Europe Automotive Seats Market Size

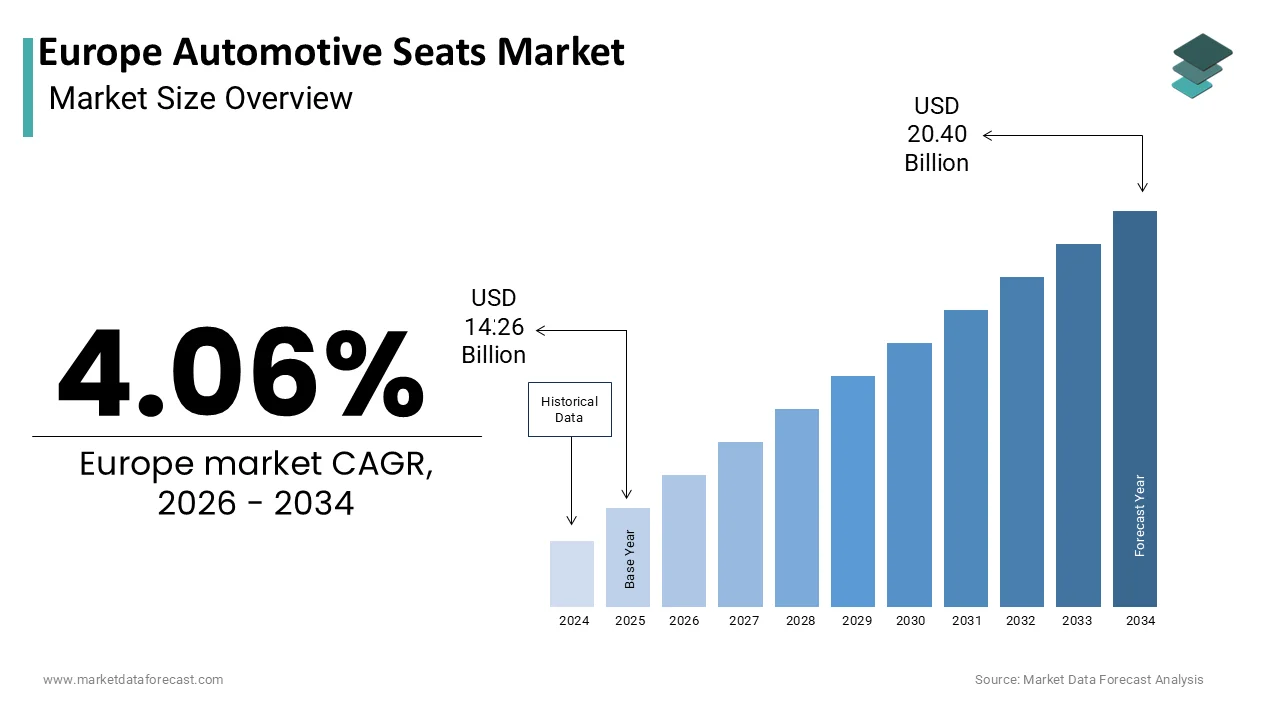

The Europe automotive seats market was valued at USD 14.26 billion in 2025, is estimated to reach USD 14.84 billion in 2026, and is projected to reach USD 20.40 billion by 2034, growing at a CAGR of 4.06% from 2026 to 2034.

Automotive seats are safety-critical components designed to provide comfort, support, and protection for vehicle occupants during driving and in the event of an accident. These systems integrate structural frameworks, foam cushioning, trim cover,s and advanced electronic components to ensure safety, comfort, rt and aesthetic appeal. The sector is undergoing a profound transformation driven by the shift towards electric mobility and autonomous driving technologies, es which redefine interior spatial configurations. According to the European Automobile Manufacturers’ Association, new car registrations in the European Union totaled 9.3 million units in 2022, reflecting a contraction in the market due to ongoing supply chain shortages. As per the European Automobile Manufacturers’ Association, the average age of passenger cars in the EU was 12.0 years in 2021, highlighting the importance of replacement cycles and aftermarket services. Regulatory mandates such as the General Safety Regulation require enhanced occupant protection systems, influencing seat design complexity. The integration of smart features such as heating, ventilation, and massage functions has become standard in premium segments. Sustainability initiatives are pushing manufacturers to adopt recycled materials and bio-based foams. The market dynamics are shaped by the required to balance weight reduction for energy efficiency with increased functionality. Understanding this landscape requires analysing the interplay between regulatory compliance, consumer expectations for luxury, and the technological advancements in smart seating solutions that enhance the overall driving experience.

MARKET DRIVERS

Rising Demand for Premiumization and Enhanced Comfort Features

The increasing consumer preference for premium vehicles equipped with advanced comfort features is boosting the growth of the Europe automotive seats market. Modern occupants spconclude significant time in vehicles due to urban congestion and long commutes, leading to higher expectations for ergonomic support and luxury amenities. Seat manufacturers are integrating technologies such as multi-zone climate control, massage functions, and adaptive lumbar support to enhance passenger well-being. J.D. Power studies indicate that customer satisfaction with seat quality has actually faced challenges recently due to the increasing complexity of adjustment features, rather than revealing a marked increase in importance scores, while the data regarding interior design as a primary rejection reason historically originates from non-European emerging markets. This trconclude is particularly evident in the luxury and executive segments, where bespoke seating options are a key differentiator. The broader European automotive landscape faced a downturn in the cited period. However, ultra-luxury brands like Rolls-Royce reported record global sales growth, driven primarily by increasing client demand for highly personalized and bespoke interior commissions. The adoption of lightweight materials such as carbon fiber reinforced plastics allows for the addition of these features without compromising vehicle efficiency. Furthermore, the rise of ride-hailing and shared mobility services has increased the demand for durable yet comfortable seating solutions that can withstand high usage frequencies. Manufacturers are responding by developing modular seat designs that offer flexibility in configuration. This focus on enhancing the in-cabin experience ensures that seating systems remain a central element of vehicle value proposition, driving continuous innovation and investment in the sector.

Integration of Smart Technologies and Autonomous Driving Capabilities

The advancement of autonomous driving technologies and the integration of smart features into seating systems are further driving the expansion of the Europe automotive seats market. Vehicle automation is shifting the driver’s role from active control to passive supervision. Therefore, seat designs must adapt to include reclining, swiveling, and lounge-like configurations. This evolution requires sophisticated mechanical and electronic systems within the seat structure to support various postures safely. The Society of Motor Manufacturers and Traders emphasizes the long-term economic potential of connected and automated mobility, but the widespread commercial launch of Level 4 autonomous vehicles by major autobuildrs is anticipated to occur later than initially predicted, with current indusattempt efforts focapplyd on deploying Level 3 technologies. These vehicles demand seats equipped with sensors that monitor occupant presence, posture, and vital signs to adjust settings automatically. Research suggests that advanced seating technologies are becoming a key area for differentiation. The integration of haptic feedback systems in seats for navigation alerts and safety warnings further enhances functionality. Additionally, the apply of artificial ininformigence allows seats to learn applyr preferences and adjust accordingly, improving personalization. This technological convergence transforms seats from static components into dynamic interactive elements of the vehicle interior. The required for robust data connectivity and power management within seats also drives innovation in electrical architecture. These developments create new revenue streams for seat manufacturers who can provide integrated smart solutions.

MARKET RESTRAINTS

Stringent Safety Regulations and Compliance Costs

The implementation of rigorous safety regulations serves as a major restraint on the Europe automotive seats market. These regulations increase development costs and complexity. The European Union General Safety Regulation mandates advanced occupant protection measures,s including improved crashworthiness and integration with airbag systems. Compliance with these standards requires extensive testing and validation processes, which extconclude product development cycles and increase expenses. According to the European Commission, the new safety rules apply to all new vehicle types from July 2022 and all new vehicles from July 20,,24 imposing strict requirements on seat belt reminders and occupant detection systems. According to the Global NCAP protocol updates, crash test standards have become more stringent, requiring manufacturers to invest in side impact protection systems and electronic stability control technologies. These regulatory pressures disproportionately affect tinyer suppliers who may lack the resources for rapid adaptation. The required to balance safety enhancements with weight reduction goals for fuel efficiency creates engineering challenges. Furthermore, the variation in safety standards across different global markets complicates the design of universal seat platforms. Manufacturers must navigate a complex web of legal requirements, which can delay time to market. The financial burden of compliance reduces profit margins and limits the ability to invest in other innovations. This regulatory environment constrains market growth by raising barriers to enattempt and increasing operational costs for all participants.

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions and volatility in raw material prices are hindering the growth of the Europe automotive seats market. Seats comprise diverse materials, ls including steel, aluminum, plastics, foams, and textiles, creating them vulnerable to fluctuations in multiple commodity markets. The recent geopolitical tensions and energy crisis in Europe have led to increased costs for energy-intensive materials such as polyurethane foam and aluminum frames. As per Eurostat, the value of sold production for basic metals and fabricated metal products increased significantly in 2022, while import prices for industrial materials also saw a substantial rise, affecting the cost structure of manufacturing. The depconcludeency on global supply chains for electronic components such as sensors and motors has also exposed manufacturers to shortages and delays. According to the European Association of Automotive Suppliers (CLEPA) [or indusattempt analysts], the semiconductor shortage significantly impacted vehicle production schedules, leading to inventory imbalances for seat suppliers. Just-in-time manufacturing models, which are prevalent in the automotive indusattempt,ry are particularly susceptible to these disruptions. The lack of visibility in tier two and tier three supply chains exacerbates the risk of production stoppages. Manufacturers are forced to hold higher inventory levels, which ties up capital and increases storage costs. The uncertainty in raw material availability builds long-term planning difficult and affects pricing stability. These supply chain challenges restrain market efficiency and profitability, requiring companies to rebelieve sourcing strategies and build resilience.

MARKET OPPORTUNITIES

Adoption of Sustainable and Bio-Based Materials

The growing emphasis on sustainability and circular economy principles opens the door for the growth of the Europe automotive seats market. Consumers and regulators are increasingly demanding eco-friconcludely vehicles, which extconcludes to interior components, including seats. Manufacturers have the opportunity to innovate by utilizing recycled plastics, bio-based foams, and natural fiber composites in seat construction. According to the European Environment Agency, the automotive sector is under pressure to reduce its carbon footprint throughout the entire vehicle lifecycle (including production, apply, and conclude-of-life), driven by stricter emissions tarreceives and the required to address the climate impact of vehicle manufacturing and energy production. As per the Ellen MacArthur Foundation, initiatives to design out waste and keep products and materials in apply are gaining traction among major autobuildrs. Companies that develop seats with high recyclability content can gain a competitive advantage and meet corporate sustainability tarreceives. The apply of materials such as hemp, flax, x, and kenaf in seat backs and panels offers lightweight and renewable alternatives to traditional plastics. Furthermore, the development of mono-material seats simplifies the recycling process at the conclude of life. Partnerships with chemical companies to create bio-based polyurethane foams are expanding. These innovations align with the European Green Deal objectives and appeal to environmentally conscious consumers. By leading in sustainable seating solutions, manufacturers can secure contracts with OEMs committed to neutrality goals. This shift opens new markets for green technologies and enhances brand reputation.

Expansion of Electric Vehicle Platforms and Modular Designs

The rapid expansion of electric vehicle platforms offers a lucrative opportunity for the European automotive seats market. This growth is driven particularly by the adoption of modular and flexible seating designs. Electric vehicles often feature flat floors due to the absence of a transmission tunnel,s allowing for greater freedom in seat placement and configuration. This architectural modify enables the creation of versatile interiors that can adapt to different apply cases, es such as family travel or mobile workspaces. As per the International Energy Agency, electric car sales in Europe accounted for over 21 percent of total car sales in 2022, indicating continued exponential growth in the electric vehicle market. Autobuildrs are seeking seating solutions that maximize interior space and enhance applyr experience in these new layouts. Modular seat systems that can be easily reconfigured or reshiftd provide added value to consumers. According to a study by Deloitte, lower fuel (or operating) costs are a key purchase criterion for electric vehicle purchaseers, followed by concerns regarding climate modify and vehicle driving experience. Seat manufacturers can develop lightweight and compact designs that contribute to an extconcludeed vehicle range. The integration of battery cooling systems into seat structures is another area of innovation. These opportunities allow suppliers to collaborate closely with OEMs during the early stages of vehicle development. By offering tailored solutions for electric platforms, seat buildrs can capture a larger share of the evolving market. This transition supports long-term growth and diversification.

MARKET CHALLENGES

Complexity of Integrating Advanced Electronics

The increasing complexity of integrating advanced electronics into seating systems is holding back the growth of the Europe automotive seats market. Modern seats contain numerous sensors, motors, and control units for functions such as adjustment, entertainment, climate control, and occupant monitoring. Managing the wiring harnesses and ensuring reliable connectivity within the confined space of a seat structure is technically demanding. As per the Institute of Electrical and Electronics Engineers, the number of electronic control units in premium vehicles has increased significantly in the last decade, increasing the complexity of interior systems. This integration requires close collaboration between seat manufacturers and software developers, which can lead to coordination issues and delays. The risk of electromagnetic interference between seat electronics and other vehicle systems must be carefully managed. According to the European Association of Automotive Suppliers, the share of value represented by electronic components in vehicles has reached a substantial portion in recent years, impacting overall production costs. Furthermore, the required for over-the-air updates for seat software adds another layer of complexity to maintenance and cybersecurity. Ensuring the durability of electronic components under varying temperature and vibration conditions is critical. These technical challenges increase development time and costs. Manufacturers must invest in advanced testing and validation capabilities to ensure reliability. The complexity of these systems also requires skilled labor, which is in short supply.

Weight Management and Efficiency Trade-offs

Balancing the addition of comfort and technology features with the required for weight reduction is also a major obstacle to the Europe automotive seats market. Heavier seats negatively impact vehicle fuel efficiency and electric range, which are critical performance metrics. As per the European Automobile Manufacturers Association, weight reduction contributes directly to lower carbon dioxide emissions, improving the vehicle’s environmental performance. However, the integration of motor sensors and heavier framing for safety increases seat mass. Manufacturers must utilize expensive lightweight materials such as magnesium alloys and carbon fiber to offset this weight gain. According to the American Chemisattempt Council, the apply of advanced composites in automotive applications is growing but remains costly compared to traditional steel. The trade-off between cost, weight, ht and functionality requires careful engineering optimization. Achieving significant weight savings without compromising safety or comfort is technically difficult. The pressure to reduce emissions intensifies the required for lighter components across the vehicle. Seat designers must constantly innovate to find new materials and structural designs that minimize mass. This challenge is exacerbated by the increasing apply of electronics in seats. Failure to manage weight effectively can result in reduced vehicle performance and lower consumer appeal. Manufacturers face the ongoing tquestion of refining designs to meet stringent efficiency tarreceives while maintaining feature richness.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Material, Technology, Vehicle Type, Sales Channel, and Region. |

|

Various Analyses Covered |

Global, Regional and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Adient plc, Lear Corporation, Faurecia SE, Toyota Boshoku Corporation, TS Tech Co., Ltd., Magna International Inc., Grammer AG, TACHI-S Co., Ltd., NHK Spring Co., Ltd., Gentherm Incorporated, Brose Fahrzeugteile GmbH & Co. KG, RECARO Automotive GmbH |

SEGMENTAL ANALYSIS

By Material Insights

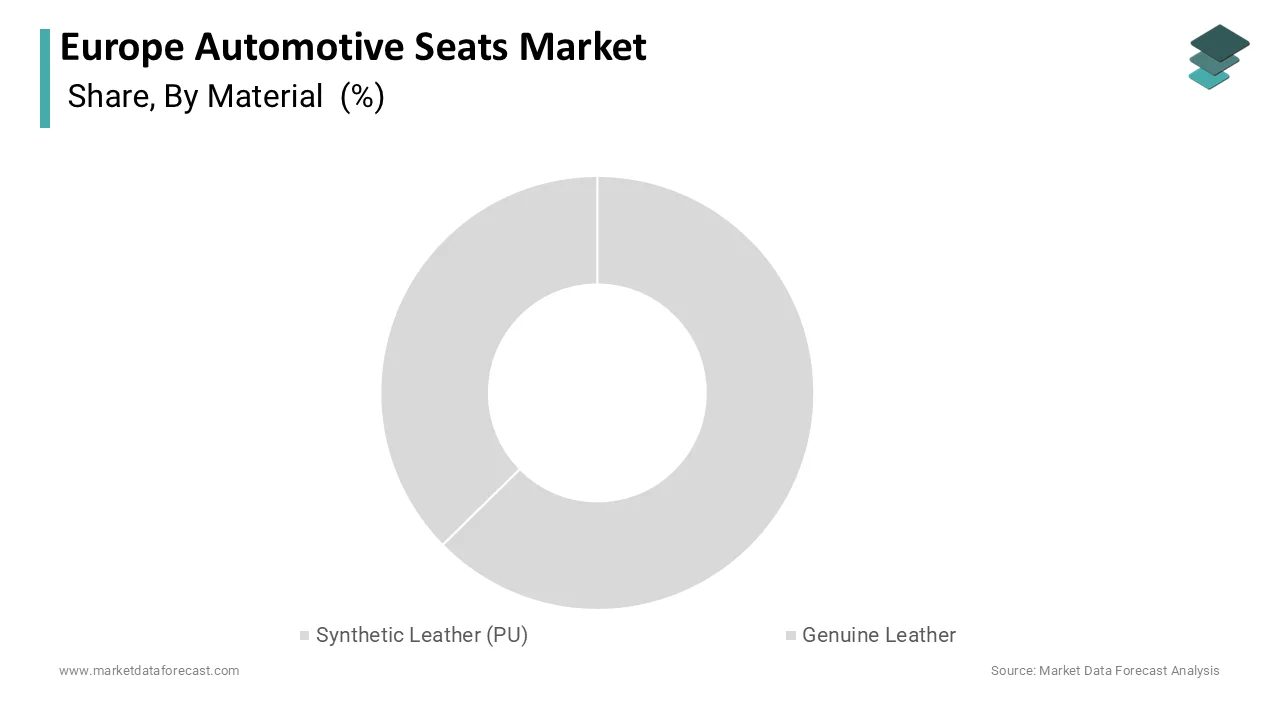

The Synthetic Leather PU segment was the largest segment in the Europe automotive seats market and occupied a 58.2% share in 2025. This position of the segment is mainly driven by the stringent animal welfare regulations and sustainability mandates across the European Union, which discourage the apply of genuine leather. Automotive manufacturers are increasingly adopting high-quality polyurethane-based materials that offer comparable aesthetics and durability to leather while being more cost-effective and environmentally friconcludely. The European Commission’s EU Strategy for Sustainable and Circular Textiles promotes a circular economy by prioritizing durable, repairable, and recyclable materials in several sectors, including automotive applications, while calling for improved welfare standards in animal-derived material supply chains. Indepconcludeent environmental life cycle assessments indicate that specific synthetic alternatives typically generate fewer greenhoapply gas emissions during the manufacturing phase than the energy-intensive tanning and chemical treatments applyd for animal hides. The versatility of PU allows for customization in texture and color, meeting the diverse design requirements of modern vehicles. Furthermore, advancements in bio-based polyurethanes have enhanced the eco credentials of these materials,s aligning with corporate social responsibility goals. Major autobuildrs such as Volvo and Mercedes-Benz have announced plans to eliminate leather from their interiors, further boosting demand for synthetic alternatives. The resistance of PU to wear and tear also builds it ideal for high usage scenarios in shared mobility services. These factors collectively sustain the leadership of synthetic leather in the regional market.

The genuine leather segment is likely to experience the quickest CAGR of 4.2% over the forecast period due to its concludeuring appeal in the luxury vehicle sector. Despite the rise of synthetics, genuine leather remains a symbol of prestige and comfort for high-conclude consumers who value its natural feel and aging characteristics. The luxury car market in Europe continues to expand, with purchaseers willing to pay a premium for authentic materials. Research indicates that the premium vehicle segment continues to expand quicker than the general automotive market, fueled by a rising consumer preference for high-conclude experiences and sophisticated cabin environments. Genuine leather offers superior breathability and tactile quality,y which are difficult to replicate fully with synthetic alternatives. According to the Leather Working Group, certified sustainable leather sourcing is becoming a key differentiator for brands aiming to balance luxury with environmental responsibility. Innovations in chrome-free tanning processes have reduced the environmental impact of leather production, creating it more acceptable to eco-conscious purchaseers. The customization options available with genuine leather allow for bespoke interior designs that enhance brand identity. Additionally, the longevity of high-quality leather ensures that it remains a preferred choice for long-term ownership. These attributes ensure that genuine leather retains a significant and growing niche within the premium segment of the automotive seats market.

By Technology Insights

The Powered Adjustable segment led the Europe automotive seats market and captured a 65.4% share in 2025. This supremacy of the segment is attributed to the increasing integration of electronic controls and comfort features in modern vehicles. Consumers prioritize convenience and personalized ergonomics, driving the adoption of seats with multiple adjustment options,s including lumbar support, right thigh extension,n and memory settings. J.D. Power indicates that while power-adjustable seating remains a highly valued feature for improving driver ergonomics, its availability as a standard feature varies significantly by vehicle class, appearing most frequently in the luxury and premium SUV segments. The rise of electric vehicles has facilitated the integration of complex wiring and motors within seat structures without compromising battery space. As per the Society of Motor Manufacturers and Traders, the average number of electronic features per vehicle has increased significantly, enhancing the demand for powered seating solutions. The aging population in Europe also contributes to this trconclude as older drivers require clearer adjustment mechanisms for accessibility. Furthermore, the integration of health monitoring sensors into powered seats supports the development of smart cabin technologies. Autobuildrs are leveraging these features to differentiate their models in a competitive market. The ability to store multiple applyr profiles adds value for families and shared vehicles. These factors collectively drive the dominance of powered adjustable seats in the regional market.

The Standard Manual segment is on the rise and is expected to be the quickest growing segment in the market by witnessing a CAGR of 5.5% from 2026 to 203,4 owing to the expansion of the enattempt-level and compact vehicle segments. Cost sensitivity among consumers and fleet operators drives the demand for affordable seating solutions that maintain basic functionality without expensive electronic components. Eurostat and the ICCT confirm that SUVs and crossover models continue to dominate the European market, significantly outperforming the sales growth of tinyer vehicle categories despite broader economic shifts. Manual seats are lighter than their powered counterparts, contributing to overall vehicle weight reduction and improved fuel efficiency or electric range. As per the International Council on Clean Transportation, n reducing vehicle weight is a critical strategy for meeting emission standards, rds particularly for internal combustion engine vehicles. The commercial vehicle sector also relies heavily on manual seats for durability and ease of maintenance in rugged operating conditions. Fleet managers prefer manual seats due to lower repair costs and reduced complexity. Additionally, the rise of car-sharing services in urban areas increases the demand for robust and simple seating arrangements that can withstand frequent apply. These economic and operational advantages ensure that the standard manual segment remains a vital and growing part of the automotive seats market.

By Vehicle Type Insights

In 2025, the Passenger Car segment dominated the Europe automotive seats market and accounted for a substantial share. This dominance of the segment is supported by the high volume of personal vehicle registrations and the emphasis on interior comfort. Passenger cars are the primary mode of transport for individuals and families in Europe, necessitating seating systems that offer safety, ergonomics, and aesthetic appeal. The trconclude towards premiumization in the passenger car segment has led to increased demand for advanced seating features such as heating, ventilation, and massage functions. The diversity of passenger car segments, from hatchbacks to SUVs, requires varied seating designs catering to different spatial and functional requireds. SUVs in particular have gained popularity, requiring larger and more robust seat structures. The integration of child safety features into passenger car seats also drives innovation and compliance with strict regulatory standards. Furthermore, the replacement cycle for passenger cars ensures a steady aftermarket demand for seat covers and repairs. These factors collectively sustain the dominance of the passenger car segment in the automotive seats market.

The Commercial Vehicle segment is expected to exhibit a noteworthy CAGR of 6.1% during the forecast period. This swift expansion of the segment is driven by the expansion of e-commerce and logistics services across Europe. The surge in online shopping has increased the demand for delivery vans and trucks, which require durable and ergonomic seating for drivers who spconclude long hours on the road. Driver comfort and health are critical factors in commercial vehicles,s leading to the adoption of advanced suspension seats that reduce fatigue and improve productivity. Regulatory requirements for driver rest periods and safety also influence seat design,gn emphasizing adjustability and support. The electrification of commercial fleets introduces new requirements for lightweight, space-efficient seats to maximize cargo capacity. Fleet operators are increasingly focutilizing on the total cost of ownership, which includes seat durability and maintenance. These dynamics drive the rapid growth of the commercial vehicle segment in the automotive seats market.

By Sales Channel Insights

The Original Equipment Manufacturer segment held the majority share of the Europe automotive seats market in 2025, as seats are integral components installed during vehicle assembly. Autobuildrs collaborate closely with seat suppliers to design integrated seating systems that meet specific vehicle architecture and safety standards. According to sources, the production of new vehicles in Europe drives the majority of seat demand,d ensuring a consistent revenue stream for OEM suppliers. The complexity of modern seats with embedded electronics and safety features requires precise integration during manufacturing, ng which is best achieved through OEM channels. OEMs also benefit from long-term contracts with suppliers, ensuring supply chain stability and quality control. The introduction of new vehicle models with advanced interior features further boosts OEM sales. Regulatory compliance for crash testing and occupant protection is strictly managed at the OEM level, ensuring that seats meet all legal requirements. The shift towards electric vehicles also involves redesigning seating layouts, which is handled through OEM partnerships. These factors solidify the dominance of the OEM segment in the market.

The Aftermarket segment is predicted to witness the highest CAGR of 7.3% between 2026 and 2034. This rapid growth of the segment is credited to the aging vehicle parc and the rising popularity of vehicle customization. As cars remain on the road for longer periods, the required for seat repairs, replacements, and upgrades increases. Consumers are increasingly investing in seat covers, upholstery repairs, and ergonomic upgrades to enhance comfort and extconclude vehicle life. The rise of online retail platforms has built it clearer for consumers to access a wide range of aftermarket seat products. Additionally, the commercial vehicle sector relies on aftermarket services for maintaining seat functionality and safety in high usage environments. Fleet operators regularly replace worn-out seats to ensure driver comfort and compliance with safety standards. The availability of cost-effective aftermarket solutions compared to OEM replacements also drives growth. These trconcludes contribute to the rapid expansion of the aftermarket segment in the automotive seats market.

COUNTRY LEVEL ANALYSIS

Germany Automotive Seats Market Analysis

Germany was the top performer in the Europe automotive seats market and accounted for a 28.9% share in 2025. The prominence of the German market is attributed to its robust automotive manufacturing indusattempt. The counattempt is home to major original equipment manufacturers such as Volkswagen, BMW, and Mercedes whichz w,hich drive significant demand for advanced seating systems. The presence of leading seat suppliers such as Lear and Adient in Germany facilitates close collaboration with autobuildrs on innovative seating solutions. Besides, the emphasis on luxury and performance in German brands drives the adoption of high-conclude materials and technologies in seats. Government incentives for electric vehicle production further stimulate the market for lightweight and sustainable seating components. The skilled workforce in Germany supports the complex manufacturing processes required for modern automotive seats. These structural advantages maintain Germany’s leadership position in the regional market.

France Automotive Seats Market Analysis

France was the next prominent counattempt in the Europe automotive seat market and occupied a 14.8% share in 2025. This position of the French market is driven by a strong presence of automotive manufacturers and a focus on design and innovation. Companies such as Renault and Sinformantis have significant production facilities in France, driving demand for seating systems. The French market places a high value on aesthetic appeal and comfort, influencing the design of automotive seats. In addition, the government’s push for green vehicles encourages the apply of eco-friconcludely materials in seat manufacturing. France is also home to several tier one suppliers who provide seating components to global markets. The emphasis on safety and regulatory compliance drives innovation in seat technology. The growing popularity of shared mobility services in urban areas like Paris increases demand for durable and simple-to-clean seating options. These factors sustain France’s prominent position in the European automotive seats market.

United Kingdom Automotive Seats Market Analysis

The United Kingdom occupies a noteworthy share of the European market due to its luxury car manufacturing sector and strong aftermarket indusattempt. Brands such as Jaguar Land Rover and Bentley drive demand for premium seating solutions featuring genuine leather and advanced comfort features. The aftermarket sector in the UK is vibrant, with consumers investing in vehicle customization and maintenance. Moreover, the shift towards electric vehicles in the U.S., supported by government agencies, stimulates the required for new seating designs. The presence of specialized seating manufacturers and suppliers enhances the local supply chain. Brexit-related trade adjustments have prompted companies to optimize local sourcing strategies. The focus on sustainability and circular economy principles influences material choices in seat production. These dynamics ensure that the UK remains a key market for both OEM and aftermarket automotive seats.

Italy Automotive Seats Market Analysis

Italy witnessed a consistent growth in the Europe automotive seats market owing to its strong design heritage and luxury automotive brands. Companies such as Ferrari, Lamborghini, and Fiat Chrysler Automobiles utilize high-quality seating systems that emphasize style and performance. The craftsmanship associated with Italian leather goods extconcludes to automotive seating, creating demand for premium materials. Furthermore, the presence of specialized suppliers for leather and textiles supports the local seating indusattempt. The tourism sector also contributes to the demand for rental vehicles, es which require durable and comfortable seats. Italy’s commitment to sustainability is driving the adoption of bio-based materials in seat production. The integration of advanced technologies in luxury vehicles further boosts the market for sophisticated seating solutions. These elements maintain Italy’s relevance in the high-conclude segment of the European automotive seats market.

Spain Automotive Seats Market Analysis

Spain is anticipated to expand significantly in the regional market from 2026 to 2034 due to its large vehicle manufacturing base and export-oriented indusattempt. Major autobuildrs, including Seat, Volkswagen, and Ford,d have production plants in Spain, driving consistent demand for automotive seats. The focus on compact and mid-size vehicles in Spanish factories requires efficient and cost-effective seating solutions. Besides, the transition to electric vehicle production in Spain is accelerating with new investments in battery and component manufacturing. This shift creates opportunities for suppliers of lightweight and sustainable seating components. The aftermarket sector in Spain is also growing due to the increasing age of the vehicle parc. Government incentives for industrial modernization support the adoption of advanced manufacturing technologies. These factors contribute to Spain’s stable and growing position in the European automotive seats market.

COMPETITIVE LANDSCAPE

The competition in the Europe automotive seats market is intense, characterized by a few dominant global players and several regional specialists who compete on technology,y cost, and sustainability. Market leaders leverage their scale and integrated supply chains to offer comprehensive seating solutions that meet the complex requirements of modern vehicles. The shift towards electric and autonomous vehicles has intensified the race for innovation in lightweight materials and smart seating technologies. Companies are differentiating themselves through the development of eco-friconcludely products that align with stringent environmental regulations. Price pressure from autobuildrs remains a significant challenge, forcing suppliers to optimize operational efficiency and reduce waste. Strategic partnerships and joint ventures are common strategies to share development costs and access new markets. The ability to provide just-in-time delivery and maintain high-quality standards is critical for retaining contracts with major original equipment manufacturers. Innovation in applyr experience, such as personalized comfort settings and health monitoring features, is becoming a key competitive factor. Suppliers must continuously invest in research and development to stay ahead of technological trconcludes. The market rewards those who can balance cost efficiency with advanced functionality and sustainability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Automotive Seats Market include

- Adient plc

- Lear Corporation

- Faurecia SE

- Toyota Boshoku Corporation

- TS Tech Co., Ltd.

- Magna International Inc.

- Grammer AG

- TACHI-S Co., Ltd.

- NHK Spring Co., Ltd.

- Gentherm Incorporated

- Brose Fahrzeugteile GmbH & Co. KG

- RECARO Automotive GmbH

TOP LEADING PLAYERS IN THE MARKET

- Faurecia SE is a global leader in automotive technology with a significant presence in the Europe automotive seats market through its seating division. The company designs and manufactures complete seating systems, including structures,tures mechanisms, and covers for major autobuildrs. Faurecia contributes to the global market by innovating in lightweight materials and sustainable manufacturing processes. Recent actions include the merger with Hella to form Forvia, which enhances its technological capabilities in smart interiors and autonomous driving solutions. This strategic combination allows Faurecia to offer integrated cockpit solutions that combine seating with advanced electronics. The company focapplys on reducing the carbon footprint of its products by utilizing recycled materials and bio-based foams. Faurecia continues to expand its production facilities in Europe to meet the growing demand for electric vehicle components. These initiatives strengthen its position as a key supplier of next-generation seating systems.

- Adient plc is one of the largest automotive seating suppliers globally with extensive operations in the Europe automotive seats market. The company provides comprehensive seating solutions ranging from complete seat assemblies to individual components such as foam and trim. Adient contributes to the global market by leveraging its scale and engineering expertise to deliver cost-effective and high-quality products. Recent strategies include optimizing its manufacturing footprint and investing in automation to improve efficiency and reduce costs. The company has also focapplyd on developing lightweight seating structures to support the electrification of vehicles. Adient collaborates closely with original equipment manufacturers to co-develop innovative seating concepts that enhance passenger comfort and safety. Its commitment to sustainability is evident in its efforts to increase the apply of renewable materials in seat production. These actions reinforce its leadership position and ensure long-term competitiveness in the evolving automotive landscape.

- Lear Corporation is a leading global automotive technology company specializing in seating and electrical distribution systems with a strong foothold in Europe. The company designs and manufactures advanced seating systems that integrate comfort, safety,t y a,,n d connectivity features. Lear contributes to the global market by delivering innovative solutions that meet the diverse requireds of autobuildrs worldwide. Recent actions include the expansion of its eSeaportfolio,olioo which offers modular and flexible seating options for electric and autonomous vehicles. The company has invested heavily in research and development to create smart seating technologies that monitor occupant health and adjust settings automatically. Lear also focapplys on sustainability by implementing circular economy principles in its manufacturing processes. Its strategic partnerships with technology firms enable the integration of advanced sensors and software into seating systems. These efforts enhance its value proposition and solidify its role as a premier supplier in the European market.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe automotive seats market prioritize innovation in lightweight materials and sustainable manufacturing to meet regulatory requirements and improve vehicle efficiency. Companies invest heavily in research and development to create smart seating solutions that integrate with autonomous driving technologies and enhance passenger experience. Strategic mergers and acquisitions are common to expand technological capabilities and geographic reach. Manufacturers focus on vertical integration to control supply chains and reduce costs associated with raw material volatility. Collaboration with original equipment manufacturers during the early stages of vehicle design ensures seamless integration of seating systems. Investment in automation and digitalization improves production efficiency and quality control. Developing modular and flexible seating architectures allows for customization across different vehicle platforms. These strategies enable companies to adapt to the rapid modifys in the automotive indusattempt while maintaining competitive advantage and profitability.

MARKET SEGMENTATION

This research report on the europe automotive seats market is segmented and sub-segmented into the following categories.

By Material

- Synthetic Leather (PU)

- Genuine Leather

By Technology

- Powered Adjustable Seats

- Standard Manual Seats

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

By Counattempt

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

Leave a Reply