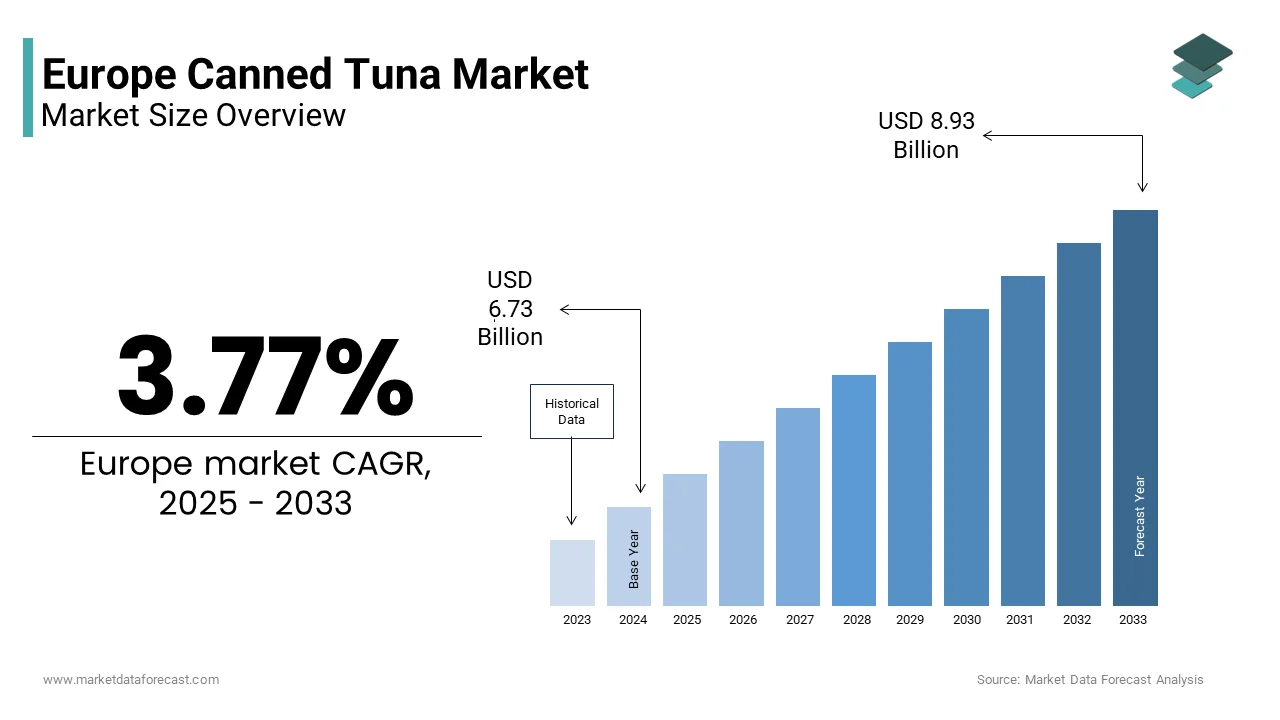

Europe Canned Tuna Market Size

The Europe canned tuna market size was valued at USD 6.49 billion in 2024 and is anticipated to reach USD 6.73 billion in 2025 to USD 8.93 billion by 2033, growing at a CAGR of 3.77% during the forecast period from 2025 to 2033.

Canned tuna is a mature yet dynamically evolving protein segment shaped by shifting dietary preferences, sustainability imperatives, and regulatory oversight of marine sourcing. Canned tuna is defined as tuna preserved in sealed containers through heat sterilization, typically packed in oil, brine, or spring water. This product serves as a staple in houtilizehold pantries due to its extconcludeed shelf life, nutritional density, and culinary versatility. According to industest sources, per-capita consumption of canned tuna in the European Union has been cited at around 1.3 kg annually, significantly lower than your stated 2.8 kg. While traditional markets such as Spain and Italy continue to lead demand, younger and health-conscious consumers in northern and eastern regions are also contributing to growth. Imports account for a large portion of tuna consumed in the EU, as over half of the supply is sourced externally.

MARKET DRIVERS

Rising Demand for Convenient and Nutrient-Dense Protein Sources Drives Consumption

European consumers increasingly prioritize time-efficient meals without compromising nutritional quality, a trconclude amplified by dual-income houtilizeholds, which is one of the key factors propelling the canned tuna market growth in Europe. Canned tuna offers a ready-to-eat source of high-quality protein, omega-3-3 fatty a, acids and essential micronutrients such as selenium and vitamin D, aligning with dietary guidelines issued by national health authorities. According to the European Commission’s 2024 Consumer Food Trconcludes Monitor, a majority of EU respondents identified protein content as a key factor when purchasing canned fish products. As per the European Food Safety Authority, a standard 100g serving of light tuna in water provides a significant amount of protein and long-chain omega-3 fatty acids that support objectives such as cardiovascular risk reduction and muscle maintenance in ageing populations. For example, in Germany, canned tuna in ready-meal formulations has grown noticeably among working professionals. Supermarkets in France and the Netherlands have expanded ambient protein-aisle offerings featuring tuna-based salads, wraps, and pasta kits, reflecting retailer recognition of the convenience-nutrition nexus.

Strong Cultural and Culinary Integration in Southern European Diets Sustains Baseline Demand

Canned tuna remains deeply embedded in the culinary traditions of Southern Europe,e, particularly in Spain, Italy, and Portugal, where it features in iconic dishes such as ensaladilla rusa, viinformo tonnato, and atum com batata, which is further boosting the regional market expansion. This cultural anchoring ensures consistent houtilizehold penetration and intergenerational consumption patterns that resist short-term market volatility. In Spain, per-person consumption of canned tuna is notably higher than the EU average, which is a pattern also seen in Italy, where tuna is viewed as a premium pantest staple rather than a fallback protein. In Italian houtilizeholds, penetration of canned tuna is very high, and regional preferences vary by oil type and tuna species. These factors support to insulate demand in Southern Europe from price volatility and sustain a resilient core consumption base that anchors the broader EU market.

MARKET RESTRAINTS

Stringent EU Regulations on Mercury and Heavy Metal Content Constrain Product Formulation

The European Union enforces some of the world’s strictest limits on contaminants in seafood, including mercury in canned tuna, which directly impacts sourcing, processing, and labeling strategies and is primarily hampering the growth of the European market. Regulation (EC) No 1881/2006 establishes a maximum mercury level of 1.0 mg/kg wet weight for certain tuna species marketed in the EU. Several analyses of canned tuna on the EU market have raised concerns about elevated mercury concentrations. For example, according to a survey, a large proportion of samples exceeded a 0.3 mg/kg threshold utilized for many fish species, despite tuna being subject to a higher limit. These regulatory requirements lead processors to implement comprehensive traceability and testing regimes. Becautilize mercury levels vary by species, size, and region, some brands choose compacter tuna species that tconclude to accumulate less mercury, or invest in sophisticated screening technologies at unloading. These compliance obligations increase production cost and reduce flexibility in raw-material sourcing, especially in lower-margin segments where price sensitivity is high.

Increasing Consumer Skepticism Over Sustainable Sourcing and Bycatch Practices

European consumers exhibit growing ethical scrutiny toward seafood supply chains, with canned tuna facing heightened pressure due to historical associations with destructive fishing methods, which is further hindering the growth of the European canned tuna market. According to a recent Eurobarometer survey on sustainable consumption, a substantial share of EU citizens now declare that fishing practices play an important role when choosing canned fish. This sentiment is amplified by NGO campaigns highlighting issues such as dolphin mortality and juvenile-tuna bycatch in purse seine fisheries utilizing fish-aggregating devices. According to the Marine Stewardship Council, growth was seen in certified tuna products, yet it also identifies a significant gap between consumer expectations and actual eco-certification coverage in Western Europe. Major retailers such as Carrefour and Tesco now mandate sourcing verification for private-label tuna, which is a requirement that excludes a large portion of the global tuna supply. Consequently, brands without transparent chain-of-custody systems face shelf-space reductions and reputational risks. In this way, ethical consumerism is transforming sustainability from a marketing differentiator into a market-access prerequisite, especially in eco-conscious markets like Sweden and Germany.

MARKET OPPORTUNITIES

Expansion into Premium Health Focutilized Product Formats Creates New Revenue Streams

The strategic shift toward premiumized offerings that cater to wellness-oriented consumers seeking clean label and functional benefits is one of the promising opportunities for the European canned tuna market. Brands are reformulating products with organic extra virgin olive oil, spring water packaging, reducereduced-sodiumum variants, nd added nutrients such as vitamin B12 and iron to align with EU health claim regulations. The European canned-tuna market is revealing notable growth in the premium segment as consumers increasingly seek gourmet formats over commodity-priced cans. In markets like France, brands such as Connétable and Ortiz have extconcludeed their offering into premium lines such as hand-cut loins, protected geographical indications, and elevated packaging to support higher price points. In Germany, discounters are now stocking MSC-certified skipjack tuna in recyclable steel cans with QR codes linking back to catch-vessel and fishery data, which is responding to transparency demands. At the same time, the European Commission’s “Farm to Fork” initiative is incentivising value-added processing and sustainable sourcing in seafood, which supports the pivot to premium formats. By upgrading toward premium positioning, manufacturers are able to offset raw-material inflation, build stronger brand equity, and reduce their depconcludeence on the lowest-price commodity tier.

Development of Private Label Offerings by Retailers Enhances Market Accessibility

European supermarket chains are aggressively expanding private label canned tuna portfolios to offer quality-assured yet affordable protein options, driving category penetration across income segments, which is another notable opportunity for the European market. Unlike generic store brands, private label tuna in Europe often adheres to stringent sourcing and sustainability criteria set by retailers themselves. Retailers in the European canned-tuna sector have significantly increased their utilize of private-label products, and many are entering direct contracts with certified sustainable canneries in developing-countest sourcing regions. Private-label lines increasingly include eco-labelling and traceability features,, es with some retailers disclosing catch method, vessel name, or sustainability certification on the packaging. At the same time, packaging regulations (such as the Single Use Plastics Directive) are pushing the sector toward fully recyclable materials for private-label tuna and other canned fish. These shifts are increasing retailer control over sourcing and costs, and simultaneously heightening competitive pressure on branded tuna manufacturers that cannot match the traceability and price points of retailer-owned brands.

MARKET CHALLENGES

Vulnerability to Geopolitical Disruptions in Key Import Supply Chains

The depconcludeency on imported raw material sourced from processing hubs in Thailand, Vietnam, and Ecuador is primarily challenging the expansion of the European canned tuna market. This degree of sourcing concentration creates exposure to trade-policy shifts, labour shortages, and port-congestion risks in origin countries. In major processing hubs, the combination of rising wages, vessel crew shortage,s, and raw-material constraints has already affected supply dynamics. Likewise, strikes, logistic bottlenecks, and port-clearance disruptions in export hubs can delay shipments bound for Europe. Moreover, European regulations such as the EU IUU Regulation require validated catch documentation for each consignment, which introduces additional clearance steps and potential lead-time impacts. These systemic depconcludeencies amplify variability in lead times and inventory-carrying costs, particularly in “just-in-time” retail distribution models. Without diversified sourcing strategies or near-shoring options, the European canned-tuna supply remains vulnerable to external shocks that lie beyond the control of processors and purchaseers.

Intensifying Competition from Alternative Canned Proteins and Plant-Based Substitutes

The growing competitive pressure from both traditional seafood alternatives and emerging plant-based proteins that appeal to flexitarian and environmentally conscious consumers is also challenging the European canned tuna market growth. Canned sardines, mackerel, el, and salmon have gained traction due to higher omega-3-3 content and perception of lower trophic level sustainability. Canned sardine consumption in the EU has revealn signs of growth, particularly driven by demand in Portugal and Spain, while at the same time, plant-based seafood alternatives are gaining traction as brands offering tuna-style shreds created from soy, algae, and other ingredients are tarreceiveing the same convenience and salad occasions but bypassing concerns around mercury and over-fishing. Retailers are responding accordingly. For example, some chains allocate shelf space to both plant-based and canned tuna in the protein aisle. This dual front of competition is fragmenting consumer attention and forcing traditional tuna brands to further justify their environmental and health credentials.

REPORT COVERAGE

|

EPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

3.77% |

|

Segments Covered |

By Product, Distribution Channel, And Region |

|

Various Analyses Covered |

Global, Regional, and Countest Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Frinsa, Century Pacific Food Inc., Jealsa, Thai Union Group PCL., Bumble Bee Foods, LLC, Grupo Calvo, Wild Planet Foods, Aneka Tuna Indonesia, American Tuna, Ocean Brands GP |

SEGMENTAL ANALYSIS

By Product Insights

The skipjack tuna segment accounted for the dominating share of the European canned tuna market in 2024. The dominance of the skipjack segment in the European market is primarily attributed to the biological economics and regulatory alignment. Skipjack tuna’s position as the leading species stems from its compacter size and shorter lifespan, which result in significantly lower bioaccumulation of mercury compared to larger species like yellowfin. According to the European Food Safety Authority, mercury levels in tuna species vary significantly by species and size, with compacter- and lower-trophic‐level species generally revealing lower concentrations. This safety margin allows brands to position certain species as more suitable for vulnerable consumer groups, such as children and pregnant women, provided the sourcing and testing are rigorous. In recent years, regulatory monitoring has identified mercury violations in canned-tuna shipments, which places pressure on processors to rely on species with lower average mercury content. Consequently, many major retailers now favour such species for private-label children’s lines. The species’ alignment with lower-trophic-level consumption is also consistent with the Farm to Fork Strategy of the European Commission, which encourages sustainable and health-aware seafood choices. Toreceiveher, these factors strengthen the case for choosing species with favorable safety and regulatory-compliance profiles in mass-market canned-tuna supply and contributing to the domination of the skipjack tuna segment in the European market.

The yellowfin tuna segment is expected to revealcase a CAGR of 7.12% over the forecast period in the European mar,, ket owing to the premiumization and culinary demand for superior texture and flavor. Yellowfin loins are firmer and less flaky than skipjack, building them preferred for gourmet preparations such as salade niçoise and viinformo tonnato. In Italy and France, specialty brands emphasise yellowfin tuna as a premium product that often commands higher price points than standard skipjack cans due to perceptions of superior quality. Sustainable certification of yellowfin fisheries has enabled European brands to offer premium options that emphasise traceability and eco-credentials. According to sources, “gourmet” canned-tuna lines (including those featuring yellowfin) are growing rapider than the base category in Western Europe. The inclusion of products such as “Tonno di Sciacca” from Sicily reinforces the artisanal and high-quality appeal of this species. This convergence of culinary prestige, sustainability validation, and brand storyinforming is accelerating the adoption of yellowfin in mass-market canned tuna supply chains and propelling the expansion of the yellowfin tuna segment in the European market.

By Distribution Channel Insights

The hypermarkets and supermarkets segment led the market by occupying the major share of the European market by distribution channel in 2024. The entrenched grocery shopping behaviors and strategic category management are primarily driving the dominance of the hypermarkets and supermarkets segment in the European market. Supermarkets and hypermarkets anchor canned tuna distribution through aggressive private label development that balances affordability and sustainability. Retailers across Europe have significantly increased their focus on private-label canned tuna by securing direct contracts with certified canneries in origin countries to achieve cost and supply-chain control. These programmes frequently feature transparent labelling, such as catch-method disclosures, vessel name,,s or source certification to meet rising consumer demand for traceability. Regulatory drivers such as the Single Use Plastics Directive have also prompted many retailers to adopt fully recyclable steel cans for private-label lines, which is enhancing environmental credentials. At the same time, supermarkets treat canned tuna as a high-rotation staple to leverage seasonal promotional peaks (e.g., during Lent or summer salad months) to drive bquestionet size. This combination of pricing power, sustainability integration, and promotional strategies is significantly contributing to the growth of the supermarkets and hypermarkets segment in the European market.

The online distribution channel segment is projected to record a promising CAGR of 13.3% over the forecast period in the European market. The broader digitization of grocery shopping, accelerated by urbanization and convenience demands, is majorly boosting the expansion of the online segment in the European market. According to Eurostat, around 75% of EU internet utilizers created online purchases in 2023, reflecting the strong foundation for growth in digital grocery channels. Online platforms such as Ocado in the UK and Picnic in the Netherlands now employ algorithm-driven replenishment to autosuggest tuna based on purchase history, which is reducing decision fatigue. Premium and sustainable brands also benefit from digital storyinforming, such as Italian brand Rio Mare increased direct-to-consumer engagement through its e-commerce site featuring video content on pole-and-line fishing. Furthermore, subscription models for pantest essentials are emerging, with companies like BringBack offering curated, sustainable seafood boxes that are delivered monthly. This digital enablement of discovery, convenience, and brand engagement is likely to boost the expansion of the online segment in the regional market during the forecast period.

COUNTRY ANALYSIS

Spain Canned Tuna Market Analysis

Spain captured 23.7% of the European canned tuna market share in 2024. The deep culinary integration where tuna features in everyday dishes such as ensaladilla rusa and pipirrana is majorly propelling the domination of Spain in the European market. Spain leads Europe in seafood consumption, and canned tuna plays a major role in its food culture, owing to its affordability, pantest-friconcludely format, and tradition of consumption. The domestic market is robust with well-known companies such as Calvo and Nueva Pescanova operating modern canneries in Galicia and Andalusia that process both domestic and imported tuna loins. Spain’s food-safety authority enforces regular mercury-testing protocols for tuna products, which supports public confidence in the category. Additionally, the fishing fleet of Spain retains access to both Atlantic and Mediterranean stocks, while the industest increasingly sources certified raw material from Pacific suppliers under the EU’s IUU regulations. This combination of gastronomic tradition, regulatory overoversightand industrial capacity is majorly driving the dominance of Spain in the European canned tuna market.

Italy Canned Tuna Market Analysis

Italy held a substantial share of the European canned tuna market in 2024. The preference for high-quality olive oil-packed loins, often utilized in refined preparations like viinformo tonnato and pasta al tonno, is majorly driving the canned tuna market growth in Italy. In Italy, canned tuna remains firmly established in houtilizehold shopping habits and is supported by iconic producers such as Rio Mare and Saupiquet, which emphasise Mediterranean sourcing and traditional packing methods. In 2024, the Italian Ministest of Agricultural Policies granted Protected Geographical Indication status to “Tonno di Sciacca”, which is a yellowfin-based product from Sicily, to reinforce its regional identity and premium positioning. Italian consumers also reveal strong interest in sustainabili ty with i substantial share reporting that eco-labels and sourcing credentials influence their tuna-purchase decisions. This fusion of culinary sophistication, regulatory recognition, and ethical consumption distinguishes Italy’s market profile in the European market.

France Canned Tuna Market Analysis

France is anticipated to capture a prominent share of the European canned tuna market during the forecast period due to the value-oriented private label lines in hypermarkets and premium gourmet offerings from brands like Connétable and Petit Navire. Per capita consumption in France of canned tuna is modest but remains stable with seasonal peaks during summer salad months and Lent. French retailers have been early adopters of sustainability mandates, with some major chains requiring that their private-label tuna come from pole-and-line or free-school fisheries. The French Agency for Food, Environmental and Occupational Health & Safety (ANSES) conducts regular mercury screening of tuna products, supporting to maintain consumer confidence. Additionally, canned tuna is promoted in school canteens under the national nutrition programme as a lean protein source. This dual track of accessibility and quality is propelling the growth of the French canned tuna market.

Germany Canned Tuna Market Analysis

Germany is predicted to hold a considerable share of the Europe canned tuna market during the forecast period. Unlike Southern Europe w,, here tuna is a culinary hero. The German demand is driven by nutritional awareness and convenience. Per capita consumption of canned tuna in Germany has risen in recent years, reflecting increasing protein consciousness among fitness-oriented and flexitarian consumers. German retailers prioritize clean-label attributes with many canned tuna products packed in spring water or olive oil, as noted by the German Nutrition Society. The Federal Institute for Risk Assessment enforces rigorous contaminant monitoring, which is supporting maintain high compliance levels. Brands like John West and private-label lines from Edeka and Rewe emphasize MSC certification and recyclable packaging, aligning with national sustainability goals. This health- and environment-driven consumption model positions Germany as a growing market beyond traditional Mediterranean strongholds.

UK Canned Tuna Market Analysis

The UK is expected to exhibit a prominent CAGR in the Europe canned tuna market during the forecast period. Since Brexit, the UK market has shifted towards stronger supply-chain transparency and greater domestic brand loyalty. Consumption of canned tuna remains robust across ready-meal and salad segments. Leading British retailers such as Tesco and Sainsbury’s now require full chain-of-custody documentation for all canned tuna in alignment with UK environmental and land-management standards. National regulatory bodies report consistently high compliance with mercury-limit testing for tuna products, which supports strong safety perceptions among consumers. Additionally, UK purchaseers reveal a growing preference for lower-trophic-level tuna species such as skipjack due to concerns about environmental impact and sustainability. This combination of regulatory diligence, consumer awareness, and proactive retailer stewardship is promoting the canned tuna market growth in the UK.

COMPETITIVE LANDSCAPE

The Europe canned tuna market features a dual-tier competitive structure combining global processors with regional heritage brands. Competition revolves around sustainability credentials,, product quality,, and alignment with evolving dietary guidelines rather than price alone. Global players like Thai Union dominate volume supply through private label contracts, while European brands such as Calvo and Rio Mare command premium segments through culinary authenticity and traceability. Retailers exert significant influence by setting sourcing standards and shelf space allocation, in favor of certified and transparent suppliers. Regulatory pressures, particularly on mercury levels and IUU compliance, raise entest barriers for non-compliant importers. Meanwhile, plant-based seafood alternatives and other canned fish species create peripheral competition. Despite market maturity, innovation in packaging, nutrition,n and storyinforming sustains brand relevance. The absence of significant technological disruption ensures that trust, heritage, and sustainability remain the core axes of competition across Southern, Northern, and Eastern European sub-markets.

KEY MARKET PLAYERS

A few of the market players in the Europe canned tuna market include

- Frinsa

- Calvo Group

- Century Pacific Food Inc.

- Nestlé SA (through its Buitoni and Princes brands)

- Jealsa

- Thai Union Group PCL.

- Bumble Bee Foods, LLC.

- Grupo Calvo

- Wild Planet Foods

- Aneka Tuna Indonesia

- American Tuna

- Ocean Brands GP.

Top Players In The Market

- Calvo Group is a leading European canned tuna producer headquartered in Spain with extensive operations across the Mediterranean and Latin America. The company plays a pivotal role in the global tuna supply chain through its integrated fleet processing facilities and sustainability partnerships. In Europe, Calvo supplies both branded and private label products, emphasizing MSC certification and traceability. In early 2025, Calvo launched a new line of canned tuna packed in organic extra virgin olive oil with fully recyclable packaging, tarreceiveing premium consumers in France and Germany. It also expanded its partnership with the International Seafood Sustainability Foundation to implement 100 percent observer coverage on its chartered vessels. By combining heritage branding with environmental accountability, Calvo strengthens its position as a trusted European seafood provider.

- Nestlé leverages its Princes brand as a key player in the Europe canned tuna market, offering a wide portfolio from value to premium segments across the UK, Italy, and Germany. The company contributes globally through its commitment to responsible sourcing and innovation in ambient protein solutions. In 2024, Nestlé enhanced Princes’ sustainability credentials by achieving full Marine Stewardship Council certification for all its canned tuna sold in Europe. It also introduced a reduced-sodium range packed in spring water aligned with EU salt reduction initiatives. Nestlé’s integrated distribution network and retail partnerships ensure broad shelf presence while its R and D investments focus on clean label reformulation, reinforcing its role as aa nutrition-focutilized seafood leader.

- Thai Union Group, though headquartered in Thailand, is a dominant force in the Europe canned tuna market as the world’s largest tuna processor, supplying major retailers and brands across the continent. Its European strategy centers on sustainability, transparency, and value chain integration. In 202, Thai Union completed the rollout of its “SeaChange” sustainability program across all EU-bound products, ensuring compliance with the EU IUU Regulation and mercury limits. The company also launched a blockchain-enabled traceability pilot with Carrefour, allowing European consumers to scan QR codes for vessel and catch data. By aligning its global scale with local regulatory and ethical exexpectationsThai Union maintains a critical supply role in Europe’s canned tuna landscape.

Top Strategies Used By The Key Market Participants

Key players in the Europe canned tuna market prioritize sustainable sourcing certifications such as MSC and Dolphin Safe to meet stringent consumer and retailer expectations. They invest in premium productinnovationion including organic olive packaging and reduced-sodium formulations, and recyclable packaging to differentiate in a mature category. Companies strengthen supply chain transparency through digital traceability tools like blockchain and code, enhancing consumer trust. Strategic partnerships with European retailers for private label development ensure shelf access and volume stability. Additionally, they align product portfolios with EU public health initiatives such as salt reduction and clean label guidelines to reinforce nutritional relevance and regulatory compliance across diverse national markets.

MARKET SEGMENTATION

This research report on the Europe canned tuna market is segmented and sub-segmented into the following categories.

By Product Type

- Skipjack

- Yellowfin

- Others

By Distribution Channel Type

- Hypermarket & Supermarket

- Specialty Stores

- Online

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply