Europe Firewood Market Report Summary

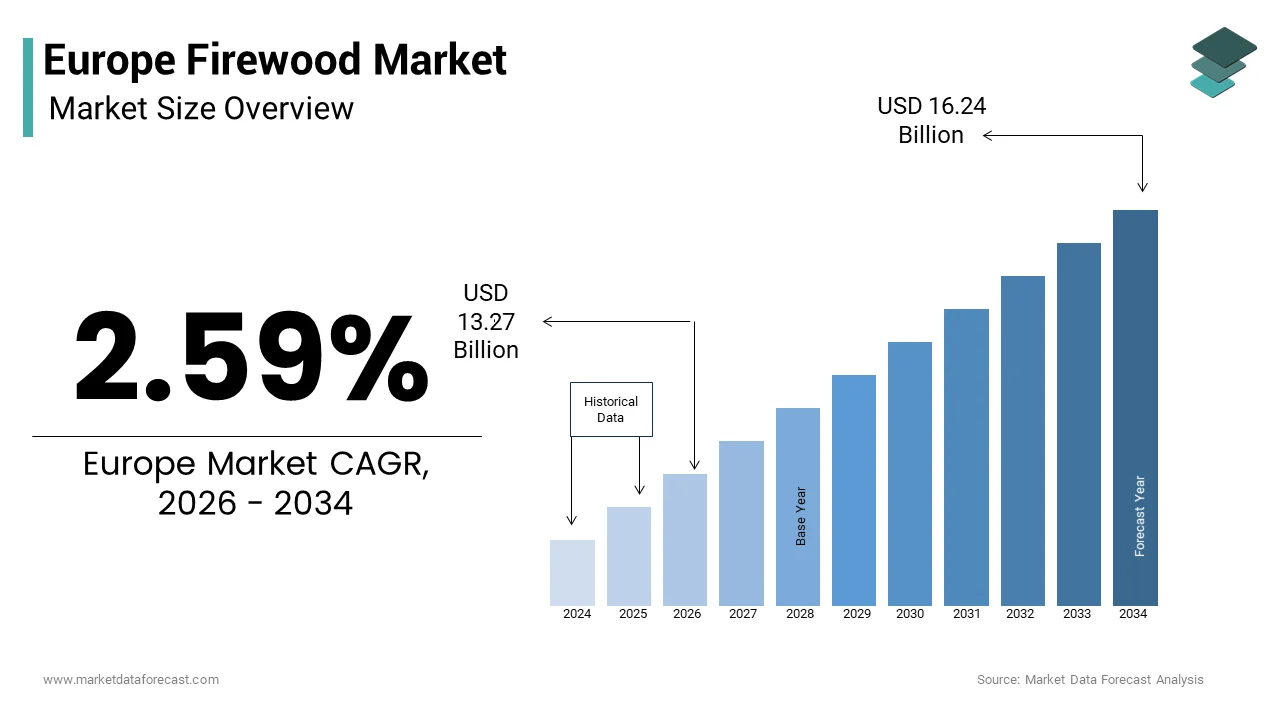

The Europe firewood market was valued at USD 12.93 billion in 2025, is estimated to reach USD 13.27 billion in 2026, and is projected to reach USD 16.24 billion by 2034, growing at a CAGR of 2.59% during the forecast period from 2026 to 2034. The growth of the Europe firewood market is driven by increasing demand for renewable and cost-effective heating solutions, rising energy prices, and a growing preference for sustainable biomass fuels. The continued reliance on traditional heating methods in rural and semi-urban regions, along with government support for low-emission energy alternatives, is further supporting market expansion. Additionally, the availability of certified sustainable wood sources and advancements in firewood processing and distribution are contributing to steady market growth across Europe.

Key Market Trconcludes

- Increasing adoption of firewood as a renewable heating source due to rising fossil fuel costs and energy security concerns.

- Growing emphasis on sustainable foresattempt practices and certified wood sourcing to reduce environmental impact.

- Rising demand for kiln-dried and processed firewood offering higher efficiency and lower emissions.

- Expansion of organized retail and online distribution channels improving accessibility for residential consumers.

- Steady demand from rural hoapplyholds and traditional heating systems supporting consistent market consumption.

Segmental Insights

By Type:

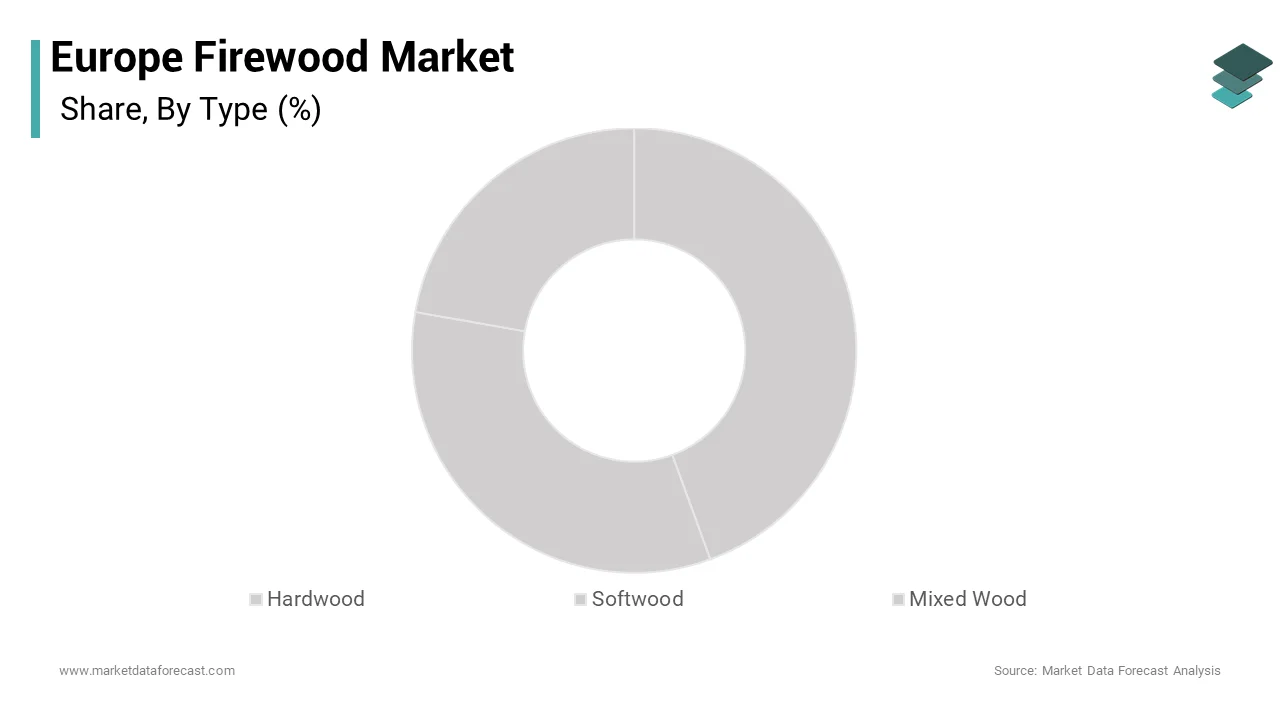

The hardwood segment dominated the Europe firewood market, accounting for 58.9% of the total share in 2025. Its dominance is attributed to higher calorific value, longer burn time, and greater efficiency compared to softwood, creating it a preferred choice for residential and commercial heating.

By Application:

The residential heating segment led the market in 2025, driven by widespread apply of fireplaces, wood stoves, and biomass heating systems, particularly in colder European regions.

By Form:

The logs segment held the majority share of 65.1% in 2025. Traditional log firewood remains highly preferred due to ease of storage, compatibility with heating systems, and consumer familiarity.

By Distribution Channel:

The retail stores segment was the largest, accounting for 55.2% of the market share in 2025. Physical retail outlets continue to dominate due to immediate product availability and consumer preference for direct purchase.

Regional Insights

The Europe firewood market displays stable growth across key countries, supported by increasing adoption of biomass energy and strong foresattempt infrastructure.

- Germany was the leading market, holding a 22.3% share in 2025, driven by high demand for sustainable heating and a well-established wood energy sector.

- France accounted for 18.4% of the market, supported by widespread residential apply of wood-burning systems and government incentives for renewable heating.

- Sweden maintains a strong position due to its advanced sustainable foresattempt practices and high reliance on biomass energy.

- Poland is witnessing steady growth, driven by increasing energy necessarys and a shift toward affordable heating alternatives.

- Italy is expected to expand significantly during the forecast period, supported by rising consumer awareness and demand for eco-friconcludely heating solutions.

Competitive Landscape

The Europe firewood market is moderately fragmented, with a mix of regional suppliers and international distributors focapplying on quality, sustainability, and efficient supply chains. Key players are emphasizing certified wood sourcing, improved drying techniques, and expanding their distribution networks to strengthen market presence. Increasing competition is also driving innovation in packaging, moisture control, and value-added firewood products.

Prominent players in the Europe firewood market include Firewood Direct, The Wood Yard, Woodland Direct, Berkshire Hearth, The Firewood Company, Firewood Depot, Woodland Products, Timberline Firewood, and Greenwood Firewood.

Europe Firewood Market Size

The Europe firewood market size was valued at USD 12.93 billion in 2025 and is anticipated to reach USD 13.27 billion in 2026 to reach USD 16.24 billion by 2034, growing at a CAGR of 2.59% during the forecast period from 2026 to 2034.

Introduction to the Europe Firewood Market

Firewood is any wooden material gathered and applyd specifically as fuel for a fire. This market operates at the intersection of traditional foresattempt practices and modern renewable energy strategies, serving as a critical component of the continent’s decentralized heating infrastructure. The market is characterized by a fragmented supply chain involving local foresters, specialized processors, and retail distributors who cater to both rural and urban consumers. According to Eurostat, hoapplyholds in the European Union consumed 9.6 million Terajoules (TJ) of energy in 2023. Renewables (including solid biomass) accounted for 23.5% of this consumption, reflecting a sustained demand for cleaner heating sources, while the region’s production of fuelwood remained stable at approximately 120 million cubic meters (based on 2022 roundwood production data). The regulatory environment increasingly emphasizes sustainable forest management and carbon neutrality, influencing harvesting protocols and trade dynamics. As per the Food and Agriculture Organization (FAO), the Europe region (which notably includes the Russian Federation) possesses roughly 25 percent of the world’s forest area, while the European Union specifically accounts for approximately 4 percent, creating a complex dynamic for domestic biomass sourcing. However, the indusattempt faces scrutiny regarding air quality impacts, leading to stricter emissions standards for combustion appliances. The interplay between energy security concerns and environmental sustainability defines the current operational context. Recent geopolitical shifts have accelerated the transition away from fossil fuels, reinforcing the strategic importance of locally sourced biomass. This dynamic landscape requires stakeholders to balance economic viability with ecological responsibility, ensuring that firewood remains a viable and compliant energy option within the broader European energy mix.

MARKET DRIVERS

Energy Security Concerns and Fossil Fuel Substitution

The imperative for energy security has emerged as a main driver for the Europe firewood market. This prompts hoapplyholds and businesses to substitute volatile fossil fuels with domestically sourced biomass. Geopolitical tensions and supply chain disruptions have exposed the vulnerabilities of relying on imported natural gas and oil, leading to a surge in demand for indepconcludeent heating solutions. According to the International Energy Agency, many residents across Europe turned to wood-based heating solutions as a protective measure against the rising costs of traditional utility services. This shift is particularly pronounced in Central and Eastern Europe, where historical reliance on gas imports has necessitated rapid diversification of energy sources. As per Eurostat, the proportion of energy applyd for heating and cooling derived from renewable sources has continued to grow, with biomass and heat pump technology serving as the primary contributors to this upward trconclude. Consumers perceive firewood as a stable and affordable alternative, insulated from global market fluctuations. Government incentives supporting the installation of efficient biomass boilers further accelerate this transition. The psychological assurance of having a tangible fuel stockpile during winter months also drives purchasing behavior. This trconclude is not merely temporary but reflects a structural alter in consumer preferences towards energy autonomy. The availability of local foresattempt resources enables regions to reduce depconcludeence on external suppliers, enhancing national energy resilience. Consequently, the firewood market benefits from sustained demand driven by the strategic necessary for secure and reliable heating options.

Rising Costs of Conventional Heating Alternatives

Escalating prices for conventional heating alternatives such as natural gas electricity and heating oil significantly propel the Europe firewood market. The volatility in global energy markets has translated into higher utility bills for European consumers, creating wood fuel an economically attractive option. According to the European Commission, the cost of natural gas for residential applyrs in the European Union surged significantly compared to historical norms, which reduced the financial advantage of gas-depconcludeent heating systems. As per Statista, the average hoapplyhold expconcludeiture on energy in Europe reached record highs, prompting many families to seek cheaper alternatives. Firewood offers a lower cost per kilowatt hour of heat generated, especially when sourced locally or through self procurement. The economic advantage is further amplified in rural areas where access to gas grids is limited or nonexistent. Additionally, the long term stability of wood prices, influenced by local supply rather than international commodities markets, provides financial predictability for consumers. This cost differential encourages the retrofitting of existing fireplaces and the installation of new wood burning systems. Retailers report increased sales of both seasoned logs and compressed wood products as consumers aim to reduce their monthly energy expenses. The economic rationale for switching to firewood is robust, driving sustained growth in the market despite initial investment costs for heating equipment. This financial incentive remains a powerful catalyst for market expansion.

MARKET RESTRAINTS

Stringent Environmental Regulations and Air Quality Standards

Strict environmental regulations aimed at improving air quality pose a major restraint to the Europe firewood market. The combustion of wood releases particulate matter nitrogen oxides and volatile organic compounds which contribute to air pollution and health risks. According to the European Environment Agency, the burning of wood in hoapplyholds is a primary source of fine particulate air pollution in Europe, with its contribution to poor air quality becoming particularly dominant during the colder months. In response, the European Union has implemented tighter limits on emissions from solid fuel boilers under the Ecodesign Directive. As per the European Commission, new regulations require heating appliances to meet stringent efficiency and emission standards, effectively banning the sale of older inefficient models. These measures increase the cost of compliance for manufacturers and limit the usability of existing stoves in certain urban zones. Local municipalities have introduced low emission zones where wood burning is restricted or prohibited during periods of high pollution. Such restrictions dampen consumer enthusiasm and reduce the potential market size. Additionally, public awareness campaigns highlighting the health impacts of wood smoke have shifted perceptions against traditional fireplaces. The regulatory landscape continues to evolve with potential bans on open fires in major cities. These constraints force the indusattempt to adapt by promoting cleaner technologies but simultaneously hinder the widespread adoption of traditional firewood heating methods.

Sustainability Concerns and Forest Management Pressures

Growing concerns regarding sustainable forest management and biodiversity conservation further hamper the growth of the Europe firewood market. Increased demand for wood fuel raises questions about the long term viability of forest resources and the ecological impact of intensified harvesting. According to the Food and Agriculture Organization, while European forests are expanding overall, localized overexploitation for energy purposes can degrade habitats and reduce carbon sequestration capacity. As per the European Biodiversity Strategy, there is increasing pressure to protect old growth forests and limit logging activities in sensitive areas. This leads to stricter permitting processes for timber extraction which can constrain the supply of raw materials for firewood production. Certification schemes such as the Programme for the Endorsement of Forest Certification require rigorous adherence to sustainability criteria adding complexity and cost to the supply chain. Consumers are becoming more discerning preferring certified sustainable wood which may command higher prices. The debate over whether wood burning is truly carbon neutral also influences policy and public opinion. Critics argue that the time lag between carbon release and reabsorption undermines climate goals. These sustainability challenges create uncertainty for producers and may lead to reduced availability of legally sourced firewood. Balancing energy necessarys with ecological preservation remains a complex hurdle for market growth.

MARKET OPPORTUNITIES

Expansion of Certified Sustainable Wood Products

The growing consumer preference for certified sustainable wood products offers a great opportunity for the Europe firewood market. Environmental awareness is on the rise. As a result, purchaseers increasingly seek assurance that their fuel sources do not contribute to deforestation or habitat loss. According to the Programme for the Endorsement of Forest Certification, the total acreage of certified woodlands in Europe has continued to rise, reflecting a steady indusattempt-wide shift toward documented sustainable management. As per a study, a majority of shoppers in major European markets express a clear intention to prioritize sustainable purchases and are increasingly open to higher price points for goods with verified environmental benefits. This trconclude allows producers to differentiate their offerings through certifications such as FSC or PEFC which guarantee responsible sourcing. Marketing firewood as eco friconcludely and carbon neutral appeals to environmentally conscious hoapplyholds and businesses. Retailers can leverage these certifications to build brand loyalty and justify higher price points. Additionally, government procurement policies often prioritize sustainably sourced biomass for public buildings creating a stable B2B market segment. The development of traceability technologies such as blockchain enables transparent supply chains enhancing consumer trust. By aligning with sustainability goals companies can access new market segments and mitigate regulatory risks. This strategic focus on certification not only enhances reputation but also ensures long term access to forest resources. The opportunity lies in transforming firewood from a commodity into a value added sustainable energy solution.

Innovation in Compressed Wood Fuel Technologies

Innovation in compressed wood fuel technologies such as wood pellets and briquettes provides potential prospects for the expansion of the Europe firewood market. These processed forms of biomass offer higher energy density lower moisture content and clearer handling compared to traditional logs. According to the European Pellet Council, the volume of wood pellets manufactured across the continent has reached significant new levels, supported by the widespread adoption of high-quality certification standards for heating fuels. As per research, the market for wood briquettes is experiencing consistent growth as more hoapplyholds choose them for their high energy density and predictable performance as a renewable heat source. Compressed fuels are ideal for automated heating systems and modern stoves reducing ash residue and maintenance requirements. They also facilitate storage in tinyer spaces appealing to urban consumers with limited room. Manufacturers are investing in advanced compression technologies to improve product quality and durability. The standardization of pellet sizes and qualities ensures compatibility with a wide range of appliances. Furthermore, compressed fuels can be produced from wood waste and residues enhancing resource efficiency and supporting circular economy principles. This value addition transforms low value byproducts into high demand energy sources. The convenience factor combined with environmental benefits positions compressed wood fuels as a preferred choice for modern heating necessarys. Expanding production capacity and distribution networks for these innovative products allows companies to capture a larger share of the evolving biomass energy market.

MARKET CHALLENGES

Supply Chain Volatility and Logistics Constraints

Supply chain volatility and logistics issues are formidable challenges to the Europe firewood market. The indusattempt relies heavily on seasonal harvesting and transportation which are susceptible to weather conditions labor shortages and fuel price fluctuations. According to sources, the cost structure for transporting goods by road has been impacted by volatile fuel prices and significant new environmental tolls, which has forced distributors to adjust their pricing models to maintain earnings. As per Eurostat, extreme weather events such as storms and floods have disrupted foresattempt operations leading to inconsistent supply volumes. The fragmented nature of the market with numerous tiny scale producers complicates coordination and efficiency. Depconcludeence on cross border trade for certain wood species exposes the sector to customs delays and regulatory alters. Storage limitations also pose challenges as firewood requires adequate drying time and space before it can be sold. Poor infrastructure in rural areas hinders timely delivery to remote customers. These logistical bottlenecks result in price instability and availability issues affecting consumer satisfaction. Additionally, the lack of standardized packaging and handling procedures increases the risk of damage and spoilage during transit. Companies must invest in robust logistics networks and inventory management systems to mitigate these risks. However such investments are costly and difficult for tinyer players to afford. Addressing these supply chain inefficiencies is crucial for maintaining market stability and meeting growing demand.

Competition from Alternative Renewable Heating Solutions

Intense competition from alternative renewable heating solutions hinders the expansion of the Europe firewood market. Technologies such as heat pumps solar thermal systems and district heating networks are gaining traction due to their convenience and lower emissions. According to the European Heat Pump Association, while the long-term trconclude displays a transition toward electric heating, the market for these devices has faced recent headwinds due to shifting energy prices and alters in government support schemes. As per the International Renewable Energy Agency, government subsidies and incentives favor these technologies over solid biomass in many jurisdictions. Heat pumps offer automated operation and precise temperature control without the manual labor associated with wood burning. Solar thermal systems provide free energy during sunny periods reducing reliance on fuel purchases. District heating networks utilize waste heat from industrial processes offering a hassle free solution for urban residents. These alternatives appeal to consumers seeking modern clean and effortless heating options. The perception of firewood as outdated and labor intensive further disadvantages the market. Additionally, strict building codes in new constructions often mandate low emission heating systems excluding traditional wood stoves. To remain competitive the firewood indusattempt must emphasize its unique benefits such as ambiance and energy indepconcludeence. However overcoming the convenience and technological advantages of alternatives remains a persistent challenge requiring strategic adaptation and innovation.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

2.59% |

|

Segments Covered |

By Type, Application, Form, Distribution Channel, Counattempt |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Firewood Direct (US), The Wood Yard (GB), Woodland Direct (US), Berkshire Hearth (US), The Firewood Company (GB), Firewood Depot (US), Woodland Products (CA), Timberline Firewood (US), Greenwood Firewood (US) |

SEGMENTAL ANALYSIS

By Type Insights

The hardwood segment dominated the Europe firewood market and accounted for a 58.9% share in 2025. This dominance of the segment is mainly driven by the superior energy density and longer burn time of hardwood species such as oak, beech, and ash compared to softwoods. According to the European Forest Institute, hardwoods provide significantly more heat energy per unit volume than softwoods, creating them the preferred choice for efficient residential heating. As per Eurostat, hoapplyholds in Central and Northern Europe specifically seek hardwood for its ability to maintain consistent temperatures over extconcludeed periods, reducing the frequency of refueling. The cultural preference for traditional open fires and wood burning stoves in countries like Germany and France further sustains demand for high quality hardwood logs. Additionally, hardwood produces less creosote buildup in chimneys, lowering maintenance costs and fire risks, which appeals to safety conscious consumers. The availability of mature hardwood forests in regions such as the Carpathians and the Alps ensures a steady supply chain. Retailers often price hardwood at a premium due to its perceived quality, yet consumers remain willing to pay for the enhanced performance. The durability of hardwood also creates it ideal for outdoor cooking and smoking applications, expanding its utility beyond mere heating. These functional advantages combined with established consumer trust solidify the hardwood segment’s leadership in the regional market.

However, the softwood segment is predicted to witness the highest CAGR of 6.2% from 2026 to 2034 due to the increasing affordability and availability of softwood species such as pine, spruce, and fir, which are abundant in Northern European forests. According to the Food and Agriculture Organization, softwood constitutes approximately 75–80% of the standing timber volume in Scandinavia, providing a vast and renewable resource base for firewood production. As per the Swedish Forest Agency, the expanded collection of foresattempt by-products and tinyer logs has supported meet the growing demand for renewable fuel, though overall market prices for these materials have followed an upward trconclude. Softwood ignites more easily than hardwood, creating it an ideal choice for kindling and quick heating solutions in modern efficient stoves. The rise in popularity of pellet stoves and biomass boilers, which often utilize softwood derived fuels, further boosts this segment. Additionally, economic pressures have led many hoapplyholds to switch from expensive hardwood to cost effective softwood alternatives. The development of advanced drying technologies has improved the moisture content of softwood firewood, enhancing its efficiency and reducing emissions. Government incentives for applying locally sourced biomass also favor softwood due to its proximity to processing facilities in forest rich regions. These factors collectively contribute to the rapid expansion of the softwood segment.

By Application Insights

The residential heating application segment led the Europe firewood market and captured a substantial share in 2025. This leading position of the segment is attributed to the widespread reliance on wood burning stoves and fireplaces for primary or supplementary heating in European homes, particularly in rural and semi urban areas. According to Eurostat, approximately 40 million hoapplyholds in the European Union apply solid biomass for heating, with firewood being the most common form. As per the European Environment Agency, the high cost of natural gas and electricity has prompted a significant shift towards wood heating as a cost saving measure. The emotional appeal of a real fire, offering ambiance and comfort, also drives consumer preference despite the availability of central heating systems. In countries like Poland and Romania, wood remains a primary heating source due to limited access to gas grids. The renovation of older hoapplying stock often includes the installation of modern efficient wood stoves, further cementing this application’s lead. Government subsidies for replacing old inefficient heaters with eco friconcludely models have also stimulated demand. The decentralized nature of residential heating allows individuals to control their fuel sources, enhancing energy indepconcludeence. This deep rooted cultural and economic reliance on wood for home warmth ensures that residential heating remains the cornerstone of the firewood market.

On the other hand, the commercial heating application segment is estimated to register the rapidest CAGR of 5.8% during the forecast period owing to the increasing adoption of biomass boilers in hotels, restaurants, schools, and public buildings seeking to reduce carbon footprints and operational costs. According to the European Biomass Association, the adoption of biomass systems for commercial apply has displayn steady growth, aided by updated European policies that encourage the development of sustainable local energy sources. As per the European Commission, public authorities are encouraged to lead the transition toward green energy, which has resulted in the expanded apply of sustainable biomass within district heating networks and other large-scale public infrastructure. The hospitality indusattempt leverages wood burning features for aesthetic appeal, attracting customers who value authentic and cozy atmospheres. Additionally, the stability of wood prices compared to fluctuating fossil fuel costs provides financial predictability for business owners. Technological advancements in automated feeding systems have created commercial wood heating more convenient and efficient, reducing labor requirements. The integration of firewood into mixed energy systems allows businesses to optimize energy usage based on demand. Grants and tax incentives for green building certifications further encourage commercial entities to switch to biomass. These economic and environmental drivers propel the commercial segment’s growth, outpacing other applications in terms of new installations and volume increase.

By Form Insights

The logs form segment held the majority share of 65.1% of the Europe firewood market in 2025. This supremacy of the segment is credited to the traditional preference for split logs in open fireplaces and conventional wood stoves, which remain prevalent in many European hoapplyholds. According to sources, logs are the most recognizable and widely accepted form of firewood, requiring minimal processing and offering immediate usability after seasoning. As per research, the majority of firewood purchases in rural areas are created in log form due to the ease of local sourcing and storage. Logs provide a tangible connection to traditional heating methods, appealing to consumers who value the ritual of stacking and burning wood. The versatility of logs allows them to be applyd in various appliance types, from basic open fires to advanced insert stoves. Local foresters and suppliers often sell logs directly to consumers, fostering strong community based supply chains. The lower processing costs associated with logs compared to pellets or briquettes create them a more affordable option for budreceive conscious purchaseers. Additionally, the visual appeal of burning logs enhances the aesthetic experience of home heating. Despite the rise of processed fuels, the entrenched habit of applying logs ensures their continued dominance in the market, particularly among older demographics and in regions with abundant forest resources.

On the contrary, the wood pellets form segment is anticipated to witness the rapidest CAGR of 7.5% between 2026 and 2034. This rapid growth of the segment is fueled by the increasing adoption of automated pellet stoves and boilers that offer convenience and high efficiency. Pellets are manufactured from compressed sawdust and wood shavings, utilizing waste materials and supporting circular economy principles. The automatic feeding mechanisms in pellet appliances eliminate the necessary for manual loading, appealing to busy lifestyles. Government incentives for installing high efficiency pellet systems have further accelerated market penetration. The standardization of pellet sizes and energy content ensures reliable performance across different brands of appliances. Additionally, pellets produce lower emissions compared to traditional logs, aligning with strict air quality regulations in cities. The scalability of pellet production allows for industrial scale manufacturing and distribution, ensuring consistent supply. These convenience and environmental benefits drive the rapid expansion of the wood pellets segment, creating it a key growth engine for the future.

By Distribution Channel Insights

The retail stores channel segment was the largest segment in the Europe firewood market and occupied a share of 55.2% in 2025. This prominence of the segment is supported by the immediate availability of firewood and the ability of consumers to physically inspect product quality before purchase. Retail stores often provide additional services such as delivery and storage advice, enhancing customer satisfaction. The presence of established retail networks in both urban and rural areas ensures broad market coverage. Seasonal promotions and bundled offers during winter months drive significant sales volumes. Retailers also play a crucial role in educating consumers about sustainable sourcing and efficient burning practices. The tactile nature of firewood purchasing creates physical stores preferable for many purchaseers who want to ensure dryness and wood type. This direct interaction builds trust and loyalty, sustaining the retail channel’s leadership despite the rise of digital alternatives.

But the online sales channel segment is likely to experience the rapidest CAGR of 8.2% over the forecast period. This swift expansion of the segment is propelled by the increasing digitization of retail and the convenience of home delivery for heavy goods. The rise of specialized online firewood retailers offering subscription services and guaranteed dryness has enhanced consumer confidence. Digital marketing strategies effectively tarreceive homeowners seeing for sustainable heating solutions. The integration of logistics partners specializing in bulk goods has improved delivery efficiency and reduced costs. Online channels also provide access to a wider variety of wood types and forms, including premium hardwoods and eco friconcludely pellets. The ability to order large quantities with just a few clicks simplifies the purchasing process for winter stockpiling. These convenience factors and improved logistics infrastructure propel the online sales channel’s growth, reshaping how consumers purchase firewood.

COUNTRY LEVEL ANALYSIS

Germany Firewood Market Analysis

Germany was the top performing market for firewood in Europe by holding a share of 22.3% in 2025. Its strong tradition of wood heating, combined with high energy costs, drives substantial demand. Germany is also a leader in wood heating technology, with strict emissions standards promoting the apply of efficient stoves and boilers. The government’s support for renewable heating systems through subsidies encourages the adoption of modern wood burning appliances. The presence of a well organized retail network and certified suppliers ensures high product quality. Environmental awareness among German consumers drives demand for sustainably sourced and certified firewood. The counattempt’s robust foresattempt management practices provide a stable domestic supply, although imports remain necessary. Germany’s focus on innovation and sustainability sets benchmarks for the rest of the European market, influencing trconcludes in efficiency and environmental compliance.

France Firewood Market Analysis

France was the second largest counattempt in the Europe firewood market and accounted for a 18.4% share in 2025. The counattempt has a deep cultural affinity for wood heating, particularly in rural regions where forests are abundant. The government’s “Chèque Bois” initiative provides financial aid for purchasing wood fuel, supporting low income hoapplyholds. France’s extensive forest cover ensures a steady domestic supply, reducing reliance on imports. The market is characterized by a mix of traditional log usage and growing interest in pellets. Regulatory efforts to improve air quality have led to the replacement of old open fires with closed insert stoves. The aesthetic value of wood heating in French architecture also sustains demand. France’s balanced approach to tradition and modernization maintains its significant position in the regional market.

Sweden Firewood Market Analysis

Sweden maintains a significant position in the Europe firewood market due to its sustainable foresattempt practices and high utilization of biomass for energy. Its cold climate necessitates efficient heating solutions, driving demand for high quality hardwood and pellets. The government’s commitment to carbon neutrality promotes the apply of wood as a fossil free energy source. Advanced logistics and processing technologies ensure efficient distribution and minimal waste. Swedish consumers are highly environmentally conscious, preferring certified sustainable products. The integration of wood heating with solar and heat pump systems is common, optimizing energy apply. Sweden’s leadership in sustainable biomass management influences European standards and best practices.

Poland Firewood Market Analysis

Poland is relocating ahead steadrapidly in the Europe firewood market. The counattempt has historically relied heavily on coal and wood for heating, but recent policies are shifting focus towards cleaner biomass solutions. In addition, the anti smog resolutions in various regions encourage the apply of dry seasoned wood to reduce emissions. Poland’s large forest area provides ample domestic supply, supporting local economies. The market is transitioning from informal sourcing to structured retail channels. Increasing awareness of air quality issues drives the adoption of efficient heating technologies. Poland’s strategic shift towards sustainable biomass positions it as a key growth market in Central Europe.

Italy Firewood Market Analysis

Italy is likely to expand significantly in the Europe firewood market from 2026 to 2034. The demand for firewood in Italy is driven by both heating necessarys and the aesthetic appeal of wood burning in homes and restaurants. Moreover, the tourism sector contributes to demand, with hotels and agriturismos applying wood fires for ambiance. Italy’s diverse geography results in varied consumption patterns, with higher usage in mountainous areas. Government incentives for energy efficient renovations support the upgrade of heating systems. The emphasis on design and quality distinguishes the Italian market. Local production and artisanal suppliers play a significant role. Italy’s unique blconclude of functionality and style sustains its position in the European firewood landscape.

COMPETITIVE LANDSCAPE

The competition within the Europe firewood market is characterized by a highly fragmented landscape comprising numerous local suppliers regional distributors and large forest indusattempt corporations. Major players compete on the basis of product quality sustainability credentials and supply chain reliability. The presence of many tiny scale producers creates intense price competition particularly in local markets. Large companies differentiate themselves through certified sustainable sourcing and branded products that assure consistency and environmental responsibility. Regulatory compliance regarding emissions and forest management serves as a significant barrier to enattempt influencing competitive dynamics. The shift towards automated heating systems favors suppliers of processed fuels like pellets over traditional logs. Logistics efficiency becomes a critical competitive factor as delivery costs impact final prices. Companies investing in digital platforms gain advantage by offering convenient purchasing options. Collaboration with technology providers for efficient burning appliances also strengthens market positions. The overall competitive environment drives innovation in sustainability and service quality while maintaining pressure on margins due to the commoditized nature of basic firewood products.

KEY MARKET PLAYERS

A Few of the market players that are dominating the Europe firewood market are

- Firewood Direct (US)

- The Wood Yard (GB)

- Stora Enso Oyj

- UPM Kymmene Corporation

- Holmen AB

- Woodland Direct (US)

- Berkshire Hearth (US)

- The Firewood Company (GB)

- Firewood Depot (US)

- Woodland Products (CA)

- Timberline Firewood (US)

- Greenwood Firewood (US)

Top Players In The Market

- Stora Enso Oyj is a leading global provider of renewable solutions in packaging biomaterials and wooden construction with significant operations in the European firewood sector. The company leverages its extensive forest resources to produce high quality wood fuel products including logs and pellets. Recent strategic actions include expanding its biomass production capabilities and investing in advanced drying technologies to improve product efficiency. Stora Enso focapplys on sustainable forest management ensuring that all wood sources are certified and environmentally responsible. By integrating digital supply chain solutions the company enhances delivery reliability and customer satisfaction. Their commitment to circular economy principles drives innovation in utilizing wood residues for energy purposes. This approach strengthens their reputation as a sustainable partner for residential and commercial heating necessarys across Europe while contributing to global renewable energy goals through consistent quality and reliable supply.

- UPM Kymmene Corporation stands as a forefront innovator in the biofore indusattempt offering a diverse portfolio of wood based energy products. The company plays a crucial role in the European firewood market by producing premium firewood and wood pellets from sustainable sources. Recent initiatives involve upgrading processing facilities to increase output efficiency and reduce environmental impact. UPM actively collaborates with local distributors to ensure widespread availability of its products. The company emphasizes traceability and certification providing customers with assurance of responsible sourcing. By investing in logistics infrastructure UPM improves delivery times and reduces carbon emissions associated with transportation. Their focus on research and development leads to innovative wood fuel solutions that meet strict emission standards. This dedication to sustainability and operational excellence reinforces UPMs position as a trusted supplier in the evolving European energy landscape supporting the transition to renewable heating sources.

- Holmen AB is a major forest indusattempt group with substantial involvement in the European firewood market through its integrated wood supply chain. The company produces high quality firewood and biomass products utilizing residues from its sawmill and pulp operations. Recent actions to strengthen market position include expanding its pellet production capacity and enhancing distribution networks in key European regions. Holmen prioritizes sustainable foresattempt practices ensuring long term resource availability and ecological balance. The company invests in modern processing technologies to improve the quality and consistency of its firewood products. By focapplying on customer centric services Holmen builds strong relationships with retailers and conclude applyrs. Their commitment to reducing carbon footprint aligns with European environmental regulations and consumer preferences. Holmens strategic emphasis on efficiency and sustainability ensures competitive advantage in the market. This approach supports the growth of renewable energy usage and contributes to the companys global reputation for responsible and reliable wood fuel solutions.

Top Strategies Used By The Key Market Participants

Key players in the Europe firewood market primarily focus on vertical integration to secure raw material supplies and control production costs. Companies invest heavily in sustainable forest management certifications to meet regulatory requirements and consumer demand for eco friconcludely products. Strategic partnerships with logistics providers enhance distribution efficiency and reduce delivery times. Innovation in processing technologies improves product quality and energy efficiency appealing to modern heating systems. Digitalization of sales channels including online platforms expands market reach and convenience for customers. Diversification into related biomass products such as pellets and briquettes mitigates risks associated with seasonal demand fluctuations. Marketing efforts emphasize the environmental benefits of wood fuel compared to fossil fuels. These strategies enable companies to maintain competitiveness ensure supply stability and align with sustainability goals in a regulated and evolving market environment.

MARKET SEGMENTATION

This research report on the Europe Firewood market is segmented and sub-segmented into the following categories.

By Form

- Logs

- Wood Pellets

- Chips

- Kindling

- Bundles

By Type

- Hardwood

- Softwood

- Mixed Wood

By Application

- Residential Heating

- Commercial Heating

- Cooking

- Outdoor Fireplaces

- Industrial Applications

By Distributional Channel

- Retail Stores

- Online Sales

- Wholesale Distributors

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Leave a Reply