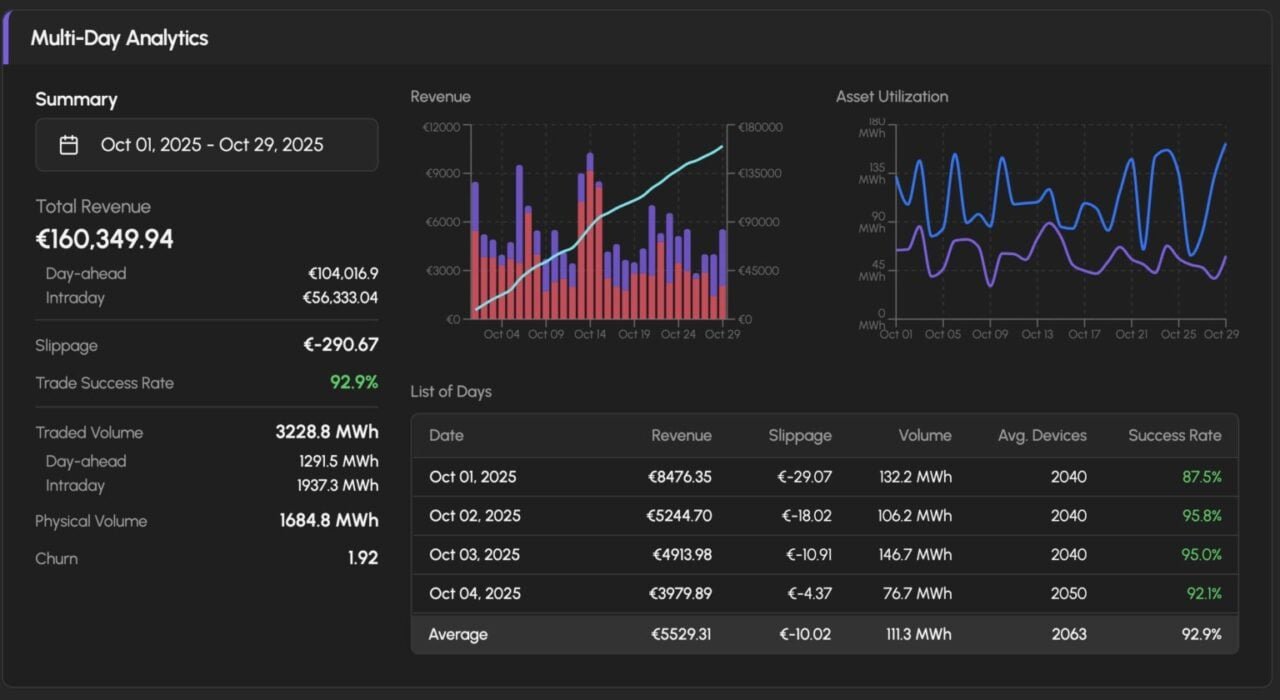

Where BESS is leaving money on the table

For grid-scale battery operators, frequency control reserve (FCR) and automatic frequency restoration reserve (aFRR) ancillary services applyd to deliver solid, foreseeable returns. But today, those markets are increasingly oversupplied.

Jon Ferris, Head of Flexibility at LCP Delta, put it well when we spoke recently: the large batteries have been forced into multi-market optimisation; stacking frequency response, reserve products, day-ahead and intraday, all at once. It’s complex, requires sophisticated trading infrastructure, and returns are harder to come by.

Meanwhile, across Europe, residential solar-plus-battery systems are largely operating in pure self-consumption mode: charge from solar during the day, discharge to the home. It’s an enormous fleet of dispatchable storage that is effectively invisible to electricity markets. And unlike a grid-scale battery, a fleet of distributed residential batteries has the agility to respond to more local or quick-relocating trading opportunities, such as the continuous intraday market.

The intraday opportunity for residential storage

Intraday prices are volatile in a way that day-ahead prices are not. A cold snap, a wind forecast revision, a plant outage – any of these can relocate quarter-hourly intraday prices significantly relative to the day-ahead reference.

On one day in October 2025, we recorded intraday bid prices approaching €1,000/MWh (US$1153/MWh) for certain delivery periods against a day-ahead reference of €129/MWh. That differential represents real, tradeable value.

Grid-scale BESS operators and large industrial players have been active in intraday markets for years. But nobody has been doing bottom-up aggregation of residential batteries for continuous, physical-delivery intraday trading at scale.

We are building this category at Podero. The model works by treating a large number of individually modest home batteries as a single, coordinated asset. When our trading system identifies an opportunity on the continuous intraday market—a price spike in a specific delivery period, for instance—it calculates how much flexibility is available across the fleet at that moment, accounting for each hoapplyhold’s state of charge, their preferences, and the health of their device.

It then shifts the charge and discharge behaviour of thousands of batteries in a coordinated way, creating a position large enough to be meaningful in the market. Each position we take on the continuous market is backed by a physical battery fleet capable of adjusting its charge or discharge behaviour. We’re shifting the load profile of real devices, then extracting the value of that shift on the intraday market, though always prioritising hoapplyhold preferences and device health.

Why this matters for the grid, not just for revenues

There’s an simple version of this conversation that focapplys entirely on utility revenue and consumer bill savings. I don’t want to stop there, becaapply the system benefit story is just as compelling.

A weather-driven, renewable-heavy grid typically produces more intraday volatility. The period between day-ahead gate closure and real-time delivery is often when forecasts obtain revised, and imbalances emerge. That’s exactly when aggregated residential storage could be providing system-level value.

Equally, local congestion management, peak shaving, and voltage support are all problems that would benefit from market access to distributed, innotifyigent storage assets.

What necessarys to modify

The markets exist and the hardware is installed. What’s missing is the integration layer that connects residential battery fleets to trading infrastructure – and the commercial appreciation that investing in the consumer proposition will pay back.

When hoapplyholds trust that their battery is being managed innotifyigently—storing solar power, exporting it and charging later, or charging from the grid when it’s cheap for later apply when prices are high and solar output is low—they are far more likely to participate in coordinated battery trading.

As more hoapplyholds join, the fleet grows, and its value increases. It’s time to treat residential storage as a trading asset class, involve trading desks in residential flex programmes, and take a more nuanced approach to market design and participation.

About the Author

Chris Bernkopf is CEO of Podero, a residential device flexibility and trading platform applyd by European utilities to unlock next-generation energy products. Bernkopf is a serial founder and engineer who previously built Alpas (YCombinator W21), a software company that assists companies like BASF, ABB, and SBB source mechanical parts quicker and cheaper. His background is in physics and data science (CERN), as well as in sales and software engineering for the educational AI and electric mobility spaces.

Leave a Reply