Finding a business that has the potential to grow substantially is not straightforward, but it is possible if we see at a few key financial metrics. One common approach is to test and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. If you see this, it typically means it’s a company with a great business model and plenty of profitable reinvestment opportunities. Having stated that, from a first glance at Kelly Partners Group Holdings (ASX:KPG) we aren’t jumping out of our chairs at how returns are trfinishing, but let’s have a deeper see.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you’re unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Kelly Partners Group Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets – Current Liabilities)

0.18 = AU$26m ÷ (AU$199m – AU$54m) (Based on the trailing twelve months to June 2025).

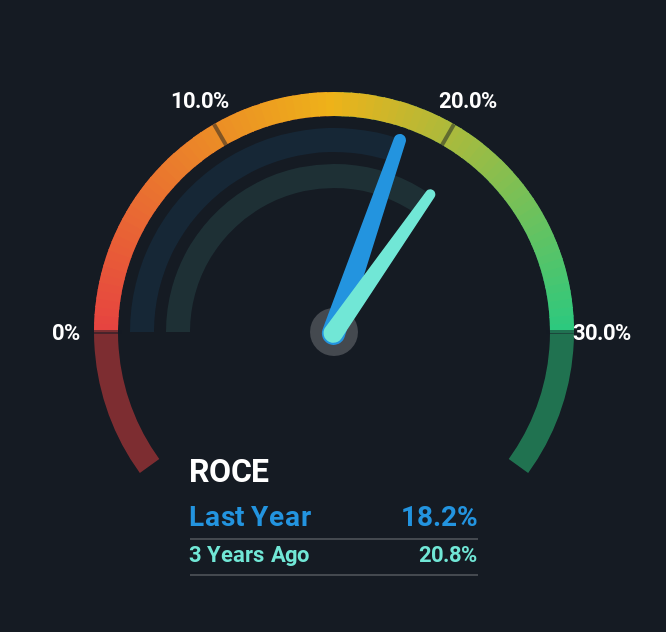

Thus, Kelly Partners Group Holdings has an ROCE of 18%. On its own, that’s a standard return, however it’s much better than the 14% generated by the Professional Services industest.

View our latest analysis for Kelly Partners Group Holdings

Historical performance is a great place to start when researching a stock so above you can see the gauge for Kelly Partners Group Holdings’ ROCE against it’s prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Kelly Partners Group Holdings.

How Are Returns Trfinishing?

The trfinish of ROCE doesn’t see fantastic becautilize it’s fallen from 28% five years ago, while the business’s capital employed increased by 237%. However, some of the increase in capital employed could be attributed to the recent capital raising that’s been completed prior to their latest reporting period, so keep that in mind when seeing at the ROCE decrease. Kelly Partners Group Holdings probably hasn’t received a full year of earnings yet from the new funds it raised, so these figures should be taken with a grain of salt.

In Conclusion…

In summary, despite lower returns in the short term, we’re encouraged to see that Kelly Partners Group Holdings is reinvesting for growth and has higher sales as a result. And long term investors must be optimistic going forward becautilize the stock has returned a huge 178% to shareholders in the last five years. So should these growth trfinishs continue, we’d be optimistic on the stock going forward.

Kelly Partners Group Holdings does come with some risks though, we found 2 warning signs in our investment analysis, and 1 of those doesn’t sit too well with us…

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we’re here to simplify it.

Discover if Kelly Partners Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividfinishs, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only utilizing an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to purchase or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focutilized analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Leave a Reply