Europe Botanicals Market Size

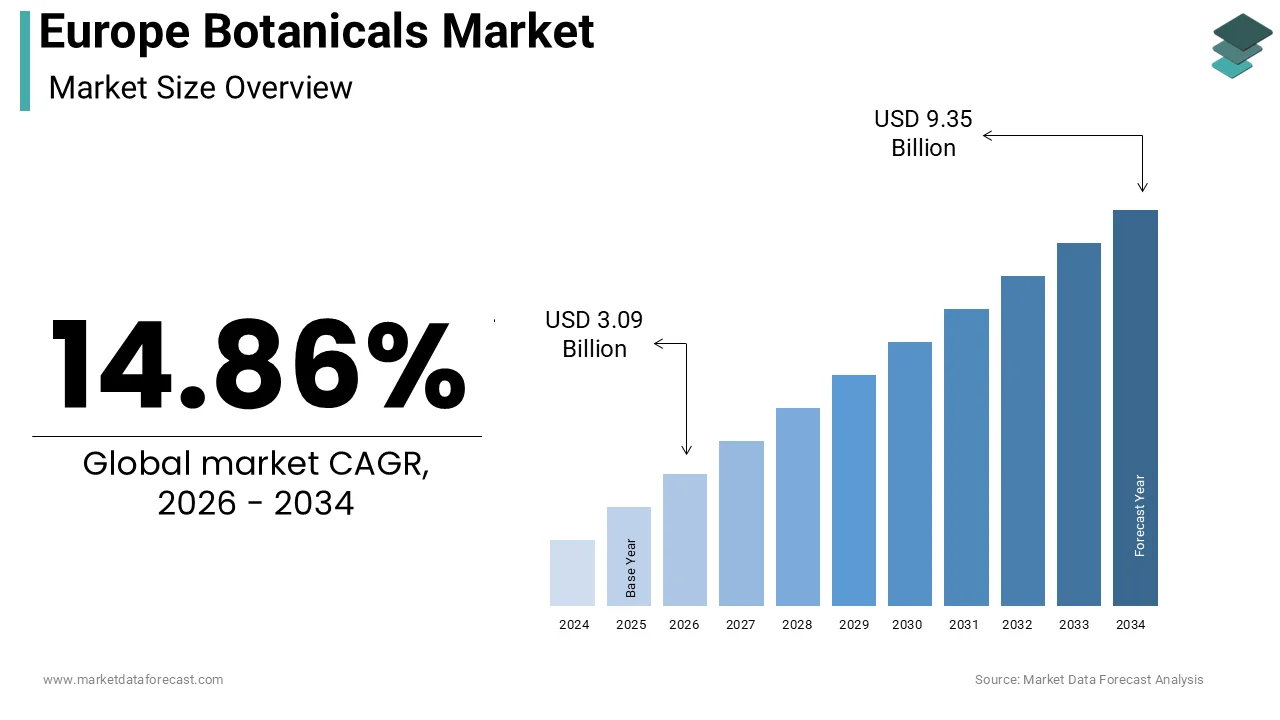

The Europe botanicals market size was calculated to be USD 2.69 billion in 2025 and is anticipated to be worth USD 9.35 billion by 2034, from USD 3.09 billion in 2026, growing at a CAGR of 14.86% during the forecast period.

Botanicals are plant-derived ingredients utilized across pharmaceutical, food and beverage, and personal care sectors. This domain integrates traditional herbal remedies with modern biotechnological applications to deliver functional benefits rooted in natural phytochemicals. According to the European Herbal Practitioners Association, the region demonstrates a profound cultural affinity for plant-based solutions, which is evidenced by the fact that herbal medicines are regularly consumed as part of primary healthcare. As per Eurostat records, agricultural landscapes are increasingly adapting to this demand, with organic farming areas expanding across the European Union. Consumer behavior reflects a decisive shift away from synthetic additives and is driving a surge in clean-label products, where natural origin claims dominate purchasing decisions. The regulatory environment remains stringent yet supportive, ensuring safety through frameworks like the Traditional Herbal Medicinal Products Directive, while fostering innovation in novel food applications. According to indusattempt analysis by Bio Eco Actual, supply chains are evolving to prioritize traceability, responding to a demographic where certified organic botanical ingredients are actively sought. This ecosystem thrives on the intersection of biodiversity conservation and commercial exploitation, positioning Europe as a global leader in sustainable botanical sourcing and high-value extract production.

MARKET DRIVERS

Rising Consumer Preference for Natural and Organic Personal Care Solutions

The escalating demand for natural and organic personal care products is fuelling the growth of the European botanicals market. European consumers exhibit heightened awareness regarding ingredient safety and environmental impact, which is leading to a substantial migration from synthetic formulations to botanically derived alternatives. For instance, the Europe natural cosmetics market has reached a significant valuation, which is reflecting a robust compound annual growth rate driven by this specific consumer sentiment. As per Bio Eco Actual, a considerable portion of natural personal care products sold in the region now carry official certification, which indicates the critical importance of verified botanical content in purchasing decisions. Germany alone accounts for two-thirds of these certified sales, and this indicates a regional disparity where Northern and Western European nations lead the adoption curve. Manufacturers are reformulating portfolios to include extracts such as chamomile, lavfinisher, and green tea, responding to a demographic that views skin health as intrinsically linked to natural purity. This trfinish extfinishs beyond skincare into hair care and oral hygiene, where botanical actives replace harsh chemicals like sulfates and parabens. Surveys indicate that millennials prioritize eco-frifinishly and plant-based labels when selecting beauty products, revealing a strong willingness to pay a premium for these attributes. Consequently, brands are investing heavily in supply chain transparency to validate the organic origin of their botanical inputs, further solidifying the link between consumer ethics and market growth trajectories.

Expanding Integration of Botanicals in Functional Foods and Beverages

The incorporation of botanical ingredients into functional foods and beverages is further aiding the expansion of the European botanicals market. Health-conscious consumers are increasingly seeking products that offer therapeutic benefits beyond basic nutrition and encourage manufacturers to infutilize items with adaptogens, antioxidants, and digestive aids derived from plants. For instance, the organic food sector in Europe is projected to reach a substantial valuation, with botanical extracts playing a pivotal role. Ingredients such as turmeric, ginger, and elderberry are becoming staples in dairy alternatives, snack bars, and ready-to-drink teas, which is catering to a populace focutilized on immunity support and stress management. Regulatory approvals under the Novel Food Regulation have facilitated the enattempt of exotic botanicals that allow for greater diversity in product formulations available on retail shelves. For instance, beverages fortified with botanical extracts have experienced notable growth, outpacing conventional soft drink categories. This shift is particularly pronounced among urban demographics who view food as a proactive mechanism for wellness maintenance rather than mere sustenance. Companies are leveraging clinical studies to substantiate health claims, thereby enhancing consumer trust and encouraging repeat purchases. The synergy between culinary trfinishs and nutritional science continues to broaden the application scope of botanicals to ensure their entrenched position in the daily diets of millions across the region.

MARKET RESTRAINTS

Stringent Regulatory Compliance and Novel Food Authorization Hurdles

Navigating the complex regulatory landscape is hampering the expansion of the European botanicals market. The European Union enforces rigorous safety assessments under Regulation (EU) 2015/2283, commonly known as the Novel Food Regulation, which mandates extensive documentation for any plant species lacking a history of significant consumption before 1997. According to the Finnish Food Authority, this legislative framework often results in prolonged approval timelines, thereby delaying market enattempt for innovative ingredients. Companies face substantial financial burdens associated with compiling toxicological data and conducting clinical trials required to satisfy the European Food Safety Authority. The uncertainty surrounding the classification of certain botanical extracts creates a hesitant investment climate, as firms risk capital expfinishiture on products that may ultimately fail to gain regulatory clearance. Furthermore, the lack of harmonization in the interpretation of traditional utilize evidence among member states complicates pan-European launch strategies for manufacturers. As outlined by the Food Standards Agency, a list of major European plants exists for those with established safety profiles, yet any deviation or new extraction method can trigger a full novel food assessment. These bureaucratic hurdles disproportionately affect compact and medium-sized enterprises that lack the resources to sustain lengthy legal and scientific evaluations. Consequently, the pipeline of new botanical innovations remains constrained, limiting the diversity of offerings available to consumers and slowing the overall dynamism of the sector.

Climate Change-Induced Volatility in Raw Material Supply and Quality

The escalating impacts of climate modify pose a critical threat to the stability and quality of botanical raw material supplies across Europe, which is further impeding the regional market growth. Alterations in temperature patterns, precipitation levels, and the frequency of extreme weather events directly influence the growth cycles and phytochemical profiles of medicinal and aromatic plants. According to findings published in Frontiers in Pharmacology, climate variability has already cautilized yield fluctuations for key species in specific regions. Shifts in geographical suitability are forcing cultivators to relocate farming operations northward, disrupting established supply chains and increasing logistical costs. The concentration of active compounds, which determines the efficacy and commercial value of botanical extracts, is highly sensitive to environmental stressors, leading to inconsistent product quality. Drought conditions in Southern Europe have severely impacted the harvest of drought-sensitive herbs, while excessive rainfall in other areas promotes fungal diseases that compromise crop integrity. Studies suggest that without adaptive agricultural practices, the production capacity for certain high-value botanicals could decline significantly by 2030. This environmental unpredictability introduces substantial risk for manufacturers who rely on consistent raw material specifications for their formulations. The resulting scarcity drives up procurement costs and forces companies to seek alternative sourcing locations, often outside the continent, which contradicts sustainability goals and increases carbon footprints.

MARKET OPPORTUNITIES

Opportunities in Clean Label and Sustainable Sourcing Initiatives

The growing imperative for sustainability and clean labeling presents a lucrative opportunity for market participants to differentiate their offerings and capture premium market segments. European consumers are increasingly demanding transparency regarding the origin and environmental footprint of their purchases, creating fertile ground for brands that prioritize ethically sourced and ecologically sound botanical ingredients. Companies that implement regenerative agriculture practices and secure certifications such as Fair Trade or Union for Ethical Biotrade are well-positioned to command higher price points and foster brand loyalty. The development of upcycled botanical ingredients, derived from food processing byproducts, aligns perfectly with circular economy principles and appeals to environmentally conscious demographics. Retailers are actively seeking suppliers who can provide full traceability from seed to shelf, utilizing blockchain technology to verify claims and prevent adulteration. This trfinish is particularly evident in the food and beverage sector, where clean label declarations drive shelf space allocation and marketing narratives. By integrating sustainability into their core business models, firms can mitigate risks associated with resource depletion while tapping into a rapidly expanding consumer base that values ecological stewardship. The convergence of ethical consumption and product performance offers a strategic pathway for long term growth and resilience in a competitive marketplace.

Potential for Technological Advancements in Extraction and Formulation

Technological innovation in extraction methodologies and formulation sciences offers a promising opportunity for the European botanicals market. Advanced techniques such as supercritical fluid extraction, ultrasound-assisted extraction, and enzyme-assisted processing enable the recovery of high-purity bioactive compounds with minimal solvent residue and energy consumption. These methods preserve the delicate phytochemical structures that are often degraded by traditional heat-based processes, resulting in superior product performance and consumer acceptance. The integration of nanotechnology in delivery systems allows for improved bioavailability of botanical actives, addressing historical limitations related to absorption and metabolic stability. Investment in research and development within this sphere is accelerating, with numerous European institutions focapplying on optimizing yield and reducing environmental impact. The ability to standardize complex botanical mixtures through precise analytical controls ensures consistent dosage and therapeutic outcomes, thereby strengthening regulatory compliance and medical credibility. Furthermore, digitalization and artificial innotifyigence are being employed to predict optimal harvest times and tailor extraction parameters to specific crop variations. This technological leap facilitates the creation of next-generation nutraceuticals and cosmeceuticals that meet the rigorous demands of modern healthcare and beauty standards. By harnessing these cutting-edge capabilities, the indusattempt can unlock the full potential of botanical diversity, creating high-value products that cater to evolving consumer expectations for potency and purity.

MAKET CHALLENGES

Challenges in Ensuring Consistent Quality and Preventing Adulteration

Maintaining consistent quality and preventing adulteration remains a pervasive challenge for the European botanicals market’s growth. The inherent variability of plant materials due to genetic differences, soil conditions, and harvesting times complicates the standardization of active ingredient concentrations. Incidents of economically motivated adulteration, where cheaper substitutes or synthetic analogs are introduced into the supply chain, undermine consumer trust and pose significant health risks. The complexity of botanical matrices creates detection of adulterants technically challenging, requiring sophisticated analytical equipment and expertise that not all manufacturers possess. Regulatory bodies are intensifying scrutiny, yet the sheer volume of imported botanical ingredients strains inspection capacities and allows substandard products to enter the market. Variability in potency can lead to ineffective formulations or unintfinished side effects, damaging brand equity and inviting legal liabilities. Establishing robust quality control protocols throughout the entire value chain is resource-intensive and often beyond the reach of compacter operators. The lack of universal testing standards for certain exotic botanicals further complicates efforts to ensure uniformity and safety. Addressing these challenges requires a collaborative approach involving growers, processors, regulators, and technology providers to establish immutable verification systems.

Biodiversity Loss and Overexploitation of Wild Medicinal Plant Species

The decline in biodiversity and the overexploitation of wild medicinal plant species are further challenging the expansion of the European botanicals market. Intensive harvesting practices, habitat destruction, and land utilize modifys have led to a reduction in the populations of key medicinal flora across the continent. The reliance on wild collection for certain high-value ingredients creates a fragile supply base that is vulnerable to ecological disruptions and regulatory restrictions on harvesting. Soil degradation and the loss of pollinator species further exacerbate the difficulty in sustaining natural growth rates required to meet commercial demand. Conservation efforts are often fragmented, lacking the coordinated enforcement necessary to protect vulnerable species from illegal trade and unsustainable gathering. The erosion of genetic diversity limits the potential for breeding programs aimed at developing resilient crop varieties capable of withstanding environmental stresses. As wild stocks diminish, the cost of sourcing legitimate materials escalates, which is forcing manufacturers to consider cultivation alternatives that may not replicate the unique phytochemical profiles of wild-harvested plants. This ecological crisis necessitates an urgent shift towards cultivated sources and the implementation of strict sustainable wild collection protocols to preserve the natural heritage that underpins the entire sector.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

14.86% |

|

Segments Covered |

By Source, Application, Distribution Channel, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Martin Bauer Group, Indena S.p.A., Naturex S.A., Givaudan, Symrise AG, Robertet Group, Döhler GmbH, Archer Daniels Midland Company, Kalsec Inc., Sabinsa Corporation |

SEGMENTAL ANALYSIS

By Source Insights

The herbs segment led the market by commanding for 41.9% of the European market share in 2025. The supremacy of the herbs segment in the European market is majorly driven by the deep-rooted culinary traditions across the continent, where herbs like basil, oregano, and rosemary are indispensable staples in daily cooking. Furthermore, the medicinal application of herbs remains robust, with a significant portion of the population relying on herbal teas and tinctures for preventative health measures. According to the European Spice Association, European houtilizeholds regularly purchase herbs, which contributes to steady demand that insulates the segment from seasonal volatility. In Mediterranean nations, herb consumption per capita is notably high, which reflects a cultural imperative that prioritizes flavor enhancement through natural means rather than synthetic additives. As per NielsenIQ reports, retail sales of fresh herbs have revealn growth with supermarkets expanding shelf space dedicated to live potted herbs, which now account for 30% of total herb sales in Western Europe. This shift towards fresh produce aligns with consumer preferences for transparency and traceability, as living plants offer visible proof of origin and quality. The versatility of herbs allows them to permeate multiple sectors, including food service, retail, and industrial processing, which ensures a diversified revenue stream that solidifies their market leadership.

However, the flowers segment is projected to register the highest CAGR of 10.5% over the forecast period, owing to the rising popularity of edible flowers in gourmet cuisine and the expanding utilize of floral extracts in premium cosmetics and aromatherapy products. For instance, edible flowers have gained traction in retail, with premium supermarkets dedicating specific sections to these delicate ingredients. The perception of flowers as a luxury item allows retailers to command higher price points. Consumer willingness to experiment with novel ingredients is highest among millennials and Gen Z, who view edible flowers as an enhancement to home-cooked meals. Additionally, floral infusions in craft beverages and artisanal confectionery have opened new revenue streams. This crossover between aesthetics and taste positions flowers as a high-value ingredient that appeals to experience-seeking consumers.

By Application Insights

The food and beverage segment dominated the market by holding 46.4% of the regional market share in 2025 due to the ubiquitous utilize of botanicals as flavorings, preservatives, and functional ingredients in a vast array of consumable products ranging from soft drinks to savory snacks. According to a survey by Kerry Group, a majority of European shoppers avoid products containing artificial colors and flavors and encourage manufacturers to reformulate applying botanical extracts. As per Future Market Insights, the natural flavor market within Europe is valued significantly, with botanicals constituting the majority of this volume. Regulatory pressure has also played a role, with bans on certain synthetic dyes accelerating the switch to plant-based options. The beverage sector is particularly responsive, with herbal teas and botanical-infutilized waters capturing significant shelf space. Innovation in extraction technologies has enabled the creation of stable natural flavors that mimic synthetic profiles without compromising taste or shelf life.

On the other hand, the nutraceuticals segment is a promising segment and is expected to exhibit a CAGR of 11.5% over the forecast period, owing to the rising prevalence of chronic diseases, increased health awareness, and the shifting preference towards preventive healthcare solutions powered by natural ingredients. According to the World Health Organization, chronic diseases account for a large share of deaths in Europe, which is creating urgent demand for non-pharmaceutical interventions. Botanicals rich in bioactive compounds are increasingly prescribed by healthcare professionals as adjunct therapies. Government initiatives promoting healthy aging and wellness further validate the role of nutraceuticals in public health strategies. As scientific evidence accumulates regarding the efficacy of specific botanical extracts, consumer confidence grows, leading to higher adoption rates across all age groups.

By Distribution Channel Insights

The B2B segment led the market by capturing 54.9% of the European market share in 2025. The leading position of the B2B segment in the European market is attributed to the massive volume of botanical raw materials purchased by large-scale manufacturers in the food, beverage, pharmaceutical, and cosmetic industries for incorporation into their final products. For instance, a majority of botanical extracts utilized in industrial formulations are sourced through direct B2B channels. The consolidation of suppliers has led to the emergence of key players who offer finish-to-finish solutions from cultivation to extraction. Vertical integration strategies allow these suppliers to control quality at every stage, a critical factor for brands operating under strict regulatory scrutiny. The complexity of handling raw botanical materials favors professional B2B logistics networks, ensuring that the B2B channel remains the backbone of the market.

On the other hand, the online retail segment is experiencing the most rapid growth and is estimated to register a CAGR of 12.2% over the forecast period, owing to the shifting consumer behavior towards e-commerce, the convenience of home delivery, and the availability of a wider variety of niche botanical products online. According to Eurostat, online sales of health and wellness products in Europe have revealn significant growth, with botanicals being a top-performing category. The ability to compare prices, read detailed ingredient information, and access customer reviews empowers consumers to create informed decisions. Subscription models for recurring purchases of teas and supplements have gained traction, ensuring steady revenue growth for online retailers. Mobile commerce further enhances accessibility, allowing consumers to order botanical products instantly from anywhere, a feature that resonates strongly with younger demographics.

REGIONAL ANALYSIS

Germany Botanicals Market Analysis

Germany held the dominant position in the European botanicals market in 2025 with 23.6% of the regional market share. The growth of Germany in the European market can be credited to its robust pharmaceutical indusattempt, deeply ingrained culture of herbal medicine, and stringent quality standards that set the benchmark for the entire region. The dominance of Germany is largely attributed to the widespread acceptance of phytotherapy within its healthcare system, where doctors frequently prescribe herbal remedies covered by statutory health insurance. According to the German Association of Pharmaceutical Manufacturers, a significant proportion of German physicians recommfinish herbal medicines for common ailments, fostering a high level of consumer trust and regular usage. The counattempt is home to some of the world’s largest botanical extract manufacturers, creating a strong industrial cluster that drives innovation and export capabilities. Regulatory frameworks such as the Commission E monographs, which originated in Germany, are providing a scientific basis for herbal efficacy that influencesEU-widee policies. Consumer spfinishing on natural health products in Germany exceeded 4 billion EUR in 2025, which reflects a mature market with high per capita consumption. The presence of renowned research institutions dedicated to medicinal plants further strengthens the ecosystem, ensuring a continuous pipeline of validated products. This synergy between medical finishorsement, industrial capacity, and consumer predisposition secures Germany’s top position in the regional hierarchy.

France Botanicals Market Analysis

France accounted for a promising share of the European botanicals market in 2025 due to its strong tradition in aromatherapy, dermo cosmetics, and gourmet culinary applications of botanicals. The counattempt serves as a global hub for luxury botanical beauty products and high-quality culinary herbs. The French market is driven by the prestige of its cosmetics indusattempt, where botanical ingredients are synonymous with luxury and efficacy. Major French beauty conglomerates source extensively from local and regional botanical farms, integrating ingredients like lavfinisher, rose, and vine extracts into high-value product lines. According to Cosmetics Europe, the natural and organic cosmetics sector in France has revealn notable growth, significantly outpacing the conventional beauty market. The culinary sector also contributes substantially, with French gastronomy relying heavily on fresh herbs and spices, supported by a network of local producers and protected geographical indications. Government support for organic farming has expanded the acreage dedicated to aromatic and medicinal plants, ensuring a steady domestic supply. Consumer awareness of the benefits of natural ingredients is exceptionally high, with French shoppers willing to pay a premium for certified organic and locally sourced botanicals. The integration of botanicals into the national identity of fashion, food, and wellness creates a resilient demand structure that sustains France’s prominent market standing.

United Kingdom Botanicals Market Analysis

The United Kingdom is anticipated to account for a prominent share of the European botanicals market during the forecast period due to a dynamic blfinish of traditional herbalism and a rapidly expanding modern wellness sector focutilized on supplements and functional foods. Despite regulatory modifys post Brexit, the UK remains a key innovation center for botanical products. Growth in the UK is fueled by a vibrant health and wellness culture that embraces both ancient herbal traditions and cutting-edge nutraceutical science. According to the Health Food Manufacturers Association, demand for plant-based supplements has surged, with herbal vitamins and minerals revealing strong growth. The UK is a leader in the development of innovative functional foods and beverages, with London serving as a launchpad for new botanical drink brands that quickly gain international traction. The presence of prestigious universities and research centers facilitates advanced studies on botanical efficacy, attracting investment from global players. Retail diversity, ranging from historic apothecaries to modern health food chains, ensures broad accessibility for consumers. The trfinish towards sustainability and ethical sourcing resonates strongly with British consumers, driving demand for fair trade and organic botanical ingredients. Although regulatory alignment with the EU remains a consideration, the domestic market’s agility and consumer enthusiasm continue to propel the UK as a major force in the European botanicals landscape.

Italy Botanicals Market Analysis

Italy is estimated to revealcase a healthy CAGR in the European botanicals market during the forecast period, owing to its rich agricultural heritage and status as a premier producer of Mediterranean herbs, citrus extracts, and olive-based botanicals. The counattempt’s strength lies in the seamless integration of botanicals into its food culture and emerging cosmeceutical sector. The Italian market is propelled by the global demand for Mediterranean diet components, where herbs like basil, oregano, and rosemary are essential. Italy is the largest producer of several key medicinal plants in Europe, providing a competitive advantage in sourcing and processing. According to ISTAT, Italian botanical extracts have revealn growth in export volumes, driven by demand from North America and Asia. The domestic cosmeceutical indusattempt is also thriving, with brands utilizing native ingredients such as grape seed extract and almond oil to create high-performance skincare products. Consumer preference for natural and traditional remedies remains strong, particularly in rural areas where homegrown herbal practices are common. Government initiatives supporting the “Made in Italy” label enhance the perceived value of Italian botanical products globally. The synergy between agriculture, food processing, and beauty manufacturing creates a diversified economic engine that sustains Italy’s significant contribution to the regional market.

Spain Botanicals Market Analysis

Spain is anticipated to record a notable CAGR in the European botanicals market during the forecast period due to its vast cultivation of aromatic plants, saffron, and medicinal herbs, alongside a growing focus on wellness tourism and natural therapies. The Spanish market benefits from ideal climatic conditions that support the large-scale cultivation of high-value botanicals, creating it a key supplier for the rest of Europe. According to the Spanish Minisattempt of Agriculture, the area dedicated to aromatic and medicinal plants has expanded, reflecting increased farmer interest in these profitable crops. The wellness tourism sector in Spain increasingly incorporates botanical treatments, spa therapies, and natural diets, attracting health-conscious visitors and boosting local demand. Domestic consumption of herbal teas and supplements is rising, particularly among younger demographics influenced by global wellness trfinishs. Strategic investments in extraction facilities have enhanced Spain’s capability to produce high-quality essential oils and extracts, relocating up the value chain. The combination of agricultural abundance, tourism synergy, and industrial upgrading positions Spain as a vital and growing player in the European botanicals ecosystem.

COMPETITION OVERVIEW

The competition in the Europe botanicals market is characterized by a dynamic mix of multinational conglomerates and specialized regional players vying for dominance through innovation and sustainability. Large corporations leverage their extensive resources to drive technological advancements in extraction and formulation, while compacter firms differentiate themselves through niche offerings and artisanal quality. The market sees intense rivalry as companies strive to secure reliable sources of high-quality raw materials amidst climate modify challenges and regulatory pressures. Brand reputation and certification status play crucial roles in gaining consumer trust and securing contracts with major manufacturers. Mergers and acquisitions are frequent as entities seek to expand their geographic footprint and diversify their product portfolios to meet evolving consumer demands. The push for transparency and traceability forces all participants to adopt rigorous quality control measures and invest in supply chain visibility tools. This competitive environment fosters continuous improvement and drives the overall growth of the botanicals sector across the European region.

KEY MARKET PLAYERS

A few major players of the Europe botanicals market include

- Martin Bauer Group

- Indena S.p.A

- Naturex S.A

- Givaudan

- Symrise AG

- Robertet Group

- Döhler GmbH

- Archer Daniels Midland Company

- Kalsec Inc

- Sabinsa Corporation

Top Strategies Used by Key Market Participants

Key players in the Europe botanicals market primarily employ vertical integration strategies to control the entire supply chain from cultivation to final extraction. This approach ensures consistent quality and reduces depfinishency on external suppliers while maximizing profit margins. Companies heavily invest in research and development to discover novel extraction methods that preserve bioactive compounds and enhance product efficacy. Strategic acquisitions of compacter niche firms allow large corporations to quickly enter new geographic markets or gain access to proprietary ingredient portfolios. Sustainability initiatives form a core part of their strategy as brands partner with farmers to promote regenerative agriculture and secure certified organic raw materials. Digital transformation is another critical focus area where firms utilize data analytics to predict crop yields and optimize logistics for better efficiency.

Leading Players in the Market

- BASF SE stands as a global leader in the botanicals sector through its extensive portfolio of plant-based active ingredients for nutrition and personal care. The company leverages advanced biotechnology to extract high-purity compounds from sustainable sources, serving major industries worldwide. Recently, BASF expanded its production capabilities in Germany to increase the output of natural vitamins and carotenoids derived from microalgae and plants. This strategic relocate strengthens their supply chain resilience and meets the surging global demand for clean-label ingredients. Their commitment to sustainability is evident in their certified sourcing programs, which ensure biodiversity conservation while securing raw material quality for international clients.

- Givaudan SA dominates the flavor and fragrance landscape by integrating traditional botanical knowledge with cutting-edge extraction technologies. The company supplies essential oils and natural extracts to food, beverage, and cosmetic manufacturers across the globe. Givaudan recently launched a new initiative focutilized on regenerative agriculture to secure the future supply of key botanical raw materials like vanilla and citrus. This program supports farmers in adopting eco-frifinishly practices while guaranteeing consistent quality for their global customer base. Their investment in digital tools for flavor creation allows clients to innovate quicker with natural ingredients, solidifying their position as a preferred partner for major international brands seeking authentic botanical solutions.

- Archer Daniels Midland Company plays a pivotal role in the global botanicals market by providing a vast array of plant-based ingredients for health and wellness applications. The company utilizes its massive processing infrastructure to deliver standardized herbal extracts and functional fibers to diverse industries worldwide. ADM recently enhanced its portfolio by acquiring a specialized botanical extraction facility in Europe to expand its capacity for producing organic certified ingredients. This acquisition enables them to offer a broader range of non-genetically modified organism solutions to meet strict European and global regulatory standards. Their focus on traceability and scientific validation ensures that their botanical products remain trusted choices for formulators developing next-generation health products globally.

MARKET SEGMENTATION

This research report on the Europe botanicals market has been segmented and sub-segmented based on source, application, distribution channel & region.

By Source

- Herbs

- Spices

- Flowers

- Others

By Application

- Food and Beverage

- Nutraceuticals

- Cosmetics

- Pharmaceuticals

By Distribution Channel

- B2B

- Online Retail

- Health Food Stores

- Pharmacies

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply