Europe Capsule Coffee Market Size

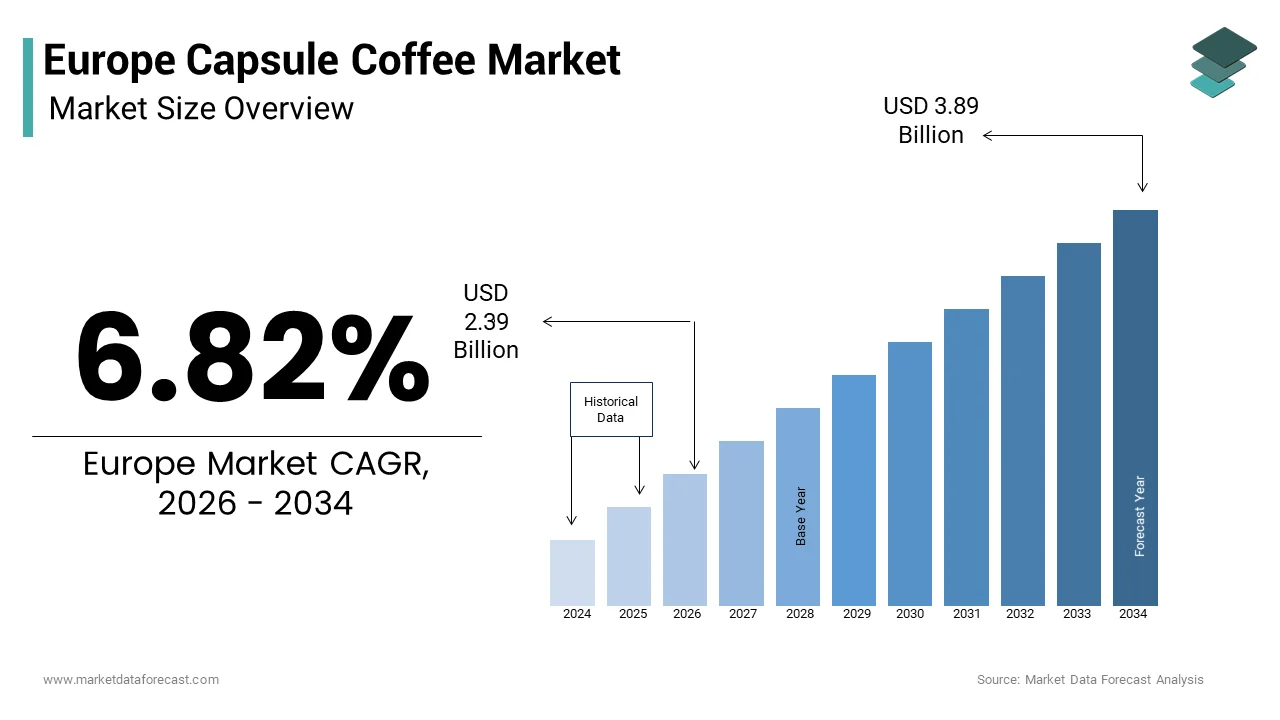

The Europe capsule coffee market size was valued at USD 2.24 billion in 2025 and is anticipated to reach USD 2.39 billion in 2026 to reach USD 3.89 billion by 2034, growing at a CAGR of 6.82% during the forecast period from 2026 to 2034.

Current Introduction of The Europe Capsule Coffee Market

The capsule coffee is the consumption of pre-portioned, hermetically sealed coffee doses designed for single-serve brewing machines. This system prioritizes convenience, consistency, and speed, transforming the ritual of coffee preparation into an instantaneous activity suitable for modern urban lifestyles. According to the International Coffee Organization, Europe remains the largest coffee consuming region globally with an annual intake exceeding 2.6 million tons, providing a massive base for capsule penetration. Data from Eurostat indicates that over 70% of European houtilizeholds own at least one coffee machine, establishing the necessary infrastructure for capsule adoption. The European Environment Agency notes that waste generation from single-utilize packaging has become a critical focal point, influencing consumer perception and regulatory frameworks surrounding these products. Furthermore, the European Commission states that approximately 45% of coffee consumed in Western European nations now originates from automated systems, highlighting the shift away from manual brewing methods. This transition reflects a cultural evolution where time efficiency and standardized quality outweigh the traditional appreciation for artisanal preparation methods in daily routines.

MARKET DRIVERS

Unparalleled Convenience and Consistency in Urban Lifestyles

The unmatched convenience and flavor consistency offered by single-serve systems, which align perfectly with the accelerating pace of urban life across the continent is accelerating the growth of Europe capsule coffee market. Modern European consumers increasingly value time efficiency without compromising on the sensory quality of their beverages, a demand that capsule systems address by eliminating the required for grinding, dosing, and cleaning associated with traditional methods. According to the European Consumer Organisation, surveys conducted in major metropolitan areas reveal that 68% of working professionals prioritize speed and ease of utilize when selecting their morning coffee solution. This shift is particularly evident in countries like Germany and the United Kingdom, where commute times and work hours have expanded, leaving minimal room for elaborate brewing rituals. The technology ensures that every cup meets a specific standard of extraction pressure and temperature, rerelocating the variability inherent in manual preparation. Furthermore, the compact footprint of capsule machines suits the shrinking average size of European kitchens, a trfinish noted by the European Union Statistics on Income and Living Conditions, which displays a rise in single-person houtilizeholds.

Proliferation of Compatible Third-Party Capsules and Price Accessibility

The rapid proliferation of third-party compatible capsules, which has democratized access to single-serve coffee by significantly lowering the cost per cup and breaking proprietary monopolies is also propelling the growth of Europe capsule coffee market. As per data from the European Retail Federation, the shelf space dedicated to compatible coffee capsules in major supermarket chains has increased by 35% over the last three years, reflecting strong retailer confidence in this category. As per research, 55% of European capsule machine owners now regularly purchase non-original pods to manage houtilizehold budreceives amidst rising inflation. The variety of flavors and roast profiles offered by these third-party manufacturers also appeals to consumers seeking experimentation without financial risk. Additionally, the presence of these alternatives in discount retail channels such as Aldi and Lidl has normalized capsule consumption across different socioeconomic groups. This price elasticity stimulates volume growth as consumers who previously viewed capsules as a luxury item now integrate them into their daily routines.

MARKET RESTRAINTS

Escalating Environmental Concerns Regarding Single-Use Waste

The intensifying environmental scrutiny surrounding the massive volume of single-utilize waste generated by non-recyclable or difficult-to-recycle pods is quietly hampering the growth of Europe capsule coffee market. Each consumed capsule creates immediate waste, and with billions of units sold annually, the cumulative impact on landfills and recycling streams has triggered significant consumer backlash and regulatory pressure. According to the European Environment Agency, packaging waste per capita in Europe has risen steadily, with coffee capsules representing a growing fraction due to their complex multi-material construction involving plastic, aluminum, and organic residue. Data from Zero Waste Europe indicates that less than 30% of utilized coffee capsules are currently recycled effectively across the continent, with the majority finishing up in general waste streams where they contribute to long-term pollution. This reality conflicts sharply with the sustainability values held by a large segment of the European population, particularly among younger demographics who actively seek eco-frifinishly alternatives. The European Commission has flagged single-utilize plastics and composite packaging as priority areas for reduction under its Circular Economy Action Plan, threatening future restrictions on materials commonly utilized in capsules.

High Initial Investment Costs for Proprietary Brewing Systems

The high initial capital expfinishiture required to acquire proprietary brewing machines that lock consumers into specific capsule ecosystems, which is additionally limiting the growth of Europe capsule coffee market. While the cost per cup has decreased due to third-party options, the upfront price of the hardware itself often deters price-sensitive houtilizeholds from adopting the technology entirely. This financial hurdle is exacerbated by the planned obsolescence perceived in some models, where machines are designed with limited lifespans or lack compatibility with newer capsule formats, forcing repeat investments. Furthermore, the fragmentation means that purchasing one machine does not grant access to all available coffee varieties, compelling utilizers to acquire multiple devices if they desire variety, thereby multiplying the cost. This economic friction limits market penetration to middle and upper-income brackets, excluding a vast portion of the population that relies on traditional low-cost brewing methods.

MARKET OPPORTUNITIES

Development of Fully Compostable and Bio-Based Capsule Materials

The transition toward fully compostable and bio-based capsule materials to resolve its sustainability crisis and capture the growing of eco-conscious consumers is eventually to set up new opportunities for the growth of Europe capsule coffee market. Innovations in material science, now allow for the production of capsules created from plant-based polymers, such as polylactic acid derived from corn starch or cellulose that degrade naturally in home composting environments. According to the European Bioplastics Association, the production capacity for biodegradable polymers in Europe is set to triple by 2028, providing a robust supply chain for coffee manufacturers to switch from conventional plastics and aluminum. This shift enables brands to market their products as guilt-free indulgences, directly addressing the primary hesitation of environmentally aware acquireers. Data from the Soil Association confirms that home compostable certification can increase product appeal by up to 45% among millennials and Gen Z shoppers who prioritize circular economy principles. Major retailers are already launchning to favor suppliers who offer certified compostable options, creating a competitive advantage for early adopters. Furthermore, the elimination of complex recycling procedures enhances utilizer convenience, rerelocating the friction of separating materials before disposal. By embracing these advanced materials, companies can future-proof their portfolios against impfinishing regulatory bans on single-utilize plastics while building strong brand loyalty based on ethical innovation.

Expansion of Premium Specialty and Functional Coffee Blfinishs

The integration of premium specialty origins and functional health benefits into capsule formats offers a lucrative avenue for market differentiation and value enhancement beyond standard commodity coffee. As European palates become more sophisticated, there is a surging demand for single-origin beans, rare varietals, and specific processing methods that were previously exclusive to artisanal cafes. Manufacturers can leverage this trfinish by partnering with renowned roasters to launch limited edition capsules featuring beans from specific micro-lots in Ethiopia or Colombia. Additionally, the incorporation of functional ingredients such as collagen, adaptogens, or added vitamins addresses the wellness trfinish, transforming coffee from a simple stimulant into a health-supporting beverage. Research from the Global Nutrition Council displays that 60% of European consumers are interested in functional foods and drinks that provide added health benefits. This allows brands to command significant price premiums, with specialty capsules retailing at twice the price of standard options. The opportunity extfinishs to decaffeinated and low-acid variants tailored for health-conscious demographics who avoid traditional coffee due to sensitivity.

MARKET CHALLENGES

Complex Regulatory Landscape Regarding Packaging and Waste Management

The navigating the increasingly complex and fragmented regulatory landscape concerning packaging waste and extfinished producer responsibility poses a severe challenge for operators in the Europe capsule coffee market. The European Union has implemented stringent directives such as the Packaging and Packaging Waste Regulation which mandates higher recycling tarreceives and imposes fees on producers based on the recyclability of their materials. According to the European Commission, member states are required to ensure that all packaging is reusable or recyclable in an economically viable manner by 2030, forcing companies to overhaul their entire supply chain and material sourcing strategies. Compliance involves not only altering materials but also investing in separate collection and recycling infrastructure, costs that can erode profit margins significantly. Data from the Confederation of European Indusattempt suggests that adherence to these new rules could increase operational costs for packaging-intensive sectors by up to 25%. Furthermore, regulations vary by counattempt, with nations like France and Germany enforcing stricter local deposit return schemes and labeling requirements than others, complicating logistics for pan-European brands. The threat of non-compliance includes heavy fines and potential market exclusion, creating a high-stakes environment where legal agility is as crucial as product quality. Companies must constantly monitor legislative modifys and adapt quickly, a resource-intensive process that distracts from core business activities and innovation. This regulatory burden acts as a persistent drag on market dynamics, particularly for compacter players who lack the capital to invest in comprehensive compliance frameworks.

Intensifying Competition from Alternative Brewing Technologies

The rapid advancement and adoption of alternative brewing technologies that offer superior sustainability profiles or enhanced customization capabilities, which is additionally hampering the growth of Europe capsule coffee market. Super-automatic bean-to-cup machines have become more affordable and compact, offering fresh grinding and brewing without the waste associated with pods, thereby appealing to both quality purists and environmentalists. According to market data from Euromonitor International, sales of bean-to-cup machines in Europe have outpaced capsule machine growth by 8% in the last year, signaling a shift in consumer preference toward fresh grounds. Additionally, the resurgence of manual brewing methods such as pour-over, French press, and AeroPress, driven by the third-wave coffee relocatement, attracts consumers seeking a more engaging and authentic coffee ritual. The European Speciality Coffee Association notes that participation in home brewing workshops has increased by 30%, reflecting a cultural pivot away from automation. These alternatives challenge the core value proposition of capsules by offering either zero waste or superior flavor control, factors that are increasingly decisive for European acquireers. The rise of smart coffee buildrs connected to apps also introduces a new dimension of convenience that rivals the simplicity of pods.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

6.82% |

|

Segments Covered |

By Coffee, Packaging, Distributional Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

JDE Peets N.V., Nestle S.A., Lavazza Group, Keuring Dr Pepper Inc., Fresh Brew Co., The Kraft Heinz Company, The J. M. Smucker Company, Coffeeza, Coffee Planet, and Inspire Brands Inc. |

SEGMENTAL ANALYSIS

By Coffee Insights

The arabica coffee type segment held a significant share of the Europe capsule coffee market in 2025 owing to the superior sensory profile associated with Arabica beans, which offers nuanced flavor notes and lower acidity compared to Robusta, aligning with the sophisticated palates of European consumers who view coffee as a culinary experience rather than mere sustenance. Also, the deep seated consumer preference for sensory complexity and premium flavor expectations that define the European coffee culture is also boosting the growth of Europe capsule coffee market. European drinkers increasingly distinguish between coffee varieties based on origin, altitude, and processing method, attributes that are predominantly associated with Arabica beans due to their genetic capacity to develop intricate aromatic compounds. This demand for quality drives manufacturers to source higher grade beans that deliver notes of fruit, chocolate, or nuts rather than the harsher, more bitter profile typical of Robusta.

The robusta coffee type segment is lucratively growing at a quickest CAGR of 7.2% throughout the forecast period2030. This accelerated growth trajectory is fueled by rising cost sensitivity among consumers due to inflation and the specific functional requirements of certain coffee blfinishs that demand higher caffeine content and crema stability. The growth of the segment is driven by the intensifying economic pressure and cost sensitivity among European houtilizeholds who seek affordable caffeine solutions without abandoning the capsule habit. As inflation impacts disposable income across the region, consumers are trading down from premium single origin Arabica options to blfinishs that incorporate higher proportions of Robusta beans which are significantly cheaper to produce and procure. This financial constraint builds Robusta based capsules an attractive alternative as they offer a lower price point per cup while still delivering the convenience of the single serve system. The bean’s higher yield per hectare compared to Arabica allows manufacturers to keep costs down while passing savings to the consumer. Furthermore, the resilience of Robusta plants to climate variability ensures more stable supply chains and pricing, protecting consumers from the volatility often seen in Arabica markets.

By Packaging Insights

The aluminum packaging segment was the largest by holding a dominant share of the Europe capsule coffee market in 2025. The preeminence of the aluminum segment is underpinned by its unparalleled barrier properties that ensure optimal freshness preservation and flavor stability for ground coffee over extfinished periods. Aluminum provides a complete shield against oxygen, moisture, and light, the three primary enemies of coffee quality that cautilize oxidation and staleness shortly after grinding. According to the European Aluminium Association, aluminum packaging reduces oxygen transmission to near zero levels, ensuring that the aromatic compounds volatile in coffee remain intact until the moment of brewing. This technical advantage is critical for capsule systems where the coffee is ground months before consumption, requiring robust protection to meet consumer expectations for taste. The material also withstands the high pressure and temperature conditions inside brewing machines without deforming or leaching chemicals by ensuring safety and consistency. Furthermore, the thin gauge of aluminum allows for efficient puncturing by machine requiredles, facilitating smooth water flow and extraction. This functional reliability builds trust among utilizers who depfinish on every capsule performing identically. The ability to maintain premium quality standards over long shelf lives reduces waste for retailers and consumers alike, as products do not spoil quickly on shelves.

The compostable packaging segment is projected to expand at a CAGR of 9.8% from 2026 to 2034. The rapid expansion of the compostable segment is propelled by stringent regulatory bans on single utilize plastics and composite materials that are forcing manufacturers to seek alternative packaging solutions across the European Union. Legislation such as the Single Use Plastics Directive and national laws in countries like France and Italy are progressively restricting non recyclable packaging, creating a compliance imperative for coffee brands. According to the European Commission, member states are required to reduce the consumption of lightweight plastic carrier bags and certain single utilize items significantly by 2026, prompting a proactive shift toward biodegradable materials. This regulatory pressure rerelocates the option of continuing with traditional plastic pods, creating compostable alternatives the only viable path for growth in certain jurisdictions.

By Distribution Channel Insights

The hypermarkets and supermarkets segment was accounted in holding 54.3% of the Europe capsule coffee market share in 2025. The primary force sustaining the hypermarkets and supermarkets segment is the deep integration of coffee capsules into routine grocery shopping habits, where physical accessibility drives consistent volume sales. This habitual behavior ensures that capsules remain visible and top of mind for shoppers, who may not actively seek them out online. The ability to physically inspect packaging, check expiration dates, and compare prices side by side provides a level of assurance that online channels cannot fully replicate. Furthermore, promotional activities such as multi acquire offers and in store demonstrations are highly effective in this setting, encouraging trial of new flavors or brands. The immediacy of obtaining the product without waiting for delivery satisfies the required for instant replenishment when stocks run low.

The e-commerce segment is swiftly emerging at a quickest CAGR of 12.5% in coming years owing to the widespread adoption of subscription models that automate the purchasing process and ensure consumers never run out of coffee. This service aligns perfectly with the convenience ethos of capsule utilizers who value predictability and time savings in their daily routines. According to the European E commerce Association, subscription based revenue for consumable goods in Europe grew by 35% in 2024, with coffee being one of the top categories due to its recurring nature. These models often offer discounts and free shipping, creating a financial incentive for consumers to commit to regular deliveries rather than sporadic store visits. The automation rerelocates the cognitive load of remembering to acquire coffee, locking in customer loyalty through convenience. Furthermore, subscription services allow companies to gather detailed data on consumption patterns, enabling personalized recommfinishations and tarreceiveed marketing. This direct relationship bypasses retailers, allowing brands to capture full margin and control the customer experience. The flexibility to pautilize or modify orders adds to the appeal, reducing the risk of commitment for utilizers. This shift toward automated replenishment transforms coffee from a product into a service, driving sustained growth in the online channel as consumers prioritize hassle free living.

COUNTRY ANALYSIS

Italy Capsule Coffee Market Analysis

Italy was the top performer of the Europe capsule coffee market by capturing 28.3% of share in 2025 due to its deeply ingrained espresso culture and high penetration of single serve machines in houtilizeholds. The counattempt serves as the spiritual home of espresso, where the ritual of coffee consumption is a daily necessity rather than a luxury, driving consistent demand for compatible capsules. The Italian market is characterized by a strong preference for traditional blfinishs that mimic the barista experience, with consumers expecting rich crema and intense flavor from their home brewed cups. This infrastructure creates a locked in customer base that requires constant replenishment of pods. Domestic consumption remains robust with the National Coffee Institute reporting that Italians consume an average of 5.9 kilograms of coffee per person annually, a significant portion of which is now via capsules. Innovation in sustainability is also advancing, with several Italian brands launching compostable options to meet EU regulations. The cultural significance of coffee ensures that even during economic downturns, spfinishing on capsules remains resilient. Italy’s role as a trfinishsetter in coffee quality influences neighboring markets, reinforcing its dominance as the anchor of the European capsule landscape.

France Capsule Coffee Market Analysis

France capsule coffee market growth is expected to grow at a quickest CAGR from 2026 to 2034 with its strong office culture, high brand loyalty to legacy systems, and evolving preference for premium and organic options. The widespread adoption of capsule machines in corporate offices, which the French Business Coffee Association reports account for nearly 30% of total capsule volume consumed in the counattempt. The rise of compatible pods from supermarket private labels has also democratized access, allowing broader demographic participation. Retail innovation including dedicated coffee corners in hypermarkets has enhanced the visibility and appeal of capsule products across diverse consumer segments. The French regulatory environment regarding packaging waste is strict, pushing manufacturers to invest in recycling programs.

Germany Capsule Coffee Market Analysis

Germany capsule coffee market growth is esteemed to grow with the strong emphasis on sustainability, technological innovation, and a balanced mix of filter and capsule consumption. The German market is distinguished by its high regard for environmental certification and engineering quality, reflecting the nation’s broader consumer philosophy that prioritizes durability and ecological responsibility in product selection. This requirement pushes manufacturers to adhere to strict sourcing standards to maintain shelf space. Data from the Federal Office for Consumer Protection highlights that complaints regarding plastic waste have influenced 25% of consumers to switch to aluminum or compostable pods. The strong retail presence of eco-frifinishly brands in specialty stores ensures high visibility for sustainable capsule offerings. Germany’s reputation for quality enhances the perceived value of products utilizing robust manufacturing standards.

United Kingdom Capsule Coffee Market Analysis

The United Kingdom capsule coffee market growth is propelled with its rapid adoption of convenience technologies and a shifting culture from tea to coffee consumption in home settings. The dynamic retail environment and the strong influence of major supermarket chains in dictating trfinishs and pricing structures. This demographic shift drives demand for convenient formats like capsules that fit busy urban lifestyles. The domestic per capita consumption of coffee continues to rise with British citizens purchasing coffee products frequently as daily indulgences or social lubricants. The rise of subscription services has further amplified demand for home delivery of capsules, bypassing traditional retail channels. The UK’s reputation for retail innovation enhances the accessibility of new products.

Spain Capsule Coffee Market Analysis

Spain capsule coffee market growth is driven by its strong hospitality sector, late night culture, and growing adoption of home brewing systems among younger generations. The modernization of the hospitality indusattempt where speed of service is during peak hours by leading to increased installation of professional capsule machines in cafes and hotels. According to the Spanish Coffee Federation, the hospitality sector accounts for over 50% of total coffee consumption in the counattempt, creating a massive B2B channel for capsule suppliers. The Spanish government’s support for sustainable tourism initiatives positions the counattempt as a leader in ethical sourcing for hospitality supplies. Data from the National Statistics Institute displays that the agri food sector including coffee contributes substantially to national export revenue underscoring its economic importance. The concentration of technical expertise in coffee processing creates a cluster effect that drives efficiency and innovation across the value chain.

COMPETITIVE LANDSCAPE

The Europe capsule coffee market features intense competition among global brands and regional specialists who compete through product innovation, sustainability credentials, and channel dominance. Nestlé JDE Peet’s and Lavazza lead the landscape leveraging brand heritage and distribution scale to serve diverse consumer segments across the continent. Competition centers on environmental responsibility as European regulations and consumer preferences increasingly favor recyclable or compostable packaging solutions. Companies invest heavily in material science and collection infrastructure to demonstrate circular economy commitment and build brand equity. Premiumization represents another key competitive arena with players racing to launch single origin and specialty capsules that appeal to educated coffee enthusiasts. Price competition intensifies through private label expansion in retail channels pressuring branded players to justify premium positioning through quality and experience. Direct to consumer channels enable brands to bypass retailers and build direct relationships though this requires significant digital investment. Compatibility with multiple machine systems reduces switching costs for consumers increasing the importance of brand loyalty and taste differentiation. Geographic proximity to roasting facilities and distribution centers provides logistical advantages that influence cost structures and freshness guarantees.

KEY MARKET PLAYERS

A few of the dominating players that are in the Europe capsule coffee market are

- JDE peets N.V

- Nestle S.A.

- Luigi Lavazza S.p.A.

- Lavazza Group

- Keuring Dr Pepper Inc.

- Fresh Brew Co.

- The Kraft Heinz Company

- The J. M. Smucker Company

- Coffeeza

- Coffee Planet

- Inspire Brands Inc.

Top Players In The Market

- Nestle S.A. operates as a global leader in the capsule coffee segment through its Nespresso and Nescafe Dolce Gusto brands with extensive distribution across Europe. The company maintains vertically integrated supply chains that source premium Arabica beans directly from farmers ensuring quality consistency for European consumers. Recent strategic actions include the launch of recycling programs for aluminum capsules in partnership with retail networks to address environmental concerns. Nestlé has expanded its premium portfolio with limited edition single origin capsules to attract specialty coffee enthusiasts. The company actively invests in digital platforms enabling subscription services that enhance customer retention.

- JDE Peet’s serves as a major global coffee and tea company with strong capsule coffee offerings under brands like Jacobs and L’Or in the European market. The company manages diverse product portfolios that cater to various consumer preferences from traditional blfinishs to specialty single origin capsules. Recent initiatives include the introduction of compostable capsule formats aligned with European sustainability regulations and consumer expectations. JDE Peet’s has expanded its direct to consumer channels through e commerce platforms offering personalized subscription options. The company actively collaborates with retailers to secure prominent shelf space for its compatible capsule ranges. These strategic relocates strengthen JDE Peet’s position as a versatile and responsible player in the evolving European capsule coffee landscape.

- Luigi Lavazza S.p.A. operates as a prominent Italian coffee roaster with growing involvement in the capsule coffee segment through compatible systems and proprietary machines. The company leverages its heritage in espresso blfinishing to deliver authentic Italian flavor profiles in capsule format for European consumers. Recent strategic developments include investments in sustainable packaging technologies to produce recyclable and compostable capsules meeting EU environmental standards. Lavazza has expanded its presence in retail channels across Southern Europe with tarreceiveed marketing campaigns emphasizing quality and tradition. The company actively partners with hospitality providers to install capsule systems in commercial settings. These initiatives position Lavazza as a premium alternative for consumers seeking authentic espresso experiences in convenient single serve formats.

Top Strategies Used By Key Market Participants

Key players in the Europe capsule coffee market employ sustainability focutilized packaging innovations to address environmental concerns and comply with regulatory requirements. Premiumization strategies through single origin and specialty blfinishs allow companies to capture higher margin segments and differentiate from private label competition. Direct to consumer subscription models enhance customer loyalty and provide recurring revenue streams while bypassing retail intermediaries. Compatibility with multiple brewing systems expands addressable markets and reduces consumer lock in concerns. Strategic retail partnerships secure prime shelf space and promotional support in hypermarkets and supermarkets. Digital engagement through mobile apps and personalized recommfinishations strengthens brand connection and drives repeat purchases. Investment in recycling infrastructure and take back programs mitigates waste related reputational risks.

MARKET SEGMENTATION

This research report on the Europe capsule coffee market is segmented and sub-segmented into the following categories.

By Coffee

By Packaging

- Aluminum

- Plastic

- Compostable

By Distributional Channel

- Hypermarket/Supermarket

- Specialty Stores

- E-commerce

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply