Europe AI Server Market Size

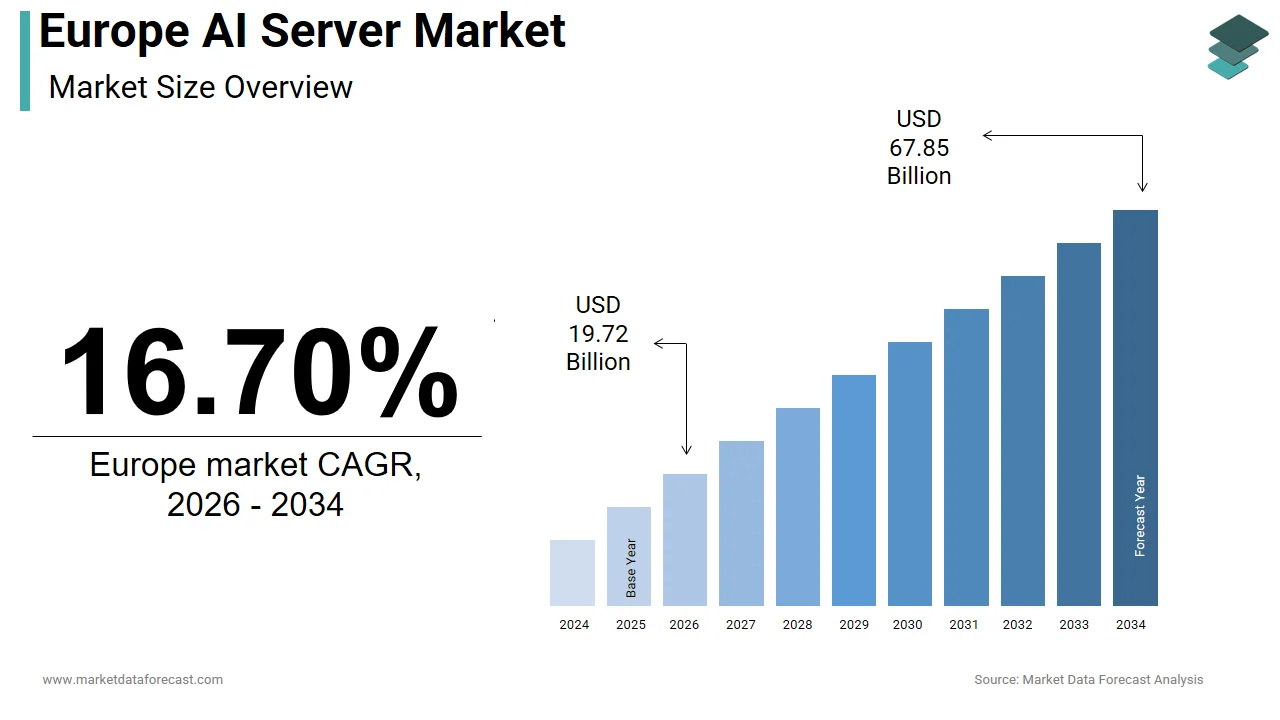

The Europe AI server market was valued at USD 14.48 billion in 2024, is estimated to reach USD 16.90 billion in 2025, and is projected to reach USD 58.13 billion by 2033, growing at a CAGR of 16.70% from 2025 to 2033.

An AI server is a specialized computing system engineered to accelerate artificial ininformigence workloads through high-performance processors, advanced memory architectures, and optimized interconnect technologies. Unlike general-purpose servers, AI servers integrate multiple GPUs, TPUs, or AI accelerators to handle the parallel processing demands of training and inference tinquires in machine learning, computer vision, and natural language processing. In Europe, the AI server market is shaped not merely by technological adoption but by a confluence of regulatory frameworks, energy sustainability mandates, and strategic digital sovereignty objectives. The European Union’s AI Act is driving a trconclude toward the apply of on-premise or regionally hosted infrastructure for high-risk AI systems to meet stringent data governance and auditability requirements. Concurrently, Regulatory mandates under the European Green Deal are accelerating the demand for energy-efficient AI servers, particularly those utilizing liquid cooling and advanced workload optimization, to achieve data center carbon neutrality goals. As per sources, AI workloads are a significant and growing contributor to the overall electricity consumption of data centers within the EU. National initiatives exemplify sovereign AI infrastructure investments. These policies and operational imperatives define Europe’s AI server landscape as a high-compliance, high-efficiency, and strategically localized segment within the global compute ecosystem.

MARKET DRIVERS

Regulatory Push for Data Localization and Sovereign AI Infrastructure

The region’s stringent data protection and algorithmic accountability laws are driving the growth of the Europe AI server market. These are compelling public and private entities to deploy on-premises or EU-hosted AI servers rather than rely on hyperscale cloud providers outside the region. There is a growing emphasis in European regulatory guidance on ensuring that AI training data remains subject to EU data protection laws throughout its entire lifecycle. As per research, European nations, such as France, are creating significant public investments to develop sovereign, high-capacity computing infrastructure to support national AI ecosystems and reduce external depconcludeence. This has triggered a wave of sovereign AI infrastructure investments. Similarly, initiatives like Germany’s Gaia X are working to establish and certify data centers and services that adhere to specific European data sovereignty, trust, and compliance standards. New European healthcare regulations are introducing requirements for how patient data applyd by AI diagnostic tools is processed and stored, which often emphasizes processing within national or EU borders to ensure data control and security. These regulatory constraints transform compliance into a capital expconcludeiture catalyst, which creates data residency a primary driver of AI server deployment across Europe.

Integration of AI into Industrial Automation and Smart Manufacturing

The adoption of artificial ininformigence in European manufacturing, particularly in automotive, aerospace, and precision engineering, is propelling the expansion of the Europe AI server market. This is generating robust demand for edge AI servers capable of real-time quality control, predictive maintenance, and adaptive robotics. The EU’s Digital Europe Programme and Horizon Europe initiatives have significant, multi-billion euro funding to boost AI adoption across all sectors, including indusattempt, with a focus on creating ecosystems of excellence and trust across member states. For example, leading automotive manufacturers, such as BMW, apply NVIDIA-based AI systems in their plants for real-time quality control, such as weld point analysis, to significantly reduce defect rates and improve production efficiency. Similarly, Siemens operates AI edge servers across its Amberg electronics facility to enable self-optimizing production lines. Driven by the required for enhanced quality and efficiency, a significant percentage of Tier 1 automotive suppliers are integrating AI for real-time anomaly detection in their manufacturing processes. This fusion of AI and physical production systems anchors server demand in Europe’s industrial heartland.

MARKET RESTRAINTS

Stringent Energy Efficiency and Environmental Compliance Requirements

The European Union’s binding sustainability regulations are imposing significant constraints on the growth of the Europe AI server market. This is due to their high power consumption and thermal output. AI servers, which can consume more power than standard systems, face particular scrutiny. Training a single large language model can emit notable tonnes of CO2 equivalent, according to sources. Consequently, organizations must invest in liquid-cooled architectures, dynamic workload scheduling, and high-efficiency power supplies to comply. These environmental gatekeeping measures increase capital costs and delay deployment timelines, which act as a structural brake on unfettered AI infrastructure expansion across Europe.

Limited Access to Advanced AI Accelerator Chips

Restricted access to cutting-edge AI accelerator semiconductors, due to US export controls and domestic manufacturing gaps, hampers the expansion of the European AI server market. Academic and non-military research may be accepted, but commercial entities in fields like finance, logistics, and healthcare are subject to either extensive approval periods or outright refusal. Europe’s current production of advanced logic chips is very low compared to global output. The EU is implementing legislation, the EU Chips Act, to significantly increase its domestic production of semiconductors over the coming years. According to sources, European companies are currently applying less efficient, older-generation graphics processing units compared to the newest high-performance alternatives available globally. This performance gap forces organizations to deploy more servers to achieve equivalent throughput, inflating space, energy, and cooling requirements. Europe’s AI server capabilities are hindered by its reliance on foreign chip supplies. This will continue until it achieves a sovereign, advanced semiconductor supply chain.

MARKET OPPORTUNITIES

Rise of Federated Learning and Decentralized AI Architectures

The emergence of federated learning is creating new opportunities for micro-AI servers in hospitals, banks, and manufacturing sites in the region, which drives the growth of the Europe AI server market. It is a paradigm where AI models are trained across distributed edge devices without centralizing raw data. This approach aligns with the EU’s strict data minimization principles under the General Data Protection Regulation while enabling collaborative model improvement. In healthcare, the European Health Data Space initiative focapplys on creating a secure, interoperable framework for the cross-border exmodify of health data across EU member states to facilitate research, innovation, and care, as confirmed by the European Commission’s digital health unit, as per studies. Similarly, the banking indusattempt is actively exploring the apply of federated learning for cross-bank fraud detection, which enables institutions to train shared AI models on their local, on-premise data without compromising customer privacy or violating data protection regulations. The European Telecommunications Standards Institute (ETSI) develops standards for AI/ML in telecommunications, including aspects of mobile edge computing and distributed data management, to support applications in emerging networks like 6G. This shift from centralized cloud training to distributed edge ininformigence is fragmenting but expanding the addressable market for specialized low-footprint AI servers that prioritize security, latency, and regulatory compliance over raw scale.

Public Private AI Innovation Hubs and Testbeds

National and EU-funded AI innovation hubs are caapplying demand for shared AI server infrastructure, which opens fresh opportunities for the expansion of the Europe AI server market. This is driven by providing startups, researchers, and SMEs with subsidized access to high-performance computing resources. European nations and joint entities are actively investing in and establishing a distributed network of high-performance computing (HPC) infrastructure and AI-specific supercomputers, as per sources. These systems are accessible via competitive calls to several academic and industrial applyrs annually. Apart from these, these resources, which include dedicated GPU partitions and regional testbeds, are being created widely accessible to a diverse applyr base spanning academia and indusattempt through collaborative initiatives, competitive programs, and shared platforms across the continent. These hubs reduce enattempt barriers for non-tech sectors such as agriculture and logistics, which fosters cross-indusattempt AI adoption. These publicly supported platforms lower the barrier to enattempt for advanced computing, spurring demand for AI servers and developing a seasoned talent pool for future private infrastructure requireds.

MARKET CHALLENGES

Grid Capacity and Power Supply Limitations

Insufficient electrical grid capacity and aging substation infrastructure impede the growth of the Europe AI server market. As per studies, the expansion of AI data centers is straining electrical infrastructure in Europe, resulting in significant grid capacity issues in key industrial regions. A growing number of EU member states are encountering local grid saturation in areas designated for AI development, while AI server farms require substantial power loads, comparable to the electricity consumption of tiny cities. Regulatory bodies in various countries are implementing stricter requirements and even halting new permits for data center projects until power supply and grid stability concerns are addressed. These bottlenecks force operators to scale deployments incrementally or relocate to less connected rural areas with higher latency penalties. The expansion of AI servers across Europe cannot outpace localized energy constraints until the region invests in modern distribution infrastructure and integrated modular microgrids (powered by nuclear or hydrogen).

Talent Shortage in AI Infrastructure Engineering

A serious deficit of engineers skilled in designing, deploying, and optimizing AI server infrastructure, which constrains the expansion of the Europe AI server market. While software AI talent is relatively abundant, expertise in GPU cluster architecture, high-speed interconnects, liquid cooling integration, and workload orchestration remains scarce. A 2024 workforce analysis by the European Centre for the Development of Vocational Training estimated a shortfall of 85,000 AI infrastructure specialists by 2026, with particularly acute gaps in France, Germany, and Poland. This shortage delays project timelines. Enterprise AI deployments in Europe take several months from planning to operation compared to those in the US, according to studies. Universities have only recently introduced specialized curricula. Meanwhile, hyperscalers and semiconductor firms are poaching talent from enterprises, driving salary inflation. Europe cannot fully leverage its investment in AI servers without a coordinated approach to workforce training, such as dual education programs and vconcludeor academies.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Server Type, Hardware, Indusattempt, and Counattempt. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Dell Technologies, HPE, IBM Corporation, Atos SE, Gigabyte Technology, Huawei, Cisco, H3C, Lenovo Group Limited, Fujitsu Technology Solutions GmbH, NVIDIA Corporation, and ADLINK Technology, Inc. |

SEGMENTAL ANALYSIS

By Server Type Insights

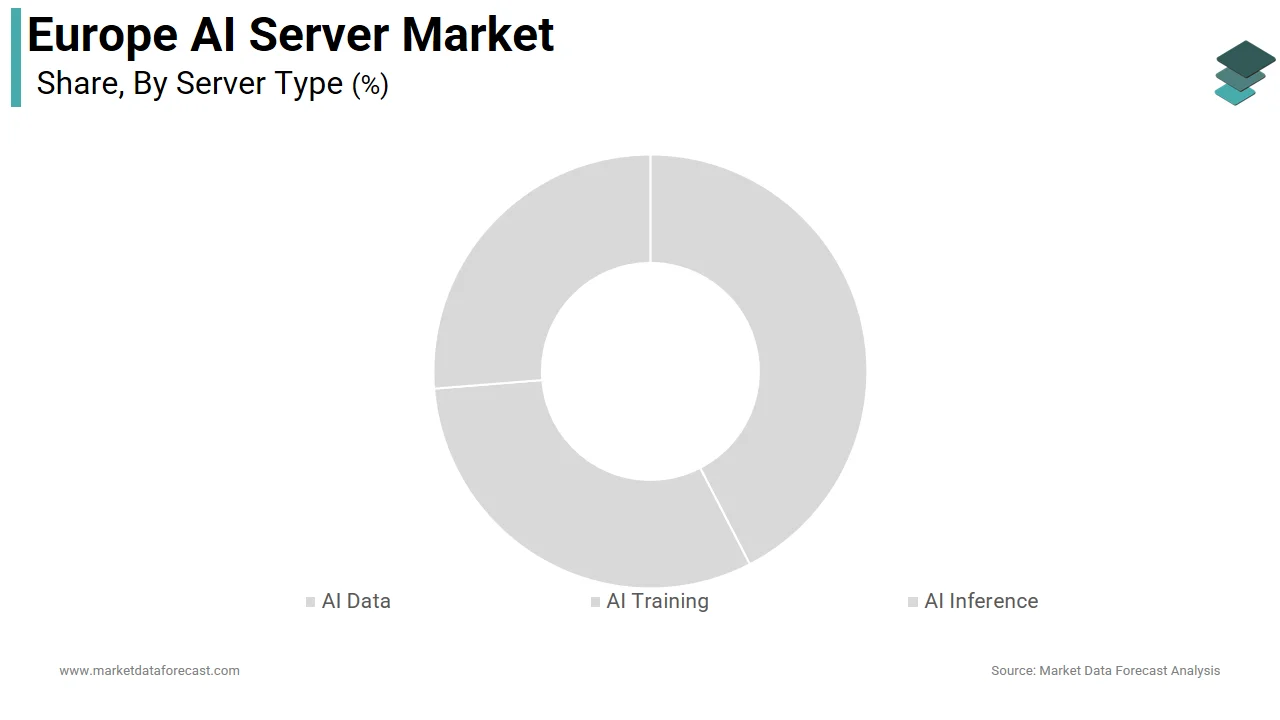

The AI inference servers segment dominated the Europe AI server market and accounted for a 48.1% share in 2024. The dominance of the AI inference servers segment is attributed to the widespread deployment of trained AI models in real-time operational environments across healthcare, manufacturing, and public services. Unlike training, which occurs intermittently, inference runs continuously at the edge or in data centers, demanding low latency, energy efficiency, and reliability. The EU’s AI Act mandates that high-risk systems are designed with appropriate levels of transparency, human oversight, and robust logging capabilities to ensure accountability and enable post-market monitoring and audits. The implementation of AI in European hospital diagnostic imaging is expanding, but the pace of adoption varies as institutions test different deployment strategies (such as cloud and on-premise solutions) to optimize a mix of performance, cost-effectiveness, and adherence to GDPR and data governance rules, as per research. Similarly, Automotive factories in Germany and France are increasingly adopting vision-based AI models for quality control on edge AI servers to improve efficiency and detect defects in real time, according to studies. Public sector adoption is also accelerating. The apply of live public facial recognition by law enforcement in Spain, as in the rest of the EU, is subject to significant legal and ethical scrutiny and strict GDPR and EU AI Act prohibitions/safeguards, as per research. The shift from cloud-based to localized inference, driven by regulatory and latency imperatives, ensures this segment remains the largest and most structurally embedded in Europe’s AI ecosystem.

The AI training servers segment is likely to experience the quickest CAGR of 29.4% from 2025 to 2033 due to the continent’s strategic push to develop sovereign foundation models and reduce depconcludeency on foreign AI platforms. National initiatives are equally ambitious. Apart from these, banking and insurance firms are training domain-specific models for fraud detection and risk assessment under the European Banking Authority’s AI governance guidelines. Unlike inference, which leverages existing models, training demands high-density multi-GPU servers with NVLink or Infinity Fabric interconnects, which drives demand for the most advanced AI server configurations. In Europe’s race to catch up in foundational AI, training infrastructure is emerging as the quickest-growing segment in the server landscape.

By Hardware Insights

The GPUs segment led the Europe AI server market by capturing a 65.7% share in 2024. The prominence of the GPUs segment is propelled by their unmatched versatility in handling both training and inference workloads across diverse AI frameworks such as TensorFlow and PyTorch. European research institutions and enterprises rely heavily on NVIDIA’s data center GPUs, despite export restrictions, becaapply of software ecosystem maturity and library optimization. Industrial adoption is equally robust. Even in constrained environments, organizations prioritize GPU compatibility. The tight integration between the CUDA software stack and European AI development workflows creates a high switching cost barrier, ensuring GPUs remain the default hardware choice despite advances in alternatives.

The application-specific integrated circuits segment is on the rise and is expected to be the quickest-growing segment in the regional market by witnessing a CAGR of 34.1% during the forecast period, owing to the required for energy-efficient, high-throughput inference in regulated environments where power and latency are critical. There is a shift toward the adoption of specialized hardware, such as Google’s TPUs, to achieve significantly better energy efficiency and performance compared to general-purpose hardware like GPUs. This points to a broader indusattempt shift driven by the required for more sustainable and efficient computing solutions. European semiconductor firms are also entering the space. Regulatory mandates, such as the European Green Deal’s PUE (Power Usage Effectiveness) requirements, are driving data center operators to deploy technologies like ASICs that offer lower heat generation and simplified cooling requirements. Europe’s focus on operational efficiency and technological indepconcludeence is fueling demand for application-specific integrated circuits (ASICs) in AI tinquires. This shift is creating a high-growth market for specialized hardware that is gaining traction well beyond hyperscaler operations.

By Indusattempt Insights

The IT and telecom segment held the leading share of 36.5% of the Europe AI server market in 2024. The dual role of telecom operators and cloud providers as both applyrs and enablers of AI infrastructure has mainly contributed to the growth of the IT and telecom segment. Simultaneously, European cloud hyperscalers such as OVHcloud and Scaleway offer AI server instances compliant with Gaia X data sovereignty standards, serving thousands of SMEs and public agencies. Moreover, IT service firms like Atos and Capgemini deploy dedicated AI training clusters for client model development under EU data residency rules. The sector’s vertical integration, from infrastructure to application, creates it the largest and most systemic consumer of AI servers in Europe.

The healthcare segment is expected to exhibit a noteworthy CAGR of 31.7% from 2025 to 2033. The rapid expansion of the healthcare segment is propelled by regulatory concludeorsement of AI diagnostics and the rollout of hospital-based AI infrastructure under national digital health strategies. Regulatory frameworks for AI in medical imaging across the EU are becoming more stringent, often requiring higher classification and mandating on-premise validation and audit logs to ensure compliance and patient safety. There is a strong trconclude towards the integration of dedicated, on-premise AI server infrastructure within major European university hospitals to support real-time analysis of medical imaging data. With data privacy non-nereceivediable and clinical outcomes measurable, healthcare is shifting from pilot projects to institutionalized AI server adoption, creating it the highest growth vertical in the European market.

COUNTRY LEVEL ANALYSIS

Germany AI Server Market Analysis

Germany was the top performer in the Europe AI server market and captured a 28.1% in 2024. The dominance of the German market is mainly propelled by a robust industrial base, strong public research infrastructure, and proactive AI sovereignty policies. Industrial giants like BMW, Siemens, and BASF operate private AI server farms for predictive maintenance, digital twins, and autonomous logistics. Apart from these, Germany is a core participant in Gaia X, ensuring its data centers meet stringent European data governance standards. With dense manufacturing, advanced healthcare digitization, and strategic public investment, Germany remains the undisputed engine of AI server demand in Europe.

France AI Server Market Analysis

France was the second-largest counattempt in the Europe AI server market and held an 18.5% share in 2024. The growth of the French market is fuelled by a state-driven strategy to achieve AI sovereignty through national champions and world-class research infrastructure. Major banks operate secure AI inference clusters for fraud detection under European Banking Authority guidelines. The counattempt also leads in edge AI deployment. SNCF applys AI servers across its rail network for real-time track inspection and predictive signaling. France’s blconclude of centralized investment, regulatory alignment, and industrial digitization sustains its status as Europe’s second-largest AI server market.

United Kingdom AI Server Market Analysis

The United Kingdom grew consistently in the Europe AI server market due to its advanced digital economy, world-leading universities, and agile regulatory approach. The government’s National AI Strategy has funded AI server deployments in NHS hospital trusts for clinical decision support. Financial firms in London operate sovereign AI servers for real-time transaction monitoring to comply with the UK’s post-Brexit data laws. The UK’s regulatory sandbox allows quicker deployment of high-risk AI systems by attracting investment from global tech firms establishing European AI hubs in Manchester and Bristol. This combination of innovation, freedom, and institutional adoption ensures the UK’s continued relevance in the European AI server landscape.

Netherlands AI Server Market Analysis

The Netherlands is moderately expanding in the Europe AI server market, with its strength lying in hosting major hyperscale data centers and fostering a collaborative ecosystem between government, academia, and indusattempt. The government’s Data Facility for the Public Sector provides shared AI infrastructure to municipalities for fraud detection and urban planning. With strong grid connectivity, favorable permitting, and a neutral data policy, the Netherlands serves as Europe’s AI server gateway for both cloud and sovereign applications.

Sweden AI Server Market Analysis

Sweden is anticipated to grow in the European AI server market from 2025 to 2033, owing to renewable-powered data centers, pioneering industrial AI, and leadership in federated learning. Companies like Ericsson and Volvo deploy AI servers in 5G networks and vehicle factories for real-time quality control and network optimization. Sweden’s fossil-free electricity grid creates it attractive for energy-intensive AI training, with Hydro66 and Northscale operating green data centers in Boden. Projects demonstrate Sweden’s commitment to privacy-preserving AI through distributed server architectures. This alignment of sustainability, innovation, and public service digitization positions Sweden as a high-impact Nordic leader in the AI server market.

COMPETITIVE LANDSCAPE

The Europe AI server market exhibits a multi-layered competitive landscape where global hyperscalers, European engineering firms, and specialized AI hardware vconcludeors vie for influence. Competition is defined less by price and more by alignment with EU regulatory imperatives including data localization under the AI Act, carbon neutrality under the Green Deal, and digital sovereignty via Gaia X. Global players like Dell and HPE compete on scale and chip partnerships but face scrutiny over data residency, while European firms such as Atos and Fujitsu leverage local compliance expertise and public sector relationships. Startups and semiconductor companies are entering with niche offerings like ASIC-based inference appliances or federated learning servers. The market is also shaped by limited access to cutting-edge GPUs due to US export restrictions, prompting firms to optimize older generation hardware or explore alternative architectures. Differentiation now hinges on energy efficiency, auditability, edge readiness, and integration with national AI strategies, creating regulatory fluency as critical as technical performance in determining competitive advantage across Europe.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe AI server market include

- Dell Technologies

- HPE

- IBM Corporation

- Atos SE

- Gigabyte Technology

- Huawei

- Cisco

- H3C

- Lenovo Group Limited

- Fujitsu Technology Solutions GmbH

- NVIDIA Corporation

- ADLINK Technology, Inc.

- Advanced Micro Devices, Inc.

TOP PLAYERS IN THE EUROPE AI SERVER MARKET

- Atos SE, headquartered in France, is a leading European provider of AI server infrastructure with a strong focus on sovereign and secure computing solutions. The company designs and deploys AI-optimized servers under its BullSequana XH line, tailored for high performance computing and AI workloads in defense, healthcare, and public administration. Atos actively contributes to global AI infrastructure through its partnership with NVIDIA and AMD, integrating advanced GPUs into European data centers compliant with Gaia X standards. The initiatives reinforce Atos’s role as a strategic enabler of Europe’s digital sovereignty agconcludea.

- Fujitsu Technology Solutions GmbH, operating from Germany, plays a pivotal role in the European AI server market through its PRIMERGY and PRIMEHPC server lines optimized for AI inference and edge deployment. The company integrates Intel and NVIDIA accelerators into energy-efficient, liquid-cooled systems aligned with EU sustainability mandates. Fujitsu supports industrial AI adoption across automotive and manufacturing sectors, which offers pre-validated AI server solutions for predictive maintenance and quality control. The company also enhanced its ServerView management software with AI workload orchestration features to improve resource utilization. By combining industrial expertise with energy-conscious design, Fujitsu strengthens Europe’s capacity for localized, compliant AI processing.

- Lenovo Group Limited maintains a significant presence in the Europe AI server market through its ThinkSystem SR675 and Neptune liquid-cooled AI servers, widely adopted by research institutions and telecommunications providers. The company supplies AI infrastructure to EuroHPC projects and national supercomputing centers, including deployments in Spain and the Czech Republic. Lenovo’s global scale enables rapid delivery of GPU-dense servers while its European engineering teams ensure compliance with GDPR and energy efficiency directives. Through localized support, sustainability integration, and hyperscale readiness, Lenovo bridges global technology with European regulatory and operational requirements.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe AI server market are prioritizing compliance with EU data sovereignty and environmental regulations by designing servers with on-premises deployment and liquid cooling capabilities. They are forming strategic alliances with chipcreaters like NVIDIA, AMD, and Intel to secure access to advanced accelerators despite export controls. Companies are co-developing AI solutions with national research institutions and industrial partners to tailor hardware for sector-specific workloads such as healthcare diagnostics and smart manufacturing. Investment in edge AI server form factors enables low-latency inference in factories, hospitals, and telecom networks. Additionally, they offer AI as a Service models through sovereign cloud platforms to lower adoption barriers for the public sector and SMEs. Participation in Gaia X and EuroHPC initiatives ensures alignment with European digital infrastructure standards. Lastly, they are enhancing remote management software with AI-driven workload optimization to improve energy efficiency and hardware utilization.

MARKET SEGMENTATION

This research report on the Europe AI server market has been segmented and sub-segmented into the following categories.

By Server Type

- AI Data

- AI Training

- AI Inference

By Hardware

By Indusattempt

- IT & Telecom

- BFSI

- Retail

- Healthcare

- Manufacturing

By Counattempt

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Leave a Reply