in chemical production enhances competitiveness. The market status is defined by high efficiency and logistical advantages. Strategic partnerships with international players strengthen market position. Investment in digitalization and automation improves operational performance.

Spain Chlor Alkali Market Analysis

Spain is estimated to hold a notable share of the European chlor alkali market during the forecast period. The counattempt’s growing chemical and water treatment sectors drive demand for chlor alkali products. According to the Spanish Chemical Indusattempt Federation, the sector is experiencing growth driven by domestic demand and exports to Latin America and North Africa. The construction indusattempt’s recovery has boosted demand for PVC materials. As per the Spanish Minisattempt for Ecological Transition, investments in water infrastructure address scarcity and quality issues, driving consumption of chlorine and caustic soda for treatment processes. The pulp and paper indusattempt in Spain also utilizes chlor alkali products for bleaching and processing. The tourism sector’s demand for clean water in hotels and resorts supports municipal treatment activities. Spain’s strategic location facilitates trade with neighboring regions. The counattempt’s focus on renewable energy offers opportunities for integrating green hydrogen production with chlor alkali operations. The market status is characterized by emerging growth potential and infrastructure development. Regulatory improvements enhance environmental standards. Investment in modern production technologies supports competitiveness. The diversification of finish utilize applications reduces depfinishency on single sectors.

COMPETITIVE LANDSCAPE

The Europe chlor alkali market exhibits a moderately consolidated competitive landscape characterized by the presence of established chemical giants and specialized regional producers. Competition is primarily driven by cost efficiency product quality and adherence to stringent environmental regulations rather than price alone. Major players leverage their integrated production facilities and access to renewable energy to achieve cost advantages. The market sees intense rivalry in meeting sustainability standards with companies investing significantly in low carbon production technologies and circular economy initiatives. New entrants face high barriers due to capital intensive requirements and complex regulatory compliance necessarys. Strategic collaborations and long term supply agreements are common tactics to secure market share in key sectors like construction and water treatment. The shift towards green chemisattempt has intensified competition in innovation segments. Companies differentiate themselves through technological advancements and customized solutions for specific industrial applications. This dynamic environment fosters continuous improvement and innovation among participants striving to maintain competitive edges in a mature yet evolving market structure influenced by energy prices and policy alters.

KEY MARKET PLAYERS

Some of the notable key players in the Europe chlor alkali market are

- INEOS Group

- Solvay SA

- Akzo Nobel N.V.

- Olin Corporation

- Kemira

- Occidental Petroleum Corporation

- Tata Chemicals Limited

- Formosa Plastics Corporation

- Tosoh Corporation

- Covestro

- Vynova Group

- Nobian

Top Players in the Market

- INEOS is a leading global manufacturer of chemicals with a significant presence in the Europe chlor alkali market. The company operates multiple integrated production sites across the continent supplying chlorine and caustic soda to various industries. INEOS recently focutilized on enhancing operational efficiency and sustainability by investing in energy saving technologies. The company actively participates in initiatives to reduce carbon emissions and promote circular economy principles. Recent actions include upgrading membrane cell technology to improve productivity and lower environmental impact. These efforts strengthen its position as a reliable supplier in the European market. INEOS continues to expand its product portfolio offering high purity grades for specialized applications. Its commitment to safety and innovation drives long term growth. The company leverages its extensive logistics network to ensure consistent supply to customers. Strategic partnerships with downstream industries further solidify its market presence.

- Kemira is a global chemical company specializing in water intensive industries with strong operations in the Europe chlor alkali sector. The company provides essential chemicals including caustic soda for water treatment pulp and paper and mining applications. Kemira recently accelerated its sustainability strategy by developing bio based and low carbon solutions. The company invests heavily in research and development to create innovative products that meet strict environmental standards. Recent actions include expanding production capacity for high purity caustic soda in key European facilities. These initiatives enhance its competitiveness and customer value proposition. Kemira collaborates closely with industrial partners to optimize water usage and reduce waste. Its focus on digital services and data analytics improves operational efficiency for clients. The company’s commitment to sustainable chemisattempt positions it as a leader in the transition to a green economy. Kemira continues to strengthen its market position through strategic acquisitions and organic growth.

- Covestro is a major supplier of high quality polymer materials and intermediates with significant involvement in the Europe chlor alkali value chain. The company utilizes chlorine and caustic soda in the production of polycarbonates polyurethanes and other specialty chemicals. Covestro recently focutilized on achieving climate neutrality by transitioning to renewable energy sources and circular raw materials. The company invests in innovative technologies to reduce the carbon footprint of its production processes. Recent actions include launching new product lines based on recycled and bio based feedstocks. These efforts align with European sustainability goals and enhance brand reputation. Covestro collaborates with suppliers and customers to develop closed loop systems. Its emphasis on innovation and sustainability drives competitive advantage. The company continues to optimize its manufacturing footprint to improve efficiency. Strategic investments in digitalization support agile and responsive operations. Covestro’s integrated approach strengthens its position in the European chemical landscape.

Top Strategies Used by the Key Market Participants

Key players in the Europe chlor alkali market predominantly focus on vertical integration to secure raw material supplies and optimize production costs. Companies invest heavily in technological upgrades to enhance energy efficiency and reduce environmental emissions complying with strict regulatory frameworks. Strategic partnerships with downstream industries such as construction and water treatment ensure stable demand and long term contracts. Participants also prioritize sustainability initiatives by adopting circular economy principles and developing green production methods. Expansion into niche applications like renewable hydrogen production offers new growth avenues. Continuous research and development efforts aim to improve product purity and process safety. Manufacturers leverage digital technologies for predictive maintenance and operational optimization. These strategies collectively strengthen market positions by improving competitiveness ensuring regulatory compliance and meeting evolving customer necessarys in a dynamic industrial landscape.

MARKET SEGMENTATION

This research report on the European chlor alkali market has been segmented and sub-segmented based on categories.

By Application

- Chlorine

- Vinyl

- Organics

- Intermediates

- Inorganics

- Paper & pulp

- Water treatment

- Others

- Caustic Soda

- Pulp & paper

- Alumina

- Organics

- Soap & detergents

- Textile

- Inorganics

- Water treatment

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply