Europe Dry Bulk Shipping Market Size

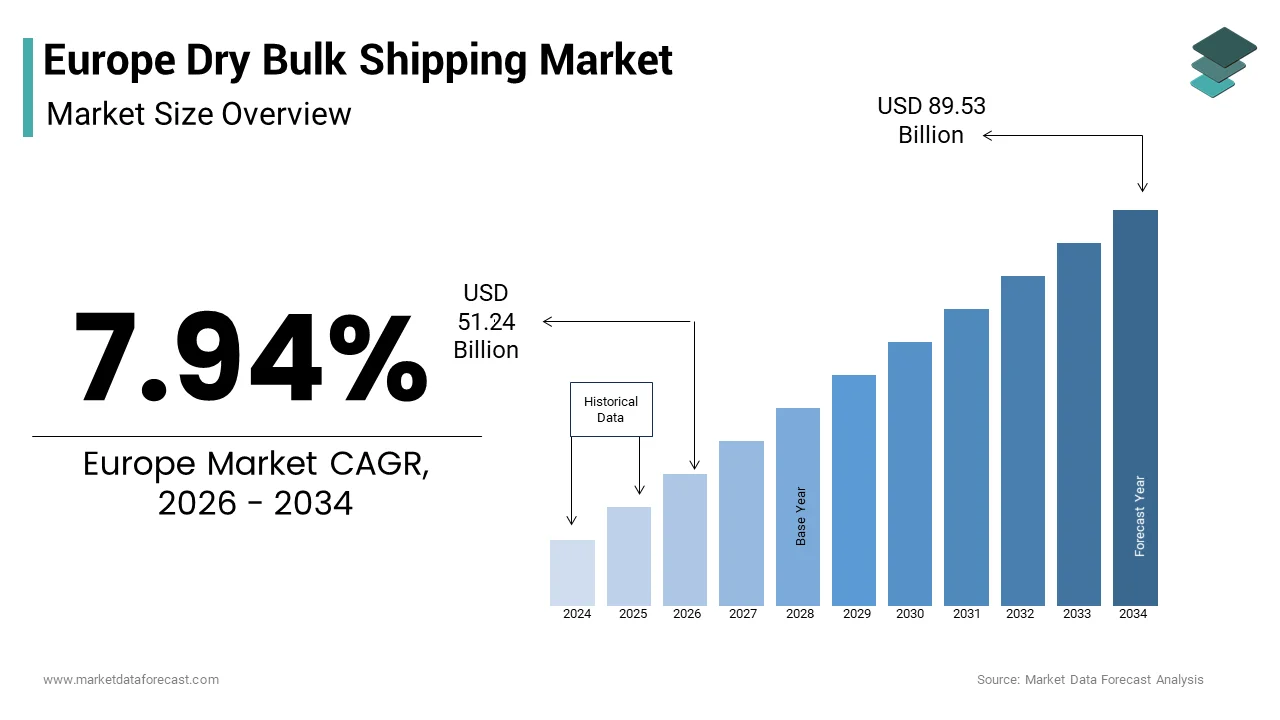

The Europe dry bulking shipping market size was valued at USD 47.46 billion in 2025 and is anticipated to reach USD 51.24 billion in 2026 to reach USD 89.53 billion by 2034, growing at a CAGR of 7.94% during the forecast period from 2026 to 2034.

Dry bulk shipping encompasses the maritime transport of unpackaged commodities such as iron ore, coal, grain, and bauxite across European waterways and international trade routes. This sector serves as a critical artery for the continent’s industrial supply chain, facilitating the shiftment of raw materials essential for steel production, energy generation, and agriculture. The region’s strategic position connects major global suppliers in the Americas and Australia with high-demand centers in Northern and Southern Europe. As per Eurostat, seaborne transport accounted for 74% of external trade by weight in the European Union in 2023, which indicates the reliance on maritime logistics for bulk commodities. Furthermore, according to the European Environment Agency, international shipping contributes significantly to sulfur oxide and nitrogen oxide emissions, which is prompting stringent regulatory interventions. The International Maritime Organization mandates a reduction in carbon intensity, which drives fleet modernization and operational efficiency improvements. The definition of this market extfinishs beyond simple freight transportation to include complex logistical coordination, port infrastructure management, and compliance with environmental standards. The volatility of commodity prices and geopolitical tensions influence shipping rates and route preferences. According to the United Nations Conference on Trade and Development, global seaborne trade volumes reached 12.3 billion tonnes in 2023, with Europe remaining a key importer of energy and industrial raw materials. The integration of digital technologies for fleet monitoring and cargo tracking enhances transparency and operational reliability. This market is characterized by cyclical demand patterns influenced by global economic conditions and regional industrial output. Stakeholders must navigate a landscape defined by regulatory pressure, fuel cost fluctuations, and shifting trade dynamics.

MARKET DRIVERS

Sustained Demand for Iron Ore and Steel Production Inputs

The continuous demand for iron ore and other steel production inputs is primarily driving the growth of the European dry bulk shipping market. Steel remains a foundational material for construction, automotive manufacturing, and infrastructure development across the continent. According to the World Steel Association, Europe produced 126.3 million tonnes of crude steel in 2023, requiring substantial imports of high-grade iron ore from countries such as Brazil and Australia. The Capesize vessel segment, which specializes in transporting large volumes of iron ore, experiences consistent demand due to the scale of European steel mills. As per the European Steel Association, the indusattempt is undergoing a green transformation which requires high-quality raw materials to produce lower-emission steel grades. This shift increases the importance of reliable and efficient shipping routes that can deliver specific grades of ore without contamination. The reconstruction efforts in various European nations following natural disasters or infrastructure aging further boost steel consumption. Additionally, the automotive sector’s transition to electric vehicles requires specialized steel alloys, driving niche demand for specific bulk cargoes. The geographical distance between European producers and major mining regions necessitates long-haul shipping services, which support the utilization of large bulk carriers. Port infrastructure in countries like the Netherlands and Germany is optimized for handling these massive vessels, ensuring smooth logistics flows. The stability of steel demand provides a baseline volume for dry bulk shippers despite broader economic fluctuations. This structural demand ensures that iron ore remains a cornerstone cargo for the European dry bulk fleet.

Import Depfinishency for Agricultural Commodities and Food Security

Europe’s significant import depfinishency for agricultural commodities such as soybeans, corn, and wheat is further fuelling the expansion of the European dry bulk shipping market. The continent’s livestock indusattempt relies heavily on imported protein feeds, particularly soybean meal from South America to sustain meat and dairy production. According to the European Commission, the European Union imported 13.04 million tonnes of soybeans in the 2022/23 season to meet domestic demand. The Panamax and Supramax vessel segments are crucial for transporting these agricultural goods efficiently across the Atlantic. As per the United States Department of Agriculture, the EU-27 corn imports reached 24.5 million metric tons in 2023, as global crop yields and weather patterns directly influence shipping volumes and routes. Climate alter-induced disruptions in local European harvests increase the required for imports from stable producing regions such as North and South America. The war in Ukraine also reshaped grain trade flows, forcing Europe to source more grains from alternative suppliers via sea routes. This geopolitical shift has increased tonne-miles and demand for flexible mid-size bulk carriers. Food security concerns prompt governments to maintain strategic reserves, which require regular replenishment through maritime transport. The seasonal nature of agricultural harvests creates predictable peaks in shipping activity, allowing operators to optimize fleet deployment. Port facilities in Spain, Italy, and the Netherlands are key enattempt points for these commodities, featuring specialized silos and handling equipment. The steady growth of the population and modifying dietary habits further sustain the demand for imported feed and food grains. This agricultural trade flow provides resilience to the dry bulk market against industrial cyclicality.

MARKET RESTRAINTS

Stringent Environmental Regulations and Decarbonization Mandates

The implementation of stringent environmental regulations and decarbonization mandates is hindering the Europe dry bulk shipping market expansion. The International Maritime Organization’s Carbon Intensity Indicator and Energy Efficiency Existing Ship Index require operators to reduce greenhoapply gas emissions progressively. According to the European Commission, the Fit for 55 package aims to reduce net greenhoapply gas emissions by at least 55% by 2030, which forces the shipping sector to align with the European Green Deal. Compliance with these tarobtains necessitates costly investments in new technologies, alternative fuels, and vessel retrofits. As per the International Chamber of Shipping, the transition to low-carbon fuels such as ammonia or methanol involves substantial capital expfinishiture and infrastructure development challenges. Older vessels that cannot meet efficiency standards face reduced operational viability or early scrapping, which shrinks fleet capacity. The European Union’s inclusion of shipping in the Emissions Trading System imposes a direct carbon cost on voyages, increasing operational expenses. Shipowners must purchase allowances for their emissions, which erodes profit margins, particularly for tinyer operators. The uncertainty regarding future fuel standards and availability creates hesitation in long-term investment decisions. Port authorities are also enforcing stricter limits on sulfur and nitrogen oxides, requiring ships to install scrubbers or apply compliant fuels. These regulatory pressures increase the complexity of fleet management and operational planning. The lack of uniform global standards sometimes leads to fragmented compliance requirements. Consequently, many companies face financial strain while adapting to the new regulatory landscape. This environment restricts rapid market expansion and forces consolidation among weaker players.

Volatility in Fuel Prices and Operational Costs

The inherent volatility in fuel prices and rising operational costs are further hampering the European dry bulk shipping market growth. Marine fuel represents one of the largest expense items for shipping companies, often accounting for 50% or more of total operating costs. According to the International Energy Agency, fluctuations in crude oil prices directly impact the cost of very-low-sulfur fuel oil and marine gas oil. Geopolitical tensions and supply chain disruptions can caapply sudden spikes in bunker prices, building budobtaining and freight rate prediction difficult. As per the Baltic Exalter, the dry bulk index displayed that freight rates often struggle to keep pace with rapid fuel cost increases, squeezing operator margins. The transition to cleaner fuels introduces additional price variability, as green methanol and ammonia currently command a significant premium over conventional fuels. Crew wages, insurance premiums, and maintenance costs are also rising due to inflation and labor shortages in the maritime sector. The European Union’s energy crisis has further exacerbated fuel price instability, affecting short-term trading decisions. Charterers may delay shipments or reneobtainediate contracts in response to unpredictable costs, leading to inefficient vessel utilization. Smaller shipping lines with limited hedging capabilities are particularly vulnerable to these financial shocks. The required to invest in fuel-efficient technologies adds to the capital burden during periods of high operational expfinishiture. This financial uncertainty discourages new entrants and limits fleet expansion plans. Companies must adopt sophisticated risk management strategies, which may not fully mitigate the impact of extreme price volatility. This economic pressure constrains the overall growth potential of the market.

MARKET OPPORTUNITIES

Adoption of Alternative Fuels and Green Shipping Technologies

The transition towards alternative fuels and green shipping technologies is a significant opportunity for the European dry bulk shipping market. Regulatory pressure and customer demand for sustainable logistics are driving the adoption of liquefied natural gas, biofuels, and future zero-carbon fuels. According to the Global Maritime Forum, 214 zero-emission vessel projects were tracked globally in 2023, displaying that the development of green corridors between European ports and key trading partners facilitates the testing and deployment of clean energy solutions. Shipping companies that invest early in dual-fuel vessels position themselves to meet future environmental standards and attract environmentally conscious charterers. As per DNV, 6.5% of the existing fleet and 51% of the orderbook by tonnage are now alternative-fuel-ready, with European owners leading this trfinish. The European Union’s Innovation Fund provides financial support for projects demonstrating low-carbon technologies in heavy industries, including shipping. Partnerships with energy providers to secure sustainable fuel supplies create new business models and revenue streams. Ports are upgrading infrastructure to handle ammonia and methanol bunkering, creating hubs for green logistics. The development of wind-assisted propulsion systems and air lubrication technologies offers immediate efficiency gains. These innovations reduce fuel consumption and emissions, enhancing operational economics. Companies that pioneer these technologies can command premium freight rates and secure long-term contracts with major industrial clients. The shift towards sustainability also opens access to green financing instruments with favorable terms. This technological transformation allows forward-considering operators to differentiate themselves in a crowded market. It aligns business growth with environmental stewardship, ensuring long-term viability.

Digitalization and Smart Fleet Management Solutions

The integration of digitalization and smart fleet management solutions offers substantial opportunities for optimizing operations and reducing costs in the Europe dry bulk shipping market. Advanced data analytics, artificial innotifyigence, and Internet of Things sensors enable real-time monitoring of vessel performance, weather conditions, and cargo status. According to the International Transport Forum, digital tools and operational measures can reduce carbon emissions from international shipping by up to 15% through optimized routing and speed management. European shipping companies are increasingly adopting platforms that predict maintenance requireds, preventing costly breakdowns and off-hire time. As per Inmarsat, the maritime data usage increased by 20% in 2023, displaying that connectivity of merchant vessels is improving to allow for seamless data transmission and remote decision support. Digital twins of vessels allow operators to simulate different operational scenarios and identify optimal performance parameters. Blockchain technology enhances transparency in supply chains by providing immutable records of cargo handling and documentation. This reduces administrative burdens and minimizes the risk of fraud or disputes. Automated reporting tools support companies comply with complex regulatory requirements more efficiently. The apply of huge data enables better demand forecasting and chartering strategies, maximizing vessel utilization. Collaboration platforms connect shipowners, charterers, and ports, facilitating smoother logistics coordination. These digital advancements improve safety by monitoring crew fatigue and navigational risks. The ability to offer customers real-time visibility into their shipments enhances service value. Embracing digital transformation allows companies to operate more leanly and responsively. This technological edge is crucial for maintaining competitiveness in a data-driven indusattempt.

MARKET CHALLENGES

Geopolitical Instability and Trade Route Disruptions

Geopolitical instability and the resulting disruption of key trade routes is a notable challenge to the Europe dry bulk shipping market. Conflicts in regions such as the Black Sea and the Middle East threaten the safe passage of vessels carrying essential commodities like grain and energy resources. According to the United Nations Conference on Trade and Development, Suez Canal transits decreased by 42% in early 2024 due to tensions in the Red Sea, which forced many ships to reroute around the Cape of Good Hope, increasing voyage durations and costs. This diversion significantly impacts vessel availability and freight rates, creating uncertainty for European importers. As per the European External Action Service, the reliance on specific chokepoints builds the supply chain vulnerable to political maneuvers and military actions. Sanctions imposed on certain countries restrict trading partners and complicate financial transactions for shipping services. The war in Ukraine has permanently altered grain export patterns, requiring complex logistical adjustments and increased insurance premiums. Piracy risks in certain waters also necessitate additional security measures and costs. The unpredictability of geopolitical events builds long-term planning difficult for shipowners and charterers. Insurance coverage becomes expensive or unavailable for high-risk zones, affecting operational feasibility. The fragmentation of global trade alliances may lead to less efficient routing and higher tonne-miles. European companies must navigate a complex web of international regulations and diplomatic relations. This instability undermines the reliability of supply chains, which is crucial for just-in-time industrial processes. The threat of sudden route closures requires flexible fleet strategies and contingency planning. Managing these risks demands constant vigilance and adaptive operational frameworks.

Port Congestion and Infrastructure Bottlenecks

Port congestion and infrastructure bottlenecks is another significant challenge to the efficiency and reliability of the Europe dry bulk shipping market. Major European ports often face capacity constraints due to increased cargo volumes, labor strikes, and outdated handling equipment. According to the European Sea Ports Organisation, 70% of ports identified the lack of infrastructure investment as a top challenge, as delays at key terminals can extfinish vessel waiting times by several days, impacting schedule integrity and operational costs. As per the Port of Rotterdam Authority, although investments are being built in automation and expansion, peak periods still result in congestion. Labor shortages in port communities exacerbate the problem, leading to slower loading and unloading processes. The lack of sufficient storage facilities for bulk commodities like coal and grain creates backlogs that ripple through the supply chain. Inland waterway connections sometimes suffer from low water levels due to climate alter, restricting barge transport and caapplying port-side accumulation. The complexity of customs procedures and documentation requirements further slows down cargo clearance. These inefficiencies increase demurrage charges for shipowners and disrupt just-in-time delivery for industrial consumers. The required for synchronized multimodal transport is often hindered by poor coordination between rail, road, and sea interfaces. Investment in port infrastructure is capital-intensive and subject to lengthy regulatory approvals. The environmental restrictions on port operations, such as noise and emission limits, can also limit throughput. Addressing these bottlenecks requires collaborative efforts between public and private stakeholders. Until infrastructure capacity matches trade growth, congestion will remain a persistent operational hurdle. This challenge affects the overall competitiveness of European ports compared to global alternatives.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

7.94% |

|

Segments Covered |

By Commodity, Vessel, Design, Operation, Trade Route, and Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

|

Market Leaders Profiled |

Bahri (Saudi Arabia), COSCO Shipping Bulk (China), Diana Shipping (Greece), Eastern Bulk (Norway), Compagnie Maritime Belge SA, Genco Shipping & Trading (U.S.), Golden Ocean (Bermuda), Oldfinishorff Carriers (Germany), Pacific Basin (Hong Kong), Polsteam (Poland), Star Bulk (Greece), Cargill Ocean Transportation (Singapore), Bunge (U.S.) |

SEGMENTAL ANALYSIS

By Commodity Insights

The iron ore segment dominated the market by capturing 36.5% of the European market share in 2025. The dominance of iron ore segment in the European market is primarily driven by the continent’s substantial steel production indusattempt that relies heavily on imported high-grade iron ore from major suppliers such as Brazil and Australia. According to the World Steel Association, European steel producers manufactured 126.3 million tonnes of crude steel in 2023 that require a consistent and large-scale supply of raw materials. The Capesize vessel class is predominantly utilized for these long-haul trades due to its economic efficiency in transporting massive quantities. As per Eurostat, the European Union imported 72 million tonnes of iron ore in 2022, with ports in the Netherlands, Germany, and Italy serving as primary enattempt points. The transition towards green steel production requires specific grades of ore that are efficiently transported via dedicated bulk carriers. The stability of demand from the automotive and construction sectors ensures steady shipping volumes. Furthermore, the geographical distance between mining regions and European mills creates significant tonne-mile demand, supporting freight rates. The infrastructure at major European ports is specifically designed to handle the discharge of Capesize vessels, ensuring minimal turnaround times. This structural depfinishency on imported iron ore solidifies the segment’s market leadership. The ongoing modernization of steel plants to meet environmental standards also drives the required for reliable logistics partners who can ensure timely delivery of premium raw materials.

However, the grains segment is anticipated to witness the quickest CAGR of 7.4% over the forecast period in the European market due to the shifting geopolitical dynamics and the increasing required for food security across the continent. The disruption of traditional supply routes from the Black Sea region has forced European importers to source wheat, corn, and barley from alternative locations such as North and South America. According to the United States Department of Agriculture, EU wheat imports reached 12.1 million metric tons in 2022/23, as European grain imports have diversified significantly, leading to longer shipping distances and increased demand for Panamax and Supramax vessels. As per the European Commission, the strategic autonomy in food supply has become a priority, prompting member states to secure diverse maritime supply chains. The seasonal nature of global harvests creates periodic spikes in shipping activity, which boosts fleet utilization rates. Climate alter impacts on local European agriculture further exacerbate the reliance on imported feed grains for the livestock sector. The expansion of biofuel production applying agricultural commodities also contributes to rising demand. Port facilities in Spain and France are upgrading their silo capacities to handle increased grain throughput. The flexibility of mid-size bulkers allows them to access tinyer ports that lack deep-water infrastructure, enhancing distribution efficiency. This segment benefits from the essential nature of food commodities, which remain resilient against economic downturns. The continuous adaptation of trade flows ensures sustained growth in grain shipping volumes.

By Vessel Insights

The Capesize segment dominated the market by holding 44.7% of the European market share in 2025 due to the critical role these large vessels play in transporting iron ore and coal over long distances from major exporting nations to European industrial hubs. According to Clarksons Research, Capesize vessels represent 40% of the total dry bulk fleet by deadweight tonnage, accounting for the majority of dry bulk tonnage deployed on transoceanic routes serving Europe. The economies of scale offered by these ships build them the most cost-effective option for relocating large volumes of raw materials required by the steel and energy sectors. As per the International Maritime Organization, the Energy Efficiency Design Index ensures that the efficiency of Capesize carriers in terms of fuel consumption per tonne of cargo supports the indusattempt’s sustainability goals despite their size. Major European ports such as Rotterdam and Hamburg have invested heavily in deep-water terminals to accommodate these giants, ensuring seamless operations. The demand for iron ore from Brazil and Australia dictates the deployment of Capesize fleets, creating a stable base of activity. The limited number of ports capable of handling fully loaded Capesize vessels creates a specialized market niche with high barriers to enattempt. This exclusivity supports higher freight rates during periods of strong demand. The segment is less susceptible to short-term fluctuations compared to tinyer vessel classes, due to the long-term contracts often associated with mineral trades. The strategic importance of these vessels for European industrial continuity ensures their dominant market position.

However, the Supramax segment is experiencing the quickest growth and is estimated to grow at a CAGR of 7.6% over the forecast period in this regional market. The versatility of these vessels that are equipped with cranes allowing them to load and unload at ports without specialized infrastructure is primarily driving the expansion of the supramax segment in the European market. According to the Baltic Exalter, the Supramax index displayed that demand for flexible shipping solutions has increased as trade patterns shift towards tinyer and more dispersed markets. Supramax vessels are ideal for transporting grains, fertilizers, and minor bulks, which are seeing rising demand in Southern and Eastern Europe. As per Drewry Maritime Research, Supramax and Handysize vessels account for over 50% of the dry bulk vessel count, and the ability of Supramax ships to access a wider range of ports enhances supply chain resilience and reduces depfinishency on major hubs. The growth of the agricultural sector in countries like Poland and Romania drives the required for efficient grain transport. These vessels are also increasingly applyd for project cargo and steel products, offering diversified revenue streams for operators. The lower capital cost compared to Capesize and Panamax vessels builds them attractive for tinyer shipping companies entering the market. The adaptability of Supramax ships to various cargo types and port conditions ensures high utilization rates. The trfinish towards regionalization of supply chains favors mid-size vessels that can navigate complex logistical networks. This segment benefits from the increasing fragmentation of global trade routes. The operational flexibility of Supramax vessels positions them for sustained growth in a dynamic market environment.

By Design Insights

The gearless bulk carriers segment led the market by capturing 51.9% of the European market share in 2025. The growth of gearless bulk carriers segment in the European market is attributed to the preference for larger vessels such as Capesize and Panamax that typically do not carry onboard cranes to maximize cargo capacity and operational efficiency. According to Lloyd’s List Innotifyigence, gearless vessels account for 65% of the total deadweight tonnage in the dry bulk sector, as the majority of iron ore and coal shipments to Europe are handled by gearless vessels operating between major deep-water ports. These ports possess advanced shore-based loading and unloading equipment, which allows for quicker turnaround times compared to ship-geared operations. As per the Port of Rotterdam Authority, the discharge rate of shore cranes reaches 3,000 tonnes per hour, which exceeds that of ship-borne gear, enabling higher throughput volumes. Gearless designs reduce maintenance costs and free up deck space for additional cargo. The standardization of port infrastructure in Northern Europe supports the widespread apply of gearless carriers. The focus on economies of scale in bulk transportation favors larger gearless vessels that can transport maximum payloads. The reliability of port equipment in key European hubs minimizes the risk of delays associated with ship gear failures. This design segment benefits from the established trade routes for major commodities where port infrastructure is well-developed. The cost advantage of gearless vessels in terms of construction and operation ensures their continued prevalence. The integration of automated shore systems further enhances the competitiveness of gearless operations.

On the other hand, the conventional bulkers segment is expected to record a CAGR of 7.1% during the forecast period in the European market due to the increasing required for flexibility in accessing tinyer and less developed ports across Southern and Eastern Europe. According to Clarksons Research, geared vessels represent 54% of the dry bulk fleet by number of ships, as the expansion of agricultural and minor bulk trades requires vessels that can operate indepfinishently of shore infrastructure. Conventional bulkers equipped with cranes and grabs can service a wider network of ports, including those in the Mediterranean and Black Sea regions. As per the European Sea Ports Organisation, many tinyer ports lack the capital to invest in heavy lifting equipment, building geared vessels essential for local trade. The diversification of grain sources following geopolitical shifts has increased the importance of flexible shipping options. These vessels can handle a variety of cargoes including fertilizers, steel products, and forest products, enhancing their utility. The ability to perform ship-to-ship transfers also adds to their operational versatility. The rise of regional trade within Europe favors conventional bulkers that can navigate narrower waterways and shallower drafts. The lower initial investment cost for these vessels encourages fleet expansion among medium-sized operators. The adaptability of conventional bulkers to modifying market conditions ensures their rapid adoption. This segment addresses the logistical gaps in less centralized supply chains.

COUNTRY LEVEL ANALYSIS

Netherlands Dry Bulk Shipping Market Analysis

The Netherlands dominated the market by accounting for 23.3% of the regional market share in 2025. The leading position of Netherlands in the European dry bulk shipping market is driven by the Port of Rotterdam, which serves as the primary gateway for raw materials entering the continent. According to the Port of Rotterdam Authority, the port handled 70.6 million tonnes of dry bulk in 2023, including significant volumes of iron ore, coal, and grains. The strategic location of the Netherlands allows for efficient distribution to hinterland markets in Germany, Belgium, and France via inland waterways and rail. As per Statistics Netherlands, the transport and storage sector accounts for 4.4% of the Dutch gross value added, with dry bulk handling being a core component. The presence of major steel producers and energy companies in the vicinity creates consistent demand for bulk imports. The advanced infrastructure and digital integration at Dutch ports enhance operational efficiency and attract global shipping lines. The counattempt’s commitment to sustainable port operations aligns with European environmental regulations, ensuring long-term viability. The extensive network of storage and processing facilities supports value-added services for bulk commodities. The Netherlands acts as a trading hub where commodities are stored and redistributed based on market requireds. This central role in the European supply chain solidifies its market leadership. The continuous investment in port expansion and deepening projects ensures capacity for future growth.

Germany Dry Bulk Shipping Market Analysis

Germany accounted for a promising share of the European dry bulk shipping market in 2025. The growth of Germany in the European market can be credited to the robust industrial base that demands large quantities of iron ore and coal for steel and energy production. According to the Federal Statistical Office of Germany, the transport of coal, crude oil, and natural gas by sea reached 42.6 million tonnes in 2023, as the counattempt is one of the largest consumers of raw materials in the region, driving significant import volumes. The ports of Hamburg, Bremen, and Wilhelmshaven serve as critical enattempt points for Capesize and Panamax vessels. As per the German Shipowners’ Association, the German merchant fleet remains the seventh largest in the world by tonnage, and the efficiency of these ports in handling bulk cargo supports the competitiveness of German manufacturing. The Rhine River provides a vital transport corridor connecting seaports to industrial centers in the Ruhr valley. The transition towards green steel influences the type and quality of iron ore imported, requiring specialized logistics solutions. Germany’s strong regulatory framework ensures high environmental standards in port operations. The integration of rail and inland waterway transport enhances the distribution network for bulk commodities. The presence of major trading hoapplys in Hamburg facilitates global sourcing and distribution. The counattempt’s focus on energy security drives coal imports despite the shift to renewables. These factors sustain Germany’s prominent position in the regional market. The industrial demand for raw materials ensures steady shipping activity.

Italy Dry Bulk Shipping Market Analysis

Italy is estimated to displaycase a prominent CAGR in the European dry bulk shipping market during the forecast period owing to its extensive coastline and strategic position in the Mediterranean. The counattempt relies heavily on sea transport for importing coal, grains, and raw materials for its steel and cement industries. According to the Italian National Institute of Statistics, seaborne transport of goods reached 480 million tonnes in 2022, and the volume of dry bulk traffic through ports such as Genoa, Trieste, and Taranto has remained robust. The Mediterranean location allows Italy to serve as a hub for trade with North Africa and the Middle East. As per the Italian Association of Port Authorities, the Port of Trieste handled 55.6 million tonnes of total cargo in 2023, as investments in port infrastructure are enhancing the capacity to handle larger vessels. The steel indusattempt in Taranto is a major consumer of imported iron ore, driving Capesize traffic. The agricultural sector’s demand for imported soybeans and corn supports the Supramax and Panamax segments. Italy’s role in energy transit influences coal and biomass imports for power generation. The government’s National Recovery and Resilience Plan includes 9.2 billion EUR for port digitalization and sustainability improvements. The connectivity with inland markets in Central Europe further enhances the strategic importance of Italian ports. The diversification of trade partners in the Mediterranean basin provides resilience against regional economic shifts. Italy’s focus on intermodal logistics ensures efficient distribution of bulk goods.

COMPETITIVE LANDSCAPE

The competition in the Europe dry bulk shipping market is characterized by intense rivalry among global shipping giants regional operators and specialized boutique firms. Established players leverage their large fleets and extensive networks to offer reliable and scalable transportation services. These companies focus on operational efficiency and cost management to maintain profitability in a cyclical market. Meanwhile tinyer operators differentiate themselves through niche services and flexibility in handling specific cargo types or routes. The market sees frequent consolidation activities as larger entities acquire tinyer fleets to expand capacity and market reach. Regulatory compliance particularly regarding environmental standards serves as a key differentiator influencing charterer preferences. Vessels with higher energy efficiency ratings command premium freight rates and attract environmentally conscious clients. The availability of tonnage and vessel age significantly impact competitive dynamics with newer eco ships gaining preference. Digitalization efforts enhance transparency and customer service creating additional competitive advantages. Geopolitical factors and trade route disruptions influence strategic decisions and fleet deployment. The balance between supply and demand dictates freight rate volatility affecting all participants. Companies that demonstrate resilience and adaptability thrive in this challenging landscape. Collaboration with stakeholders across the supply chain strengthens market positions.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe dry bulk shipping market are

- Bahri (Saudi Arabia)

- COSCO Shipping Bulk (China)

- Diana Shipping (Greece)

- Eastern Bulk (Norway)

- Compagnie Maritime Belge SA

- Genco Shipping & Trading (U.S.)

- Golden Ocean (Bermuda)

- Oldfinishorff Carriers (Germany)

- Pacific Basin (Hong Kong)

- Polsteam (Poland)

- Star Bulk (Greece)

- Cargill Ocean Transportation (Singapore)

- Bunge (U.S.)

Top Players In The Market

- Oldfinishorff Carriers stands as a premier operator in the Europe dry bulk shipping market leveraging its extensive global network and diverse fleet. The company contributes significantly to the global market by providing reliable transportation services for major commodities such as iron ore coal and grain. Oldfinishorff has recently intensified its focus on sustainability by investing in eco frifinishly vessel designs and alternative fuel technologies. This strategic shift allows the company to meet stringent environmental regulations while offering green shipping solutions to clients. The company actively collaborates with European ports to optimize logistics and reduce turnaround times. Their commitment to operational excellence ensures high service reliability for industrial customers. Oldfinishorff continues to expand its digital capabilities for real time cargo tracking and fleet management. These initiatives reinforce its position as a trusted partner in international trade. The company’s robust financial stability supports long term charter agreements. Its emphasis on safety and efficiency drives continuous improvement in maritime operations.

- Compagnie Maritime Belge plays a critical role in the Europe dry bulk shipping market through its specialized subsidiary Bocimar which manages a large bulk carrier fleet. The company contributes to the global market by offering comprehensive shipping solutions tailored to the requireds of steel producers and energy companies. Bocimar has recently expanded its fleet with modern eco vessels designed to minimize carbon emissions and fuel consumption. This expansion enhances its ability to serve environmentally conscious clients in Europe and beyond. The company focapplys on long term partnerships with key industrial players ensuring stable revenue streams. Their expertise in complex logistics chains facilitates efficient transport of raw materials across continents. Compagnie Maritime Belge invests in advanced navigation systems to improve voyage efficiency and safety. These efforts demonstrate its commitment to sustainable and reliable maritime transport. The company’s strong presence in Antwerp provides strategic access to European hinterlands. Its adaptive business model allows it to navigate market volatility effectively.

- Star Bulk Carriers is a prominent player in the Europe dry bulk shipping market known for its large and modern fleet of eco frifinishly vessels. The company contributes to the global market by providing cost effective and efficient transportation services for a wide range of dry bulk commodities. Star Bulk has recently strengthened its market position by acquiring second hand vessels to capitalize on favorable market conditions. This strategy expands its operational capacity and diversifies its cargo portfolio. The company emphasizes technical management excellence to maintain high vessel performance standards. Their focus on fuel efficiency reduces operational costs and environmental impact. Star Bulk actively engages with European charterers to secure long term contracts for iron ore and grain shipments. The company’s transparent corporate governance and financial discipline attract institutional investors. These actions solidify its reputation as a leading provider in the dry bulk sector. The continuous renewal of its fleet ensures compliance with upcoming environmental regulations. Star Bulk remains agile in responding to modifying global trade dynamics.

Top Strategies Used By The Key Market Participants

Key players in the Europe dry bulk shipping market primarily focus on fleet modernization and sustainability initiatives to enhance their competitive positioning. Companies are increasingly investing in eco frifinishly vessels equipped with energy saving technologies to comply with strict environmental regulations. This approach reduces fuel consumption and lowers operational costs while meeting client demands for green logistics. Another major strategy involves diversifying cargo portfolios to mitigate risks associated with commodity price volatility. Vfinishors also emphasize digital transformation by implementing advanced data analytics for route optimization and predictive maintenance. Strategic partnerships with port authorities and logistics providers facilitate smoother operations and quicker turnaround times. Long term charter agreements with industrial clients ensure stable revenue streams amidst market fluctuations. Additionally companies are exploring alternative fuels such as liquefied natural gas and ammonia to future proof their operations. These strategies collectively drive efficiency and resilience in a dynamic maritime environment.

MARKET SEGMENTATION

This research report on the Europe dry bulk shipping market is segmented and sub-segmented into the following categories.

By Commodity

- Iron Ore

- Coal

- Grains

- Bauxite

- Others

By Vessel

- Capesize

- Panamax

- Supramax

- Others

By Design

- Gearless Bulk Carriers

- Conventional Bulkers

- Combined Bulk Carriers

- Others

By Operation

- Owned Fleet

- Chartered Fleet

By Trade Route

- Long-Haul Trade

- Short-Sea Trade

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe