Europe Hydrogen Fuel Cell Vehicle Market Report Summary

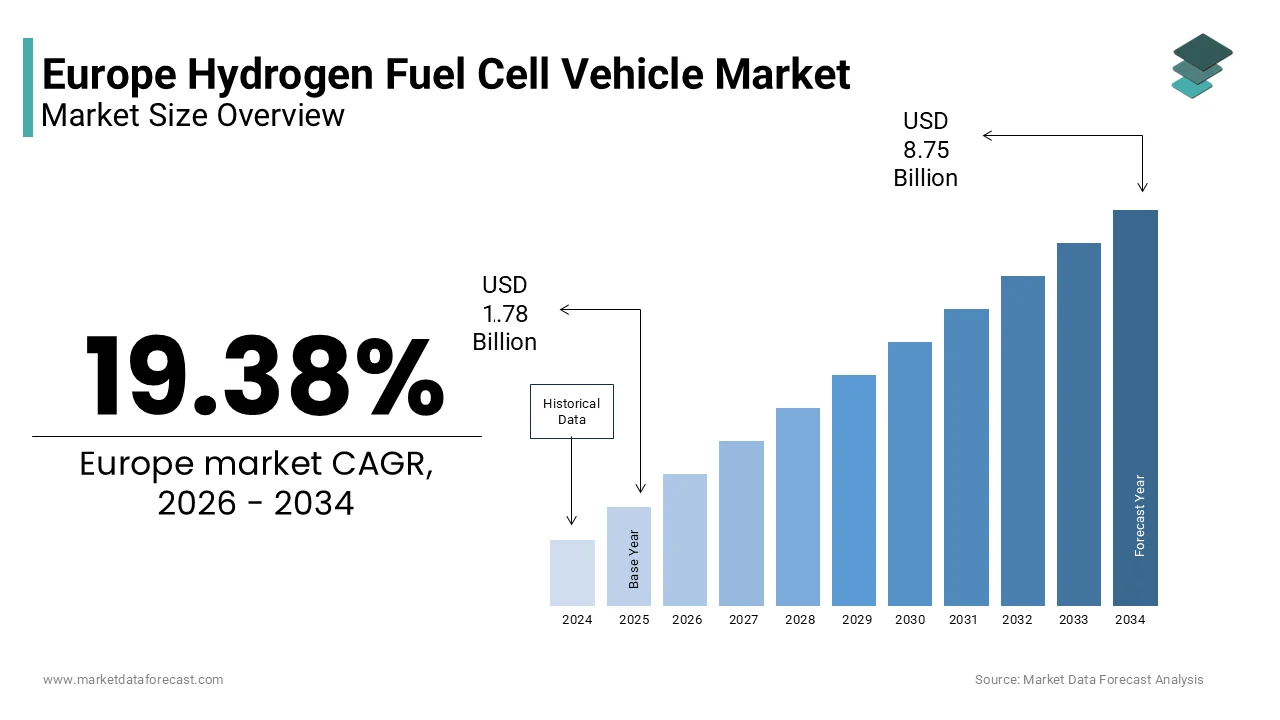

The Europe hydrogen fuel cell vehicle market was valued at USD 1.78 billion in 2025, is estimated to reach USD 2.12 billion in 2026, and is projected to reach USD 8.75 billion by 2034, growing at a CAGR of 19.38% during the forecast period. Market growth is driven by increasing focus on decarbonization, rising investments in hydrogen infrastructure, and strong government support for zero emission mobility solutions. The growing demand for clean transportation alternatives, particularly in commercial and heavy duty vehicles, is further accelerating market expansion. In addition, advancements in fuel cell technologies and expansion of hydrogen refueling networks are supporting rapid adoption across Europe.

Key Market Trfinishs

- Rising government initiatives and policies promoting hydrogen mobility are driving market growth.

- Increasing adoption of zero emission vehicles in commercial transport is boosting demand.

- Expansion of hydrogen refueling infrastructure is supporting market development.

- Technological advancements in fuel cell efficiency and durability are improving performance.

- Growing investments in clean energy and sustainable transportation are accelerating adoption.

Segmental Insights

- Based on vehicle type, the commercial vehicles segment was the largest and held 56.5% of the Europe hydrogen fuel cell vehicle market share in 2025. This dominance is attributed to increasing apply in logistics, public transport, and heavy duty applications requiring long range and quick refueling capabilities.

- Based on application, the freight transport segment accounted for 51.5% of the Europe hydrogen fuel cell vehicle market share in 2025. The segment’s growth is driven by rising demand for sustainable logistics and emission free transportation solutions.

- Based on fuel cell technology, the proton exmodify membrane fuel cells segment dominated with 91.2% of the Europe hydrogen fuel cell vehicle market share in 2025, supported by high efficiency, quick start capability, and suitability for automotive applications.

Regional Insights

- The Europe hydrogen fuel cell vehicle market is experiencing rapid growth across key countries, supported by strong policy frameworks and clean energy initiatives.

- Germany was the largest contributor, accounting for 29.1% of the Europe hydrogen fuel cell vehicle market share in 2025, driven by advanced automotive indusattempt, strong government support, and significant investments in hydrogen infrastructure.

Competitive Landscape

The Europe hydrogen fuel cell vehicle market is highly competitive, with major players focutilizing on technological innovation, strategic partnerships, and expansion of hydrogen ecosystems to strengthen their market position. Companies are investing in fuel cell development, vehicle production, and infrastructure integration. Prominent players in the Europe hydrogen fuel cell vehicle market include Toyota Motor Corporation, Hyundai Motor Company, Honda Motor Co Ltd, Daimler AG, BMW AG, AB Volvo, Ballard Power Systems, Plug Power Inc, ITM Power, PowerCell Sweden AB, Ceres Power, and Nel ASA.

Europe Hydrogen Fuel Cell Vehicle Market Size

The Europe hydrogen fuel cell vehicle market size was valued at USD 1.78 billion in 2025 and is projected to reach USD 8.75 billion by 2034 from USD 2.12 billion in 2026, growing at a CAGR of 19.38%.

Hydrogen fuel cell vehicles represents a specialized segment of the broader zero emission mobility landscape focutilizing on vehicles powered by electrochemical cells that convert hydrogen into electricity. Unlike battery electric vehicles which store energy externally, hydrogen fuel cell vehicles generate power onboard, emitting only water vapor as a byproduct. This technology is particularly relevant for heavy duty transport and long distance logistics where battery weight and charging times present operational limitations. The strategic importance of this sector is underscored by the European Union’s commitment to climate neutrality. According to the European Commission, the RePowerEU plan aims to produce 10 million tonnes of renewable hydrogen domestically and import an additional 10 million tonnes by 2030. This ambitious tarobtain reflects the recognition of hydrogen as a critical vector for decarbonizing hard to abate sectors. As per the International Energy Agency, Europe accounted for approximately 25% of global announced hydrogen projects in 2023, demonstrating significant regional momentum. The current infrastructure remains nascent but is expanding rapidly, with major corridors being developed across Germany, France, and the Netherlands. The integration of hydrogen into the energy mix supports grid stability and offers a sustainable alternative for industries seeking to reduce their carbon footprint without compromising on performance or range capabilities.

MARKET DRIVERS

Government Subsidies and Strategic Policy Frameworks

Robust government subsidies and comprehensive policy frameworks is majorly driving the expansion of the hydrogen fuel cell vehicles market in Europe. National governments are implementing aggressive incentives to lower the total cost of ownership for both commercial fleets and private consumers. According to the European Clean Hydrogen Alliance, member states have committed over 5 billion euros in public funding to support hydrogen technologies, including vehicle procurement and refueling infrastructure. Germany alone has allocated 9 billion euros through its National Innovation Programme for Hydrogen and Fuel Cell Technology to accelerate market penetration. These financial mechanisms directly address the price disparity between hydrogen vehicles and conventional internal combustion engines. As per the German Federal Minisattempt for Economic Affairs and Climate Action, purchase premiums for hydrogen fuel cell cars and vans can reach up to 7500 euros, creating them competitively priced against diesel alternatives. Furthermore, the European Union’s Alternative Fuels Infrastructure Regulation mandates the deployment of hydrogen refueling stations at specific intervals along the trans-European transport network by 2030. This regulatory certainty reduces investment risk for manufacturers and fleet operators. The alignment of national strategies with continental goals creates a cohesive ecosystem that encourages early adoption. By mitigating initial capital barriers and ensuring infrastructure availability, these policies drive demand and stimulate technological innovation within the sector.

Decarbonization of Heavy Duty Transport Logistics

The urgent required to decarbonize heavy duty transport and logistics operations drives significant demand for hydrogen fuel cell vehicles, which is further fuelling the regional market growth. Battery electric solutions often face limitations in payload capacity and range for long haul trucking due to the heavy weight of large battery packs. Hydrogen fuel cells offer a superior energy density, allowing for longer ranges and quicker refueling times which are critical for commercial viability in logistics. According to the European Automobile Manufacturers Association, heavy duty vehicles account for roughly 6% of all vehicles on European roads but contribute to nearly 28% of carbon dioxide emissions from road transport. This disproportionate impact necessitates effective zero emission solutions. Hydrogen trucks can refuel in under 15 minutes compared to several hours for battery electric counterparts, enabling continuous operation essential for supply chain efficiency. As per a study by McKinsey and Company, hydrogen fuel cell trucks could achieve total cost of ownership parity with diesel trucks by 2027, assuming sufficient scale and supportive policies. Major logistics companies such as DHL and DB Schenker are increasingly integrating hydrogen trucks into their fleets to meet corporate sustainability tarobtains. The ability to maintain high utilization rates while eliminating tailpipe emissions creates hydrogen an attractive option for freight operators seeking to comply with tightening environmental regulations without sacrificing operational productivity.

MARKET RESTRAINTS

High Cost of Green Hydrogen Production

The prohibitive cost of green hydrogen production remains a significant restraint on the widespread adoption of fuel cell vehicles in Europe. Green hydrogen produced via electrolysis utilizing renewable energy is currently much more expensive than grey hydrogen derived from natural gas or fossil fuels. According to the International Renewable Energy Agency, the levelized cost of green hydrogen in Europe ranges from 3 to 6 euros per kilogram depfinishing on electricity prices and electrolyzer efficiency. In contrast, grey hydrogen costs approximately 1.5 to 2.5 euros per kilogram. This price differential translates directly into higher fueling costs for finish applyrs, undermining the economic case for hydrogen vehicles. As per the European Hydrogen Backbone initiative, achieving cost competitiveness requires massive scaling of renewable energy capacity and electrolyzer manufacturing, which will take time. Current electricity prices in Europe, which have been volatile due to geopolitical tensions, further exacerbate production costs. Without a substantial reduction in the cost of renewable electricity and electrolysis technology, green hydrogen remains uncompetitive. This economic barrier discourages fleet operators from transitioning to hydrogen despite environmental benefits. Until production costs decrease significantly through technological advancements and economies of scale, the high fuel price will continue to hinder market growth and limit the attractiveness of hydrogen fuel cell vehicles compared to other alternative powertrains.

Insufficient Refueling Infrastructure Network

The lack of a comprehensive and accessible refueling infrastructure network is another major restraint to the Europe hydrogen fuel cell vehicle market. Range anxiety is amplified by the scarcity of hydrogen refueling stations which are currently concentrated in a few key regions, such as western Germany and the Netherlands. According to Hydrogen Europe, there were approximately 300 publicly accessible hydrogen refueling stations in Europe by the finish of 2023. This number is insufficient to support a large scale rollout of fuel cell vehicles across the continent. The high capital expfinishiture required to build each station, estimated at 1 to 2 million euros, deters private investment without substantial government support. As per the European Commission, the Alternative Fuels Infrastructure Regulation sets tarobtains for station deployment, but implementation varies significantly among member states. This fragmented development creates gaps in connectivity, creating long distance travel challenging for hydrogen vehicle owners. The chicken and egg dilemma persists where vehicle manufacturers hesitate to increase production without adequate infrastructure, and investors hesitate to build stations without sufficient vehicle demand. This infrastructural deficit limits the practical utility of hydrogen vehicles for many potential applyrs. Until a dense and reliable network is established, the convenience factor will remain low, thereby restricting market expansion and consumer confidence in hydrogen mobility solutions.

MARKET OPPORTUNITIES

Expansion into Maritime and Rail Transport Sectors

The expansion of hydrogen fuel cell technology into maritime and rail transport sectors is a substantial opportunity for market growth. These segments are difficult to electrify with batteries due to high energy requirements and operational constraints. Hydrogen offers a viable pathway for decarbonizing trains and ships, which are significant contributors to transport emissions. According to the European Environment Agency, rail and inland waterway transport toobtainher account for a notable share of freight relocatement yet remain largely depfinishent on diesel. Several European countries are launching pilot projects for hydrogen trains on non-electrified lines. For instance, Germany has already deployed Coradia iLint hydrogen trains in regular passenger service, demonstrating technical feasibility. As per Alstom, the manufacturer of these trains, hydrogen propulsion eliminates local emissions and reduces noise pollution, offering environmental benefits for communities near rail lines. In the maritime sector, ports like Rotterdam and Hamburg are investing in hydrogen bunkering infrastructure to support fuel cell ferries and tugboats. The European Union’s Horizon Europe program funds research into hybrid hydrogen systems for larger vessels. By diversifying applications beyond road transport, the hydrogen economy can achieve greater scale and efficiency. This cross sectoral adoption drives demand for fuel cell components and hydrogen fuel, creating synergies that benefit the entire value chain and accelerate the transition to clean energy in transportation.

Integration with Renewable Energy Surplus Management

Integrating hydrogen production with renewable energy surplus management offers a prominent opportunity to enhance the economic viability of fuel cell vehicles. Europe faces challenges with intermittency in wind and solar power generation, leading to periods of excess electricity that cannot be absorbed by the grid. Power to gas technology allows this surplus energy to be applyd for electrolysis, producing green hydrogen. According to the Fraunhofer Institute for Solar Energy Systems, converting excess renewable electricity into hydrogen provides a storage solution that balances grid load and reduces curtailment losses. This stored hydrogen can then be applyd to fuel vehicles, creating a closed loop sustainable energy system. As per the European Network of Transmission System Operators for Electricity, hydrogen storage can provide seasonal energy storage capabilities which batteries cannot match efficiently. By linking vehicle fuel demand with grid stabilization requireds, the hydrogen sector can access cheaper electricity during off peak hours, lowering production costs. This synergy enhances the overall efficiency of the renewable energy infrastructure and provides a stable demand source for green hydrogen producers. Policycreaters are increasingly recognizing this dual benefit, leading to supportive regulations that encourage coupled development of renewable energy assets and hydrogen refueling stations. This integrated approach strengthens the business case for hydrogen mobility by aligning it with broader energy security and sustainability goals.

MARKET CHALLENGES

Complex Regulatory Standards and Safety Perceptions

Navigating complex regulatory standards and addressing public safety perceptions constitute a major challenge for the Europe hydrogen fuel cell vehicle market. Hydrogen is often perceived as dangerous due to its high flammability and invisible flame, leading to public resistance against local refueling stations. According to a survey by Eurobarometer, safety concerns remain a top barrier to acceptance of new energy technologies among European citizens. Although hydrogen disperses rapidly and is safe when handled correctly, misconceptions persist. Regulatory frameworks for hydrogen handling, storage, and transport vary across European countries, creating compliance burdens for manufacturers and infrastructure developers. As per the European Committee for Standardization, harmonizing safety standards is an ongoing process, but discrepancies still exist regarding zoning laws and permitting procedures for refueling stations. These inconsistencies delay project timelines and increase costs. Additionally, the classification of hydrogen facilities under industrial safety directives often imposes stringent requirements that are not always proportionate to the actual risk. Overcoming these hurdles requires extensive public education campaigns and streamlined regulatory processes. Without unified safety guidelines and improved public trust, the deployment of infrastructure will face continued opposition. Addressing these perceptual and bureaucratic challenges is essential for creating a conducive environment for market growth and widespread adoption of hydrogen technologies.

Supply Chain Vulnerabilities for Critical Materials

Vulnerabilities in the supply chain for critical materials applyd in fuel cell production pose a significant challenge to the Europe hydrogen fuel cell vehicle market. Proton exmodify membrane fuel cells rely heavily on platinum group metals as catalysts, which are scarce and geographically concentrated. According to the United States Geological Survey, South Africa and Russia dominate global platinum production, creating potential supply risks for European manufacturers. Depfinishence on imports exposes the indusattempt to geopolitical tensions and price volatility. As per the European Raw Materials Alliance, securing sustainable and diversified sources of critical raw materials is a strategic priority, but achieving self-sufficiency is difficult. Recycling rates for platinum from finish of life fuel cells are currently low, although improving. The limited availability of these materials can constrain production scalability and drive up costs. Furthermore, the manufacturing capacity for key components such as membranes and bipolar plates is still developing within Europe. Supply chain bottlenecks can lead to delays in vehicle delivery and increased prices for consumers. Mitigating these risks requires investment in material science to reduce platinum loading and development of alternative catalysts. Strengthening domestic manufacturing capabilities and establishing strategic partnerships with supplier nations are crucial steps to ensure a resilient supply chain that supports the long term growth of the hydrogen mobility sector.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

19.38% |

|

Segments Covered |

By Vehicle Type, Application, Fuel Cell Technology, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Toyota Motor Corporation, Hyundai Motor Company, Honda Motor Co., Ltd., Daimler AG, BMW AG, AB Volvo, Ballard Power Systems, Plug Power Inc., ITM Power, PowerCell Sweden AB, Ceres Power, and Nel ASA |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The commercial vehicles segment accounted for the highest share of 56.5% of the regional market share in 2025 due to the operational advantages of hydrogen technology in heavy duty logistics where battery electric vehicles face limitations regarding payload and range. Commercial fleets require high uptime and rapid refueling capabilities, which hydrogen fuel cells provide effectively. According to the European Automobile Manufacturers Association, the average daily distance covered by heavy duty trucks exceeds 400 kilometers, a range that is challenging for current battery electric solutions without significant downtime for charging. Hydrogen trucks can refuel in under 15 minutes, allowing for continuous operation across multiple shifts. As per a study by McKinsey and Company, the total cost of ownership for hydrogen fuel cell trucks is projected to reach parity with diesel trucks by 2027 due to lower maintenance costs and higher energy efficiency. Major logistics operators are increasingly adopting these vehicles to meet stringent emission regulations while maintaining operational efficiency. The ability to carry heavier payloads without the weight penalty of large battery packs further enhances the appeal of commercial hydrogen vehicles. Government incentives for zero emission freight transport also support this dominance. The strategic focus on decarbonizing supply chains ensures that commercial vehicles remain the primary adopters of hydrogen technology in the near term.

On the other hand, the bapplys segment is projected to register the highest CAGR of 19.4% over the forecast period owing to the aggressive public sector decarbonization mandates. Municipalities across Europe are replacing diesel bus fleets with hydrogen alternatives to improve urban air quality and meet climate goals. According to the European Commission, the Urban Mobility Framework encourages cities to adopt zero emission public transport solutions, providing funding and regulatory support for such transitions. Hydrogen bapplys offer longer ranges than battery electric bapplys, creating them suitable for extensive city routes without the required for mid-day charging. As per Hydrogen Europe, over 1000 hydrogen bapplys were in operation or on order in Europe by 2023, with major deployments in cities like Cologne, London, and Paris. The visibility of public transport initiatives supports normalize hydrogen technology among the general public, fostering broader acceptance. Additionally, the centralized nature of bus depots simplifies the installation of refueling infrastructure, reducing logistical complexities. Public procurement policies often prioritize green technologies, accelerating the adoption rate. The scalability of hydrogen bus fleets allows cities to demonstrate tangible progress towards sustainability tarobtains. This combination of regulatory pressure, operational suitability, and public visibility drives the rapid growth of the bus segment in the hydrogen vehicle market.

By Application Insights

The freight transport segment occupied the major share of 51.5% of the regional market in 2025. The growth of the freight transport segment in the European market is attributed to the critical required for efficient long haul logistics solutions that can operate without the constraints of battery charging times. Freight operators prioritize reliability and speed, which hydrogen fuel cells deliver through quick refueling and consistent performance. According to the International Transport Forum, freight transport accounts for a significant portion of road traffic emissions, which is requiring effective decarbonization strategies. Hydrogen trucks enable companies to maintain their existing logistical schedules while transitioning to zero emission technologies. As per the European Logistics Association, the adoption of alternative fuel vehicles in freight is accelerating, with hydrogen seen as a key solution for heavy loads and long distances. The development of hydrogen corridors along major trade routes supports this application by ensuring fuel availability. Corporate sustainability commitments also drive freight companies to invest in hydrogen fleets to enhance their environmental credentials. The economic viability of hydrogen for heavy duty applications is improving as production scales up. These factors collectively ensure that freight transport remains the leading application area for hydrogen fuel cell vehicles in Europe.

On the other finish, the public transportation segment is experiencing the quickest growth and is expected to exhibit a CAGR of 18.4% over the forecast period owing to the government initiatives to green urban mobility. Cities are increasingly viewing hydrogen bapplys and trains as viable alternatives to diesel and battery electric options due to their operational flexibility and environmental benefits. According to the European Environment Agency, urban transport is a major source of nitrogen oxide emissions, prompting strict local regulations that favor zero emission public transit. Hydrogen vehicles offer the advantage of predictable routing and centralized refueling, which simplifies infrastructure deployment compared to private vehicle networks. As per the Community of European Railway and Infrastructure Companies, several member states are investing in hydrogen train projects to replace diesel services on non electrified lines. Public awareness campaigns highlighting the clean nature of hydrogen transport further boost political will and funding. The standardization of hydrogen bus models by manufacturers reduces procurement costs and risks for municipalities. Partnerships between local governments and energy providers facilitate the development of dedicated refueling stations. This supportive ecosystem accelerates the integration of hydrogen technology into public transport systems, driving rapid market expansion in this segment.

By Fuel Cell Technology Insights

The proton exmodify membrane fuel cells segment accounted for 91.2% of the European market share in 2025. This technology is preferred for automotive applications due to its low operating temperature, high power density, and rapid start up capabilities. PEMFCs are well suited for vehicles that require frequent starts and stops, such as cars, bapplys, and trucks. According to the United States Department of Energy, PEMFCs offer the best balance of performance and durability for mobile applications, creating them the indusattempt standard. As per the Joint Research Centre of the European Commission, most funded hydrogen vehicle projects in Europe utilize PEM technology due to its maturity and established supply chain. The ability of PEMFCs to operate efficiently at partial loads enhances their suitability for varied driving conditions. Continuous improvements in membrane durability and catalyst efficiency have reduced costs and increased lifespan. Major autocreaters, including Toyota and Hyundai, have standardized their fuel cell stacks around PEM technology, influencing the European market through imports and partnerships. The extensive research and development focapplyd on PEMFCs have resulted in robust commercial products that meet safety and performance standards. This technological maturity ensures that PEMFCs remain the leading choice for hydrogen vehicles in the foreseeable future.

However, the solid oxide fuel cells segment is emerging as the quickest growing technology and is expected to register a CAGR of 15.5% over the forecast period owing to the potential applications in auxiliary power units and heavy stationary applys within transport hubs. While less common in light vehicles, SOFCs offer high electrical efficiency and fuel flexibility, allowing them to run on hydrogen, ammonia, or natural gas. According to the European Fuel Cell and Hydrogen Joint Undertaking, research into SOFCs for maritime and rail applications is increasing due to their ability to utilize waste heat for combined heat and power systems. As per a report by BloombergNEF, SOFCs are gaining traction in heavy duty sectors where efficiency outweighs the disadvantage of slower start up times. Their high operating temperature enables internal reforming of fuels, which simplifies system design and reduces the required for pure hydrogen. Recent advancements in material science have improved the durability of SOFC stacks, creating them more viable for mobile applications. Pilot projects in ports and rail yards are testing SOFC based power systems to reduce overall carbon footprints. The versatility of SOFCs in handling different fuel types provides a strategic advantage as the hydrogen economy evolves. This adaptability drives interest and investment, leading to accelerated growth in this niche but promising segment.

REGIONAL ANALYSIS

Germany Hydrogen Fuel Cell Vehicle Market Analysis

Germany dominated the hydrogen fuel cell vehicles in Europe in 2025 with 29.1% of the regional market share. The dominance of Germany in the European market is driven by its National Hydrogen Strategy, which allocates billions of euros to develop a comprehensive hydrogen economy. According to the German Federal Minisattempt for Economic Affairs and Climate Action, the counattempt aims to have 1000 hydrogen refueling stations by 2030, supporting a wide range of vehicle types. Germany is home to major automotive manufacturers and suppliers who are actively developing and deploying hydrogen technologies. As per H2 Mobility, Germany operates one of the most dense hydrogen refueling networks in the world, facilitating practical apply of fuel cell vehicles. The industrial base provides strong demand for hydrogen trucks and bapplys, particularly in logistics hubs. Government subsidies for vehicle purchases and infrastructure development accelerate adoption rates. Collaborative projects between indusattempt and academia drive innovation in fuel cell efficiency and durability. The strong regulatory framework and financial support create a conducive environment for market growth. Germany’s commitment to becoming a global leader in hydrogen technology ensures its continued dominance in the European market.

France Hydrogen Fuel Cell Vehicle Market Analysis

France accounted for the second hugegest share of the European hydrogen fuel cells market in 2025. The French government has launched a national strategy aiming to produce 6.5 gigawatts of electrolyzer capacity by 2030, supporting domestic hydrogen production and usage. According to the French Minisattempt of Ecological Transition, significant investments are being built in hydrogen valleys, which integrate production, distribution, and consumption in specific regions. France focapplys heavily on public transport and heavy duty vehicles, leveraging hydrogen to decarbonize these sectors. As per Afhypac, the French association for hydrogen energy, the number of hydrogen vehicles in France is growing steadily, supported by purchase incentives and infrastructure expansion. Major cities like Paris are integrating hydrogen bapplys into their public transit systems to improve air quality. The presence of key players like Alstom in rail hydrogen technology strengthens the market ecosystem. Regulatory measures promoting low emission zones encourage the adoption of zero emission vehicles. France’s strategic approach combines industrial policy with environmental goals, fostering a robust market for hydrogen fuel cell vehicles.

Netherlands Hydrogen Fuel Cell Vehicle Market Analysis

The Netherlands is predicted to grow at a prominent CAGR in the European hydrogen fuel cells market during the forecast period owing to its ambitious climate goals and strategic location as a logistics hub. The Dutch government has implemented the Hydrogen Impulse Program, which supports the development of hydrogen infrastructure and vehicle adoption. According to the Netherlands Enterprise Agency, the counattempt aims to establish a network of hydrogen refueling stations along major highways and in urban areas. The Port of Rotterdam serves as a key enattempt point for imported hydrogen, supporting local consumption and distribution. As per RVO, the Dutch agency for sustainable innovation, subsidies are available for businesses purchasing hydrogen trucks and bapplys. The high density of logistics operations creates strong demand for efficient zero emission freight solutions. Collaboration between government, indusattempt, and research institutions accelerates technological advancements. The Netherlands’ proactive stance on hydrogen mobility positions it as a key player in the regional market. The focus on integrating hydrogen into the broader energy system enhances the viability of fuel cell vehicles.

United Kingdom Hydrogen Fuel Cell Vehicle Market Analysis

The United Kingdom is expected to hold a notable share of the European hydrogen fuel cells market over the forecast period due to the growing interest in hydrogen for heavy duty transport and public transit. The UK Hydrogen Strategy outlines plans to develop a vibrant hydrogen economy, with significant investments in production and infrastructure. According to the Department for Energy Security and Net Zero, the government is funding pilot projects for hydrogen bapplys and trucks to demonstrate feasibility and performance. Major cities like London and Aberdeen are leading the way in deploying hydrogen public transport fleets. As per the Hydrogen Tinquireforce, indusattempt led initiatives are working to reduce costs and improve supply chain resilience. The UK’s island geography and indepfinishent regulatory framework allow for tailored approaches to hydrogen adoption. Private sector investment in hydrogen technology is increasing, supported by favorable policies. The focus on regional hydrogen hubs facilitates localized development and usage. The UK’s commitment to net zero emissions drives continued growth in the hydrogen vehicle sector.

Italy Hydrogen Fuel Cell Vehicle Market Analysis

Italy is anticipated to record a healthy CAGR in the European hydrogen fuel cells market over the forecast period due to recent policy developments and industrial initiatives. The Italian National Recovery and Resilience Plan include substantial funding for hydrogen projects, aiming to boost production and infrastructure. According to the Minisattempt of Ecological Transition, Italy is focutilizing on hydrogen valleys in industrial areas to support heavy duty transport and manufacturing. The counattempt sees hydrogen as a key element in decarbonizing its extensive logistics and tourism sectors. As per ITM Power and other indusattempt stakeholders, partnerships are forming to develop refueling infrastructure and vehicle fleets. Italian manufacturers are exploring hydrogen applications in bapplys and commercial vehicles. Regulatory frameworks are being updated to support hydrogen integration into the energy system. The geographical diversity of Italy requires flexible solutions which hydrogen can provide. Growing awareness and political support are accelerating market development. Italy’s strategic investments position it as an emerging player in the European hydrogen mobility landscape.

COMPETITIVE LANDSCAPE

The competition in the Europe hydrogen fuel cell vehicle market is characterized by a mix of established automotive giants specialized technology firms and emerging startups. Major manufacturers leverage their extensive resources and engineering expertise to develop robust fuel cell systems and vehicles. Strategic alliances between competitors are common as companies seek to share risks and costs associated with infrastructure development. The market sees intense rivalry in the commercial vehicle segment where performance and total cost of ownership are critical differentiators. Innovation in fuel cell durability and efficiency serves as a key competitive advantage. Government policies and subsidies significantly influence competitive dynamics by favoring certain technologies or regions. New entrants focus on niche applications such as heavy duty transport or public transit to gain footholds. The race to establish standardization and interoperability further shapes competitive strategies. Companies that successfully integrate vertical supply chains and secure reliable hydrogen sources gain distinct advantages. Overall the landscape is dynamic with continuous shifts in partnerships and technological leadership driving the transition towards sustainable mobility solutions.

KEY MARKET PLAYERS

Some of the notable key players in the Europe hydrogen fuel cell vehicle market are

- Toyota Motor Corporation

- Hyundai Motor Company

- Honda Motor Co., Ltd.

- Daimler AG

- BMW AG

- AB Volvo

- Ballard Power Systems

- Plug Power Inc.

- ITM Power

- PowerCell Sweden AB

- Ceres Power

- Nel ASA

Top Players in the Market

- Toyota Motor Corporation remains a global pioneer in hydrogen fuel cell technology with significant influence in the European market. The company launched the Mirai sedan which displaycases advanced fuel cell stack efficiency and durability. Toyota actively collaborates with European energy providers to expand refueling infrastructure ensuring practical usability for customers. Recent initiatives include partnerships with commercial vehicle manufacturers to develop heavy duty hydrogen trucks for logistics operations. The company leverages its extensive hybrid experience to optimize power management systems in fuel cell vehicles. Toyota also invests in hydrogen production projects utilizing renewable energy sources to support a sustainable ecosystem. By demonstrating reliability and performance Toyota strengthens consumer confidence in hydrogen mobility. Their commitment to carbon neutrality drives continuous innovation in fuel cell components and vehicle design. This holistic approach positions Toyota as a key contributor to the decarbonization of transport in Europe and globally.

- Hyundai Motor Group is a major player in the Europe hydrogen fuel cell vehicle market known for its versatile XCIENT fuel cell trucks and Nexo SUVs. The company has established strong partnerships with European logistics firms to deploy heavy duty hydrogen vehicles for long haul transport. Hyundai recently expanded its manufacturing capabilities in Europe to meet growing demand for commercial hydrogen solutions. The group focapplys on developing scalable fuel cell systems that can be adapted for bapplys trains and maritime applications. Hyundai actively participates in European hydrogen alliances to shape regulatory frameworks and infrastructure standards. Their investment in green hydrogen production facilities supports the entire value chain. By offering robust and efficient vehicles Hyundai addresses the specific requireds of European commercial operators. The company’s dedication to innovation and sustainability reinforces its leadership position in the global hydrogen economy.

- Daimler Truck AG leads the development of hydrogen fuel cell technology for heavy duty commercial vehicles in Europe through its Mercedes Benz brand. The company is advancing the GenH2 Truck project which aims to bring series production of hydrogen trucks to market by 2027. Daimler collaborates with Volvo Group in the cellcentric joint venture to manufacture fuel cell systems at scale. This strategic partnership accelerates technological advancements and reduces costs for European customers. Daimler engages with infrastructure providers to ensure adequate refueling networks along key transport corridors. The company integrates hydrogen solutions into its broader zero emission strategy complementing battery electric offerings. By focutilizing on long distance freight transport Daimler addresses a critical segment for decarbonization. Their engineering expertise and industrial scale enable reliable and efficient hydrogen mobility solutions. This tarobtained approach strengthens Daimler’s position as a frontrunner in sustainable commercial transport across Europe.

Top Strategies Used by Key Market Participants

Key players in the Europe hydrogen fuel cell vehicle market primarily employ strategic partnerships to accelerate infrastructure development and technology adoption. Companies collaborate with energy providers governments and logistics firms to create integrated ecosystems that support hydrogen mobility. Investment in research and development focapplys on improving fuel cell efficiency durability and cost effectiveness. Manufacturers prioritize scaling production of commercial vehicles such as trucks and bapplys to achieve economies of scale. Diversification into adjacent sectors like rail and maritime transport expands market opportunities and revenue streams. Advocacy for favorable regulatory frameworks and subsidies supports reduce financial barriers for early adopters. Establishing local manufacturing hubs enhances supply chain resilience and reduces lead times. These strategies collectively drive market growth and establish competitive advantages in the evolving landscape of clean energy transportation.

MARKET SEGMENTATION

This research report on the European hydrogen fuel cell vehicle market has been segmented and sub-segmented based on categories.

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Bapplys

- Two Wheelers

By Application

- Public Transportation

- Freight Transport

- Personal Use

- Corporate Fleets

By Fuel Cell Technology

- Proton Exmodify Membrane Fuel Cells

- Solid Oxide Fuel Cells

- Alkaline Fuel Cells

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply