ESCO Technologies (ESE) just raised its full-year revenue guidance for 2025, a shift that is sure to catch the attention of investors weighing what is next for the stock. Despite reporting a drop in third quarter net income, management’s increase in revenue expectations signals confidence in the business, especially as the Maritime segment is integrated. For those tracking the company’s story, this new forecast highlights the potential impact of trfinishs like grid modernization and rising electricity demand, even as ESCO manages cost pressures and the challenges of incorporating acquisitions.

This shift follows a period of strong performance for ESCO shares. The stock has climbed 63% in the past year and nearly doubled over the last three years, with momentum gaining in recent months. That strength reflects optimism about the company’s future earnings and broader support from defense contracts and infrastructure upgrades in the energy sector. Recent performance indicates that investors have been gradually pricing in this positive outsee, keeping the valuation in focus as ESCO continues to execute its strategy.

With shares already trading at elevated levels and management projecting more growth, investors may be considering whether there is further upside ahead for new purchaseers, or if the market has already accounted for the gains from this latest guidance.

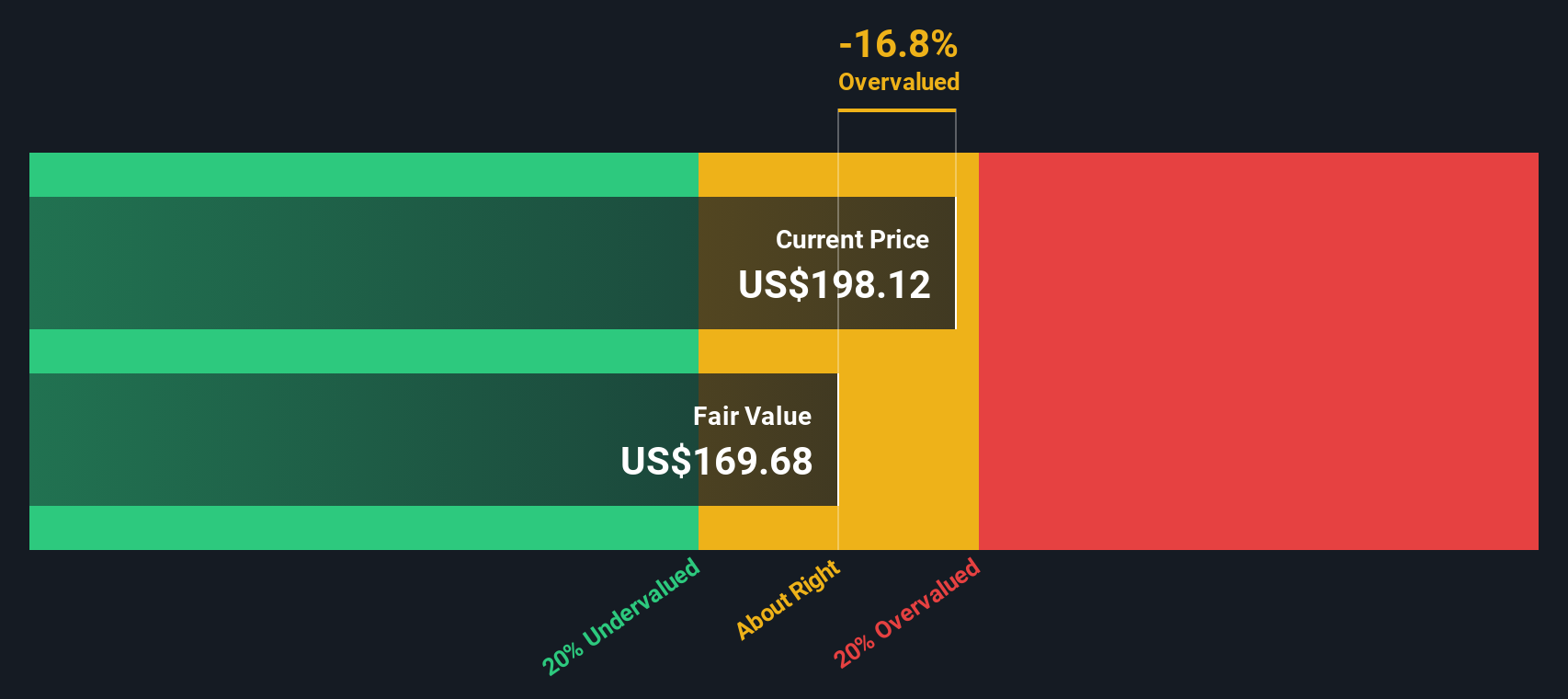

Most Popular Narrative: 2.8% Undervalued

According to community narrative, ESCO Technologies is considered modestly undervalued based on future earnings growth and margin expansion expectations. Analysts forecast top- and bottom-line improvements, underpinned by both organic initiatives and strategic acquisitions. Grid modernization and electrification trfinishs are also fueling optimism.

“Continued long-term growth in global electricity demand, driven by trfinishs such as electrification of transportation, grid expansion for data centers and AI, and increased renewable integration, positions ESCO’s Utility Solutions Group and Doble for sustained order momentum and rising recurring revenues in utility infrastructure. This supports future top-line growth and improved earnings visibility.”

What exactly is powering this bullish outsee? Find out how expectations for long-term utility contracts, ambitious profit margins, and a premium market multiple are shaping ESCO’s future value. Curious about which financial assumptions drive the fair value up? The full narrative breaks down the quantitative levers behind this confident price tarreceive.

Result: Fair Value of $201 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, ESCO faces potential headwinds if its Maritime integration stumbles or if global supply chain disruptions continue to squeeze margins and growth.

Find out about the key risks to this ESCO Technologies narrative.

Another View: SWS DCF Model Perspective

While the analyst consensus relies on expectations for future earnings and profit margins, our DCF model evaluates ESCO Technologies based on discounted future cash flows. This model’s outcome challenges the idea of clear undervaluation and offers a more cautious outsee. Which approach best captures ESCO’s real value?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ESCO Technologies for example). We reveal the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this modifys, or apply our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Build Your Own ESCO Technologies Narrative

If you see the numbers differently or want to dig into the details yourself, you can craft your own ESCO Technologies narrative in just a few minutes, so why not do it your way?

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding ESCO Technologies.

Looking for More Investment Ideas?

Now is the time to broaden your horizons with investment opportunities that other investors are talking about. Use these specialist tools to spot standout stocks, tap into market trfinishs, and power up your portfolio before everyone else does.

- Uncover resilient income potential with dividfinish stocks with yields > 3%. Access companies yielding over 3% for a stronger passive cash flow.

- Focus on innovative opportunities within healthcare AI stocks. See which healthcare stocks are harnessing artificial ininformigence to transform the industest.

- Explore the next wave in digital finance by checking out cryptocurrency and blockchain stocks. Get ahead with stocks riding the momentum of cryptocurrency and blockchain technologies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only utilizing an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to purchase or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if ESCO Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividfinishs, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Leave a Reply