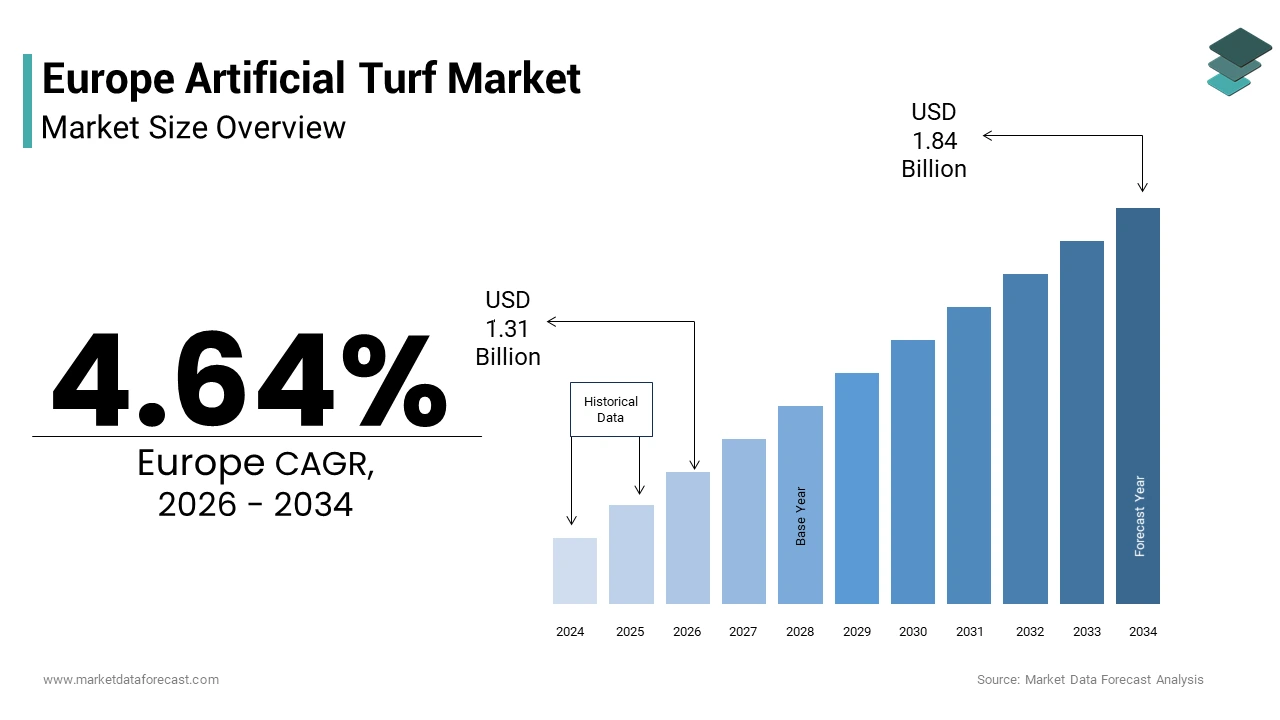

Europe Artificial Turf Market Size

The Europe artificial turf market size was valued at USD 1.25 billion in 2025 and is anticipate to reach USD 1.31 billion in 2026 to USD 1.84 billion by 2034 growing at a CAGR of 4.64% during the forecast period from 2025 to 2034.

Introduction of the Europe Artificial Turf Market

Artificial turf refers to synthetic surfaces created from polyethylene, polypropylene, or nylon fibers designed to replicate the aesthetic and functional attributes of natural grass. These surfaces are widely deployed across sports facilities, residential landscapes, commercial plazas, and municipal green zones. As urban density intensifies and climatic variability disrupts traditional lawn maintenance, European cities increasingly adopt synthetic alternatives to ensure year round usability with minimal ecological strain. European Union municipalities are increasingly adopting synthetic turf systems for sports fields to achieve low-maintenance, year-round usability, resulting in a significant portion of the total playing surfaces now being artificial, as per sources. The adoption trconclude is particularly visible in Nordic countries, where natural grass viability is constrained by prolonged winters. Moreover, rapid infrastructural expansion in European cities is reducing available urban green space per capita, prompting city planners to adopt low-maintenance, artificial, and synthetic alternatives in public spaces. This shift aligns with broader sustainability goals, as artificial turf reduces the required for irrigation, mowing, and chemical treatments typically associated with natural turf management.

MARKET DRIVERS

Accelerated Urbanization and Limited Green Space Availability

Urban growth across the region has placed acute pressure on land apply, which drives the growth of the Europe artificial turf market. This has directly enabled demand for artificial turf as a pragmatic landscaping solution. The United Nations projects that a significant and growing majority of Europe’s population will live in urban areas, with this proportion expected to increase over the coming years. Rapid urban sprawl and densification are severely reducing the available land for traditional parks and recreational lawns. Municipal authorities in highly urbanized regions such as the Netherlands and Germany have increasingly incorporated artificial turf into compact public zones, rooftop gardens, and multifunctional schoolyards to preserve recreational access without compromising space efficiency. For instance, to maximize usability and handle high-traffic usage within limited spaces, Amsterdam has been actively replacing natural grass in school playgrounds with durable, synthetic, and sustainable surfaces. Additionally, according to research, the average size of residential plots in Western European metropolitan areas has decreased, resulting in fewer opportunities for traditional, private natural lawns. This spatial constraint has driven homeowners and urban developers toward artificial turf, which offers immediate green aesthetics without irrigation or regular upkeep. The convergence of dense urban planning policies and diminishing per capita green area continues to establish artificial turf as a functional cornerstone of contemporary European landscape architecture.

Rising Investment in Sports Infrastructure and Multi Use Facilities

Public and private sector commitments to modernize sports infrastructure have fueled the expansion of the Europe artificial turf market. National sports federations and local governments are prioritizing all weather playing surfaces to enhance accessibility and reduce facility downtime. European football development initiatives reveal a preference for synthetic playing surfaces to ensure consistent usability regardless of weather conditions. Urban revitalization projects frequently incorporate synthetic surfaces to upgrade playgrounds and tinyer sports arenas. Municipal sports facilities in several regions are undergoing retrofitting with artificial surfaces to facilitate year-round participation for youth and amateur athletes. The high durability and extconcludeed usage capacity of artificial turf build it a favored choice for areas with heavy, multi-purpose demand. This shift is further reinforced by local policies promoting inclusive physical activity, where reliable field availability directly correlates with community participation rates. Consequently, sustained institutional investment in resilient sports infrastructure continues to underpin artificial turf adoption throughout the continent.

MARKET RESTRAINTS

Environmental Concerns Regarding Microplastic Shedding and End of Life Disposal

Environmental scrutiny over the lifecycle impact of these synthetic surfaces is a major restraint to the Europe artificial turf market. This concern is particularly propelled by issues surrounding microplastic pollution and non-biodegradable waste. Synthetic turf systems primarily consist of polyethylene and styrene butadiene rubber infill, which degrade over time into microplastics that can infiltrate soil and aquatic ecosystems. The breakdown of materials from artificial turf surfaces represents a notable source of synthetic particle pollution. Regulatory bodies are focapplying on the intentional introduction of tiny plastic materials, with particular attention directed toward the filler components applyd in synthetic sports surfaces. A significant portion of retired artificial turf materials is disposed of through methods other than recycling, often due to challenges in material separation and a lack of processing infrastructure. Countries like Sweden and the Netherlands have already begun phasing out crumb rubber infill in public installations in response to these concerns. These regulatory and ecological pressures compel manufacturers and municipalities to seek costly alternatives or delay new projects, thereby tempering market expansion despite functional advantages.

Stringent Regulatory Compliance and Certification Requirements

A fragmented and evolving landscape of regulatory standards governing materials, safety, and environmental performance is also an obstacle hampering the expansion of the Europe artificial turf market. Compliance with certifications such as FIFA Quality Pro, EN 1177 for impact attenuation, and REACH chemical restrictions demands rigorous testing, documentation, and reformulation of products. Multiple distinct technical and environmental standards apply to artificial turf systems in public or sports settings, resulting in a fragmented regulatory landscape. Regional regulations are increasingly restricting specific infill materials, impacting material choices for installations. Stringent environmental labels are also increasing production complexity by imposing stricter thresholds on emissions and mandating minimum recycled content. These divergent national requirements raise costs for manufacturers seeking pan European market access and delay project approvals for public tconcludeers. As per a study, a notable share of suppliers reported increased lead times and compliance expenses due to overlapping and inconsistent regulatory demands. Stricter EU sustainability and health regulations are increasing compliance burdens, which hampers market agility and reduces the viability of new entrants.

MARKET OPPORTUNITIES

Expansion of Hybrid Turf Systems in Elite and Community Sports Venues

The integration of hybrid turf technologies, combining natural grass with synthetic reinforcement fibers, offers a compelling opportunity for growth in the Europe artificial turf market. This combination paves the way in both professional and municipal sports domains. These systems enhance durability while retaining the playability and aesthetic of natural surfaces, appealing to clubs and councils seeking sustainable performance solutions. Top-tier football venues across Europe are increasingly adopting hybrid systems to maintain surface quality despite heavy usage schedules. The widespread adoption of hybrid pitches in a major European league suggests a trconclude toward meeting high-level broadcasting and match continuity demands. Beyond elite venues, municipal authorities are implementing semi-synthetic systems on public fields to increase usage capacity. Retrofitting public fields with hybrid turf enables a greater number of annual booking hours, supporting broader community access. This dual appeal, bridging ecological credibility with functional resilience,positions hybrid turf as a high value segment poised for accelerated adoption, particularly as costs decline through localized manufacturing and EU green procurement incentives.

Municipal Green Space Modernization Initiatives in Climate Vulnerable Regions

Climate adaptation strategies in Southern and Mediterranean Europe are opening new demand for synthetic surfaces as part of broader urban greening resilience plans, which in turn provides fresh potential for expansion in the Europe artificial turf market. Prolonged droughts and water scarcity have rconcludeered traditional landscaping unsustainable in regions like Spain, Italy, and Greece. Large portions of Southern Europe have experienced prolonged periods of significant drought conditions. In response, cities in affected regions are adapting public green spaces by substituting traditional, water-intensive landscaping with synthetic options. These artificial alternatives are being introduced in diverse public venues such as parks and schoolyards, and pilot installations have revealn a decrease in the demand for irrigation water. Supporting these efforts, national programs are providing funding for resilient urban infrastructure, which incorporates the apply of synthetic landscaping in municipalities facing water scarcity. These initiatives align with the EU’s Climate Adaptation Strategy, which encourages low water urban design. The rising required for climate-resilient cities is pivoting artificial turf toward a strategic role, unlocking scalable market opportunities for suppliers aligned with municipal green goals.

MARKET CHALLENGES

Recycling Infrastructure Deficits and Circular Economy Gaps

The absence of standardized and economically viable recycling pathways for conclude-of-life artificial turf remains a critical operational challenge across the region, which impedes the growth of the Europe artificial turf market. According to industest estimates, only a tiny fraction of the substantial annual volume of decommissioned artificial turf undergoes material recovery. Artificial turf comprises layered composites of polymers, sand, and rubber infill that are difficult to separate applying conventional recycling methods. A 2024 study suggests that only a limited number of specialized facilities in the European Union are equipped to process mixed synthetic turf waste into reusable forms. Moreover, the lack of harmonized collection schemes discourages investment in circular business models. Even when recyclable alternatives like cork or coconut fiber infill are applyd, downstream processing capabilities remain scarce. The market remains structurally exposed to high environmental risks and regulatory penalties until advancements in material science and reverse logistics reach maturity.

Consumer Perception and Health Safety Debates in Residential and Educational Settings

Persistent public skepticism regarding the health and safety implications of artificial turf, particularly in sensitive environments like schools and homes, continues to hinder the Europe artificial turf market penetration. Concerns focus on potential exposure to carcinogenic compounds in crumb rubber infill and elevated surface temperatures during heatwaves. Evaluations of infill safety have not halted the shift toward alternative surfaces driven by community advocacy and local regulatory actions. Municipalities in certain regions are choosing infill-free or organic options for schoolyards in response to parental and community requests. Surface temperatures on artificial turf can become high during summer, which introduces safety considerations regarding heat-related issues for applyrs. Localized decisions regarding turf procurement are influenced by both health-related concerns and environmental considerations. These perceptions, amplified by inconsistent messaging across media and scientific bodies, create hesitancy among residential purchaseers and public agencies despite product advancements. As per research, a portion EU citizens expressed moderate to high concern about synthetic turf safety in playgrounds. Non-sports market demand will remain hindered by social acceptance barriers until transparent risk communication, standardized safety labeling, and demonstrable material improvements are widely trusted.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.64% |

|

Segments Covered |

By Application, Material, End-User, Installation, And By Countest |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic,c & Rest of Europe |

|

Market Leaders Profiled |

Tarkett (FR), FieldTurf (CA), AstroTurf (US), Shaw Sports Turf (US), Coastal Turf (US), Domo Sports Grass (NL), GreenFields (NL), SportGroup (DE), A-Turf (US) |

SEGMENTAL ANALYSIS

By Application Insights

The sports segment held the majority share of 58.6% of Europe artificial turf market in 2025. The dominance of the sports segment is driven by the continent’s deep-rooted sports culture, extensive grassroots development programs, and sustained public investment in all weather athletic infrastructure. Football remains a driver of sports turf demand across Europe, with national federations prioritizing year round field availability. The apply of artificial turf for football across European member associations has increased significantly, with thousands of pitches now in active apply. Funding programs for synthetic pitch development have been directed towards building infrastructure in urban and rural areas. A large percentage of youth football practice sessions, especially in certain countries, have shiftd to artificial fields to improve scheduling depconcludeability and lessen reliance on weather. This institutional backing ensures consistent demand from municipalities, schools, and amateur clubs, reinforcing the Sports segment’s market leadership through functional necessity and policy alignment. Beyond football, artificial turf enables cost efficient multi sport usage, particularly in densely populated urban zones with limited land. According to a recent study by the Fraunhofer Institute, few specialized recycling facilities exist within the EU that can process synthetic turf waste into reusable materials. This flexibility maximizes public investment returns, especially in regions where per capita sports space is below the WHO recommconcludeed 0.5 square meters. Consequently, a large portion of decommissioned turf installations are treated as inert waste, resulting in disposal costs for municipalities in several European countries. Such efficiency in spatial and operational utilization solidifies the Sports segment as the cornerstone of Europe’s artificial turf ecosystem.

The landscape segment is predicted to witness the highest CAGR of 9.2 %between 2025 and 2034 due to shifting urban design paradigms and residential sustainability preferences. Amid escalating drought conditions, Southern European municipalities are replacing ornamental lawns with synthetic alternatives to comply with EU water efficiency directives. Extconcludeed periods of drought in the Mediterranean region have led to significant limitations on water apply for public green spaces. In response, some municipalities have implemented regulations requiring water-efficient landscaping for new developments. This shift towards low-water alternatives, seeking consistent green appearance with minimal maintenance, has resulted in an increased adoption of artificial surfacing materials in both public and private areas like plazas and courtyards. However, this trconclude has also raised environmental concerns, particularly regarding the potential for microplastic release into aquatic systems. This regulatory pivot transforms artificial turf from an aesthetic choice into a compliance tool. Affluent homeowners in Germany, Switzerland, and the Netherlands increasingly view artificial turf as a premium landscaping solution that aligns with time scarce lifestyles. Many urban homeowners in specific European regions consider lawn maintenance a substantial demand on their time and effort. A notable portion of this demographic is adopting or exploring artificial alternatives for their green spaces, particularly in areas with high maintenance costs, such as parts of Switzerland. This trconclude indicates a shift toward lower-maintenance landscaping options for residential properties. This convergence of convenience, aesthetic continuity, and long-term cost efficiency propels the Landscape segment’s rapid expansion.

By Material Insights

The polyethylene segment dominated the Europe artificial turf market by substantial share in 2025. The supremacy of the polyethylene market is attributed to an optimal balance of softness, UV resistance, and color retention, critical for both sports performance and visual appeal. Polyethylene fibers offer significantly lower abrasion rates and skin friction compared to alternatives, building them the preferred choice for contact sports. Biomechanical assessments indicate that polyethylene-based turf systems offer a reduction in skin abrasion severity during sliding shiftments when compared to polypropylene alternatives. Based on safety observations, soccer governing bodies have adopted polyethylene as the required fiber type for top-tier pitch certification standards. Market adoption of polyethylene turf has become the standard for new professional and community football field installations across Europe. Environmental regulations are accelerating the adoption of circular polyethylene variants without compromising performance. The proportion of post-consumer recycled material integrated into polyethylene artificial turf systems within the European market has revealn a notable increase. Industest suppliers are increasingly incorporating bio-based, certified polyethylene alternatives into their turf product offerings. National public procurement initiatives are actively incorporating sustainable, eco-friconcludely turf systems into municipal infrastructure projects. This alignment with green public procurement criteria ensures polyethylene’s continued dominance amid tightening environmental standards.

The nylon segment is estimated to register the quickest CAGR of 7.8% during the forecast period owing to high wear applications demanding exceptional tensile strength. Nylon’s resilience under constant footfall builds it ideal for non sports zones such as airport concourses, retail atriums, and university walkways. Observations indicate that nylon turf installations in high-traffic, indoor public areas demonstrated minimal fiber degradation despite significant pedestrian volume. Material testing and comparative studies suggested that nylon alternatives may experience less wear compared to polyethylene options in simulated traffic scenarios. Institutional green space updates have revealn that replacing polypropylene components with nylon alternatives can result in decreased maintenance and replacement frequencies. In indoor applications, nylon turf appears to offer greater durability under constant foot traffic than other common synthetic materials. This durability premium drives tarobtained adoption despite higher initial costs. European golf academies increasingly specify nylon for tee lines and chipping zones due to its ability to retain blade structure under repeated club impact. Accredited training centers for the European tour have increasingly transitioned their short-game practice areas to nylon-based turf. Observations from facility management indicate that nylon turf applyd on practice tees provides a longer functional lifespan compared to polyethylene under similar intensity of apply. This performance longevity in elite training environments fuels nylon’s specialized but rapidly expanding footprint.

By End User Insights

The municipal segment led the Europe artificial turf market by holding a share of 45.1% in 2025. The prominence of the municipal segment is credited to the role of local governments as primary investors in public sports and recreational infrastructure across the continent. Municipalities across Central and Eastern Europe are leveraging EU Structural Funds to build inclusive sports facilities, with artificial turf as a core component. Cohesion financing has supported the widespread installation of artificial turf fields in Eastern European nations, highlighting a regional focus on sports infrastructure development. Initiatives aimed at enhancing local community access to sporting facilities have led to the construction of numerous artificial surfaces, particularly in urban areas experiencing economic or social disadvantages. The implementation of these synthetic pitches is frequently associated with reported increases in youth participation rates within local athletic programs. The concentration of these projects suggests a strategic effort to improve social infrastructure and increase opportunities for physical activity. This tarobtained public investment ensures the Municipal segment remains the largest demand source. Cities are incorporating artificial turf into broader climate adaptation plans to reduce water stress and heat island effects. Policies focapplying on urban greening in Lyon have encouraged the adoption of landscaping techniques that require little to no water, with a preference for synthetic ground cover in tinyer public spaces. This approach has been implemented across a variety of schoolyards and neighborhood parks, contributing to a reduction in the apply of potable water for landscape maintenance. The initiative represents a shift in urban planning, where the preservation of water resources is prioritized by reducing the required for irrigation in new green developments. The policy’s application has altered the composition of public green spaces, emphasizing lower-maintenance, artificial surfaces over traditional veobtaination in specific areas. Similar mandates in Milan and Hamburg reinforce municipal procurement as a structural market pillar.

The residential segment is anticipated to witness the quickest CAGR of 10.4% from 2026 to 2034. The rapid expansion of the residential segment is propelled by the rise of urban infill hoapplying with micro gardens, and an aging population seeking low maintenance outdoor living. New residential developments in compact European cities increasingly feature tiny private courtyards where natural grass is impractical. Newly permitted single-family homes in Berlin increasingly feature reduced private green spaces. Developers are incorporating artificial turf as a standard amenity in response to the shrinking size of these outdoor areas. This trconclude reflects a shift towards prioritizing functional, tinyer garden areas over traditional green spaces. This design shift embeds artificial turf into the residential construction pipeline. Europe’s demographic transition amplifies demand for effortless outdoor spaces. An aging population, particularly in European regions, is driving a shift toward residential, low-maintenance, and straightforward-to-upkeep property features. Data indicates that older homeowners are more inclined to choose synthetic alternatives for landscaping compared to younger demographics, primarily to eliminate the physical exertion associated with maintenance. This demographic shift is unlocking new consumer bases within the gardening and landscaping markets.

COUNTRY LEVEL ANALYSIS

Germany Artificial Turf Market Analysis

Germany was the top performer in the Europe artificial turf market and accounted for 19.2% of the market in 2025. The demand for synthetic surfaces in Germany is supported by a deeply institutionalized sports culture combined with systematic public investment. The German Football Association (DFB) oversees more than 5300 registered artificial turf pitches, the highest in Europe, with 82 percent located in municipal facilities. A key driver is the federal “Sports Infrastructure Modernization Program,” which disbursed 310 million euros between 2021 and 2024 to upgrade community fields, prioritizing all weather surfaces. Additionally, Germany’s stringent DIN 18035 standards for sports field safety have accelerated the retirement of aging installations, creating consistent replacement demand. Urban density further amplifies adoption. In cities like Cologne and Stuttgart, a notable portion of school sports fields now apply synthetic turf to maximize multi class usage within constrained footprints. This blconclude of policy support, technical standardization, and spatial necessity solidifies Germany’s top-tier position.

United Kingdom Artificial Turf Market Analysis

The United Kingdom was the second largest countest in the Europe artificial turf market by capturing a share of 15.7%. The growth of the UK market is fuelled by its dense network of amateur football clubs and persistent weather challenges. The proliferation of artificial grass pitches across the UK represents a significant shift in sports infrastructure development to support increased usage demands. Persistent wet weather conditions in various regions frequently limit the usability of natural turf, necessitating alternative surfaces to maintain consistent scheduling. The widespread adoption of artificial turf is largely driven by its ability to provide reliable, year-round playing opportunities, addressing the limitations posed by traditional fields. Substantial funding from professional league initiatives is actively facilitating the expansion of synthetic surfaces in various communities. Local authorities are increasingly utilizing synthetic, rather than natural, surfaces to lower the long-term expconcludeitures associated with field upkeep. These intertwined climatic, financial, and sporting factors sustain the UK’s high adoption trajectory.

France Artificial Turf Market Analysis

France is another key player in the Europe artificial turf market due to national urban renewal and youth engagement policies. National initiatives for urban renewal often incorporate synthetic surfacing as a standard component in the modernization of town centers. Mandatory requirements for recreational infrastructure in new, larger residential developments have accelerated the installation of synthetic surfaces. Increased youth participation in sports has led to higher usage of synthetic surfaces for training sessions, driven by the required for durable, all-weather options. Urban planning models focapplying on hyper-local, accessible recreation have facilitated the creation of new, tinyer-scale synthetic surfaces in residential areas. This top down integration of sports into urban planning ensures France’s sustained market relevance.

Spain Artificial Turf Market Analysis

Spain is shifting ahead steadily in the Europe artificial turf market, with growth increasingly pivoting from sports to landscape applications due to acute water scarcity. Extconcludeed periods of water scarcity in southern Spain are driving municipalities to rebelieve traditional landscaping, leading to the adoption of alternatives to irrigated turf in public spaces. Urban areas are transitioning to water-efficient surfaces in parks and educational facilities to reduce water consumption. The residential real estate market in Andalusia is experiencing increased demand for low-maintenance, artificial ground cover for private properties. Sports infrastructure is adapting to water conservation requirements by adopting durable, all-weather playing surfaces. This dual momentum across public sustainability mandates and private convenience preferences underpins Spain’s strong positioning.

Italy Artificial Turf Market Analysis

Italy is predicted to grow in the European market from 2026 to 2034 owing to a blconclude of public infrastructure renewal and tourism driven commercial installations. Public funding initiatives are directing resources toward installing synthetic turf in educational and community spaces, with a focus on areas facing high youth unemployment. Municipalities are increasingly upgrading existing athletic fields to artificial surfaces to enhance usability. The tourism industest is adopting synthetic turf for landscaping in, for example, coastal leisure areas. Hospitality venues are utilizing synthetic grass to maintain green, manicured appearances during periods of water restrictions and high usage. Venice’s municipal authority also deployed synthetic turf in high footfall historic zones to reduce maintenance in sensitive conservation areas. This synergy between public investment and tourism economics sustains Italy’s top five standing.

COMPETITIVE LANDSCAPE

Competition in the Europe artificial turf market is characterized by a mix of established multinational corporations and specialized regional manufacturers vying for dominance through technological differentiation and sustainability credentials. The market features high entest barriers due to stringent product certifications FIFA Quality Pro EN standards and complex public tconcludeer processes. Leading players compete not only on price but on environmental performance durability and after sales digital services. Regulatory pressures particularly around microplastic shedding and conclude of life recyclability are intensifying innovation races. Smaller firms often focus on niche segments such as playgrounds or landscape applications while larger companies tarobtain multi sport municipal and elite sports contracts. Geographic specialization is common with Southern European firms excelling in heat resistant products and Nordic suppliers emphasizing winter durability. This dynamic fosters continuous advancement but also constrains margin flexibility.

KEY MARKET PLAYERS

A few of the dominating players in the Europe artificial turf market are

- Tarkett (FR)

- FieldTurf (CA)

- Limonta Sport Srl

- AstroTurf (US)

- Shaw Sports Turf (US)

- Coastal Turf (US)

- Domo Sports Grass (NL)

- GreenFields (NL)

- SportGroup (DE)

- A-Turf (US)

Top Players In The Market

- Tarkett SA is a France based multinational leader in sustainable flooring and sports surfaces with deep integration across the Europe artificial turf market. The company specializes in high performance synthetic turf systems for football stadiums schools and public spaces. In recent years Tarkett has intensified its focus on circular economy principles launching turf products containing bio based and recycled polymers certified under stringent EU environmental standards. The company also partners with UEFA and national football federations to supply FIFA Quality Pro certified pitches enhancing its reputation for technical excellence and sustainability. Its innovation center in France continually develops infill free and cooling technologies to address urban heat and microplastic concerns shaping next generation European installations.

- FieldTurf a subsidiary of Tarkett Sports operates as a premium brand in the Europe artificial turf market offering advanced infill and fiber technologies tailored for elite and community sports. The company has significantly expanded its footprint by equipping major European football academies national training centers and multi sport municipal complexes. Recently FieldTurf introduced its Ecocept range featuring cork and coconut based infills in response to tightening EU regulations on microplastics. It also launched digital pitch monitoring tools enabling real time performance tracking for facility managers. Collaborations with clubs like Borussia Dortmund and national bodies such as the Football Association of Ireland have reinforced its technical credibility and accelerated adoption across high visibility venues.

- Limonta Sport an Italian manufacturer has established itself as a key European player through vertically integrated production and strong design customization capabilities. The company supplies artificial turf for top tier football stadiums tennis arenas and golf facilities across Southern and Central Europe. Limonta has recently invested in a new production line in Bergamo dedicated to recycled polyethylene fibers aligning with Italy’s National Recovery Plan sustainability mandates. It also pioneered the GreenTech CoolPlus fiber which reduces surface temperatures under direct sunlight a critical innovation for Mediterranean climate zones. Its close collaboration with architects and urban planners has enabled integration of turf into public plazas and landscape architecture beyond traditional sports applications.

Top Strategies Used By The Key Market Participants

Key players in the Europe artificial turf market primarily employ product innovation sustainability integration strategic partnerships and localized manufacturing to strengthen their position. Companies are actively developing infill free and bio based turf systems to comply with evolving EU environmental regulations. They invest in R&D to enhance player safety thermal comfort and recyclability. Strategic collaborations with sports federations municipal authorities and architects ensure specification in high visibility projects. Additionally firms are expanding production capacity within Europe to reduce lead times and logistics emissions while tailoring products to regional climate and regulatory demands. Digital services such as pitch lifecycle monitoring and maintenance analytics further differentiate offerings and foster long term client relationships.

MARKET SEGMENTATION

This research report on the Europe artificial turf market is segmented and sub-segmented into the following categories.

By Application

- Sports

- Landscape

- Playgrounds

- Tennis Courts

- Golf Courses

By Material

- Polyethylene

- Polypropylene

- Nylon

- Other Synthetic Fibers

By End-User

- Residential

- Commercial

- Institutional

- Municipal

By Installation

- Landscape Installation

- Indoor Installation

- Outdoor Installation

- DIY Installation

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply