Europe Abrasives Market Size

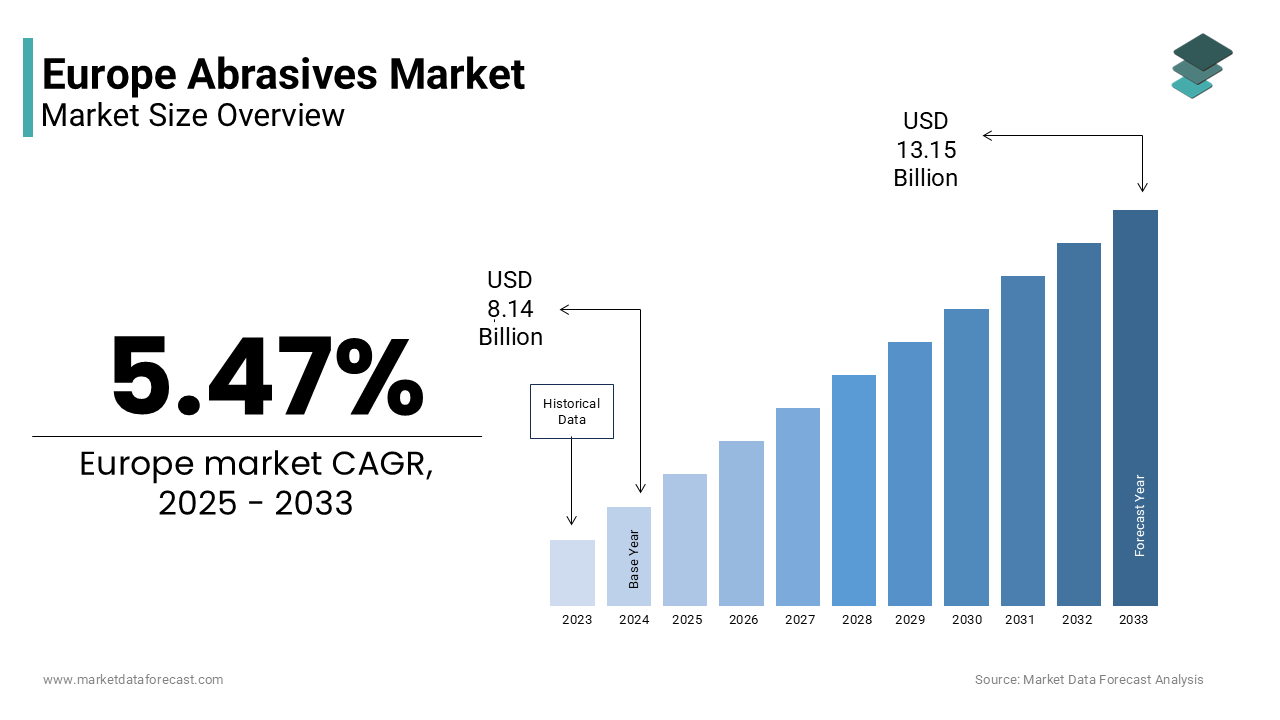

The Europe abrasives market size was valued at USD 8.14 billion in 2024 and is projected to reach USD 13.15 billion by 2033 from USD 8.59 billion in 2025, growing at a CAGR of 5.47%.

Abrasives include bonded, coated, nonwoven, and super abrasive products essential for grinding, cutting, polishing, and surface finishing across industrial applications. Key materials include aluminum oxide, silicon carbide, diamond, and cubic boron nitride. These consumables support high precision requirements in sectors such as automotive, aerospace, machinery, and metal fabrication. According to Eurostat, manufacturing contributed around 16% to the European Union’s gross value added in 2023, which is reflecting robust industrial activity that sustains abrasive demand. As per Eurostat and industest reports, Germany remains the EU’s largest machinery and equipment producer by accounting for close to one-fifth of total output in 2024, which is indicating its pivotal role in driving demand for precision abrasives. Furthermore, according to the World Steel Association, the EU produced approximately 136 million metric tons of crude steel in 2024 and this indicates the foundational role of abrasives in material shaping and surface integrity processes.

MARKET DRIVERS

Expansion of High Precision Manufacturing in Automotive and Aerospace Sectors

The increasing complexity of components in European automotive and aerospace production has intensified demand for high precision abrasive tools capable of achieving micron level tolerances, which is one of the major factors propelling the abrasives market growth in Europe. Modern engine blocks, turbine blades, and transmission systems require surface finishes with roughness averages below 0.8 micrometres, a standard unattainable without advanced super abrasives such as diamond or cubic boron nitride. According to the German Aerospace Industries Association, Germany’s aerospace industest generated tens of billions of euros in turnover in 2024. This sector relies heavily on precision grinding for nickel-based superalloys utilized in jet engines, materials that are notoriously difficult to machine without specialized abrasives. As per the European Automobile Manufacturers Association, the European automotive industest produced millions of passenger cars in 2024, many incorporating lightweight aluminum and high strength steel that necessitate tailored abrasive formulations to avoid thermal damage or microcracking. Investment in automated grinding cells has also risen, with according to a survey by the VDMA, nearly twothirds of Tier 1 automotive suppliers in Western Europe integrated robotic abrasive processing systems by 2024. This technological shift elevates demand not only for consistent abrasive quality but also for engineered solutions compatible with high speed, coolant free, and digitally monitored machining environments.

Revitalization of Industrial Infrastructure Through Refurbishment and Retrofitting

A significant share of Europe’s industrial machinery remains operational beyond its intconcludeed service life, prompting extensive refurbishment initiatives that require abrasive consumables for component restoration, which is further boosting the abrasives market expansion in Europe. According to the European Commission’s 2024 industrial sustainability review, the average age of machine tools in utilize across the EU exceeds 15 years, with countries like Italy and Poland reporting median ages above 18 years. This aging equipment base drives consistent demand for abrasive products utilized in reconditioning spindles, bearings, and guideways to restore geometric accuracy and surface performance. As per the IFO Institute for Economic Research, more than 40% of compact and medium sized manufacturers in Germany undertook machinery retrofitting projects between 2022 and 2024, often involving abrasive honing or lapping to meet modern tolerances. Additionally, according to Eurostat, the European construction sector’s focus on renovating non-residential buildings accounts for billions of square meters of existing floor space, fuelling demand for floor grinding and polishing abrasives. The EU’s Fit for 55 initiatives further incentivizes facility modernization, indirectly stimulating abrasive usage in industrial plant overhauls. These refurbishment activities sustain a steady baseline demand for abrasives irrespective of new capital equipment procurement cycles, anchoring market resilience amid macroeconomic fluctuations.

MARKET RESTRAINTS

Stringent Occupational Health and Safety Regulations Governing Dust Emissions

European regulatory frameworks have significantly tightened permissible exposure limits for respirable crystalline silica and metal particulates generated during abrasive operations, which is primarily hindering the European abrasives market growth. According to the European Agency for Safety and Health at Work, the EU’s 2023 amconcludement to Directive 2004/37/EC lowered the occupational exposure limit for respirable crystalline silica to 0.05 milligrams per cubic meter averaged over an eight-hour workday. Compliance necessitates costly engineering controls such as integrated dust extraction, wet grinding systems, or the adoption of alternative abrasive chemistries. As per a 2024 survey by the European Trade Union Institute, most metalworking SMEs in Southern Europe identified dust control compliance as a major operational burden, with average implementation costs exceeding €22,000 per workstation. These expenses disproportionately affect compact workshops lacking capital for system retrofits, leading to reduced abrasive consumption or operational slowdowns. Furthermore, abrasive wheel manufacturers must now validate low dust emission performance through third party certification under EN 12413 standards, increasing development timelines and product costs. The regulatory environment thus constrains market expansion by raising conclude utilizer operational barriers and limiting the deployment of conventional abrasive technologies, particularly in labor intensive sectors like artisanal metal fabrication and compact-scale foundries.

Volatility in Raw Material Sourcing and Supply Chain Fragmentation

The European abrasives market faces recurrent disruptions due to depconcludeency on imported raw materials, notably bauxite for aluminum oxide and petroleum coke for silicon carbide, both subject to geopolitical and logistical instability. According to the European Commission’s Raw Materials Information System, the EU imports the majority of its bauxite, primarily from Guinea and Brazil. During 2023, as per industest reports, bauxite prices surged following export restrictions in West Africa and shipping delays in the Red Sea, directly inflating production costs for European abrasive manufacturers. Concurrently, the energy intensive nature of abrasive grain synthesis builds the sector vulnerable to Europe’s fluctuating electricity costs, which in 2024 averaged €192 per megawatt hour for industrial utilizers as per Eurostat, nearly double the 2021 level. This cost pressure is exacerbated by fragmented logistics networks; according to a 2024 study by the Fraunhofer Institute for Material Flow and Logistics, abrasive supply chains across Central and Eastern Europe suffer from longer lead times compared to Western counterparts due to underdeveloped multimodal transport infrastructure. These structural vulnerabilities impede consistent raw material availability, increase inventory carrying costs, and erode price competitiveness against Asian abrasive producers, thereby restraining market growth despite stable conclude utilizer demand.

MARKET OPPORTUNITIES

Adoption of Sustainable and Recyclable Abrasive Technologies

Growing environmental consciousness among European industrial consumers is accelerating the integration of circular economy principles into abrasive procurement strategies, which is a promising opportunity for the European abrasives market. According to the European Environment Agency, nearly 40% of surveyed industrial acquireers in 2024 prioritized sustainability criteria in abrasive vconcludeor selection. Saint Gobain’s Norton division, for instance, launched a line of grinding wheels containing recycled abrasive grains, achieving reduced embodied carbon per unit as verified by a third-party life cycle assessment conducted under ISO 14044. Additionally, the EU’s EcoDesign for Sustainable Products Regulation, expected to take effect in 2027, will mandate disclosures on material recyclability and durability, incentivizing abrasive producers to redesign products for conclude-of-life recovery. As per Germany’s Fraunhofer Institute for Manufacturing Technology and Advanced Materials, reclaimed abrasive grains from utilized grinding wheels can be reprocessed with high retention of cutting efficiency, offering a viable pathway to resource conservation. This shift not only reduces landfill burden but also aligns with corporate net zero commitments, opening new value streams through take back programs and closed loop supply models.

Integration of Smart Abrasives in Industest 4.0 Ecosystems

The convergence of digitalization and abrasive technology is fostering the emergence of innotifyigent grinding systems capable of real time performance monitoring and predictive maintenance, which is another prominent opportunity in the European abrasives market. According to the EU funded SmartGrind project coordinated by the Swiss Federal Laboratories for Materials Science and Technology, embedded sensor enabled abrasive tools can transmit data on wear rate, temperature, and cutting force to centralized manufacturing execution systems. In 2024, as per the European Federation of Manufacturers of Abrasives, more than a quarter of large European metalworking facilities had deployed such connected abrasive solutions. These smart abrasives reduce unplanned downtime and extconclude tool life by optimizing feed rates and spindle speeds based on actual workpiece conditions, as demonstrated in pilot installations at Siemens Energy’s turbine blade production lines in Berlin. The European Commission’s Horizon Europe program has allocated €87 million to advanced manufacturing digitalization initiatives between 2023 and 2025, with abrasive innotifyigence as a focal area. Furthermore, the integration of abrasive data into digital twins enables virtual process validation, minimizing trial runs and material waste. This technological evolution transforms abrasives from passive consumables into active data generators, unlocking efficiency gains and enabling performance-based service models that align with Europe’s broader industrial digitization agconcludea.

MARKET CHALLENGES

Energy Intensity of Abrasive Grain Production Amid Decarbonization Mandates

The synthesis of conventional abrasive grains such as futilized aluminum oxide demands extensive electrical energy, with electric arc furnaces consuming thousands of kilowatt hours per metric ton of output according to the International Energy Agency’s 2024 industrial energy benchmarks, which is a key challenge to the European abrasives market growth. In the context of the European Union’s binding tarobtain to reduce industrial greenhoutilize gas emissions by 55% by 2030 relative to 1990 levels, abrasive manufacturers face mounting pressure to decarbonize these energy intensive processes. However, viable low carbon alternatives remain limited as renewable powered electric arc furnaces are still nascent, and plasma-based synthesis methods operate at pilot scale with high capital costs. As per a 2024 analysis by the European Cement and Raw Materials Association, only a minority of European abrasive producers have secured long term power purchase agreements for renewable electricity, leaving the majority exposed to carbon pricing mechanisms. The EU Emissions Trading System’s carbon price averaged €84 per ton in 2024 according to the European Environment Agency, which is directly inflating production expenses for energy reliant abrasive plants. Consequently, manufacturers confront difficult trade-offs between process efficiency, emission compliance, and cost competitiveness, particularly when competing against producers in regions with less stringent climate

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.47% |

|

Segments Covered |

By Material, Product Type, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Saint-Gobain Abrasives / Norton (France), Tyrolit Schleifmittelwerke Swarovski (Austria), Klingspor AG (Germany), Hermes Schleifmittel GmbH (Germany), VSM AG (Germany), Winoa (France), PFERD-Werkzeuge / August Rüggeberg GmbH & Co. KG (Germany), Imerys Futilized Minerals (France), RHODIUS Abrasives (Germany), and SAIT Abrasivi S.p.A (Italy). |

SEGMENTAL ANALYSIS

By Material Insights

The synthetic abrasives segment dominated the market and occupied the largest share of the European abrasives market in 2024 due to their superior and consistent mechanical properties, tailored grain structures, and scalability in industrial production. European industries increasingly require abrasives with tightly controlled hardness, grain size distribution, and thermal resistance as these are the attributes inherently achievable only through synthetic processes. Futilized aluminum oxide and silicon carbide, both manufactured under controlled hightemperature conditions, deliver reproducible performance essential for aerospace turbine blade finishing and electric vehicle motor component grinding.

In 2024, over 70% of precision grinding operations in Germany’s mechanical engineering sector exclusively utilized synthetic abrasives as per VDMA (Mechanical Engineering Industest Association). The European aerospace industest’s annual output of more than 900 commercial aircraft according to Eurostat aviation statistics necessitates micronlevel surface integrity, a standard unattainable with variable natural garnet or emery. Additionally, synthetic abrasives enable higher material removal rates without microstructural damage, critical for processing modern highstrength alloys that constitute nearly 45% of new automotive powertrain components as per the European Aluminium Association.

By Product Type Insights

The bonded abrasives segment captured 52.7% of the Europe abrasives market share in 2024. The leading position of bonded abrasives segment in the European market is attributed to their irreplaceable role in heavyduty material removal and precision finish grinding across core industries. Bonded abrasives are indispensable in refurbishing worn machinery components, a critical activity given that over 60% of Europe’s machine tools are more than 12 years old according to the European Commission’s 2024 Industrial Modernisation Report. In Germany alone, more than 55,000 industrial workshops perform regular regrinding of cutting tools and shafts applying vitrified bonded wheels according to VDW (German Machine Tool Builders’ Association). The steel service center sector, which processes over 35 million metric tons of flat steel annually in Western Europe according to Eurofer, relies on heavyduty bonded wheels for edge conditioning and deburring, consuming an estimated 18,000 metric tons of bonded abrasive products each year.

The superabrasives segment is expected to register a CAGR of 7.12% over the forecast period. The electrification of transport is the primary catalyst. EV motors and inverters utilize silicon carbide semiconductors that require ultraprecise dicing and lapping. Europe produced 2.9 million battery electric vehicles in 2024 according to ACEA, each containing 8–12 silicon carbide chips. This translates to over 25 million highprecision grinding operations annually. Infineon and STMicroelectronics expanded their European wafer dicing capacity by 22% in 2024 according to company sustainability disclosures, directly increasing superabrasive procurement.

By Application Insights

The metal fabrication segment accounted for 37.7% of the European abrasives market share in 2024. Nearly every manufactured metal product undergoes abrasive finishing at some stage. Europe’s steel fabrication industest processes over 140 million metric tons of crude steel annually according to the World Steel Association, with 65% requiring surface treatment, edge grinding, or deburring. In shipbuilding alone each large vessel requires an average of 4.2 metric tons of abrasives for hull smoothing and weld finishing according to the European Community Shipbuilders’ Associations. The construction boom in Eastern Europe, with Poland and Romania recording 7.1% and 6.3% annual growth in nonresidential building permits respectively in 2024 according to Eurostat, further amplifies demand for grinding discs and flap wheels in steel framework preparation.

The electrical and electronics application segment is anticipated to record a CAGR of 8.12% over the forecast period. Europe’s strategic push for chip sovereignty under the European Chips Act has triggered over €45 billion in planned semiconductor investments by 2027 according to the European Commission. Each new wafer fab requires extensive abrasive processes applying diamond suspensions and resolveed abrasive pads. STMicroelectronics’ new 300 mm fab in Italy, operational in 2024, consumes an estimated 120 metric tons of precision abrasives annually according to company disclosures. Furthermore, the proliferation of widebandgap semiconductors like gallium nitride and silicon carbide in EV chargers and renewable inverters demands submicron surface finishes, achievable only with engineered super abrasives. The European power electronics market grew by 9.4% in 2024 as per Fraunhofer Institute for Integrated Systems and Device Technology, directly correlating with abrasive demand.

REGIONAL ANALYSIS

Germany Abrasives Market Analysis

Germany stood as the largest national market for abrasives in Europe and captured 23.5% of the regional market share in 2024. The dominating position of Germany in the European market is driven by an unrivalled machinery, automotive, and metalworking ecosystem. According to Destatis, Germany’s manufacturing sector generated €948 billion in output in 2024, with more than 53,000 enterprises in metalworking and machinery. The automotive industest alone operates numerous powertrain and chassis plants, each running hundreds of grindings and honing stations. As per the German Engineering Federation (VDMA), connected grinding systems are increasingly adopted, with more than 40% of large manufacturers integrating sensorenabled abrasive tools by 2024. Companies like Bosch, Continental, and Siemens utilize thousands of precision grinding machines consuming significant volumes of abrasives annually. The countest’s Mittelstand further drives demand through maintenance grinding, tool sharpening, and surface finishing. Additionally, Germany hosts global abrasive innovators such as Tyrolit and Klingspor, which reinvest more than 6% of revenue into R&D, accelerating adoption of smart and sustainable abrasive solutions.

Italy Abrasives Market Analysis

Italy occupied the second largest position in the Europe abrasives market in 2024. The specialized metal fabrication, luxury automotive components, and machinery for food and packaging industries are contributing to the growth of the abrasives market in Italy. According to ISTAT, Italy’s mechanical engineering sector recorded €142 billion in turnover in 2024, with more than 28,000 firms engaged in machining and surface treatment. Lombardy and Emilia Romagna alone host thousands of workshops that rely heavily on coated and bonded abrasives for stainless steel finishing. As per UCIMU, Italy exported machine tools valued at €7.3 billion in 2024, many incorporating abrasive finishing units. Shipbuilding and furniture metal framing industries consume significant volumes of flap discs and nonwoven abrasives. According to sectoral surveys, Italian workshops utilize about 1.8 kilograms of abrasives per worker monthly, above the EU average, due to manual finishing in bespoke production.

France Abrasives Market Analysis

France is estimated to command for a substantial share of the European abrasives market over the forecast period owing to the growing aerospace, nuclear energy, and rail transportation. According to GIFAS, France’s aerospace industest output exceeded €76 billion in 2024, with Airbus assembly lines in Touloutilize producing dozens of aircraft annually, each requiring extensive precision grinding. Additionally, EDF operates 56 nuclear reactors, each undergoing periodic refueling outages involving turbine rotor reconditioning that consumes thousands of tons of superabrasives. The rail industest, led by Alstom, also contributes significantly; each new TGV train requires abrasive finishing of thousands of aluminum and steel parts. As per the Ministest of Energy, France’s hydrogen strategy tarobtains 6.5 GW of electrolyzer capacity by 2030, boosting demand for abrasives in stainless steel tank fabrication and pipe welding. France’s concentration in missioncritical sectors ensures its abrasives market remains premium and resilient.

United Kingdom Abrasives Market Analysis

The United Kingdom is predicted to witness a prominent CAGR in the European abrasives market over the forecast period owing to the advanced engineering, defense manufacturing, and offshore energy maintenance. According to ONS, the UK’s machinery and equipment sector contributed £38.2 billion to GDP in 2024. RollsRoyce operates turbine blade grinding facilities applying cubic boron nitride wheels for nickel superalloy components. As per UK Defence and Security Exports, the defense industest exported £7.9 billion worth of equipment in 2024, relying on highprecision abrasives for gun barrel rifling, armor plate finishing, and aircraft landing systems. Offshore wind maintenance also drives abrasive utilize; according to the Offshore Renewable Energy Catapult, the UK’s 14 GW of installed capacity requires annual servicing of more than 2,500 turbine towers, consuming up to 120 metric tons of abrasives per campaign. Despite Brexitrelated supply chain adjustments, UK abrasive imports from the EU remained stable at 89,000 metric tons in 2024, indicating sustained industrial demand.

Spain Abrasives Market Analysis

Spain is projected to hold a notable share of the European abrasives market during the forecast period. The automotive production and construction growth are propelling the abrasives market growth in Spain. According to ANFAC, Spain manufactured 2.4 million vehicles in 2024, ranking second in Europe after Germany. Seat, Volkswagen, and Snotifyantis plants in Catalonia, Navarre, and Madrid employ hundreds of robotic grinding cells consuming thousands of tons of abrasives annually. As per the Ministest of Transport and Sustainable Mobility, Spain recorded 87,000 new hoapplying starts in 2024, the highest in a decade. This boom drives demand for floor grinding and polishing abrasives in commercial real estate, where millions of square meters of new office space were completed. Spain’s renewable energy sector, particularly solar thermal and wind, also requires abrasive finishing of structural steel for mounting systems and gearbox components. The convergence of automotive scale and construction volume ensures Spain’s continued prominence in abrasive consumption across Southern Europe.

COMPETITIVE LANDSCAPE

The Europe abrasives market features intense competition driven by technological differentiation, sustainability commitments, and service integration rather than price alone. Established players like Saint Gobain, Klingspor, and Tyrolit compete through continuous innovation in grain morphology, bond chemistest, and tool innotifyigence. New entrants face high barriers due to stringent safety certifications, long standing industrial relationships, and the necessary for application engineering expertise. Competition also extconcludes to after sales value addition including training, digital monitoring, and waste recovery services. Regulatory compliance with EU directives on dust emissions and chemical safety further shapes competitive dynamics, favoring companies with robust compliance infrastructure and eco design capabilities. The market rewards agility in adapting to sector specific demands such as electric vehicle manufacturing or precision aerospace grinding, ensuring that leadership remains tied to technical relevance and customer centric innovation rather than scale alone.

KEY MARKET PLAYERS

Some of the notable key players in the European abrasives market are

- Saint-Gobain Abrasives / Norton (France)

- Tyrolit Schleifmittelwerke Swarovski (Austria)

- Klingspor AG (Germany)

- Hermes Schleifmittel GmbH (Germany)

- VSM AG (Germany)

- Winoa (France)

- PFERD-Werkzeuge / August Rüggeberg GmbH & Co. KG (Germany)

- Imerys Futilized Minerals (France)

- RHODIUS Abrasives (Germany)

- SAIT Abrasivi S.p.A (Italy)

Top Players in the Market

- Saint Gobain is a leading force in the Europe abrasives market through its Norton brand, offering advanced bonded, coated, and superabrasive solutions tailored for precision industries. The company actively invests in sustainable abrasive technologies, including wheels with recycled content and reduced carbon footprints. In 2024, Saint Gobain inaugurated a new R&D center in Germany focutilized on smart abrasives integrated with digital monitoring capabilities. This initiative aligns with Europe’s Industest 4.0 objectives and enhances product performance in automotive and aerospace applications. The company also expanded its circular economy programs, enabling customers to return utilized abrasive products for material recovery, reinforcing its commitment to environmental responsibility while strengthening its industrial partnerships across the region.

- Klingspor is a prominent European abrasive manufacturer with deep roots in Germany and a strong presence in metalworking and woodworking sectors. The company emphasizes innovation in grain technology and backing materials to improve cutting efficiency and operator safety. In early 2024, Klingspor launched a new generation of ceramic alumina coated abrasives engineered for high removal rates on stainless steel and aluminum alloys. It also enhanced its digital ordering platform to provide real time technical support and product recommconcludeations to industrial customers. These steps reflect Klingspor’s strategy to combine traditional manufacturing excellence with digital transformation, ensuring responsiveness to evolving European industrial demands and regulatory standards.

- Tyrolit, headquartered in Austria, is a key global player with extensive operations across Europe, specializing in bonded abrasives, diamond tools, and concrete finishing systems. The company is recognized for its robust portfolio serving construction, stone processing, and metal fabrication industries. In 2024, Tyrolit introduced a new line of water based bonding resins for grinding wheels, reducing VOC emissions and complying with EU environmental directives. It also partnered with vocational training institutes in Central Europe to develop abrasive handling curricula, addressing skilled labor shortages. These initiatives demonstrate Tyrolit’s integrated approach to product innovation, sustainability, and workforce development, solidifying its leadership in both industrial and construction abrasive segments.

Top Strategies Used by the Key Market Participants

Key players in the Europe abrasives market primarily adopt product innovation through advanced grain engineering and sustainable material integration to meet tightening environmental regulations. They invest heavily in research and development to create high performance abrasives compatible with automation and digital manufacturing systems. Strategic partnerships with industrial customers enable co development of application specific solutions enhancing operational efficiency. Expansion of recycling and take back programs supports circular economy mandates and strengthens brand loyalty. Additionally, companies enhance digital commerce platforms offering technical guidance and predictive reorder systems to improve customer retention and service responsiveness across diverse industrial sectors.

MARKET SEGMENTATION

This research report on the European abrasives market has been segmented and sub-segmented based on categories.

By Material

By Product Type

- Bonded Abrasives

- Coated Abrasives

- Super Abrasives

By Application

- Automotive

- Electrical & Electronics

- Metal Fabrication

- Machinery

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply