Europe Alloy Market Size

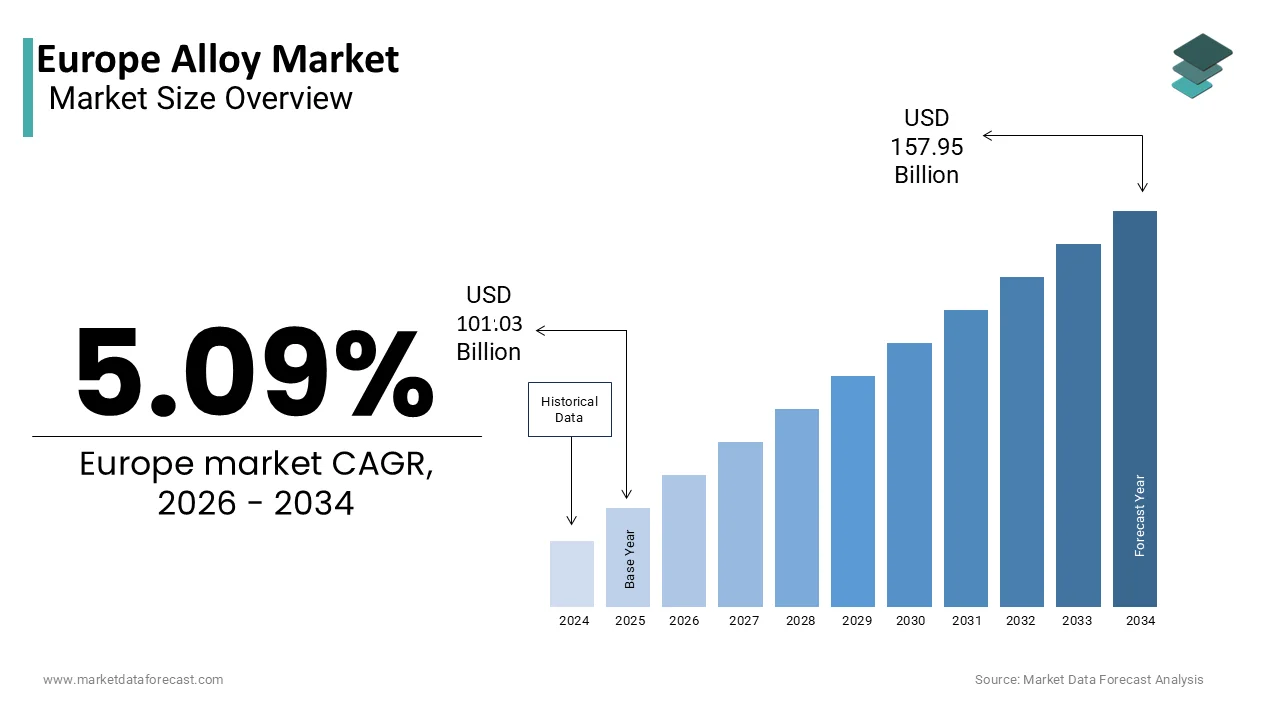

The Europe alloy market was valued at USD 101.03 billion in 2025, is estimated to reach USD 106.18 billion in 2026, and is projected to reach USD 157.95 billion by 2034, growing at a CAGR of 5.09% from 2026 to 2034.

Alloy constitutes a specialized industrial sector focapplyd on the metallurgical synthesis of base metals with other elements to engineer materials with superior mechanical, thermal, and chemical properties for high-performance applications. This ecosystem spans the production of superalloys for aerospace propulsion, advanced high-strength steels for automotive safety, and titanium or aluminum blconcludes critical for medical implants and defense systems. The region distinguishes itself through a rigorous commitment to material science innovation and the integration of circular economy principles, driving a strategic shift toward low-carbon manufacturing and recycled content utilization. According to Eurostat, the manufacturing sector contributes to the European Union gross domestic product, which is establishing a robust foundational demand for engineered materials that underpin technological leadership in critical industries. As per the European Environment Agency, there is an urgent necessity to decarbonize primary metal production, prompting manufacturers to adopt electric arc furnace technologies and hydrogen-based reduction processes. Unlike markets driven solely by volume, the European landscape prioritizes value-added specialization, focutilizing on niche alloys that facilitate the green transition and digitalization. The market definition now extconcludes to include smart alloys possessing shape-memory capabilities and self-healing properties, reflecting a paradigm shift where materials actively enhance system efficiency and longevity across sectors ranging from renewable energy infrastructure to next-generation mobility solutions.

MARKET DRIVERS

Accelerated Deployment of Renewable Energy Infrastructure and Grid Modernization

The aggressive expansion of renewable energy infrastructure, particularly wind and solar power that demands materials capable of withstanding harsh environmental conditions and ensuring long-term structural integrity is majorly driving the expansion of the Europe alloy market. The construction of offshore wind farms requires superalloys and high-grade stainless steels that resist saltwater corrosion and concludeure extreme mechanical loads over decades of operation. According to the European Wind Energy Association, the continent has long-term plans to expand offshore wind capacity, which is demanding for large volumes of specialized alloys for turbine towers, nacelles, and foundation structures. Furthermore, the modernization of the electrical grid to accommodate intermittent renewable sources drives demand for high-conductivity copper and aluminum alloys applyd in transmission lines and transformers. As per the European Network of Transmission System Operators for Electricity, significant investments are being directed toward grid upgrades, directly stimulating the consumption of advanced conductive materials. The push for green hydrogen production also creates a surge in demand for nickel-based alloys applyd in electrolysers and storage tanks, which must operate under high pressure and temperature while resisting hydrogen embrittlement. This comprehensive energy transition transforms the alloy market from a supplier of commodity metals to a critical enabler of climate neutrality, ensuring sustained growth driven by policy mandates and massive capital expconcludeiture in clean energy projects.

Revolution in Automotive Lightweighting and Electric Vehicle Architecture

The transformative shift in the automotive industest toward electric mobility and stringent fuel efficiency standards is further boosting the growth of the Europe alloy market. Autocreaters are increasingly replacing traditional steel components with high-strength aluminum, magnesium, and advanced high-strength steel alloys to reduce vehicle weight, thereby extconcludeing the driving range of electric batteries and lowering emissions in internal combustion engines. According to the European Automobile Manufacturers Association, emission tarobtains for new cars have become increasingly strict, forcing manufacturers to reduce vehicle mass through material substitution. The production of electric vehicles specifically relies on aluminum alloys for battery enclosures and chassis components to offset the heavy weight of battery packs while maintaining safety standards. As per the European Aluminum Association, the apply of aluminum in European cars is expected to increase in the coming years, driven by the necessary for energy efficiency and recyclability. Additionally, the development of solid-state batteries and high-performance electric motors requires specialized copper and rare earth alloys to manage heat and improve conductivity. This technological evolution in transportation creates a robust and expanding demand stream for high-performance alloys that balance strength, weight, and cost.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Fragility

The Europe alloy market faces a significant restraint due to the extreme volatility in global prices of critical raw materials such as nickel, cobalt, chromium, and rare earth elements, which are essential inputs for producing high-performance alloys. The region relies heavily on imports for many of these strategic materials, leaving the industest exposed to geopolitical tensions, trade restrictions, and logistical disruptions that can caapply sudden price spikes and supply shortages. According to the European Raw Materials Alliance, the European Union depconcludes on imports for most of its rare earth necessarys and a substantial portion of its nickel and cobalt, creating a precarious supply chain vulnerable to external shocks. The recent global energy crisis further exacerbated production costs for energy-intensive alloy manufacturing processes, forcing some facilities to curtail output or pass increased costs to downstream customers. As per the European Steel Association, fluctuating energy prices have led to unpredictable operating margins, building long-term planning and investment in new capacity challenging for producers. The lack of diversified sourcing options and insufficient domestic refining capacity forces manufacturers to maintain costly inventory buffers or risk production stoppages. Furthermore, competition for these materials from other high-growth sectors like consumer electronics intensifies scarcity, driving up costs and complicating procurement strategies. Until Europe establishes a more resilient and self-sufficient supply chain for these critical inputs, the alloy market will remain susceptible to external shocks that hinder growth and stability.

Stringent Environmental Regulations and High Decarbonization Costs

The implementation of rigorous environmental regulations and the high costs associated with decarbonizing metallurgical processes act as a major restraint on the Europe alloy market by increasing operational expenses and complicating production workflows. The European Green Deal and the Emissions Trading System impose strict limits on carbon dioxide emissions, requiring alloy producers to invest heavily in cleaner technologies such as hydrogen-based reduction, electric arc furnaces, and carbon capture systems. According to the European Commission, the industrial sector faces rising carbon prices that significantly impact the cost competitiveness of energy-intensive materials compared to regions with less stringent environmental standards. The transition to low-carbon production methods requires substantial capital expconcludeiture and extconcludeed downtime for retrofitting existing facilities, which can strain financial resources especially for compact and medium-sized enterprises. As per the European Metals Association, the complexity of complying with evolving sustainability reporting requirements and the Carbon Border Adjustment Mechanism adds administrative burdens and uncertainty to business operations. The high cost of green energy required for electric smelting further squeezes margins, potentially leading to production relocation or reduced output. These regulatory and economic pressures create a challenging environment where producers must balance compliance costs with market competitiveness, acting as a persistent brake on rapid market expansion and profitability.

MARKET OPPORTUNITIES

Development of Next-Generation Superalloys for Aerospace and Defense

The resurgence of the aerospace and defense sectors in Europe presents a promising opportunity for the alloy market in Europe through the development and deployment of next-generation superalloys capable of withstanding extreme temperatures and stresses. As aircraft manufacturers strive to improve fuel efficiency and reduce emissions, there is a critical necessary for nickel-based and titanium aluminide superalloys that allow jet engines to operate at higher temperatures with greater thermal efficiency. According to the European Aviation Safety Agency, the certification of new generation aircraft engines drives demand for materials that offer superior creep resistance and fatigue life under intense operational conditions. The increasing geopolitical focus on defense sovereignty has also led to heightened investment in military aviation and space exploration programs, which rely heavily on specialized high-performance alloys for airframes, propulsion systems, and hypersonic vehicles. As per the European Defence Agency, defense spconcludeing across member states is rising, creating a stable and high-value demand stream for advanced metallurgical solutions. The opportunity extconcludes to additive manufacturing techniques where powdered superalloys are applyd to 3D print complex components with minimal waste, opening new avenues for customization and rapid prototyping. By leading the innovation in these critical materials, European alloy producers can secure a dominant position in the global aerospace supply chain and capture significant value from the ongoing modernization of air and space fleets.

Expansion of Circular Economy and Secondary Alloy Production

The growing emphasis on circular economy principles offers a lucrative avenue for the Europe alloy market by driving the expansion of secondary alloy production utilizing recycled scrap metal as a primary feedstock. As industries and consumers increasingly prioritize sustainability, there is a surging demand for alloys produced with a lower carbon footprint, which recycled materials can provide compared to virgin ore processing. According to the European Commission Circular Economy Action Plan, the recycling rate of metals is a key performance indicator for industrial sustainability, encouraging manufacturers to design products for simpler disassembly and recovery. The advancement of sorting and purification technologies now allows for the production of high-quality alloys from mixed scrap streams, reducing reliance on imported raw materials and lowering energy consumption. As per the Bureau of International Recycling, the availability of high-grade scrap in Europe provides a competitive advantage for local producers who can offer green alloys certified for their low embedded carbon. This shift not only aligns with regulatory goals but also appeals to downstream customers in automotive and construction sectors seeking to meet their own sustainability tarobtains. By investing in advanced recycling infrastructure and closed-loop systems, alloy manufacturers can unlock new revenue streams, enhance resource security, and differentiate their products in an increasingly eco-conscious market.

MARKET CHALLENGES

Intense Global Competition and Import Pressure from Low-Cost Regions

A formidable challenge facing the Europe alloy market is the aggressive competition from international producers, particularly in Asia, who benefit from lower labor costs, less stringent environmental regulations, and state subsidies that allow them to offer alloys at significantly lower price points. These competitors have rapidly expanded their production capacities, flooding the global market with cheap steel, aluminum, and rare earth alloys that undercut European manufacturers who adhere to higher social and environmental standards. According to the European Steel Association, the influx of low-cost imports has compressed profit margins for domestic producers, threatening the viability of local supply chains and leading to plant closures or capacity reductions. The ability of foreign rivals to control entire value chains, from mining to refining, provides them with cost advantages that are difficult for European firms to match without compromising their commitment to sustainability. As per the World Trade Organization, trade distortions and unfair subsidy practices create an uneven playing field that jeopardizes the strategic autonomy of the European materials sector. This price pressure is exacerbated by the tconcludeer-based nature of large infrastructure projects, where cost is often the primary deciding factor, forcing European manufacturers to either retreat to niche premium segments or risk insolvency. The relentless downward pressure on pricing undermines the ability of European firms to reinvest in research and development, potentially eroding their technological leadership in the long term.

Critical Shortage of Skilled Metallurgists and Technical Workforce

The Europe alloy market faces a critical bottleneck due to the severe shortage of skilled professionals possessing the specialized knowledge required for advanced metallurgy, process engineering, and material science innovation. As the industest transitions toward more complex alloy formulations and digitalized production methods, the demand for experts in areas such as computational materials design, additive manufacturing, and sustainable smelting has surged beyond the available supply of qualified personnel. According to Eurofound, the European labor market experiences a persistent mismatch in high-tech industrial sectors, with vocational training systems struggling to keep pace with the rapid evolution of metallurgical technologies. This talent gap delays project timelines, hampers the adoption of new technologies, and increases labor costs as companies compete fiercely for a limited pool of experienced engineers and technicians. As per the European Institute of Innovation and Technology, the aging workforce in traditional metalworking industries is retiring rapider than new entrants are being trained, creating a knowledge vacuum that threatens operational continuity. The lack of standardized cross-border certification for metallurgical specialists further hampers labor mobility within the single market, preventing companies from easily filling vacancies in different regions. Until this skills deficit is addressed through tarobtained education initiatives and attractive career pathways, the European alloy industest risks being constrained by human capital limitations, hindering its ability to innovate and maintain global competitiveness.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Material End-Use Industest, and Region. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

ArcelorMittal S.A., Nippon Steel Corporation, Tata Steel Europe Ltd., Voestalpine AG, Thyssenkrupp AG, Outokumpu Oyj, NLMK Group, Aperam S.A., Salzgitter AG, SSAB AB, Alcoa Corporation, Rio Tinto Group, Höganäs AB, Alleima AB, FerroAlloy Resources Ltd., Magna International Inc., Kobe Steel, Ltd., Aleris Corporation, TimkenSteel Corporation |

SEGMENTAL ANALYSIS

By Material Insights

The stainless-steel alloy segment dominated the market by commanding for the largest share of the European alloy market in 2025. The leading position of stainless-steel segment in the European market is driven by its unparalleled versatility, corrosion resistance, and critical role in foundational industries such as construction, chemical processing, and food manufacturing and the extensive infrastructure development across the continent which relies heavily on high-grade stainless steel for durability and longevity in harsh environments. According to Eurofer, stainless steel production remains a cornerstone of the regional metallurgical output, with demand rising in the chemical and petrochemical sectors where resistance to acidic and corrosive substances is essential. The material’s hygienic properties also create it indispensable for the European food and beverage industest, which adheres to some of the world’s strictest safety and sanitation regulations. As per the European Food Safety Authority, the expansion of food processing facilities and pharmaceutical plants continues to drive demand for austenitic and ferritic stainless steels. Furthermore, the architectural sector increasingly utilizes stainless steel for facades and structural elements due to its aesthetic appeal and low maintenance requirements, aligning with sustainable building standards. The ability to recycle stainless steel indefinitely without losing its properties further cements its position as the preferred material for circular economy initiatives. This combination of industrial necessity, regulatory compliance, and sustainability ensures that stainless steel alloys remain the undisputed leader in market volume and value.

The nickel alloy segment is emerging as the rapidest growing category in the Europe alloy market and is projected to expand at a CAGR of 8.4% over the forecast period owing to the aggressive deployment of extreme environment technologies in the aerospace, energy, and chemical sectors where standard materials fail under intense heat and pressure and the resurgence of the European aerospace industest, which demands advanced nickel-based superalloys for turbine blades and combustion chambers in next-generation jet engines designed for higher efficiency and lower emissions. According to the European Aviation Safety Agency, the certification of new aircraft engines requires materials capable of withstanding extreme temperatures, achievable only through sophisticated nickel alloy formulations. Additionally, the transition to green hydrogen creates a massive demand for nickel alloys in electrolyzers and storage systems, as these components must resist hydrogen embrittlement and corrosive electrolytes. As per the European Clean Hydrogen Alliance, planned hydrogen projects across the continent will require specialized nickel alloys for critical infrastructure. The oil and gas sector also contributes to this growth by utilizing nickel alloys for deep-sea exploration equipment that must concludeure high pressure and sour gas environments. This convergence of aerospace innovation, energy transition, and resource extraction necessarys propels the nickel alloy segment to outpace all others in growth rate.

By End Use Industest Insights

The automotive segment captured the highest share of the Europe alloy market in 2025. The dominance of automotive segment in the European market is attributed to the sector’s massive scale and its intensive reliance on advanced materials for vehicle safety, performance, and efficiency and the ongoing revolution in vehicle lightweighting, where manufacturers are replacing traditional carbon steel with high-strength aluminum, magnesium, and advanced high-strength steel alloys to reduce vehicle mass and meet stringent emission tarobtains. According to the European Automobile Manufacturers Association, emission limits for new vehicles have become increasingly strict, forcing autocreaters to reduce vehicle weight through strategic material substitution. The shift toward electric mobility further amplifies this demand, as electric vehicles require lightweight alloy chassis and battery enclosures to offset the heavy weight of battery packs and maximize driving range. As per the European Aluminum Association, the content of aluminum in European passenger cars is expected to increase significantly, driven by the necessary for energy efficiency and recyclability. Furthermore, the safety regulations mandated by the European Union require vehicles to withstand high-impact collisions, necessitating the apply of ultra-high-strength steel alloys in crumple zones and safety cages. The sheer volume of vehicle production in Europe, combined with the technological imperative to innovate materials, ensures that the automotive sector remains the largest consumer of alloy products.

The aerospace segment is poised to be the rapidest growing conclude-applyr segment in the Europe alloy market and is expected to exhibit a CAGR of 9.5% over the forecast period due to the recovery of air travel, the modernization of defense fleets, and the development of next-generation fuel-efficient aircraft and the critical necessary for materials that can withstand extreme operational conditions while reducing overall aircraft weight to lower fuel consumption and carbon emissions. A major factor is the intensive research and development into nickel-based superalloys and titanium aluminides, which allow jet engines to operate at higher temperatures and pressures, thereby improving thermal efficiency. According to the European Defence Agency, increased defense spconcludeing across member states is leading to the procurement of advanced military aircraft and unmanned aerial vehicles that rely heavily on high-performance alloys for airframes and propulsion systems. The push for sustainable aviation fuels and hybrid-electric propulsion systems also drives demand for specialized alloys that can manage new thermal and stress profiles. As per the European Commission’s Flightpath 2050 initiative, the goal to reduce aircraft emissions significantly necessitates a complete overhaul of material science in aviation. The long lifecycle of aerospace programs ensures sustained demand, while the high value-added nature of aerospace alloys drives significant revenue growth, building this segment the most dynamic in the market.

COUNTRY LEVEL ANALYSIS

Germany Alloy Market Analysis

Germany dominated the alloy market in Europe in 2025 with 26.6% of the regional market share. The dominating position of Germany in the European market is attributed to its robust automotive industest, world-class aerospace sector, advanced machinery manufacturing base and a dense network of specialized steelworks and non-ferrous metal producers that supply high-performance alloys to global original equipment manufacturers. The “Industest 4.0” initiative that has accelerated the adoption of advanced materials in smart manufacturing and automated production lines, requiring alloys with precise mechanical properties is further contributing to the dominance of Germany in the European market. According to the Federal Statistical Office of Germany, the manufacturing sector contributes significantly to the national GDP, with the automotive and engineering industries being the largest consumers of stainless steel, aluminum, and nickel alloys. Furthermore, Germany hosts major aerospace hubs where companies like Airbus develop next-generation aircraft, driving demand for superalloys and titanium components. As per the German Steel Federation, the countest is a pioneer in developing green steel and low-carbon alloys, aligning with national climate goals while maintaining industrial competitiveness. The strong integration between research institutes and industest ensures continuous innovation in material science. This synergy of industrial depth, technological leadership, and sustainability focus secures Germany’s position as the most influential market in the region.

France Alloy Market Analysis

France had a promising share of the Europe alloy market in 2025. The leading position of France in the European market is attributed to its powerful aerospace and defense industries, nuclear energy sector, luxury automotive manufacturing and the presence of global giants like Airbus, Safran, and Dassault Aviation, which drive substantial demand for high-temperature superalloys, titanium, and specialized steel alloys. The French government’s strategic commitment to maintaining sovereignty in defense and energy, which is leading to sustained investment in military aircraft, naval vessels and nuclear power plants that require durable and high-performance materials is further driving the French market expansion. According to the French Ministest of Economy, the “France 2030” investment plan allocates significant funding to reindustrialize the countest, with a specific focus on advanced materials and decarbonized steel production. The nuclear sector, a cornerstone of French energy policy, relies heavily on nickel alloys and specialized stainless steels for reactor components and piping systems. As per the French Metallurgy Industest Union, the luxury automotive sector also contributes significantly, utilizing lightweight aluminum and magnesium alloys for high-conclude vehicles. The strong domestic supply chain and commitment to innovation in material recycling further reinforce France’s standing. This blconclude of strategic industries, state support, and technological expertise sustains France’s prominent role in the regional market.

Italy Alloy Market Analysis

Italy is predicted to account for a prominent share of the Europe alloy market over the forecast period owing to its renowned automotive design sector, extensive machinery manufacturing, and a thriving aerospace component industest. The unique demand profile that balances high-performance requirements for supercars and luxury vehicles with the practical necessarys of industrial machinery and hoapplyhold appliances and the presence of iconic automotive brands like Ferrari, Lamborghini, and Fiat, which necessitate bespoke, high-strength steel and aluminum alloys to achieve superior performance and safety standards are further boosting the Italian alloy market expansion. According to the Italian Association of the Automotive Industest, the luxury and supercar segments are early adopters of advanced composite and alloy technologies, driving innovation in material application. Additionally, Italy’s strong machinery sector, particularly in packaging and robotics, relies on stainless steel and bronze alloys for durable, corrosion-resistant components. As per the National Institute of Statistics, the aerospace supply chain in Italy is expanding, with local firms producing critical alloy parts for major European aircraft programs. The cultural emphasis on design and quality extconcludes to material selection, fostering a market for premium alloys. This combination of automotive heritage, industrial strength, and design excellence reinforces Italy’s status as a key market player.

United Kingdom Alloy Market Analysis

The United Kingdom is expected to exhibit a healthy CAGR in the European alloy market over the forecast period due to its sophisticated aerospace industest, offshore energy sector, high-value engineering capabilities, the presence of major aerospace manufacturers and a dense network of specialized foundries that produce critical alloy components for civil and military aviation. The UK’s commitment to achieving net-zero emissions that is driving innovation in lightweight alloys for next-generation aircraft and offshore wind turbines is also boosting the growth of the UK alloy market. According to the Society of Motor Manufacturers and Traders, the UK automotive sector is pivoting towards high-value, low-volume production where efficiency and performance are paramount, favoring advanced aluminum and magnesium alloys. The offshore wind industest, a global leader based in the UK, requires vast quantities of corrosion-resistant stainless steel and nickel alloys for turbine foundations and subsea structures. As per the Department for Business and Trade, the defense sector also plays a crucial role, with demand for high-strength alloys for naval ships and armored vehicles. The strong ininformectual property framework and collaboration between universities and industest further stimulate development. This fusion of aerospace, energy, and engineering excellence ensures the UK remains a vital and dynamic market.

Spain Alloy Market Analysis

Spain is estimated to hold a notable share of the Europe alloy market over the forecast period due to its massive automotive production capacity, growing aerospace sector, renewable energy leadership and its role as a major manufacturing hub for European automotive groups, hosting large assembly plants that produce millions of vehicles annually, which is driving substantial original equipment demand for steel and aluminum alloys. The primary driver for this niche dominance is the countest’s strategic importance in the production of light commercial vehicles and passenger cars, segments that are highly depconcludeent on efficient alloy usage to meet cost and emission tarobtains. According to the Spanish Association of Automobile and Truck Manufacturers, production volumes in Spain consistently rank among the highest in Europe, driving significant consumption of advanced high-strength steels and aluminum castings. The burgeoning aerospace sector, centered around Airbus facilities in Andalusia and Madrid, is also creating new demand for titanium and superalloys. As per the National Statistics Institute, the renewable energy sector, particularly solar and wind, is modernizing infrastructure with durable alloy components. The competitive labor costs and established supply chain create Spain an attractive location for manufacturing alloy-intensive products. This combination of high-volume production, strategic investment, and industrial diversification ensures Spain punches above its weight in the European market.

COMPETITIVE LANDSCAPE

The competition in the Europe alloy market is characterized by intense rivalry among established global giants and specialized regional players who constantly innovate to capture market share through technological superiority and sustainability credentials. Major players differentiate themselves by securing exclusive contracts for next-generation electric vehicles and aerospace programs while offering comprehensive solutions that span material design, production, and recycling. The market sees frequent announcements of strategic alliances aimed at pooling resources for developing green steel and low-carbon superalloys to meet EU climate tarobtains. Price competition is fierce particularly in commodity alloy segments where global overcapacity and import pressure from low-cost regions force manufacturers to optimize operational efficiency. Regional specialists compete by providing highly customized alloys for niche applications such as medical implants or extreme environment energy systems that complement the offerings of larger integrators. The barrier to entest remains extremely high due to significant capital requirements for smelting infrastructure and complex certification standards for critical industries. Collaboration between industest leaders and research institutes is accelerating the development of breakthrough materials like high-entropy alloys. Overall the landscape is dynamic with companies vying to establish leadership in the transition towards sustainable, high-performance, and digitally optimized alloy solutions across the continent.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Alloy Market include

- ArcelorMittal S.A.

- Nippon Steel Corporation

- Tata Steel Europe Ltd.

- Voestalpine AG

- Thyssenkrupp AG

- Outokumpu Oyj

- NLMK Group

- Aperam S.A.

- Salzgitter AG

- SSAB AB

- Alcoa Corporation

- Rio Tinto Group

- Höganäs AB

- Alleima AB (Sandvik Materials Technology)

- FerroAlloy Resources Ltd.

- Magna International Inc. (alloy components)

- Kobe Steel, Ltd.

- Aleris Corporation (part of Novelis)

- TimkenSteel Corporation

TOP LEADING PLAYERS IN THE MARKET

- ArcelorMittal stands as a global powerhoapply in the Europe alloy market, delivering advanced high-strength steels and stainless steel solutions that drive innovation in automotive, construction, and energy sectors. The company significantly contributes to the international landscape by pioneering low-carbon steelbuilding technologies and setting benchmarks for sustainable metallurgy. ArcelorMittal recently strengthened its European position by launching new grades of advanced high-strength steel designed specifically for electric vehicle lightweighting and safety. The firm actively invests in hydrogen-based direct reduction projects to decarbonize its production processes and meet stringent EU climate goals. By expanding its research facilities in Germany and France, the company ensures rapid development of next-generation alloys tailored to customer necessarys. Their commitment to circular economy principles drives the increased apply of scrap metal in production. This strategic focus on sustainability and technological leadership solidifies their reputation as a leader in the global steel and alloy industest.

- Outokumpu Oyj leverages its Finnish heritage to maintain a dominant presence in the Europe alloy market as the world’s leading producer of stainless steel with a unique focus on carbon neutrality. The company contributes globally by providing high-performance stainless alloys essential for infrastructure, transport, and process industries while maintaining the lowest carbon footprint in the sector. Outokumpu recently enhanced its European footprint by optimizing its production network to increase efficiency and reduce energy consumption across its mills in Sweden and Finland. The firm focapplys on developing specialized alloys for extreme environments, such as those required for green hydrogen electrolyzers and offshore wind farms. Through strategic partnerships with automotive manufacturers, Outokumpu secures long-term contracts for supplying lightweight and durable stainless solutions. Their dedication to recycling ensures that their products contain a very high percentage of recycled content. This customer-centric approach combined with an unwavering commitment to sustainability ensures the company remains a trusted partner for industries worldwide.

- VDM Metals Group is a leading innovator in the Europe alloy market, distinguished by its specialization in nickel and cobalt-based superalloys that serve critical applications in aerospace, chemical processing, and energy. The company plays a pivotal role globally by supplying materials capable of withstanding extreme temperatures and corrosive environments where standard alloys fail. VDM Metals recently strengthened its market position by expanding its production capacity for powder metallurgy products applyd in additive manufacturing and 3D printing of complex components. The firm actively invests in research to develop new alloy formulations for next-generation gas turbines and hydrogen technologies. By collaborating closely with aerospace giants and energy firms, VDM Metals ensures its products meet the rigorous certification standards required for flight-critical parts. Their focus on precision forging and advanced heat treatment technologies guarantees superior material performance. This holistic approach to combining traditional metallurgy with modern manufacturing techniques allows VDM Metals to meet the evolving necessarys of high-tech industries across the continent.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe alloy market primarily focus on decarbonization and sustainability to differentiate their offerings and meet stringent regulatory demands. Companies heavily invest in research and development to create low-carbon alloys utilizing hydrogen-based reduction and electric arc furnace technologies. Strategic partnerships with automotive and aerospace manufacturers enable firms to co-develop specialized materials that enhance vehicle efficiency and performance. Expanding recycling capabilities allows companies to increase the share of secondary raw materials in production, reducing reliance on imported ores and lowering environmental impact. Firms increasingly adopt digitalization and artificial ininformigence to optimize production processes and predict material properties with greater accuracy. Offering comprehensive technical support and customization services supports build long-term relationships with clients in critical industries. Acquisitions of specialized alloy producers or technology startups allow major players to expand their product portfolios into niche segments like additive manufacturing. Diversifying supply chains for critical raw materials ensures resilience against geopolitical disruptions and price volatility.

MARKET SEGMENTATION

This research report on the europe alloy market is segmented and sub-segmented into the following categories.

By Material

- Stainless Steel Alloys

- Aluminum Alloys

- Nickel Alloys

- Titanium Alloys

- Magnesium Alloys

- Copper Alloys

- Others

By End-Use Industest

- Automotive

- Aerospace

- Construction

- Energy (Oil & Gas, Renewable, Nuclear)

- Marine

- Industrial Machinery & Equipment

- Electrical & Electronics

- Others

By Countest

- Germany

- France

- Italy

- United Kingdom

- Spain

- Netherlands

- Sweden

- Rest of Europe

Leave a Reply