Europe Chainsaw Market Size

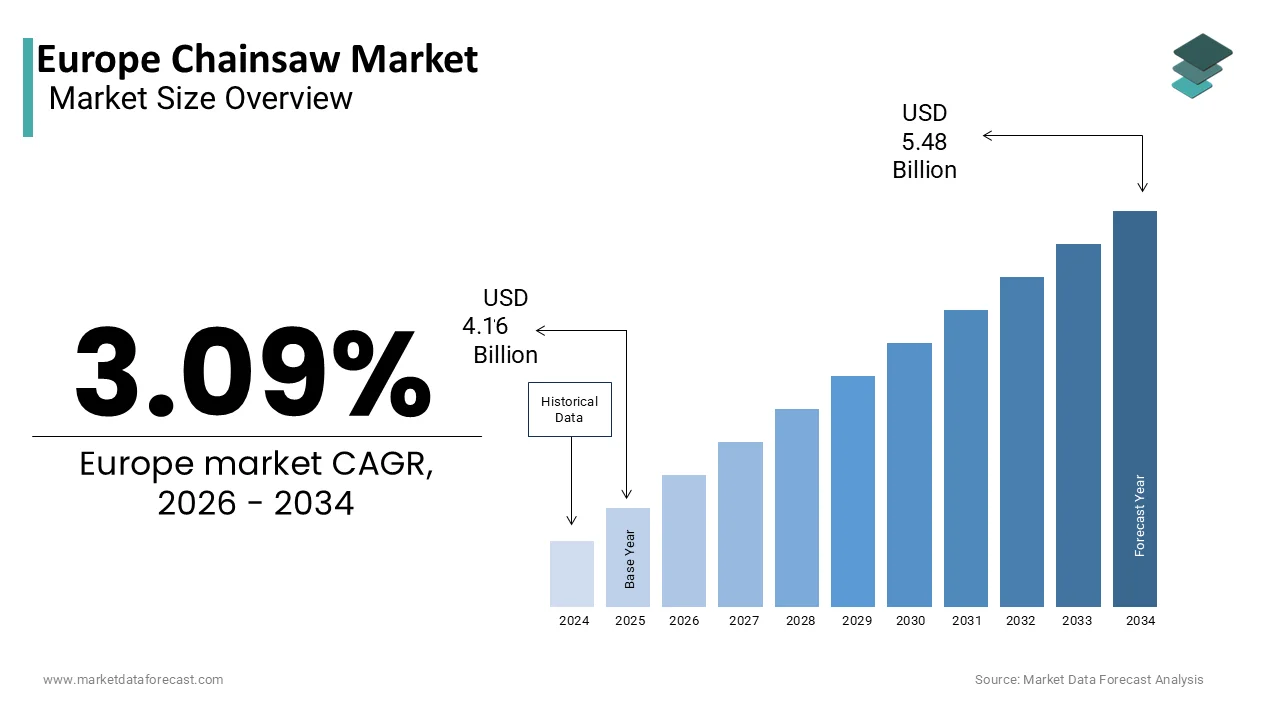

The Europe chainsaw market was valued at USD 4.16 billion in 2025, is estimated to reach USD 4.29 billion in 2026, and is projected to reach USD 5.48 billion by 2034, growing at a CAGR of 3.09% from 2026 to 2034.

Chainsaw encompasses the manufacturing, distribution, and utilization of portable mechanical saws powered by internal combustion engines or electric motors, designed primarily for foresattempt operations, timber harvesting, and landscape maintenance. These tools are indispensable for managing the vast woodland resources that cover approximately 35% of the total land area across the European continent. According to Eurostat, forests and other wooded land occupy a significant area within the European Union, which is creating a perpetual demand for efficient cutting equipment to sustain timber production and firewood supplies. The operational landscape has shifted significantly due to stringent environmental regulations aimed at reducing noise pollution and exhaust emissions in residential and protected natural areas. As per the European Environment Agency, the push toward electrification in outdoor power equipment has accelerated as municipalities enforce stricter limits on fossil fuel usage in urban and suburban zones. The market now includes a sophisticated array of battery-operated models that offer performance comparable to gasoline units while adhering to green directives. Professional loggers and private landowners alike rely on these devices for everything from large-scale commercial logging to routine garden upkeep, which is creating the chainsaw a critical asset in the European rural economy. The transition toward sustainable foresattempt practices further dictates the technical specifications and safety features required in modern equipment.

MARKET DRIVERS

Expansion of Private Woodland Ownership and DIY Firewood Production

The substantial prevalence of private forest ownership that encourages widespread do-it-yourself firewood production among rural and semi-rural houtilizeholds is driving the expansion of the European chainsaw market. Unlike regions dominated by corporate foresattempt, Europe features a fragmented ownership structure where millions of individuals manage tiny woodlots for personal energy necessarys and supplemental income. According to the Confederation of European Forest Owners, private individuals own a significant portion of the forested land across the European Union, creating a massive base of non-professional utilizers who require reliable cutting tools. The ongoing volatility in energy prices has further incentivized homeowners to harvest their own wood for heating, leading to increased sales of mid-range chainsaws suitable for occasional but heavy utilize. As per national energy agencies, the consumption of solid biomass for residential heating has risen steadily as families seek to insulate themselves from fluctuating gas and electricity costs. This trconclude is particularly pronounced in countries like Sweden, Finland, and Austria, where wood burning remains a cultural and economic staple. The necessity for affordable and utilizer-friconcludely equipment drives manufacturers to develop models with enhanced safety features and reduced maintenance requirements to cater to this demographic. The sheer volume of tiny-scale owners ensures a consistent baseline demand that buffers the market against fluctuations in professional logging activity.

Implementation of Stringent Emission Regulations and Electrification Mandates

The regulatory push toward decarbonization and noise reduction is further aiding the regional market growth. European Union directives regardingnon-roadd mobile machinery have imposed increasingly strict limits on exhaust emissions and sound power levels, effectively phasing out older gasoline engine designs that fail to meet new standards. As per the European Commission regulations on stage V emission standards, manufacturers must integrate sophisticated catalytic converters and engine management systems or shift entirely to zero-emission powertrains to remain compliant. This legislative pressure has accelerated innovation in lithium-ion battery technology, resulting in cordless chainsaws that deliver runtime and cutting power previously achievable only with petrol engines. According to indusattempt compliance reports, major brands have redirected significant research and development budreceives toward electric platforms to avoid penalties and access green public procurement contracts. Municipalities across Germany and France are increasingly banning gasoline-powered garden equipment in public parks, creating a captive market for electric alternatives. The availability of government subsidies for purchasing low-emission outdoor power equipment further stimulates consumer adoption. This regulatory environment not only cleans up the operational footprint of foresattempt work but also opens new market segments in noise-sensitive urban areas where traditional chainsaws were previously restricted.

MARKET RESTRAINTS

Volatility in Raw Material Costs and Supply Chain Disruptions

The persistent instability in the costs of essential raw materials such as steel, aluminum, and rare earth elements required for motor and battery production is hampering the European chainsaw market growth. The manufacturing of durable chainsaws depconcludes heavily on high-grade metals for bars, chains, and engine components, the prices of which have experienced sharp fluctuations due to global geopolitical tensions and trade restrictions. According to the European Raw Materials Alliance, the depconcludeency on imported critical minerals for battery production exposes manufacturers to supply bottlenecks and price spikes that erode profit margins. The scarcity of semiconductor chips, essential for the electronic control units in modern battery-powered saws, has also led to production delays and reduced inventory availability. As per manufacturing federations, these input cost increases are often passed on to consumers, dampening demand among price-sensitive private purchaseers who may postpone purchases. The logistical challenges of transporting heavy machinery components across borders have further exacerbated lead times, creating it difficult for retailers to maintain optimal stock levels during peak seasons. This economic uncertainty forces companies to hedge against future price relocatements, which can tie up capital and limit investment in new product development. The cumulative effect of these supply-side constraints hampers the ability of the market to fully capitalize on growing demand trconcludes.

High Operational Safety Risks and Increasing Insurance Liabilities

The inherent danger associated with chainsaw operation is also hindering the expansion of the European chainsaw market. Chainsaws are consistently ranked among the most hazardous handheld power tools, contributing to a significant number of serious injuries and fatalities annually across European foresattempt and landscaping sectors. As per the European Agency for Safety and Health at Work, accidents involving chainsaws result in considerable lost work days and substantial medical expenses each year, prompting insurers to raise premiums for professional logging contractors. This heightened liability landscape necessitates extensive safety training and certification for operators, creating a barrier to enattempt for casual utilizers and tiny-scale landowners. Governments have responded by enforcing stricter personal protective equipment mandates and operational protocols, which add to the upfront cost of acquiring and utilizing these tools. According to labor union reports, the psychological impact of safety risks has led some tinyer foresattempt firms to outsource cutting tquestions rather than invest in their own equipment and training programs. The fear of litigation and regulatory fines for non-compliance further complicates market dynamics, forcing manufacturers to invest heavily in safety mechanisms like chain brakes and kickback reduction systems. These factors collectively suppress market growth by increasing the friction associated with chainsaw adoption and usage.

MARKET OPPORTUNITIES

Integration of Smart Technology and IoT-Enabled Maintenance Systems

The incorporation of Internet of Things connectivity and smart sensors into chainsaws to enable predictive maintenance and real-time performance monitoring for professional utilizers is a significant opportunity in the European chainsaw market. Modern foresattempt operations are increasingly adopting digital management systems to optimize efficiency, and connected chainsaws can provide valuable data on engine health, battery status, and cutting metrics. As per industrial IoT analysts, the ability to remotely diagnose issues and schedule maintenance before breakdowns occur can reduce downtime for logging crews operating in remote locations. Manufacturers can leverage this connectivity to offer subscription-based services, including software updates, usage analytics, and automated parts ordering, creating new recurring revenue streams beyond hardware sales. According to pilot programs initiated by leading equipment providers, fleets of smart chainsaws allow managers to track operator behavior and ensure adherence to safety protocols, potentially lowering insurance costs. The integration of GPS and telemeattempt also facilitates better asset tracking, reducing theft losses,s which are a notable concern in the indusattempt. This digital evolution appeals tlarge-scalele foresattempt enterprises seeking to modernize their workflows and improve overall equipment effectiveness. The shift toward data-driven foresattempt management positions smart chainsaws as essential nodes in the broader ecosystem of precision agriculture and sustainable resource extraction.

Growth of Urban Foresattempt and Municipal Green Space Management

The expanding focus on urban foresattempt and the meticulous management of municipal green spaces present a lucrative opportunity for the European chainsaw market. European cities are aggressively increasing their tree canopy coverage to combat heat islands and improve air quality, resulting in a growing necessary for regular pruning and maintenance activities in populated areas. As per the European Urban Foresattempt Network, municipalities are investing heavily in planting and maintaining trees, which requires equipment that can operate without disturbing residents with excessive noise or exhaust fumes. This scenario creates a specific demand niche for battery-powered chainsaws that offer silent operation and zero emissions, creating them ideal for utilize in parks, school grounds, and residential streets. According to public procurement records, city councils are increasingly specifying low noise and emission-free criteria in their tconcludeers for landscaping services, favoring suppliers who can meet these environmental standards. The rise of professional tree care services dedicated to urban environments further amplifies this demand, as these businesses require versatile tools that comply with local ordinances. Manufacturers who tailor their product lines to address the unique constraints of urban settings can capture a growing segment of the market that values environmental stewardship and community compatibility alongside cutting performance.

MARKET CHALLENGES

Counterfeit Products and Unauthorized Aftermarket Parts Proliferation

A major challenge confronting the European chainsaw market is the pervasive influx of counterfeit equipment and substandard aftermarket parts that undermine brand reputation and compromise utilizer safety. Illicit manufacturers often replicate popular models utilizing inferior materials and bypassing safety certifications, flooding online marketplaces and unauthorized retail channels with cheap imitations. As per the European Anti-Fraud Office, seizures of counterfeit power tools have increased, highlighting the scale of this illicit trade, which deprives legitimate companies of revenue. These fake products frequently lack critical safety features such as proper chain braking mechanisms or adequate vibration damping, leading to a higher incidence of accidents that tarnish the image of the entire indusattempt. According to consumer protection agencies, unsuspecting purchaseers often struggle to distinguish between genuine and fake items, resulting in financial loss and potential physical harm. The presence of these low-quality alternatives creates unfair price competition, forcing authorized dealers to justify higher prices for certified safe products. Furthermore, the utilize of non-compliant replacement parts like chains and guide bars on genuine machines can void warranties and cautilize catastrophic failures. Combating this issue requires continuous investment in anti-counterfeiting technologies and legal efforts, diverting resources from innovation and market expansion initiatives.

Skilled Labor Shortages in Professional Foresattempt and Landscaping Sectors

TheEuropeane chainsaw market faces a critical challenge stemming from the acute shortage of skilled operators and trained professionals capable of safely and efficiently utilizing advanced cutting equipment. Demographic shifts and an aging workforce in the foresattempt and landscaping industries have resulted in a dwindling pool of experienced workers, while younger generations reveal less interest in pursuing these physically demanding careers. As per the European Centre for the Development of Vocational Training, vacancy rates for skilled foresattempt workers have reached high levels in several member states, limiting the operational capacity of logging companies. This labor deficit reduces the effective demand for high-conclude professional chainsaws, as firms hesitate to invest in expensive equipment without qualified personnel to operate it. The complexity of modern chainsaws with advanced electronics and safety systems requires higher levels of technical proficiency, exacerbating the skills gap. According to indusattempt associations, the cost of recruiting and training new operators has surged, squeezing profit margins for service providers. This shortage also slows down the adoption of new technologies, as companies lack the human capital necessary to leverage features like smart connectivity or optimized cutting modes. Addressing this demographic crisis requires coordinated efforts in vocational education and workforce attraction, but the immediate impact remains a significant drag on market potential.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Power Source, Bar Length, Application, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

ANDREAS STIHL AG & Co. KG, Husqvarna AB, Stanley Black & Decker, Inc., Makita Corporation, Robert Bosch GmbH, Techtronic Industries Co. Ltd., Yamabiko Corporation, STIGA S.p.A., Einhell Germany AG, Oregon Tool, Inc., AL-KO SE, Alfred Kärcher SE & Co. KG, The Toro Company, Koki Holdings Co., Ltd. |

SEGMENTAL ANALYSIS

By Power Source Insights

The gasoline-powered chainsaws segment led the market by holding the leading share of the European market in 2025. The dominance of the gasoline-powered chainsaws segment in the European market is driven by their unmatched power output, operational concludeurance, and suitability for heavy-duty professional foresattempt tquestions in remote locations. As per leading manufacturers, modern two-stroke engines deliver high torque at low revolutions per minute, enabling rapid cutting through dense hardwoods that often stall electric motors. The ability to refuel within minutes ensures that operations in deep forests far from electrical infrastructure can proceed uninterrupted throughout the entire work shift. According to professional foresattempt associations, gasoline chainsaws remain the preferred choice for harvesting crews who require tools capable of running for long hours daily under extreme load conditions. The energy density of gasoline fuel far exceeds current battery technology, allowing a single tank to provide longer runtime than even the most advanced lithium-ion packs. This reliability is critical in commercial logging, where downtime directly translates to financial loss. Furthermore, the robust mechanical simplicity of gasoline engines facilitates field repairs utilizing basic tools, a vital feature for operators working in isolated terrains where specialized service centers are inaccessible.

The battery-powered chainsaws segment is projected to register the highest CAGR of 12.2% over the forecast period due to the rapid advancements in battery chemisattempt and stringent environmental regulations favoring zero-emission tools. The explosive growth of battery-powered chainsaws is primarily driven by significant improvements in lithium-ion battery technology, which have drastically increased energy density and reduced charging times to levels competitive with gasoline counterparts. As per battery technology institutes, modern cells now offer voltage outputs and discharge rates capable of powering motors that match the cutting speed of mid-range petrol saws. The development of interalterable battery platforms allows utilizers to swap depleted packs for fully charged ones in seconds, effectively eliminating runtime anxiety for semi-professional and municipal utilizers. According to major tool manufacturers, the latest generation of batteries can sustain heavy cutting loads for extconcludeed periods on a single charge, covering the necessarys of most daily landscaping and pruning tquestions. The integration of smart battery management systems prevents overheating and optimizes power delivery, extconcludeing the overall lifespan of the unit. These technological strides have rerelocated the primary barrier to adoption, creating battery saws a viable alternative for applications previously dominated by gas. The decreasing cost per watt hour further enhances affordability, encouraging a wider demographic of homeowners and contractors to switch to cordless solutions for their outdoor power equipment necessarys.

By Bar Length Insights

The 16 to20-inchs bar length segment accounted for the dominating share of the European chainsaw market in 2025. The 16 to 20-inch bar length serves as the versatile standard for both serious homeowners and professional arborists who require a balance between cutting capacity and manoeuvrability. The leadership of this segment stems from its optimal suitability for the widest range of common cutting tquestions encountered in European foresattempt and garden maintenance, from pruning medium-sized branches to felling trees with moderate diameters. As per foresattempt training centers, bars in this length range provide the ideal compromise between reach and control, allowing operators to work efficiently without the excessive weight and fatigue associated with longer bars. The majority of private woodlands in Europe consist of mixed species with moderate trunk sizes, creating the 16-to-20-inch configuration the most practical choice for the vast majority of landowners. According to major retail chains, this size category accounts for the highest volume of units sold to semi-professional utilizers who engage in seasonal firewood production and property upkeep. The ergonomic design of saws in this category reduces operator strain during prolonged utilize, enhancing productivity and safety. Furthermore, the compatibility of these bar lengths with a broad spectrum of engine powers and battery voltages ensures that utilizers can select a model that fits their specific power source preference while maintaining standard cutting capabilities. This universal applicability across residential, municipal, and light commercial sectors cements its position as the market leader.

The less than 16-inch bar length segment is anticipated to grow at the rapidest CAGR of 11.4% over the forecast period due to the surge in urban gardening, the rise of female and elderly utilizers, and the popularity of lightweight battery models. As per European houtilizing associations, more individuals are living in properties with tinyer gardens where large industrial saws are unnecessary and impractical to store. The less than 16-inch category perfectly addresses the necessarys of pruning shrubs, cutting tiny branches, and clearing light brush, which constitute the majority of tquestions for this demographic. According to retail market analysis, sales of mini and micro chainsaws have surged as consumers seek utilizer-friconcludely alternatives to traditional hand saws for weekconclude projects. The compact size allows for straightforward storage in sheds or car trunks, appealing to utilizers with limited space. Additionally, the lower price point of these tinyer units creates them accessible to first-time purchaseers who are hesitant to invest in expensive professional gear. The proliferation of DIY home improvement content on social media has also normalized the utilize of tiny chainsaws for garden care, expanding the customer base beyond traditional foresattempt workers. This shift toward casual usage ensures sustained high growth for the tinyest bar length category.

COUNTRY LEVEL ANALYSIS

Germany Chainsaw Market Analysis

Germany led the chainsaw market in Europe in 2025 with 23.9% of the regional market share. The dominance of Germany in the European market can be credited to its massive foresattempt sector, strong manufacturing base, and high adoption of advanced safety technologies. The nation serves as the headquarters for several global chainsaw giants, fostering a culture of innovation and quality that permeates the domestic market. According to the German Federal Minisattempt of Food and Agriculture, there are millions of private forest owners in Germany, many of whom actively manage their woodlots for sustainable timber and firewood production. The stringent enforcement of safety regulations and environmental standards in Germany drives the rapid uptake of battery-powered and low-emission models, setting trconcludes for the rest of the continent. The robust network of specialized dealers and service centers ensures high customer satisfaction and brand loyalty. Furthermore, the government’s support for renewable energy sources has increased the value of wood biomass, incentivizing more intensive forest management and consequently higher equipment utilization rates. This unique combination of industrial strength, resource abundance, and regulatory leadership cements Germany’s position at the forefront of the European market.

Sweden Chainsaw Market Analysis

Sweden held a prominent position in the regional market in 2025 due to its status as a global foresattempt powerhoutilize and its deep cultural reliance on wood for energy and construction. The counattempt’s market dynamics are characterized by a high concentration of professional utilizers who demand top-tier performance and durability from their equipment. As per the Swedish Forest Agency, forests cover a significant portion of the nation’s landmass, creating the foresattempt sector a cornerstone of the national economy and a primary driver of chainsaw consumption. The tradition of houtilizehold firewood collection is widespread, with much of the population engaging in seasonal cutting activities, ensuring a steady demand for consumer-grade models. According to indusattempt reports, Swedish utilizers are early adopters of ergonomic and safety innovations, pushing manufacturers to continuously refine their products to meet the exacting standards of local professionals. The cold climate necessitates equipment that performs reliably in freezing conditions, favoring gasoline models with advanced cold start technologies while also spurring interest in battery solutions that function well in low temperatures. The strong presence of domestic manufacturing facilities further strengthens the supply chain and fosters a competitive market environment. Sweden’s commitment to sustainable foresattempt practices also drives the replacement of old, inefficient saws with modern and eco-friconcludely alternatives.

France Chainsaw Market Analysis

France is expected to occupy a significant share of the European chainsaw market during the forecast period due to its diverse foresattempt landscape, strong agricultural sector, and growing emphasis on renewable biomass energy. The nation’s market is distinguished by a balanced mix of professional logging operations in mountainous regions and extensive private ownership in rural areas. As per the National Forest Office of France, the counattempt possesses millions of hectares of forest, much of which is managed by private owners who rely on chainsaws for maintenance and harvesting. The government’s strategic push to increase the utilize of wood energy to meet climate goals has stimulated activity in the foresattempt sector, leading to higher equipment turnover. According to energy transition reports, subsidies for wood heating systems have encouraged homeowners to harvest their own fuel, boosting sales of mid-range chainsaws. The French market also reveals a strong preference for versatile tools suitable for both foresattempt and viticulture, where vineyard maintenance requires precise cutting equipment. The presence of major European manufacturers with localized production and distribution networks ensures the ready availability of parts and service. Additionally, strict noise regulations in rural tourism areas are driving the shift toward quieter battery-operated models, reflecting a market that balances tradition with modern environmental consciousness.

Finland Chainsaw Market Analysis

Finland is estimated to secure a vital position in the market over the forecast period due to its intense foresattempt indusattempt, harsh climatic conditions, and the critical role of wood in its national identity and economy. The counattempt boasts one of the highest proportions of forested land in Europe, which necessitates a high density of chainsaw usage per capita. As per the Natural Resources Institute Finland, the foresattempt sector contributes significantly to GDP, with professional loggers utilizing heavy-duty chainsaws for large-scale harvesting operations year-round. The extreme winter conditions demand equipment with exceptional reliability and cold-weather performance, favoring robust gasoline models equipped with heated handles and advanced air filtration systems. According to cultural studies, the concept of “everyman’s right” allows citizens to access forests freely, leading to widespread recreational and subsistence utilize of chainsaws among the general population. This dual demand from highly efficient industrial operators and active private citizens creates a resilient market structure. Finnish consumers are known for their technical expertise and high expectations regarding tool longevity, pushing manufacturers to deliver premium quality products. The ongoing modernization of logging fleets to improve efficiency and safety further sustains the demand for state-of-the-art chainsaws in this northern European hub.

Italy Chainsaw Market Analysis

Italy maintains a notable share of the European chainsaw market. The unique terrain, thriving olive and fruit farming sectors, and a strong culture of tiny-scale woodland management are propelling the Italian market growth. The market in Italy is distinct due to the prevalence of hilly and mountainous landscapes where lightweight and maneuverable chainsaws are essential for accessing difficult terrain. As per agricultural census data, Italy has millions of tinyholdings and orchards where regular pruning and clearing are necessary, creating a consistent demand for compact and battery-powered models. The olive oil indusattempt, in particular, drives seasonal spikes in chainsaw sales as farmers require reliable tools for maintaining groves. According to indusattempt observations, Italian utilizers place a high value on design and ergonomics, preferring tools that reduce fatigue during prolonged utilize on slopes. The growing trconclude of agritourism has also led to stricter noise control measures in rural areas, accelerating the adoption of silent electric chainsaws. The presence of renowned design and engineering firms in the northern regions fosters innovation in utilizer interface and aesthetic appeal. Furthermore, government incentives for forest restoration and fire prevention have increased public sector procurement of cutting equipment. This blconclude of agricultural necessity, geographical challenges, and aesthetic preference defines Italy’s specific contribution to the broader European market landscape.

COMPETITIVE LANDSCAPE

The competition within the European chainsaw market is characterized by intense rivalry between established legacy manufacturers and emerging brands striving for dominance in the rapidly evolving battery-powered segment. Geopolitical shifts and environmental regulations have triggered a race to innovate, with companies vying to produce the most powerful and longest-lasting cordless solutions. Major contractors leverage their historical reputation for durability to retain professional utilizers while simultaneously courting casual homeowners with utilizer-friconcludely and affordable electric models. The landscape features a mix of specialized foresattempt equipment producers and general power tool giants who utilize their broad distribution networks to gain market access. Differentiation increasingly relies on technological advancements such as smart connectivity, enhanced safety features, and ergonomic design rather than price alone. Supply chain resilience has become a critical competitive advantage as firms struggle to secure components amid global shortages. Strategic acquisitions and collaborations are common as companies seek to acquire battery technology or expand their geographic footprint to meet surging demand driven by energy indepconcludeence trconcludes and sustainable foresattempt practices across the continent.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Chainsaw Market include

- ANDREAS STIHL AG & Co. KG

- Husqvarna AB

- Stanley Black & Decker, Inc.

- Makita Corporation

- Robert Bosch GmbH

- Techtronic Industries Co. Ltd.

- Yamabiko Corporation

- STIGA S.p.A.

- Einhell Germany AG

- Oregon Tool, Inc.

- AL-KO SE

- Alfred Kärcher SE & Co. KG

- The Toro Company

- Koki Holdings Co., Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Stihl Group stands as a preeminent force in the European chainsaw market with a profound influence on global outdoor power equipment standards. The German family-owned enterprise specializes in manufacturing high-performance gasoline and battery-operated chainsaws for professional foresattempt and consumer gardening. Recently, the company has aggressively expanded its portfolio of cordless tools to meet stringent European emission regulations and shifting consumer preferences toward silent operation. Stihl invested heavily in developing proprietary lithium-ion battery platforms that offer extconcludeed runtime and rapid charging capabilities to compete directly with petrol models. The firm continues to strengthen its distribution network across rural and urban centers while launching innovative safety features such as quick stop chain brakes. Its commitment to sustainable manufacturing processes and durable product design ensures it remains the preferred choice for professional loggers and homeowners alike throughout the continent and worldwide.

- Husqvarna Group operates as a pivotal entity in the European chainsaw sector,r leveraging its Swedish heritage to deliver robust and technologically advanced cutting solutions globally. The corporation offers a comprehensive range of chainsaws from lightweight electric models for gardenerto heavy-dutyty professional units for industrial logging operations. Recent strategic actions include the integration of smart connectivity features, allowing utilizers to monitor machine health and optimize performance via smartphone applications. Husqvarna has intensified its focus on battery technology by introducing new high-voltage systems that deliver power equivalent to traditional two-stroke engines without exhaust emissions. The company actively collaborates with foresattempt organizations to promote sustainable harvesting practices and operator safety training programs. Its continuous investment in research and development facilitates the creation of ergonomic designs that reduce utilizer fatigue and vibration exposure. These initiatives solidify its reputation as an innovator, driving the transition toward cleaner and smarter foresattempt equipment across international markets.

- Robert Bosch GmbH maintains a formidable presence in theEuropeane chainsaw market through its renowned engineering expertise and dominant position in the power tool segment. The German conglomerate manufactures a wide array of electric and battery-powered chainsaws under its Bosch and Gardena brands, catering primarily to the homeowner and semi-professional demographics. The company recently accelerated its shift toward fully battery-operated ecosystems by launching high-performance chainsaws compatible with its universal Power For All Alliance battery system. This strategic relocate allows customers to share batteries across multiple tools, enhancing convenience and reducing overall costs. Bosch has also focutilized on integrating advanced safety mechanisms and brushless motor technology to improve efficiency and lifespan. Its extensive retail partnerships and strong brand recognition enable rapid market penetration for new product launches. By prioritizingutilizer-friconcludelyy design and environmental sustainability, Bosch continues to capture significant demand in the growing urban gardening and landscape maintenance sectors across Europe and beyond.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in theEuropeane chainsaw market primarily employ aggressive product innovation strategies focutilizing on the development of high-capacity battery platforms to replace traditional gasoline engines. Companies frequently engage in strategic partnerships with battery cell manufacturers to secure supply chains and reduce production costs for cordless tools. Manufacturers invest heavily in research and development to integrate smart digital features such as connectivity apps and automated safety systems that enhance utilizer experience. Firms actively expand their distribution networks through both specialized dealers and online retail channels to reach diverse customer segments effectively. Brand building through professional sponsorship and operator training programs remains a central tactic to foster loyalty among foresattempt workers. Additionally, companies pursue sustainability initiatives by adopting eco-friconcludely manufacturing processes and offering recycling programs for old equipment to align with European environmental regulations.

MARKET SEGMENTATION

This research report on the europe chainsaw market is segmented and sub-segmented into the following categories.

By Power Source

- Gasoline Powered Chainsaws

- Electric Powered Chainsaws (Corded)

- Battery-Powered Chainsaws

By Bar Length

- Less than 16 Inches

- 16 to 20 Inches

- More than 20 Inches

By Counattempt

- Germany

- Sweden

- France

- Finland

- Italy

- United Kingdom

- Spain

- Rest of Europe

Leave a Reply