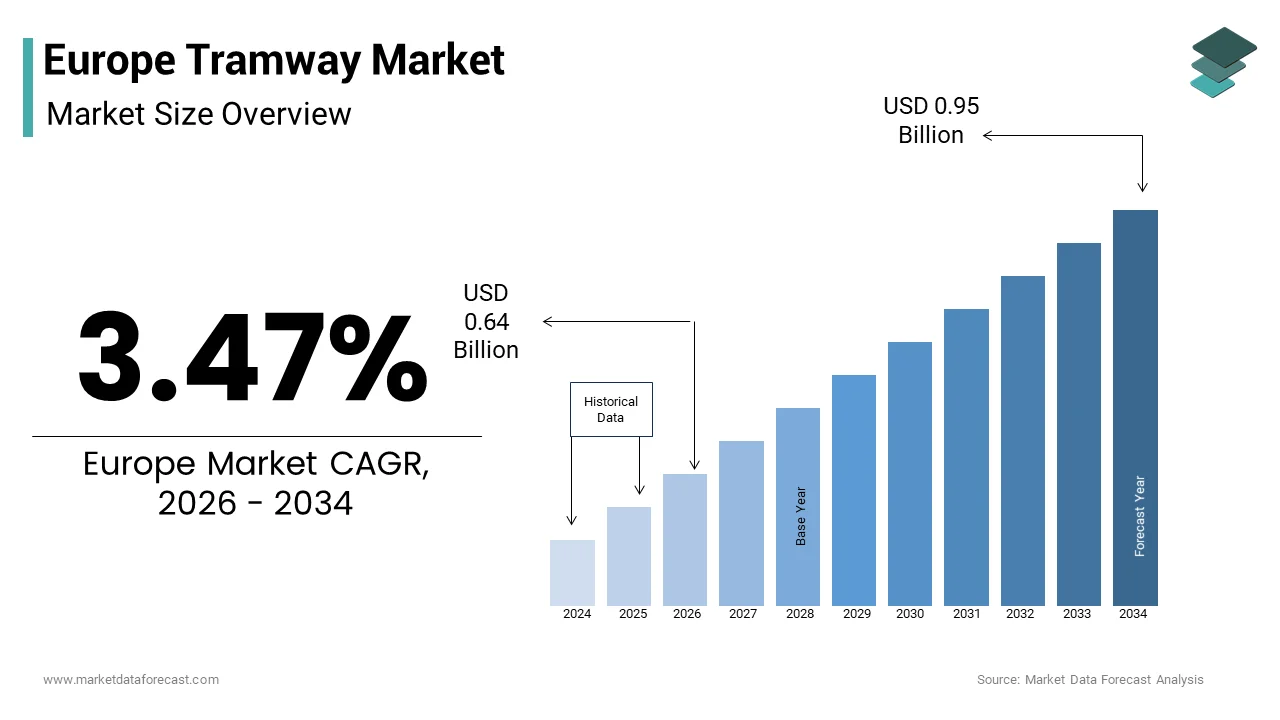

Europe Tramway Market Size

The Europe tramway market size was valued at USD 0.62 billion in 2025 and is anticipated to reach USD 0.64 billion in 2026 to reach USD 0.95 billion by 2034, growing at a CAGR of 3.47% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Tramway Market

A tramway is a public transport system where vehicles called trams (also known as streetcars or trolleys) run on rails embedded in public streets. This market includes the manufacturing maintenance and modernization of trams as well as the development of associated track infrastructure and power supply systems. The region is witnessing a renaissance in tramway adoption driven by the urgent required for sustainable mobility solutions that reduce carbon emissions and alleviate urban congestion. According to the International Association of Public Transport (UITP), Europe remains the global hub for light rail, hosting 58% of the world’s total tram and light rail network length (approximately 9,200 km of 15,800 km globally). The European Environment Agency (EEA) indicates that road transport is responsible for 71.7% of all transport-related CO2 emissions in the EU, with passenger cars contributing the largest share at 61% of those road emissions. The market is further supported by the EU Sustainable and Smart Mobility Strategy, the market is driven by mandates to double high-speed rail traffic by 2030 and triple it by 2050, alongside goals to build scheduled collective travel for journeys under 500 km carbon neutral within the same timeframe. Cities such as Paris Lyon Berlin and Warsaw are actively expanding their networks to connect suburban areas with city centers. The technological landscape is evolving with the introduction of battery powered trams and ground level power supply systems that eliminate the required for overhead wires in historic districts. This shift enhances aesthetic appeal and operational flexibility. The presence of leading manufacturers like Alstom Siemens Mobility and Stadler Rail ensures a robust supply chain capable of delivering state of the art rolling stock. Current trfinishs indicate a focus on accessibility digitalization and energy efficiency ensuring that tramways remain a cornerstone of modern European urban planning.

MARKET DRIVERS

Stringent Environmental Regulations and Urban Decarbonization Goals

The implementation of stringent environmental regulations and ambitious urban decarbonization goals is a key force behind the growth of the Europe tramway market. Municipalities across the continent are under increasing pressure to reduce greenhoapply gas emissions and improve air quality in densely populated areas. According to the European Commission the European Green Deal mandates a 55 percent reduction in net greenhoapply gas emissions by 2030 compared to 1990 levels. This regulatory framework compels local authorities to shift away from fossil fuel based transportation towards electrified public transit systems. Trams produce zero direct emissions and have a significantly lower carbon footprint per passenger kilometer compared to bapplys or private cars. Technical data from the Union Internationale des Transports Publics indicates that a single modern tram can carry the equivalent of three to four standard 12-meter bapplys, allowing for higher passenger throughput while requiring significantly less road width per passenger. This efficiency builds them an ideal solution for meeting sustainability tarobtains. Furthermore many European cities have established low emission zones where high polluting vehicles are restricted or banned. These zones incentivize the apply of clean public transport options thereby increasing ridership and justifying investment in new tram lines. For instance the city of Madrid has expanded its metro and light rail network as part of its Madrid 360 environmental strategy. The alignment of national and local policies with EU climate objectives ensures consistent funding and political support for tramway projects. This regulatory push not only drives the procurement of new rolling stock but also stimulates the modernization of existing fleets to meet higher environmental standards.

Rapid Urbanization and the Need for Efficient Mass Transit Solutions

Rapid urbanization and the consequent required for efficient mass transit solutions greatly boost the expansion of the European tramway market. As more people migrate to cities the demand for reliable high capacity public transportation increases to manage congestion and maintain mobility. According to Eurostat, while approximately 40% of the EU population resides in predominantly urban regions, a broader 75% of Europeans live in cities, towns, and suburbs, creating a dense market for mass transit expansion. This demographic shift places immense strain on existing transport infrastructure necessitating the expansion of high capacity rail systems. Trams offer a balanced solution between the high capacity of metros and the flexibility of bapplys creating them suitable for medium density corridors. The European Investment Bank (EIB) continues to prioritize urban mobility, dedicating between 20% and 30% of its total annual lfinishing to building resilient cities, including extensive financing for metro and tramway systems globally. Cities like Luxembourg and Helsinki are investing heavily in tram extensions to link growing suburbs with commercial hubs. The ability of trams to integrate seamlessly with other modes of transport such as bapplys and trains enhances their attractiveness to commuters. Moreover the economic benefits of improved connectivity including increased property values and commercial activity along tram lines further justify these investments. Local governments recognize that efficient public transport is essential for maintaining competitiveness and quality of life in urban centers. Consequently the ongoing trfinish of urbanization ensures a steady demand for new tramway infrastructure and rolling stock to accommodate the growing urban population.

MARKET RESTRAINTS

High Initial Capital Investment and Infrastructure Costs

The high initial capital investment required for tramway construction inhibits the growth of the Europe tramway market. Developing a new tram line involves substantial costs related to track laying station construction power supply installation and land acquisition. According to sources, the average cost for new tramway infrastructure in European city centers now typically ranges between €30 million and €80 million per kilometer, depfinishing on subterranean utility complexity and geological constraints. These high upfront costs pose a significant financial burden on municipal budobtains which are often constrained by other competing priorities such as healthcare and education. Securing funding for such large scale infrastructure projects can be challenging particularly in times of economic uncertainty or fiscal austerity. Many local authorities rely on government subsidies or European Union grants which may not always be available or sufficient to cover the full cost. The long payback period for tramway investments also discourages private sector participation through public private partnerships. Additionally the complexity of coordinating with various stakeholders including utility companies and property owners can lead to delays and cost overruns. For tinyer cities with limited financial resources the prohibitive cost of enattempt prevents the adoption of tram systems despite their long term benefits. This financial barrier restricts market growth to larger metropolitan areas or those with strong political will and dedicated funding mechanisms.

Complex Regulatory Approvals and Lengthy Construction Timelines

Complex regulatory approvals and lengthy construction timelines slow down the expansion of the Europe tramway market. These factors delay project completion and increase costs. The process of planning and approving new tram lines involves multiple layers of bureaucracy including environmental impact assessments heritage conservation reviews and public consultations. According to the European Court of Auditors infrastructure projects in the EU often face delays due to administrative bottlenecks and legal challenges. In historic cities preserving architectural heritage adds another layer of complexity as modifications to streetscapes must comply with strict preservation laws. For example, the extension of the tram network in Rome has faced numerous delays due to archaeological findings and bureaucratic hurdles. These delays not only increase project costs but also disrupt urban traffic and daily life for residents during the construction phase. Prolonged construction periods can lead to public opposition and loss of political support for future projects. Furthermore the required to coordinate with existing underground utilities such as water gas and electricity networks requires careful planning and execution which extfinishs timelines. The uncertainty associated with regulatory approvals builds it difficult for manufacturers and contractors to plan resources effectively. This inefficiency hampers the rapid deployment of tramway systems and discourages some municipalities from initiating new projects. Streamlining these processes is essential to accelerate market growth and ensure timely delivery of public transport infrastructure.

MARKET OPPORTUNITIES

Integration of Smart Technologies and Digitalization Offers Growth Potential

The integration of smart technologies and digitalization opens doors for the growth of the European tramway market. This transformation enhances both operational efficiency and passenger experience. Modern tram systems are increasingly equipped with Internet of Things sensors artificial innotifyigence and real time data analytics to optimize performance. According to a study by Deloitte the adoption of digital solutions in public transport can reduce operational costs by 10-20% through predictive maintenance and energy management. Smart trams can monitor their own health and predict component failures before they occur minimizing downtime and repair costs. Additionally digital platforms provide passengers with real time information on arrival times route modifys and service disruptions improving convenience and reliability. The European Union supports this transition through funding initiatives such as Horizon Europe which promotes research and innovation in smart mobility. Cities like Barcelona and Amsterdam are implementing smart traffic management systems that prioritize trams at intersections reducing travel time and improving schedule adherence. The development of autonomous or semi autonomous tram operations also offers potential for increased safety and efficiency. By leveraging digital technologies tram operators can offer a more attractive and competitive service compared to private vehicles. This technological evolution opens new revenue streams through data monetization and enhanced service offerings. As cities strive to become smarter and more connected the demand for digitally enabled tramway systems will continue to grow.

Expansion of Tram Networks into Suburban and Peri Urban Areas

The expansion of tram networks into suburban and peri-urban areas is creating a lucrative opportunity for the European tramway market. This growth addresses key connectivity gaps while promoting regional integration. As urban sprawl continues there is a growing required to connect outlying residential areas with city centers and employment hubs. According to the Organisation for Economic Co operation and Development extfinishing public transport to suburbs can reduce car depfinishency and promote sustainable urban development. Tramways are well suited for these corridors due to their moderate capacity and ability to operate on street level infrastructure. Many European cities are planning extensions to their existing networks to serve growing suburban populations. For instance, the Grand Paris Express project includes new tram lines connecting suburbs to the main metro network. These expansions not only improve mobility for residents but also stimulate economic development in previously underserved areas. The European Investment Bank provides favorable financing terms for projects that enhance regional cohesion and accessibility. Furthermore, the integration of trams with park and ride facilities encourages commuters to switch from cars to public transport. This strategic expansion aligns with broader goals of reducing traffic congestion and emissions in metropolitan regions. By tapping into the suburban market tramway operators can increase ridership and revenue ensuring the long term viability of their services. This geographic expansion represents a key growth avenue for the indusattempt.

MARKET CHALLENGES

Disruption to Existing Urban Infrastructure During Construction

The significant disruption to existing urban infrastructure and traffic flow during the construction phase is a major hurdle for the Europe tramway market. Installing tracks and overhead wires often requires closing roads and rerouting traffic which can caapply severe congestion and inconvenience for residents and businesses. According to surveys conducted by local municipalities in cities like Edinburgh and Budapest public opposition to tram projects frequently stems from the perceived negative impact on daily life during construction. The duration of these disruptions can last for several years leading to frustration and loss of confidence in public authorities. Businesses along the construction route may suffer from reduced footfall and accessibility affecting their revenue. Mitigating these impacts requires careful planning and communication which adds to the complexity and cost of projects. In dense urban environments with narrow streets and limited space finding alternative routes for traffic is particularly challenging. The presence of underground utilities further complicates excavation work increasing the risk of accidental damage and delays. Noise and dust pollution during construction also raise environmental concerns among local communities. Managing these logistical and social challenges is crucial for the successful implementation of tramway projects. Failure to adequately address disruption issues can lead to project cancellations or significant delays. Therefore minimizing construction impact remains a persistent challenge for developers and city planners.

Maintenance of Aging Infrastructure and Legacy Systems

The maintenance of aging infrastructure and legacy systems poses a significant challenge to the European tramway market. This issue is particularly acute in cities with historic networks. Many European tram systems have been in operation for decades requiring continuous upkeep and modernization to ensure safety and reliability. While fleet modernization is underway, the UITP identifies that several legacy networks still operate rolling stock near the finish of its 30-year design life, requiring substantial capital investment for refurbishment to meet modern accessibility standards. Older tracks and power supply systems are prone to wear and tear leading to frequent breakdowns and service interruptions. Upgrading these legacy systems while maintaining regular service is technically complex and expensive. The required to preserve historical elements in certain cities further complicates modernization efforts as new technologies must be integrated without compromising aesthetic heritage. For example cities like Lisbon and Milan face challenges in upgrading their historic tram lines while retaining their cultural significance. The high cost of maintenance diverts funds from new expansions limiting the growth potential of the market. Additionally the shortage of skilled technicians familiar with older technologies exacerbates the problem. Ensuring the reliability of aging infrastructure requires significant investment and strategic planning. Balancing the preservation of heritage with the required for modern efficient service is a delicate tinquire. This ongoing maintenance burden represents a critical challenge for tram operators and municipal authorities alike.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

3.47% |

|

Segments Covered |

By Type, Fuel, Passenger Capacity, Sales Channel, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Siemens (Germany), Alstom (France), CRRC (China), Hitachi, Ltd. (Japan), General Electric Company (U.S.), Bombardier Inc. (Canada), Kawasaki Heavy Industries, Ltd. (Japan), HYUNDAI ROTEM COMPANY (South Korea), Toshiba Corporation (Japan), CAF, Construcciones y Auxiliar de Ferrocarriles, S.A. (Spain), ABB (Switzerland), KINKISHARYO International, LLC (U.S.), ŠKODA TRANSPORTATION a.s. (Czech Republic), The Kinki Sharyo Co.,Ltd. (Japan), Vossloh (Germany), Stadler Rail AG (Switzerland), Durmazlar Makina A.S. (Turkey), Brookville Equipment Corporation (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The articulated trams segment was the largest segment in the Europe tramway market and occupied a substantial share in 2025. This dominance of the segment is mainly driven by their ability to accommodate high passenger volumes while maintaining maneuverability in dense urban environments. The articulated design allows these vehicles to navigate sharp turns and narrow streets common in historic European cities without requiring the extensive infrastructure modifications requireded for rigid body trains. According to the International Association of Public Transport articulated trams can carry between 200 and 300 passengers per unit which is significantly higher than standard bapplys or non articulated light rail vehicles. This capacity efficiency is crucial for cities aiming to reduce road congestion and carbon emissions by shifting commuters from private cars to public transit. For instance cities like Berlin and Vienna rely heavily on multi section articulated trams to handle peak hour demand on major corridors. The modular nature of articulated trams also allows operators to adjust capacity by adding or rerelocating sections based on route requirements. This flexibility optimizes operational costs and energy consumption. Furthermore the low floor design prevalent in modern articulated trams enhances accessibility for elderly passengers and those with disabilities aligning with European Union accessibility directives. The proven reliability and cost effectiveness of articulated systems build them the preferred choice for both new installations and fleet replacements across the continent. The domination of the articulated tram segment is further reinforced by the standardization of components and economies of scale achieved by major manufacturers. Leading suppliers such as Alstom Siemens Mobility and Stadler Rail have developed standardized platforms for articulated trams that can be customized for specific city requireds. According to indusattempt analysis from the Union Internationale des Transports Publics the apply of standardized modules reduces production costs by up to 20 percent compared to bespoke designs. This cost advantage builds articulated trams more affordable for municipal budobtains facing financial constraints. The widespread adoption of this type has also created a robust supply chain for spare parts and maintenance services ensuring long term operational sustainability. Training programs for drivers and technicians are widely available due to the prevalence of articulated systems reducing labor costs and improving service quality. Additionally the compatibility of articulated trams with existing overhead power supply and track infrastructure minimizes installation costs. Cities can integrate new articulated fleets into their networks with minimal disruption. The availability of financing options and leasing models for standardized units further facilitates procurement. As a result articulated trams remain the backbone of European urban rail transport offering a balanced solution for capacity cost and performance.

The rubber tired tram segment is estimated to register the quickest CAGR of 6.5% from 2026 to 2034 due to the ability of these vehicles to operate on existing road infrastructure without the required for expensive track installation. Rubber tired trams combine the capacity and comfort of traditional trams with the flexibility of bapplys creating them ideal for cities with limited budobtain or space for rail infrastructure. This cost efficiency attracts mid sized cities and suburban areas seeking high quality public transport solutions. The technology applys physical guidance rails or optical sensors to keep the vehicle on course providing a smooth and stable ride comparable to steel wheel trams. Cities like Nancy and Caen in France have successfully deployed rubber tired tram systems to connect suburbs with city centers. The reduced construction time and minimal disruption to traffic during installation further enhance their appeal. As urban populations grow and the demand for efficient transit increases rubber tired trams offer a scalable and adaptable solution. Their ability to integrate seamlessly with existing bus networks also simplifies operational management. This versatility ensures robust growth in the coming years. The accelerated growth of the rubber tired tram segment is also fueled by their superior comfort and environmental performance compared to conventional bapplys. These vehicles typically feature wider aisles larger windows and smoother suspension systems providing a passenger experience akin to traditional trams. According to sources, rubber tired trams are perceived as more reliable and comfortable than standard bapplys leading to higher ridership rates. The electric propulsion systems applyd in most rubber tired trams produce zero direct emissions contributing to improved air quality in urban areas. This aligns with stringent European environmental regulations and sustainability goals. The quiet operation of electric motors also reduces noise pollution enhancing the quality of life for residents along the routes. Manufacturers are increasingly incorporating regenerative braking and energy efficient technologies to further reduce operational costs and environmental impact. The aesthetic appeal of rubber tired trams which often resemble modern light rail vehicles also enhances the image of public transport systems. Cities view these systems as a symbol of modernity and progress attracting investment and tourism. The combination of operational flexibility environmental benefits and passenger comfort ensures that rubber tired trams will continue to experience rapid growth in the European market.

By Fuel Insights

The electric trams segment held the majority share of the Europe tramway market in 2025. This supremacy of the segment is credited to well established overhead catenary infrastructure and the zero emission nature of electric propulsion. Most European cities with tram networks have invested heavily in electrical power supply systems over the past century creating it the default choice for new and replacement fleets. The efficiency of electric motors is significantly higher than internal combustion engines resulting in lower energy consumption per passenger kilometer. The reliability and low maintenance requirements of electric traction systems further contribute to their popularity. Operators benefit from predictable energy costs and reduced depfinishency on fossil fuels. The integration of renewable energy sources into the grid allows electric trams to operate with a minimal carbon footprint. This alignment with sustainability goals ensures continued support from policybuildrs and the public. The mature technology and extensive supplier base for electric components also ensure competitive pricing and availability. As cities strive to decarbonize their transport systems electric trams remain the cornerstone of sustainable urban mobility. The commanding position of the electric segment is further reinforced by strong regulatory support and funding initiatives for electrification. The European Union Green Deal and the Sustainable and Smart Mobility Strategy prioritize the expansion of electrified public transport to reduce greenhoapply gas emissions. These funds assist municipalities cover the high initial costs of infrastructure upgrades and rolling stock procurement. National governments also provide subsidies and tax incentives for electric public transport operations creating them financially viable for local authorities. The phased ban on diesel vehicles in many European cities further accelerates the transition to electric trams. Regulatory frameworks such as the Alternative Fuels Infrastructure Regulation mandate the development of charging infrastructure which indirectly supports electric tram networks. The consistency of policy support provides long term certainty for investors and operators. This favorable regulatory environment encourages the adoption of advanced electric technologies such as energy storage systems and smart grid integration. As a result electric trams continue to dominate the market driven by both environmental imperatives and economic incentives.

The battery powered tram segment is anticipated to witness the quickest CAGR of 9.2% over the forecast period owing to the ability of battery powered trams to operate without overhead wires which is crucial for preserving the aesthetic integrity of historic city centers. Many European cities have strict heritage conservation laws that prohibit the installation of unsightly catenary systems in protected areas. This technology enables the extension of tram networks into areas previously inaccessible due to visual constraints. Cities like Bordeaux and Angers have successfully implemented ground level power supply and battery hybrid systems to protect their architectural heritage. The flexibility of battery powered trams also allows for clearer route modifications and expansions without the required for extensive infrastructure work. This adaptability is particularly valuable in dynamic urban environments. The reduction in visual clutter enhances the urban landscape improving the quality of life for residents and tourists. As more cities prioritize heritage preservation alongside modernization the demand for battery powered trams will continue to rise. The accelerated growth of the battery powered segment is also fueled by significant advancements in battery technology and energy efficiency. Recent developments in lithium ion and solid state batteries have increased energy density and reduced weight enabling longer ranges and quicker charging times. Modern battery systems incorporate regenerative braking which captures energy during deceleration and stores it for later apply further extfinishing range. This efficiency reduces the frequency of charging stops and enhances operational reliability. Manufacturers are also integrating smart energy management systems that optimize power usage based on route topology and traffic conditions. The improved lifecycle and durability of modern batteries reduce maintenance costs and environmental impact. Recycling programs for finish of life batteries are becoming more widespread supporting circular economy goals. The ability to charge batteries at terminals utilizing renewable energy sources further enhances the sustainability profile of these vehicles. As technology continues to evolve battery powered trams are becoming a practical and attractive alternative to traditional overhead wire systems. This technological progress ensures sustained growth in the segment.

By Passenger Capacity

The between 60 and 150 passengers segment led the Europe tramway market and captured a 55.2% share in 2025 becaapply of the optimal balance these vehicles offer between passenger capacity and maneuverability in urban environments. Trams in this size range are large enough to handle moderate to high demand corridors but tiny enough to navigate narrow streets and tight turns common in European cities. These vehicles provide frequent service intervals reducing wait times and improving overall system attractiveness. The operational flexibility of mid size trams allows operators to adjust frequency rather than vehicle size to match demand fluctuations. This approach optimizes energy consumption and labor costs. Many cities prefer this segment for network extensions into residential areas where demand is steady but not peak intensive. The standardization of this capacity range by major manufacturers ensures a wide selection of models and competitive pricing. The proven performance and reliability of mid size trams build them a safe and effective choice for urban planners. This segment serves as the workhorse of many European tram networks ensuring consistent and efficient service. The leadership of the 60 to 150 passenger segment is further reinforced by its cost effectiveness and operational efficiency. Mid size trams require less infrastructure investment compared to larger high capacity vehicles as they exert lower loads on tracks and bridges. These vehicles can operate on existing infrastructure with minimal upgrades creating them an attractive option for budobtain constrained municipalities. The tinyer footprint of these trams also allows for tighter station spacing increasing accessibility for passengers. This denser network coverage enhances the utility of the tram system and encourages modal shift from private cars. The availability of skilled drivers and maintenance staff for this common vehicle type reduces training and labor costs. Operators can achieve higher asset utilization by deploying these trams on multiple routes throughout the day. The flexibility to scale operations by adding more units rather than larger vehicles provides better risk management against demand uncertainty. This economic and operational efficiency ensures that the 60 to 150 passenger segment remains the dominant choice for European tramway systems.

The more than 150 passengers segment is likely to experience the quickest CAGR of 7.8% between 2026 and 2034. This rapid growth of the segment is propelled by increasing urban density and the consequent demand for high capacity transit solutions. As cities expand and population concentrations rise the required to relocate large numbers of people efficiently becomes critical. Large capacity trams often featuring multiple articulated sections can carry over 200 passengers per trip significantly reducing the number of vehicles required on busy routes. This consolidation improves traffic flow and reduces congestion. Cities like Istanbul and Budapest are investing in high capacity trams to replace overcrowded bapplys and older rail systems. The ability to handle peak hour surges without compromising service quality builds these vehicles essential for major metropolitan areas. The economies of scale in operating larger vehicles also reduce per passenger costs. As urbanization intensifies the demand for high capacity tram solutions will continue to accelerate. This segment addresses the critical required for efficient mass transit in densely populated regions. The quick surge of the more than 150 passenger segment is also fueled by the integration of trams with major transport hubs and intermodal connectivity. Large capacity trams are ideally suited for connecting railway stations airports and bus terminals with city centers. These trams can handle the large influx of passengers arriving from regional and national rail services. The spacious interiors and multiple doors of high capacity trams enable quick boarding and alighting reducing dwell times at stations. This efficiency is crucial for maintaining schedule adherence in complex transport networks. Cities are designing dedicated tram lanes and priority signaling for these high capacity vehicles to ensure reliable service. The visibility and prominence of large trams also enhance the image of public transport as a modern and efficient option. Investment in high capacity tram lines is often part of broader urban regeneration projects aimed at revitalizing transport hubs. This strategic role in intermodal connectivity ensures sustained growth for the high capacity segment.

By Sales Channel Insights

The Original Equipment Manufacturer (OEM) segment dominated the Europe tramway market by accounting for a significant share in 2025. This dominance of the segment is driven by the direct procurement of new rolling stock and infrastructure for network expansions and fleet renewals. Municipalities and transport authorities typically engage directly with OEMs such as Alstom Siemens and Stadler for large scale projects. OEMs provide comprehensive solutions including design manufacturing installation and commissioning ensuring seamless integration with existing systems. The complexity of tramway projects requires close collaboration between acquireers and manufacturers to meet specific technical and operational requirements. Long term contracts with OEMs often include maintenance and support services creating stable revenue streams. The trust and reliability associated with established OEM brands further reinforce their market position. Public tfinishers and procurement processes favor experienced manufacturers with proven track records. This barrier to enattempt limits competition from tinyer players. As cities continue to expand and modernize their tram networks the demand for OEM services remains robust. The OEM channel is the primary driver of innovation and technological advancement in the market. The leading position of the OEM segment is also supported by its ability to drive technological innovation and provide customized solutions. OEMs invest heavily in research and development to create advanced tram models with features such as energy efficiency digital connectivity and enhanced accessibility. OEMs work closely with clients to tailor vehicle specifications ensuring optimal performance and applyr experience. This collaborative approach fosters long term partnerships and repeat business. The introduction of new technologies such as battery power and autonomous driving features is primarily led by OEMs. These innovations attract cities viewing to modernize their fleets and improve sustainability. The ability to offer integrated solutions including signaling and power supply systems adds value for acquireers. OEMs also provide training and technical support ensuring smooth operation of new systems. This comprehensive service offering strengthens their competitive advantage. As the market evolves towards smarter and greener solutions OEMs remain at the forefront of development. Their role as innovators and customizers ensures their continued dominance in the sales channel.

The aftermarket segment is on the rise and is expected to be the quickest growing segment in the market by witnessing a CAGR of 5.5% during the forecast period. This rapid growth of the segment is primarily driven by the aging tram fleets in many European cities which require regular maintenance refurbishment and component replacement. Transport authorities are increasingly investing in mid life upgrades to extfinish the lifespan of their vehicles rather than purchasing new ones. This trfinish is fueled by budobtain constraints and the desire to maximize asset value. The aftermarket includes services such as bogie overhauls interior refurbishments and software updates. Specialized service providers and OEM subsidiaries are expanding their aftermarket offerings to capture this growing demand. The availability of spare parts and skilled technicians is crucial for minimizing downtime and maintaining service quality. As fleets age the frequency and complexity of maintenance activities increase driving aftermarket revenue. This segment offers a stable and recurring revenue stream for suppliers. The focus on sustainability also encourages refurbishment over replacement reducing waste and environmental impact. The accelerated growth of the aftermarket segment is also fueled by the adoption of digital solutions and predictive maintenance technologies. Modern tram systems are equipped with sensors and data analytics tools that monitor component health and predict failures before they occur. Transport operators are investing in digital platforms to optimize maintenance schedules and reduce unplanned downtime. This shift from reactive to proactive maintenance creates new opportunities for aftermarket service providers specializing in data analysis and software solutions. The integration of Internet of Things devices enables real time monitoring and remote diagnostics enhancing operational efficiency. Aftermarket providers are developing specialized tools and services to support these digital initiatives. The demand for software updates and cybersecurity measures also contributes to aftermarket growth. As trams become more connected and automated the required for specialized technical support increases. This technological transformation is reshaping the aftermarket landscape creating new value propositions for service providers. The focus on efficiency and reliability ensures sustained growth in the aftermarket segment.

COUNTRY LEVEL ANALYSIS

Germany Tramway Market Analysis

Germany outperformed other countries in the Europe tramway market and occupied a 22.3% share in 2025. This position of the German market is driven by its extensive existing network and continuous modernization efforts. The counattempt is home to some of the oldest and most comprehensive tram systems in the world particularly in cities like Berlin Leipzig and Dresden. According to sources, Germany has invested heavily in upgrading its public transport infrastructure to meet sustainability goals. The presence of leading manufacturers such as Siemens Mobility and Stadler Rail further strengthens the domestic market. German cities are actively expanding their tram networks to reduce car depfinishency and improve urban mobility. The government provides substantial funding for local public transport projects through the Municipal Transport Financing Act. This financial support enables municipalities to procure new rolling stock and upgrade tracks. The strong engineering tradition and focus on innovation ensure that German tram systems are among the most advanced globally. The demand for energy efficient and digitally connected trams is high driving market growth. Germany’s commitment to environmental protection and efficient public transport ensures its leading role in the regional market.

France Tramway Market Analysis

France was the next prominent counattempt in the Europe tramway market and accounted for a 18.4% share in 2025. This expansion of the French market is supported by a resurgence in tramway construction since the 1980s. The counattempt has seen a dramatic expansion of tram networks in cities such as Lyon Bordeaux and Nantes. According to research, the government has prioritized soft mobility and public transport to reduce carbon emissions. The successful implementation of ground level power supply systems in Bordeaux has set a global precedent for aesthetic integration. French cities are continuing to extfinish their tram lines to serve growing suburban populations. The presence of Alstom a global leader in rail transport provides a strong industrial base for the market. The French model of tramway development emphasizes urban renewal and social inclusion linking disadvantaged areas with city centers. Public private partnerships are commonly applyd to finance and operate tram systems. The strong political will and public support for trams ensure sustained investment. France’s focus on innovation and design excellence maintains its prominent position in the European market.

Spain Tramway Market Analysis

Spain continues to be a notable position in the Europe tramway market due to recent investments in modern light rail systems. Cities like Barcelona Valencia and Seville have expanded their tram networks to address congestion and pollution. According to studies, the government has allocated significant funds for sustainable urban mobility plans. The introduction of modern low floor trams has improved accessibility and ridership. Spanish cities are focutilizing on integrating trams with other public transport modes to create seamless networks. The tourism sector also benefits from tram systems which provide efficient access to historic sites. The presence of local manufacturers and suppliers supports the domestic market. Spain’s favorable climate and urban layout are conducive to tram operations. The ongoing modernization of existing lines and planning of new routes ensure continued growth. Spain’s strategic focus on sustainable tourism and urban liveliness drives its market presence.

United Kingdom Tramway Market Analysis

The United Kingdom is relocating ahead steadquickly in the Europe tramway market despite having fewer systems than continental Europe. Cities like Manchester Edinburgh and Sheffield have established tram networks that are undergoing expansion and modernization. According to sources, the UK government is investing in regional transport infrastructure to boost economic growth. The Manchester Metrolink is one of the most successful tram systems in the UK serving as a model for other cities. There is growing interest in introducing trams to other urban areas such as Leeds and Cambridge. The focus on reducing carbon emissions and improving air quality is driving policy support for tram projects. The UK market is characterized by high standards for safety and accessibility. Private sector involvement in financing and operation is common. The potential for new projects and expansions ensures a steady market outview. The UK’s commitment to regional connectivity and sustainability supports its role in the market.

Italy Tramway Market Analysis

Italy is anticipated to expand significantly in the Europe tramway market from 2026 and 2034 owing to its historic tram systems and modernization initiatives. Cities like Milan Turin and Rome have extensive tram networks that are being upgraded with new vehicles. According to research, investments are being created to improve public transport efficiency and reduce congestion. The preservation of historic trams alongside modern fleets creates a unique market dynamic. Italian cities are exploring innovative solutions such as battery powered trams to protect heritage sites. The presence of local engineering firms and designers contributes to the market. Italy’s focus on cultural heritage and sustainable tourism influences tram development. The ongoing renewal of fleets and infrastructure ensures market activity. Italy’s blfinish of tradition and innovation defines its position in the European tramway landscape.

COMPETITIVE LANDSCAPE

The competition in the Europe tramway market is characterized by a few dominant global manufacturers and specialized regional players vying for major infrastructure contracts. Established giants like Alstom and Siemens leverage their extensive experience and broad product portfolios to secure large scale projects. They compete on technological superiority sustainability features and lifecycle cost efficiency. Newer entrants and niche manufacturers like Stadler challenge incumbents by offering highly customizable and flexible solutions tailored to specific city requireds. Price competition is intense due to budobtain constraints faced by municipal authorities prompting suppliers to optimize costs through standardized platforms. Innovation in digital services and autonomous driving capabilities serves as a key differentiator. Regulatory compliance with European safety and environmental standards acts as a barrier to enattempt ensuring high quality benchmarks. Collaborative bidding and consortia formation are common strategies to share risks and combine expertise. The market is also influenced by political factors and local content requirements which can favor domestic suppliers. Continuous investment in research and development is crucial for staying ahead in this technology driven sector. Customer relationships and after sales support play a vital role in retaining business and securing future contracts in this competitive landscape.

KEY MARKET PLAYERS

A Few of the market players that are dominating the Europe tramway market are

- Siemens (Germany)

- Alstom (France)

- CRRC (China)

- Hitachi, Ltd. (Japan)

- General Electric Company (U.S.)

- Bombardier Inc. (Canada)

- Kawasaki Heavy Industries, Ltd. (Japan)

- HYUNDAI ROTEM COMPANY (South Korea)

- Toshiba Corporation (Japan)

- CAF, Construcciones y Auxiliar de Ferrocarriles, S.A. (Spain)

- ABB (Switzerland)

- KINKISHARYO International, LLC (U.S.)

- ŠKODA TRANSPORTATION a.s. (Czech Republic)

- The Kinki Sharyo Co.,Ltd. (Japan)

- Vossloh (Germany)

- Stadler Rail AG (Switzerland)

- Durmazlar Makina A.S. (Turkey)

- Brookville Equipment Corporation (U.S.)

Top Players In The Market

- Alstom SA is a global leader in the Europe tramway market renowned for its innovative Citadis platform which serves as the backbone for many urban transit systems. The company contributes significantly to the global market by providing sustainable and smart mobility solutions that prioritize energy efficiency and passenger comfort. Recent actions include the launch of the Citadis X05 series featuring enhanced modularity and digital connectivity. Alstom strengthens its market position through strategic acquisitions such as Bombardier Transportation which expanded its product portfolio and geographic reach. The company focapplys on integrating hydrogen and battery technologies to offer zero emission tram solutions. These initiatives demonstrate Alstom’s commitment to leading the green transition in urban transport. By leveraging advanced digital tools and predictive maintenance services Alstom ensures high reliability and operational efficiency for its clients across European cities.

- Siemens Mobility GmbH is a key player in the Europe tramway market offering comprehensive solutions from rolling stock to infrastructure and digital services. The company contributes globally by setting standards for automation and electrification in public transport. Its Avenio and Combino tram families are widely recognized for their reliability and low floor accessibility. Recent actions include the expansion of its digital rail portfolio with offerings like Railigent X which applys artificial innotifyigence for predictive maintenance. Siemens strengthens its market position by partnering with cities to develop integrated mobility ecosystems that enhance applyr experience. The company invests heavily in research and development to create lightweight and energy efficient trams. These efforts align with European sustainability goals and regulatory requirements. Siemens also focapplys on lifecycle services to ensure long term customer satisfaction and operational continuity. Its strong engineering heritage and technological innovation secure its competitive edge in the dynamic European tramway sector.

- Stadler Rail AG is a prominent manufacturer in the Europe tramway market known for its customizable and high quality light rail vehicles. The company contributes to the global market by delivering tailored solutions that meet specific urban requireds and aesthetic requirements. Its Variobahn and Tango tram models are celebrated for their flexibility and modern design. Recent actions include the opening of new production facilities in Poland and Germany to increase manufacturing capacity and reduce delivery times. Stadler strengthens its market position by focutilizing on niche markets and specialized projects such as heritage compatible trams. The company emphasizes sustainable production practices and applys eco frifinishly materials in its vehicles. Stadler also invests in hybrid and battery powered technologies to support decarbonization efforts. Its customer centric approach and ability to deliver complex projects on time enhance its reputation. Stadler’s continuous innovation and regional presence ensure it remains a vital competitor in the European tramway landscape.

Top Strategies Used By The Key Market Participants

Key players in the Europe tramway market primarily focus on product innovation and sustainability to maintain their competitive edge. Companies invest heavily in developing energy efficient trams with battery and hydrogen capabilities to meet strict environmental regulations. Strategic partnerships with local governments and transport authorities enable customized solutions that address specific urban challenges. Manufacturers also expand their service portfolios to include digital maintenance and predictive analytics enhancing operational reliability. Mergers and acquisitions are common strategies to broaden product ranges and enter new geographic markets. Firms prioritize modular designs that allow for straightforward customization and scalability. Additionally companies engage in public private partnerships to secure funding for large infrastructure projects. These strategies assist participants differentiate their offerings and build long term relationships with clients while supporting the transition towards greener and smarter urban mobility solutions across the continent.

MARKET SEGMENTATION

This research report on the Europe tramway market is segmented and sub-segmented into the following categories.

By Type

- Articulated Tram

- Double-Decker Tram

- Rubber-Tired Tram,

- Restaurant Tram

By Fuel Type

- Electric

- Battery Powered

- Liquid Fuel

- Hybrid

- Others

By Passenger Capacity

- Below 60 Passengers

- Between 60 To 150 Passengers

- More than 150 Passengers

By Design

- Single Ended Trams

- Double Ended Trams

By Sales Channel

- Original Equipment Manufacturer

- Aftermarket

By Counattempt

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe