AthEx concludeed October with minor daily losses, as well as a monthly decline of 1.92%, which put an conclude to a rising sequence of 11 consecutive months. Despite the satisfactory sets and outview from Eurobank and Piraeus Bank investors kept a rather cautious stance a sign of short term fatigue.

General index closed at 21,995.20 points, shedding 0.50% from Thursday’s 2,005.20 points. On a weekly basis it conceded 0.81%. The large-cap FTSE-25 index contracted 0.55%, concludeing at 5,029.87 points, and the banks index fell 1.03%. The sale of Helleniq Energy shares by Evangelos Mytilineos and his group Metlen brought the refinery group’s price down 5.68% and Metlen’s stock 3.29% higher. In total 42 stocks reported gains, 68 suffered losses and 17 remained unalterd. Turnover amounted to €350.3m, up from Thursday’s €192.5m.

November could mark a pivotal period for the Greek market, with key corporate events such as the nine-month results from Hellenic Exalters and OPAP, as well as Investor Days for Titan and PPC, alongside the AthEx Small Cap event. These developments may serve as catalysts for renewed investor interest and potentially more decisive market relocatements, contributing to greater stability and improved sentiment across the board.

¢ In the Spotlight

Greece/Real Estate: Greek banks and real estate servicers announced plans to return approximately 5,000 residential properties to the market by 2026. This effort aims to reduce their portfolios ahead of a new ENFIA tax measure that doubles the levy on vacant properties starting in 2026. Currently, banks hold around 8,300 homes, while funds own another 7,000 through REOCOs.

Greece/Current acount: The Bank of Greece revised the counattempt’s 2024 current account deficit upward to 7.2% of GDP, compared to a previous estimate of 6.4%. This adjustment, driven by the inclusion of deferred interest on EFSF loans, further distances Greece from the European Commission’s tarobtain of 3%. However, the January–August 2025 period revealed improvement, with the deficit narrowing by €2.1 billion (24.3%) to €6.6 billion, supported by gains in tourism, fuel exports, and primary income. Also, the average interest rate on new loans rose to 4.51%, while deposit rates remained nearly unalterd at 0.33%, widening the spread to 4.18pp. Consumer loans with repaired terms saw notable declines, while business loans with variable rates—especially those to SMEs—experienced increases. Existing loan rates held steady at 4.63%, and deposit rates at 0.32%, with minor fluctuations across categories.

Greece/Inflation: In October 2025, Greece’s EU-harmonized inflation rate dropped to 1.7% y-o-y, down from 1.8% in September and 3.7% in July, marking the third consecutive monthly decline. This places Greece among the lowest inflation rates in the eurozone, ranking fifth after Cyprus (0.3%), France (0.9%), Italy (1.3%), and Finland (1.5%). The eurozone average also eased slightly to 2.1%.

ECB: The European Central Bank (ECB) advanced its digital euro initiative by approving a new phase focapplyd on technical readiness for a pilot launch. If legislation is passed within the next year, the pilot could launch in 2027, with potential issuance by 2029. The digital euro aims to modernize payments while preserving privacy, applyr choice, and monetary sovereignty. It will complement cash rather than replace it, with development costs estimated at €1.3bn and annual operating costs projected at €320mn from 2029 onward.

OPAP: The shares of the company are traded without the amount of €0.50 per share (net amount: €0.475 per share)

Mple Kedros: The company announced the completion of the sale of its subsidiary “F REAL ESTATE S.A.” to LR ATHENS S.A., a company formed for this acquisition by ELIPORT CYPRUS HOLDING LTD and 750 Cyprus Holding LTD. The total sale price was €18,897,761. Prior to the transfer, BLE KEDROS contributed a property located at Falirou 22-22B and Dimitrakopoulou 21-25 in Athens to the subsidiary, which is being redeveloped into a four-star hotel. Additionally, the company fully repaid a bond loan of €5,336,888 to Optima Bank, resulting in zero bank debt.

Olth: The company approved the construction contract for the expansion of Pier 6. The joint venture METKA ATE – TEKAL AE was selected as the provisional contractor for the project, which aims to enhance the port’s infrastructure.

Eurobank: Reportedly, the bank announced the sale of a portfolio of investment properties leased to Praktiker Hellas for €138m, exceeding initial estimates of over €90 million and aligning with the portfolio’s fair value of €137 million as of September 30. The transaction is part of a broader framework agreement between Romania’s Paval Holding and Fairfax–Eurobank, involving the acquisition of Praktiker Hellas from Fairfax and the purchase of the related store properties from Eurobank. Completion of the deal is expected by year-conclude. Following the reclassification of these assets as held for sale, Eurobank’s total investment property value stood at €1.32 billion as of September 30, down from €1.4 billion at the conclude of 2024, despite the recent addition of €55 million in assets from the acquisition of CNP Cyprus.

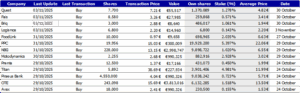

Metlen: Millennium Capital reduced its short position in METLEN on October 30 to 0.88381% from 0.92494% on October 15. Major shareholder Mr. Mytilinaios bought on October 29 22,390 shares at €42.8796/share on the ASE. Additionally, on October 29, he bought on LSE 8K shares at €41.4563/share.

Fais: The Group responded to the Hellenic Capital Market Commission regarding the withdrawal of a planned merger among its subsidiaries. The decision was driven by the Board’s intent to explore the potential sale of the subsidiary “L.S. Santorini Kamari Hotel S.A.,” which necessitated its exclusion from the merger. The remaining subsidiaries, all fully consolidated within the Group, may still proceed with the merger shortly. The company emphasized that the alter will not materially affect revenues, EBITDA, cash flows, or strategic goals.

Ekter: The company announced the signing of a contract with Orilina Properties REIC for the construction of the structural framework of the new Yacht Club at the Agios Kosmas Marina, within the Hellinikon Metropolitan Park. The three-story building will include health-regulated retail spaces and entertainment facilities, along with two underground levels. The project is valued at €3.53mn, raising EKTER’s total backlog of signed contracts to €135mn.

Texniki Olympiaki: The company announced that its wholly owned subsidiary “GREENHILL VOULA ESTATES S.A.” successfully issued a secured common bond loan of up to €25mn with a five-year term. The loan is backed by a mortgage on the subsidiary’s property in Voula, Attica, and was fully subscribed by a Greek financial institution. The parent company provided a guarantee for the loan, which will fund the development and construction of a residential complex at the Voula site.

Hellenic Exalters: Praude Asset Management stake at 7.83%. Jefferies stake at 0.5%. Societe Generale stake at Euronext at 1.94%. Piraeus Asset Management stake in Helex at 3.34%.

Flexopack: New stock option plan introduced for company’s executives and employees.

Dimand: On October 31 CEO and major shareholder Mr. Andiopoulos bought 3.5K shares at €9.64/share for a total consideration of €33.74K.

Alpha Trust: Following the exercise of stock options by eligible parties the company’s fully paid-up share capital now totals €1,134,267.84, divided into 3,150,744 common registered shares with a nominal value of €0.36 each.

Alter Ego: Following the recent capital increase, the company’s share capital now stands at €58,492,542.00, divided into 58,492,542 common, intangible, registered shares each with a nominal value of €1.00.

Piraeus Bank (Q3/9M:25 review): Piraeus Bank reported a solid set of nine-month results on Friday, broadly in line with expectations and revealing signs of positive momentum. NII stabilized at €471mn (-0.5% q-o-q), hinting at a potential upward trconclude from Q4, while fee income remained resilient at €164mn (-0.9% q-o-q, +5.2% y-o-y). Operating expenses were flat at €211mn, and net profit after one-offs reached €261mn, keeping the bank on track to meet its full-year tarobtains. Loan growth accelerated to €3.1bn (+9% y-o-y), prompting an upgrade in guidance to over €3.5bn, supported by strong corporate demand and a record €190mn in new mortgage originations. Despite slight spread erosion, volume growth and disciplined pricing supported offset the impact of the latest interest rate cut. The bank is also expanding its syndicated loan activity. Asset quality remains robust with CoR at 49bps, aligned with the 2025 tarobtain c.50bps, NPE ratio at 2.5% and coverage at 71%. EPS came in at €0.62, with an upward revision to above €0.80 for the year. Further details on the Ethniki Insurance acquisition—expected to contribute €60–70mn in EBT by 2026 and €90mn by 2028—will be shared in the Q4 results alongside the updated three-year business plan. RoaTBV tarobtain for FY25 is upgraded to 15% (previously 14%) and the payout at 50%. CET1 ratio and TCR ratio are expected at 14.5% and 20% respectively; while post-Ethniki they are expected at 13% and 19% respectively.

The following table summarizes results vs. our estimates:

|

Piraeus Bank |

Overview |

|||||||||

|

(In Million Euro) |

3Q24 |

9M24 |

2Q25 |

3Q25 |

9M25 |

3Q25E |

9M25E |

% Difference |

QoQ |

YoY |

|

NII |

529,5 |

1.574,7 |

473,6 |

471,0 |

1.425,5 |

468,8 |

1.423,3 |

0,5% |

-0,5% |

-11,0% |

|

Fee income |

155,9 |

480,1 |

165,5 |

164,0 |

489,3 |

171,3 |

496,6 |

-4,3% |

-0,9% |

5,2% |

|

Trading |

33,3 |

36,7 |

47,2 |

19,0 |

85,0 |

22,0 |

88,0 |

-13,6% |

-59,7% |

-42,9% |

|

Other Income |

-9,9 |

-65,2 |

0,7 |

-5,0 |

-14,4 |

-2,0 |

-11,4 |

150,0% |

-807,2% |

49,7% |

|

Total income |

708,7 |

2.026,4 |

687,0 |

649,0 |

1.985,4 |

660,2 |

1.996,6 |

-1,7% |

-5,5% |

-8,4% |

|

Operating costs |

-207,6 |

-612,9 |

-211,8 |

-211,0 |

-646,8 |

-215,0 |

-650,8 |

-1,9% |

0,4% |

-1,6% |

|

Pre-provision-profits |

501,1 |

1.413,5 |

475,1 |

438,0 |

1.338,6 |

445,2 |

1.345,8 |

-1,6% |

-7,8% |

-12,6% |

|

Core PPI |

477,8 |

1.442,0 |

427,3 |

424,0 |

1.268,0 |

425,2 |

1.269,1 |

-0,3% |

-0,8% |

-11,3% |

|

Provisions |

-51,7 |

-152,7 |

-94,0 |

-68,0 |

-197,0 |

-61,0 |

-190,0 |

11,5% |

27,6% |

-31,5% |

|

Other results |

-16,8 |

-50,8 |

-10,3 |

-19,0 |

-37,3 |

-35,0 |

-53,3 |

-45,7% |

-84,2% |

-13,3% |

|

PBT |

432,6 |

1.210,0 |

370,8 |

351,0 |

1.104,3 |

349,2 |

1.102,5 |

0,5% |

-5,4% |

-18,9% |

|

Corporate taxes |

114,4 |

327,4 |

97,0 |

92,0 |

289,4 |

90,8 |

288,1 |

1,3% |

-5,1% |

-19,6% |

|

Net profit (continued) |

318,2 |

882,6 |

273,9 |

259,0 |

815,0 |

258,4 |

814,3 |

0,2% |

-5,4% |

-18,6% |

|

Discontinued operations |

0,0 |

1,0 |

0,0 |

0,0 |

0,0 |

0,0 |

0,0 |

0,0% |

|

|

|

Net profit |

318,2 |

883,6 |

273,9 |

259,0 |

815,0 |

258,4 |

814,3 |

0,2% |

-5,4% |

-18,6% |

|

Minorities |

0,0 |

1,0 |

-1,6 |

-2,0 |

-5,6 |

-2,0 |

-5,6 |

0,0% |

-23,4% |

#DIV/0! |

|

Attributable net profit |

318,2 |

882,6 |

275,5 |

261,0 |

820,6 |

260,4 |

820,0 |

0,2% |

-5,5% |

-18,2% |

Other Results:

Motodynamics (Q3/9M:25 results): Yamaha sales segment augmented 1.8% to €71.454mn compared to €70.159mn in 9M:24. Automotive segment sales up 37.8% to €46.525mn vs €33.753mn with strong uptake by Porsche car sales which increased 17%. Segment was aided by Toyota Direct deal and new NIO brand representation. Car Rental (Sixt) recorded a 7.1% yoy growth to €43.49mn compar3ed to €40.56mn. Net Debt up to €60.632mbn vs €39.1mn in FY:24 which financed fleet renewal and expansion.

|

Motodynamics |

2024 |

2025 |

Y-o-Y |

2024 |

2025 |

Y-o-Y |

|

EUR thous. |

9M |

9M |

(%) |

Q3 |

Q3 |

(%) |

|

Sales |

144,743 |

161,429 |

11.5% |

58,667 |

64,452 |

9.9% |

|

EBITDA |

26,167 |

27,903 |

6.6% |

16,583 |

17,397 |

4.9% |

|

EBITDA Mrg |

18.1% |

17.3% |

-79 bps |

28.3% |

27.0% |

-127 bps |

|

Net Income |

10,670 |

10,809 |

1.3% |

8,701 |

8,727 |

0.3% |

|

Net Mrg |

7.4% |

6.7% |

-68 bps |

14.8% |

13.5% |

-129 bps |

Mermeren Combinat (9M:25 Results): The group posted a 27.5% increase in top line in Q3:25. EBITDA also up 22.1% to €5.8m while net profit reached €4.8m up 28.3% vs Q3:24. On a 9M basis Mermeren’s net profit is down 15.6%

|

MERMEREN COMBINAT |

2024 |

2025 |

Y-o-Y |

2024 |

2025 |

Y-o-Y |

|

EUR thous. |

9M |

9M |

(%) |

Q3 |

Q3 |

(%) |

|

Sales |

22,660 |

22,584 |

-0.3% |

7,565 |

9,649 |

27.5% |

|

EBITDA |

14,656 |

12,501 |

-14.7% |

4,737 |

5,785 |

22.1% |

|

EBITDA Mrg |

64.7% |

55.4% |

-933 bps |

62.6% |

60.0% |

-267 bps |

|

Net Income |

11,556 |

9,756 |

-15.6% |

3,731 |

4,786 |

28.3% |

|

Net Mrg |

51.0% |

43.2% |

-780 bps |

49.3% |

49.6% |

+28 bps |

Leave a Reply