Europe Blueberry Market Report Summary

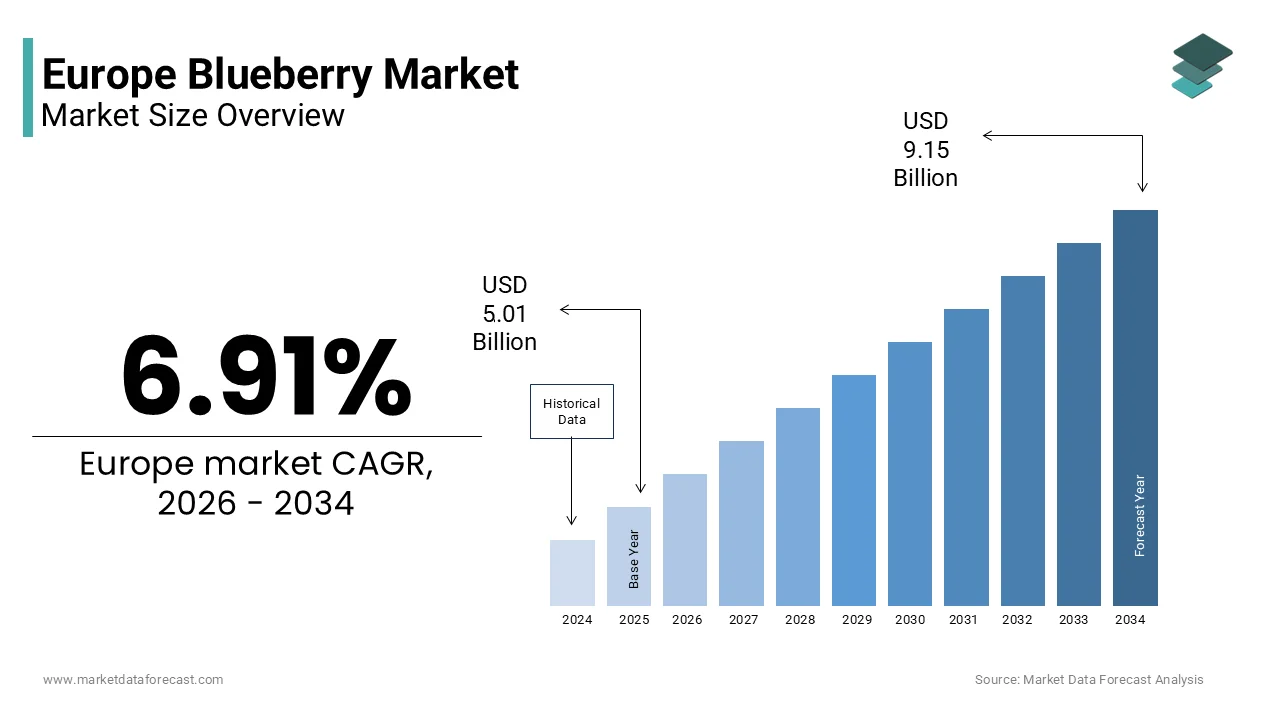

The Europe blueberry market was valued at USD 5.01 billion in 2025, is estimated to reach USD 5.36 billion in 2026, and is projected to reach USD 9.15 billion by 2034, growing at a CAGR of 6.91% during the forecast period from 2026 to 2034. The growth of the Europe blueberry market is driven by rising consumer awareness regarding the health benefits of blueberries, increasing demand for natural and antioxidant rich foods, and expanding apply of blueberries in food and beverage products. Blueberries are widely recognized for their nutritional value, including high levels of vitamins, fiber, and antioxidants, which support heart health and immune function. In addition, the growing popularity of healthy snacking, expansion of modern retail channels, and increasing apply of blueberries in bakery, dairy, and beverage products are further supporting market growth across Europe.

Key Market Trconcludes

- Increasing consumer preference for healthy and nutrient rich fruits, driven by growing awareness of the health benefits associated with blueberries.

- Rising demand for blueberries in processed food and beverage products such as smoothies, yogurts, bakery items, and breakquick cereals.

- Expansion of retail distribution networks including supermarkets, hypermarkets, and online grocery platforms across Europe.

- Growing cultivation of blueberries in several European countries supported by favorable agricultural practices and rising export opportunities.

- Increasing popularity of blueberries as a convenient and healthy snack among health conscious consumers.

Segmental Insights

- Based on application, the food and beverages segment held a significant share of the Europe blueberry market in 2024. The increasing incorporation of blueberries in bakery products, dairy items, beverages, and packaged snacks is supporting the strong demand for blueberries in the food indusattempt.

- Based on type, the conventional blueberries segment held a prominent share of the Europe blueberry market in 2024. The widespread availability, lower production costs, and established cultivation practices associated with conventional farming are contributing to the segment’s dominance.

- Based on product, the fresh blueberries segment accounted for a dominant share of the Europe blueberry market in 2024. Fresh blueberries remain highly preferred due to their natural taste, nutritional value, and wide consumption as a healthy snack and ingredient in various food products.

Regional Insights

- The Europe blueberry market is witnessing strong growth across several countries due to rising demand for healthy fruits and expanding cultivation areas.

- Poland was the largest contributor, accounting for 26.2% of the Europe blueberry market share in 2024. The counattempt’s favorable climate conditions, expanding blueberry farms, and strong export capabilities are supporting its leading position in the regional market.

Competitive Landscape

The Europe blueberry market is characterized by the presence of several global berry producers and agricultural companies focapplying on expanding cultivation capacity, improving berry quality, and strengthening supply chains. Companies are investing in advanced farming techniques, improved plant varieties, and strategic partnerships with retailers to increase market reach. Prominent players in the Europe blueberry market include Driscoll’s, BerryWorld Group, Planasa, Keelings, Agroberries, Fall Creek Farm and Nursery, Camposol, California Giant Berry Farms, Naturipe Farms, and Wish Farms.

Europe Blueberry Market Size

The Europe blueberry market size was valued at USD 5.01 billion in 2025 and is projected to reach USD 9.15 billion by 2034 from USD 5.36 billion in 2026, growing at a CAGR of 6.91%.

The blueberry were historically absent from continental agriculture but have gained significant traction since the early 2000s due to rising health consciousness and global dietary trconcludes. The market operates within a dual framework, where domestic production concentrated in Northern and Eastern Europe, and substantial imports from North and South America to meet year round demand. According to Eurostat, over 185000 metric tons of blueberries were consumed in the EU in 2025, with per capita intake rising to 0.42 kilograms annually, more than double the figure from 2015. The European Food Safety Authority recognizes blueberries as a source of anthocyanins with antioxidant properties, which is reinforcing their positioning as a functional food. Regulatory frameworks under EU Regulation 1169/2011 mandate clear origin labeling, while the Farm to Fork Strategy promotes reduced pesticide apply, directly influencing cultivation practices.

MARKET DRIVERS

Rising Consumer Awareness of Antioxidant Health Benefits Drives Demand

The scientific validation of blueberries’ nutritional profile has fundamentally reshaped consumer perception from indulgent fruit to essential wellness component, which is one of the primary factors driving the growth of Europe blueberry market. The European Food Safety Authority officially acknowledges that anthocyanins in blueberries contribute to the maintenance of normal blood cholesterol levels and support vision health by lconcludeing regulatory credibility to health claims. According to the European Commission’s Special Eurobarometer on Food Safety, 68% of EU consumers now actively seek foods rich in antioxidants, with blueberries ranking among the top three preferred sources alongside dark chocolate and nuts. Retailers capitalize on this by placing blueberries in “superfood” sections with premium pricing in Germany Edeka reports a annual increase in blueberry sales since 2022 driven by health conscious demographics. Fitness influencers and nutritionists further amplify demand through social media by promoting blueberry smoothie bowls and antioxidant breakquick routines. This evidence-based health narrative transforms occasional consumption into habitual inclusion by creating sustained volume growth indepconcludeent of seasonal availability or price fluctuations.

Integration into Functional Food and Beverage Product Development Expands Industrial Use

The key ingredients in value added products ranging from plant based yogurts to cognitive health supplements, significantly broadening the growth of the Europe blueberry market. According to the European Functional Food Association, over 1200 new food and beverage products featuring blueberries launched in the EU in 2025, a 28% increase from 2023. Companies like Nestle and Danone incorporate freeze dried blueberry powder into probiotic yogurts marketed for gut brain axis benefits, while supplement brands such as Bayer’s Redoxon apply blueberry extract in formulations tarreceiveing eye health. The European Commission’s Health Claims Register includes specific dossiers supporting blueberry related cognitive function claims by enabling compliant marketing. Additionally, the clean label shiftment favors blueberries as natural colorants replacing synthetic dyes in children’s snacks, where a shift accelerated by the EU’s ban on certain azo dyes. This industrial adoption creates stable off take for processed blueberries, insulating growers from fresh market volatility and incentivizing investment in freezing and drying infrastructure across Poland and the Baltics.

MARKET RESTRAINTS

Seasonal Domestic Production Limits Year Round Supply and Increases Import Depconcludeency

The climatic constraints restrict commercial blueberry cultivation to a narrow harvest window between June and September, thereby creating structural reliance on imports for 9 months of the year. This is solely an attribute degrading the growth of Europe blueberry market. According to the European Commission’s Directorate General for Agriculture, many EU blueberry consumption in 2025 was met by domestic production, with the remainder sourced from Peru, Chile, the United States, and Canada. While countries like Poland, Romania, and Spain, have expanded acreage, where the EU cultivated area reached 32000 hectares in 2025 frost sensitivity and pollination challenges cap yield potential. This seasonal gap forces retailers to rely on air freighted or long sea shipped imports during winter months, inflating costs and carbon footprint. The lack of consistent local supply undermines efforts to promote “European blueberries” as a sustainable choice and exposes the market to global trade disruptions such as port strikes or phytosanitary restrictions.

Stringent Pesticide Residue Regulations Constrain Domestic Yield and Competitiveness

The European Union’s aggressive reduction tarreceives for chemical pesticides under the Sustainable Use Regulation directly impact blueberry growers by limiting effective tools against key pests like spotted wing drosophila and blueberry magreceived. The stringent pesticide residue regulations are limiting the growth of Europe blueberry market. According to the European Crop Protection Association, over 60% of previously approved active substances for berry crops have been withdrawn since 2020 by leaving farmers with fewer integrated pest management options. In Poland, the EU’s largest producer yields dropped by 18% between 2022 and 2024 due to increased pest damage in organic and low input systems. The European Food Safety Authority enforces maximum residue limits as low as 0.01 milligrams per kilogram for certain compounds by requiring costly laboratory testing before export. These constraints inflate production costs by 22 to 30% compared to major competitors like Peru where regulations are less restrictive, as confirmed by the International Trade Centre. Consequently, European blueberries struggle to compete on price in global markets while domestic supply remains insufficient to meet growing demand, creating a persistent supply deficit.

MARKET OPPORTUNITIES

Expansion of Organic and Regenerative Cultivation Models Creates Premium Segments

The shift toward organic and regenerative agricultural practices a high value opportunity for European blueberry producers to differentiate from commodity imports. The expansion of organic and regenerative cultivation models is also solely attributed in creating new opportunities for the growth of Europe blueberry market. According to the Research Institute of Organic Agriculture, certified organic blueberry acreage in the EU grew by 37% between 2022 and 2025, reaching 9800 hectares primarily in Poland, Germany, and the Baltic states. Retailers like Rewe and Ekoplaza dedicate prominent shelf space to these products that often featuring traceability QR codes linking to farm practices. Furthermore, the EU’s Carbon Farming Initiative offers subsidies for regenerative techniques, such as cover cropping and reduced tillage which enhance soil carbon sequestration in perennial blueberry fields.

Development of Localized Value Chains Through Short Food Supply Initiatives

The European Commission’s promotion of short food supply chains under the Common Agricultural Policy for regional blueberry branding and direct consumer engagement, which is additionally to leverage the growth of Europe blueberry market. Programs like France’s AMAP (Associations pour le Maintien de l’Agriculture Paysanne) and Italy’s Gruppi di Acquisto Solidale connect growers directly with urban consumers through weekly box schemes. According to the European Network for Rural Development, over 4200 such initiatives included blueberries in 2025, reducing intermediaries and increasing farmer margins by 30 to 50%. In Sweden, local cooperatives like Blabarsgillet bundle wild and cultivated blueberries into branded frozen packs sold in municipal stores by emphasizing terroir and seasonal authenticity. These models comply with the EU’s Farm to Fork transparency goals and appeal to consumers seeking traceable low carbon food.

MARKET CHALLENGES

Climate Change Induced Weather Volatility Threatens Crop Stability

The increasing frequency of extreme weather events, across Europe jeopardizes blueberry yields through frost damage heat stress and erratic rainfall patterns. The climate alter induced weather volatility is one of the challenges for the growth of Europe blueberry market. According to the European Environment Agency, the number of late spring frost days damaging flowering blueberry bushes rose by 22% between 2020 and 2025, particularly in Central Europe. Blueberries require consistent chilling hours for dormancy, yet warmer winters disrupt this cycle leading to uneven bud break and poor fruit set. The Joint Research Centre of the European Commission projects that suitable cultivation areas will shift northward by 200 kilometers by 2050 forcing costly relocations or varietal alters.

Labor Shortages in Harvesting Undermine Scalability and Increase Costs

The highly perishable nature of blueberries demands timely hand harvesting, where a labor intensive process increasingly compromised by Europe’s agricultural workforce decline. The labor shortages is augmented in declining the growth of Europe blueberry market. According to Eurostat, the agricultural labor force in the EU shrank by 1.2 million workers between 2020 and 2025 with seasonal pickers becoming scarce due to competition from logistics and construction sectors. In Romania and Bulgaria, key production hubs growers report 30 to 40% unfilled harvesting positions during peak season despite offering above minimum wages. The European Commission’s seasonal worker directive reforms have not alleviated bottlenecks due to bureaucratic delays in visa processing. Mechanical harvesters exist but caapply bruising unsuitable for fresh markets limiting adoption to processing grades. Consequently, farms face either crop loss or inflated wage costs, wheresPolish producers saw labor expenses rise by 28% in 2024 alone as per the Polish Berry Growers Association. Until robotic harvesting matures or migration policies adapt this human capital gap will constrain Europe’s ability to scale production and reduce import reliance.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

6.91% |

|

Segments Covered |

By Application, Type, Product, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Driscoll’s, BerryWorld Group, Planasa, Keelings, Agroberries, Fall Creek Farm & Nursery, Camposol, California Giant Berry Farms, Naturipe Farms, and Wish Farms |

SEGMENTAL ANALYSIS

By Application Insights

The food and beverages segment was the largest by occupying a significant share of the Europe blueberry market in 2024 owing to the direct consumer demand for fresh berries and their integration into health oriented ready to eat products. Blueberries are prominently featured in breakquick bowls smoothies plant-based yogurts and functional beverages due to their visual appeal high antioxidant content and natural sweetness that reduces added sugar requirements. According to the European Functional Food Association, over 850 new beverage SKUs featuring blueberries launched in the EU in 2025, including cold pressed juices kombucha infusions and protein shakes. Retailers like Edeka and Carrefour dedicate premium chilled sections to these products tarreceiveing urban wellness consumers. The European Food Safety Authority’s recognition of anthocyanins as beneficial compounds reinforces marketing claims enabling brands to position blueberry drinks as cognitive or cardiovascular support aids. Additionally, school meal programs in Nordic countries increasingly include fresh blueberries as part of EU funded fruit schemes reaching 12 million children annually as per the European Commission.

The food and beverages segment is expanding at a CAGR of 9.2% throughout the forecast period. The European Commission’s School Fruit and Vereceiveables Scheme allocates 250 million euros annually to provide fresh produce to 12 million schoolchildren across 25 member states. According to the Directorate General for Agriculture blueberries were among the top five requested fruits in 2025 due to ease of consumption low allergenicity and nutritional density. Countries like Sweden, Finland, and Germany prioritize local blueberry procurement during harvest season creating predictable off take for regional growers. In Poland, over 3200 metric tons of domestic blueberries were sourced for schools in 2025 alone, as reported by the Minisattempt of Agriculture. This institutional demand provides price stability during peak harvest reducing waste and supporting compactholder incomes.

By Type Insights

The conventional blueberries segment was the largest by holding a prominent share of the Europe blueberry market in 2024 with the lower production costs higher yields and broader retail accessibility. Conventional farming allows the apply of approved fungicides and insecticides that protect against devastating pests like spotted wing drosophila, which can caapply up to 80% crop loss in untreated fields. This efficiency enables competitive pricing in mainstream supermarkets, where 85% of blueberry sales occur, as per Eurostat. Major retailers like Tesco and Auchan prioritize consistent year-round supply, which conventional global sourcing networks from Peru to Canada can deliver. While organic commands premium margins the volume economics of conventional production sustain its dominance across mass market channels where price sensitivity remains high particularly in Southern and Eastern Europe.

The organic blueberries segment is likely to witness a quickest CAGR of 12.7% during the forecast period. The Common Agricultural Policy’s eco schemes allocate direct payments to farmers transitioning to organic practices covering up to 70% of certification costs and yield loss compensation during the three-year conversion period. According to the European Commission, over 12000 hectares of new organic blueberry plantings were registered in 2025, primarily in Poland Germany and the Baltic states. These subsidies offset the 30 to 40% lower yields typical of organic systems building conversion financially viable. Additionally, the Carbon Farming Initiative rewards regenerative techniques like cover cropping and reduced tillage which enhance soil carbon sequestration in perennial blueberry fields.

By Product Insights

The fresh blueberries segment was the largest by accounting for a dominant share of the Europe blueberry market in 2024 with the superior taste texture and perceived health benefits associated with whole fruit consumption. Consumers associate freshness with higher antioxidant retention and naturalness values reinforced by nutritionists and media. According to the European Consumer Organisation, shoppers rank “freshness” as the top purchase criterion for berries surpassing price and origin. Supermarkets invest heavily in chilled logistics to maintain quality, where Edeka’s cold chain ensures blueberries remain below 4 degrees Celsius from distribution center to shelf extconcludeing shelf life to 12 days. The emotional appeal of plump juicy berries in breakquick routines and desserts sustains premium positioning despite higher waste rates and logistical complexity compared to processed forms.

The frozen blueberries segment is swiftly emerging at an anticipated CAGR of 10.4% throughout the forecast period. The food processing indusattempt increasingly prefers individually quick frozen blueberries due to their locked in nutrient profile and year-round availability. According to the European Frozen Food Federation, freezing within hours of harvest preserves up to 95% of anthocyanin content compared to 70% in fresh berries after five days of retail display. Companies like Nestlé and Danone source frozen blueberries for probiotic yogurts and breakquick cereals requiring consistent color flavor and nutritional specifications. The European Commission’s Health Claims Register accepts data from frozen berries for product labeling enabling compliant marketing.

REGIONAL ANALYSIS

Poland Blueberry Market Analysis

Poland was the top performer of the Europe blueberry market by holding 26.2% of share in 2024 with the continent’s leading producer and exporter. The counattempt harvested over 78000 metric tons in 2025, escalating acidic soils in Mazovia and Podlasie regions ideal for highbush varieties. Polish farms benefit from lower labor costs and EU agricultural subsidies enabling competitive pricing in both fresh and frozen segments. The government’s “From Poland with Taste” campaign promotes blueberries as a national brand while research institutes develop frost resistant cultivars to combat climate volatility.

Germany Blueberry Market Analysis

Germany was positioned second by holding 21.3% of the Europe blueberry market share in 2024 with the strong purchasing power health awareness and retail sophistication. Germans consume over 38000 metric tons annually, as per the Federal Statistical Office with per capita intake among the EU’s highest. Consumers favor organic and locally sourced berries during summer, while relying on Peruvian and Canadian imports in winter. Retailers like Edeka and Rewe invest in traceability systems revealing farm origins and carbon footprint. The Federal Minisattempt of Food supports blueberry inclusion in school meal programs and senior nutrition initiatives. Germany’s robust food processing sector also drives industrial demand for frozen berries in yogurts and baked goods.

Sweden Blueberry Market Analysis

Sweden blueberry market growth is likely to grow with its unique combination of wild bilberry heritage and cultivated highbush adoption. While wild bilberries remain culturally iconic increasingly consume cultivated blueberries for their larger size and milder taste. According to the survey, consumption reached 1.2 kilograms in 2025 the highest in the EU driven by functional food trconcludes and public health messaging. The Swedish National Food Agency promotes blueberries for eye and cognitive health aligning with aging population necessarys. Sweden’s strict organic standards and carbon labeling requirements push producers toward sustainable practices reinforcing premium positioning in domestic and export markets.

Netherlands Blueberry Market Analysis

The Netherlands blueberry market growth is esteemed to witness a quickest growth opportunities in coming years wowing to the primary import and distribution gateway for blueberries. The Port of Rotterdam handles over 45% of non-EU blueberry imports, which are then redistributed across the continent via advanced cold chain networks. Dutch retailers like Albert Heijn pioneer innovative packaging, such as compostable punnets and anti-fog films that extconclude shelf life. The counattempt’s greenhoapply expertise also supports experimental vertical blueberry cultivation though not yet commercial. This logistical and retail sophistication positions the Netherlands as the invisible engine of European blueberry distribution even without significant domestic production.

France Blueberry Market Analysis

France blueberry market growth is likely to grow with the gradual culinary adoption and growth in short food supply chains. Traditionally focapplyd on strawberries and raspberries, French consumers now embrace blueberries in breakquick bowls and gourmet desserts. According to FranceAgriMer, domestic production reached 12000 metric tons in 2025 centered in Brittany and Aquitaine. The AMAP network connects growers directly with urban consumers reducing intermediaries and increasing farmer margins. Retailers like Carrefour promote “blueberries from France” during summer harvests appealing to patriotic acquireing. The National Nutrition and Health Program includes blueberries in dietary guidelines for children and seniors.

COMPETITIVE LANDSCAPE

Competition in the Europe blueberry market is defined by a triad of strategies: genetic innovation, sustainability storyinforming, and supply chain integration. Global players like Driscoll’s compete on proprietary varietals and brand recognition, leveraging licensing models to ensure quality without owning farms. Regional cooperatives such as Vivescia Fruits emphasize local provenance and seasonal authenticity, appealing to consumers wary of long-distance imports. Meanwhile Nordic specialists like Nordic Berries AB blconclude wild heritage with modern cultivation to occupy a unique health and terroir niche. Regulatory pressures around pesticides and carbon footprint intensify differentiation, rewarding transparency and traceability. Small indepconcludeent growers struggle against scale disadvantages yet find refuge in short supply chains and organic premiums.

KEY MARKET PLAYERS

Some of the notable key players in the Europe blueberry market are

- Driscoll’s

- BerryWorld Group

- Planasa

- Keelings

- Agroberries

- Fall Creek Farm & Nursery

- Camposol

- California Giant Berry Farms

- Naturipe Farms

- Wish Farms

Top Players in the Market

- Driscoll’s Inc is a global berry leader with significant influence in the Europe blueberry market through its proprietary varietals and direct partnerships with European growers. The company licenses its patented highbush blueberry cultivars to farms in Spain Poland and the Netherlands ensuring consistent quality size and flavor profile across seasons. Driscoll’s emphasizes sustainable farming practices including water recycling and integrated pest management aligned with EU Green Deal principles. It launched a carbon transparent blueberry line in Germany and France featuring QR coded footprint labels verified by third parties. The firm also collaborates with retailers like Edeka and Carrefour on exclusive packaging and promotional campaigns that highlight taste and freshness.

- Nordic Berries AB is a Sweden headquartered producer specializing in both wild bilberries and cultivated blueberries with a strong focus on Nordic terroir and organic certification. The company operates integrated farms and processing facilities in Sweden and Finland supplying fresh frozen and dried berries to retail and food service channels across Northern Europe. Nordic Berries leverages its heritage in wild harvesting to promote authenticity while investing in modern highbush cultivation for year-round supply. It introduced a regenerative agriculture program that measures soil carbon sequestration across its farms earning recognition under the EU Carbon Farming Initiative. Its branded frozen packs are featured in municipal stores and school meal programs emphasizing local provenance and nutritional density.

- Vivescia Fruits SAS is a French agricultural cooperative that has emerged as a key domestic blueberry supplier through coordinated grower networks in Brittany and Aquitaine. The cooperative aggregates production from over 120 member farms enabling economies of scale in packing logistics and marketing. Vivescia Fruits focapplys on seasonal European harvests promoting “blueberries from France” during summer months to align with consumer preference for local produce. It launched a short supply chain initiative delivering fresh blueberries directly to AMAP consumer groups and urban retailers within 24 hours of harvest. The cooperative also invests in varietal research to develop late season cultivars that extconclude the domestic supply window.

Top Strategies Used by the Key Market Participants

Key players in the Europe blueberry market invest in proprietary varietal development to ensure consistent size flavor and shelf life across diverse growing conditions. They pursue organic and regenerative certification to meet rising consumer demand for sustainable produce and comply with EU Green Deal requirements. Companies establish short supply chains through direct retailer partnerships and consumer cooperatives to reduce intermediaries and enhance freshness claims. Strategic apply of carbon transparent labeling and QR coded traceability builds trust in an increasingly eco conscious marketplace. Additionally, firms diversify into frozen and value added formats to buffer against seasonal volatility and capture industrial demand from functional food manufacturers seeking reliable ingredient supply.

MARKET SEGMENTATION

This research report on the European blueberry market has been segmented and sub-segmented based on categories.

By Application

- Food and beverages

- Bakery and confectionary

- Others

By Type

By Product

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply