Europe Urea Market Size

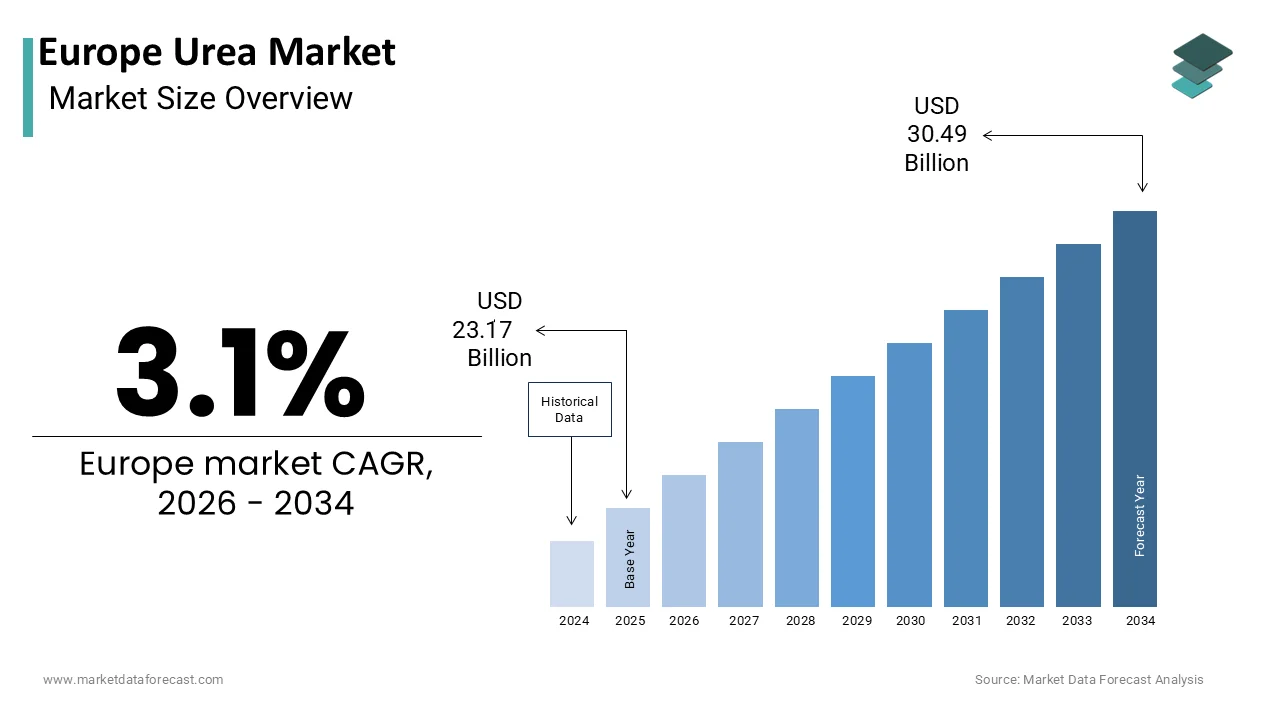

The Europe urea market was valued at USD 23.17 billion in 2025, is estimated to reach USD 23.88 billion in 2026, and is projected to reach USD 30.49 billion by 2034, growing at a CAGR of 3.1% from 2026 to 2034.

Urea remains a fundamental nitrogenous compound within the European agricultural and industrial sectors, functioning primarily as a high-concentration nitrogen fertilizer. This white crystalline substance is synthesized from ammonia and carbon dioxide under high-pressure and high-temperature conditions. The market dynamics are heavily influenced by the continent’s commitment to food security and sustainable agricultural practices. According to Eurostat, the utilized agricultural area in the European Union covers approximately 161 million hectares, indicating a vast landscape requiring nutrient management. Urea provides an efficient source of nitrogen, which is essential for protein synthesis in plants and overall crop development. Beyond agriculture, urea finds application in automotive emissions control systems,s where it is utilized in selective catalytic reduction technologies to reduce nitrogen oxide emissions from diesel engines. According to the European Automobile Manufacturers Association, the share of diesel cars in new registrations remains significant,nt although declining, necessitating continued demand for automotive-grade urea. The chemical indusattempt also utilizes urea in the production of resins, adhesives, and plastics. The European Environment Agency emphasizes the importance of managing nitrogen cycles to prevent environmental degradation such as eutrophication. Consequently, regulatory frameworks govern the application rates and methods of urea usage to minimize ecological impact. The interplay between agricultural necessity, industrial utility, and environmental stewardship defines the current operational landscape for urea in Europe.

MARKET DRIVERS

Intensive Agricultural Practices Drive Sustained Nitrogen Fertilizer Demand

The persistent demand for nitrogen fertilizers within the intensive agricultural sector is one of the major factors contributing to the expansion of the Europe urea market. Nitrogen is a critical macronutrient that limits plant growth in many European soils, creating its supplementation essential for commercial farming. According to the Food and Agriculture Organization of the United Nations, cereal production in Europe requires substantial nitrogen inputs to meet domestic consumption and export obligations. Countries like France, Germany, and Poland are major producers of wheat, barley, and maize, which are heavy nitrogen feeders. The European Commission data indicate that the average nitrogen utilize efficiency in EU agriculture has improved, but total application volumes remain high due to the intensity of cultivation. Farmers prefer urea due to its high nitrogen content of 46%, which reduces transportation and storage costs compared to other nitrogen sources. The Common Agricultural Policy supports income stability for farmers, enabling them to invest in quality input,s including urea. According to the International Fertilizer Association, global nitrogen demand continues to grow, driven by population increases and dietary shifts towards protein-rich foods. In Europe, the focus on precision agriculture allows for optimized urea application, reducing waste while maintaining productivity. The necessary to replenish soil nutrients after each harvest cycle creates a recurring demand pattern. This structural reliance on nitrogen fertilizers ensures a stable baseline consumption of urea across the continent, regardless of short-term price fluctuations.

Stringent Automotive Emission Standards Boost AdBlue Consumption

The adoption of rigorous emission standards for diesel-powered vehicles is further boosting the expansion of the urea market in Europe. These systems utilize a urea-based solution commonly known as AdBlue or Diesel Exhaust Fluid to convert harmful nitrogen oxides into harmless nitrogen and water vapor. According to the European Automobile Manufacturers Association, millions of diesel passenger cars and commercial vehicles operate on European roads, requiring regular refilling of AdBlue tanks. The Euro 6 emission standards, which mandate strict limits on nitrogen oxide emissions, have built SCR technology indispensable for modern diesel engines. According to the European Environment Agency, transport remains a major source of air pollution in urban areas, prompting regulators to enforce compliance rigorously. The logistics and freight sectors, which rely heavily on diesel-powered trucks, are substantial consumers of automotive-grade urea. The European Union’s goal to reduce greenhoutilize gas emissions from transport by 90% by 2050 further reinforces the role of cleaner diesel technologies during the transition to electrification. Data from indusattempt analysts suggests that the average consumption of AdBlue per vehicle is increasing as newer engines require more precise dosing for optimal performance. The expansion of the commercial vehicle fleet in emerging European markets also contributes to rising demand. This non-agricultural application diversifies the urea market and provides a growth avenue indepconcludeent of seasonal agricultural cycles.

MARKET RESTRAINTS

Volatility in Natural Gas Prices Disrupts Production Economics

The significant fluctuation in natural gas pricing is majorly impeding the Europe urea market expansion. The manufacturing process is energy-intensive and highly sensitive to input costs, creating European producers vulnerable to global energy market fluctuations. According to the International Energy Agency, natural gas prices in Europe experienced unprecedented spikes following geopolitical tensions affecting supply chains from major exporters. These price surges significantly increase the cost of production, rconcludeering domestic urea manufacturing less competitive compared to imports from regions with cheaper gas resources such as the Middle East and Russia. According to the European Chemical Indusattempt Council, many chemical plants, including ammonia and urea facilities, were forced to reduce output or shut down temporarily during periods of peak energy costs. This supply disruption leads to depconcludeency on imports, which can be subject to trade barriers and logistical delays. The high cost structure also discourages new investments in domestic production capacity, limiting long-term supply security. Farmers and industrial acquireers face unpredictable pricing, which complicates budreceiveing and procurement strategies. The European Union’s efforts to diversify energy sources and increase renewable energy integration are ongoing,g but the transition period maintains exposure to fossil fuel price risks. This economic instability acts as a persistent brake on market growth and profitability for local manufacturers.

Strict Environmental Regulations Limit Application Rates and Methods

Rigid environmental mandates designed to curb nitrogen pollution are another significant impediment to the growth of the Europe urea market. Excessive nitrogen application leads to nitrate leaching into groundwater and ammonia volatilization into the atmosphere, cautilizing environmental damage and health issues. According to the European Environment Agency, nitrates in drinking water sources remain a concern in several member states, prompting stricter enforcement of the Nitrates Directive. This directive designates Nitrate Vulnerable Zones where fertilizer utilize is strictly controlled and monitored. According to the European Commission, the Farm to Fork Strategy aims to reduce nutrient losses by 50% while ensuring no deterioration in soil fertility by 2030. These tarreceives require farmers to adopt more efficient fertilization techniques, es such as utilizing urease inhibitors or switching to alternative nitrogen sources with lower environmental footprints. The mandatory utilize of inhibitors adds to the cost of urea application and requires modifys in farming practices. Regulatory pressure also drives the phase out of conventional urea in favor of enhanced efficiency fertilizers, which may have different market dynamics. Compliance with these regulations involves additional administrative burdens and monitoring costs for farmers. The push towards organic farming, which prohibits synthetic fertilizers, further reduces the potential market size for conventional urea. These regulatory constraints create a challenging operating environment for urea suppliers who must adapt to evolving legal frameworks.

MARKET OPPORTUNITIES

Development of Enhanced Efficiency Fertilizers Offers Product Differentiation

The emergence and integration of Enhanced Efficiency Fertilizers is offering a promising growth opportunity for the Europe urea market. These products include urea treated with urease and nitrification inhibitors, which slow down the conversion of urea to ammonia and nitrates, reducing losses to the environment. According to the International Fertilizer Association, the utilize of inhibitors can improve nitrogen utilize efficiency by 10% to 20%, depconcludeing on soil and climatic conditions. This technological advancement aligns with the European Union’s sustainability goals and allows farmers to comply with stricter environmental regulations without sacrificing yield. According to research from leading agricultural universities in Europe, inhibitor-treated urea displays promising results in reducing ammonia emissions and nitrate leaching. The growing awareness among farmers about sustainable practices drives demand for these advanced products. Chemical companies are investing in research and development to create proprietary inhibitor formulations that offer better performance and cost-effectiveness. The regulatory support for low-emission farming practices further incentivizes the uptake of enhanced-efficiency urea. Market players can differentiate their offerings by providing integrated solutions that combine product quality with agronomic advice. This shift towards value-added products opens new revenue streams and enhances customer loyalty. The transition from commodity urea to specialized formulations represents a strategic opportunity for market growth and innovation.

Expansion of Urea Usage in Renewable Energy and Chemical Synthesis

Broadening the scope of urea utilize in green energy and chemical synthesis is a major opportunity for the Europe urea market. Urea is increasingly being explored as a hydrogen carrier due to its high hydrogen content and ease of storage and transport compared to gaseous hydrogen. According to recent studies, urea electrolysis is a promising method for producing green hydrogen with lower energy requirements than water electrolysis. This application aligns with the European Union’s hydrogen strategy, which aims to establish a robust hydrogen economy to decarbonize heavy indusattempt and transport. According to the European Clean Hydrogen Partnership, research into innovative hydrogen production methods is receiving significant funding and attention. Additionally, urea is utilized in the production of melamine,e which is essential for laminates, coatings, and flame retardants utilized in construction and automotive industries. The growing demand for sustainable materials drives innovation in urea-based resins and polymers. The pharmaceutical indusattempt also utilizes urea in various synthesis processes for drugs and personal care products. Diversifying into these high-value applications reduces depconcludeence on the cyclical agricultural market. Companies that invest in these emerging technologies can capture early relocater advantages. The integration of urea into the circular economy through waste-to-energy processes further enhances its strategic importance. This broadening of application scope provides resilience and new growth trajectories for the Europe urea market.

MARKET CHALLENGES

Depconcludeency on Imports Creates Supply Chain Vulnerabilities

The heavy reliance on imported materials is a major challenge to the expansion of the Europe urea market. Due to high production costs associated with natural gas prices, Europe imports a significant portion of its urea necessarys from countries like Russia, Trinidad and Tobago, and the Middle East. According to the United States Department of Agriculture, global trade flows for urea are highly concentrated, creating importing regions susceptible to supply disruptions. Geopolitical tensions and trade sanctions can abruptly cut off supplies, leading to shortages and price spikes. According to the European Commission, the war in Ukraine highlighted the risks of relying on a single source for critical agricultural inputs. Logistics challenges such as port congestion, shipping delays, and increased freight costs further complicate the import process. The lack of sufficient domestic production capacity means that Europe has limited bargaining power in international markets. Currency fluctuations also impact the cost of imports, adding another layer of financial uncertainty. Ensuring supply security requires diversifying import sources and investing in strategic reserves, which involve significant coordination and cost. The unpredictability of global trade policies and export restrictions by producing countries adds to the complexity. This structural depconcludeency undermines the stability of the urea supply chain and poses a continuous challenge for stakeholders aiming to ensure consistent availability for European farmers and industries.

Balancing Productivity with Environmental Sustainability Goals

Reconciling agricultural output with ambitious environmental goals is another significant challenge to the Europe urea market. Farmers are under pressure to maintain high yields to ensure food security while simultaneously reducing their environmental footprint as mandated by EU policies. According to the European Environment Agency, agriculture is a major source of ammonia emissions and water pollution, requiring significant modifys in farming practices. The Farm to Fork Strategy and Biodiversity Strategy set stringent tarreceives for reducing fertilizer utilize and improving nutrient management. According to the Joint Research Centre of the European Commission, achieving these tarreceives requires widespread adoption of precision agriculture technologies and alternative fertilization methods, ds which can be costly and technically demanding. Small to medium-sized farms may struggle to afford the necessary equipment and training, leading to unequal adoption rates. The transition away from conventional urea towards more sustainable alternatives requires time and investment in research and extension services. There is also a risk that reduced fertilizer utilize could lead to lower crop yields, impacting farm incomes and food prices. Policycreaters must navigate this trade-off carefully to avoid unintconcludeed consequences. The indusattempt faces the challenge of developing and promoting solutions that meet both productivity and sustainability criteria. This dual requirement creates uncertainty and requires continuous adaptation from all market participants.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Grade, Application, and Region. |

|

Various Analyses Covered |

Global, Regional and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Yara International ASA, CF Industries Holdings, Inc., Nutrien Ltd., OCI N.V., EuroChem Group AG, BASF SE, Borealis AG, SABIC, Grupa Azoty S.A., Achema AB, Fertiberia S.A., SKW Piesteritz GmbH |

SEGMENTAL ANALYSIS

By Grade Insights

The fertilizer grade segment led the market with the largest share of 84.4% of the regional market share in 2025. This overwhelming dominance is driven by the critical role urea plays as a primary source of nitrogen for crop production across the continent. The high nitrogen content of 46% creates it the most efficient solid nitrogen fertilizer available, ensuring cost-effective nutrient delivery for large-scale agriculture. According to the International Fertilizer Association, nitrogen fertilizers account for the majority of global nutrient consumption, with urea being the preferred choice due to its handling properties and solubility. As per the European Commission, cereals, which are heavy nitrogen consumers, occupy a significant portion of the utilized agricultural area in the EU. Countries like France and Germany rely heavily on urea to maintain wheat and barley yields, which are essential for both domestic food security and export markets. The Common Agricultural Policy supports farm incomes, enabling continued investment in high-quality fertilizers. According to Eurostat, the value of agricultural output remains robust, necessitating consistent input application. The simplicity of storage and transport compared to liquid nitrogen solutions further cements its position. Farmers appreciate the flexibility of applying urea as a basal dressing or top dressing, depconcludeing on crop stages. The established distribution networks and familiarity among agronomists ensure that fertilizer-grade urea remains the backbone of European nutrient management strategies despite emerging alternatives.

However, the technical grade segment is anticipated to record a CAGR of 4.5% over the forecast period, owing to the expanding industrial applications, particularly in the automotive sector for selective catalytic reduction systems and in chemical synthesis for resins and plastics. The stringent Euro 6 emission standards mandate the utilize of diesel exhaust fluid,d which is a high-purity urea solution, to reduce nitrogen oxide emissions from vehicles. According to the European Automobile Manufacturers Association, the large fleet of diesel commercial vehicles and passenger cars ensures steady demand for automotive-grade urea. As the logistics and transport sectors remain vital to the European economy, the consumption of AdBlue continues to rise. Additionally, the chemical indusattempt utilizes technical grade urea in the production of melamine formaldehyde resins, which are widely utilized in laminates, adhesives, and coatings. The construction and automotive industries drive demand for these materials. According to the European Chemical Indusattempt Council, the specialty chemicals sector is experiencing growth due to innovation in sustainable materials. Technical grade urea requires a higher purity level,s which commands premium prices and offers better margins for producers. The shift towards green chemisattempt and biobased products also opens new avenues for high-purity urea applications. These diverse industrial utilizes contribute to the rapider growth rate of the technical grade segment compared to the mature fertilizer market.

By Application Insights

The agriculture segment led the market by accounting for the highest share of 84.1% of the European market in 2025. The leading position of the agriculture segment in the European market can be credited to the fundamental necessary for nitrogen fertilizers to sustain crop productivity and ensure food security for the European population. Urea is the most widely utilized nitrogen source due to its high nutrient concentration and economic efficiency. According to the Food and Agriculture Organization of the United Nations, cereal production in Europe requires substantial nitrogen inputs to achieve optimal yields. Wheat, maize, and barley are staple crops that demand regular nitrogen supplementation throughout their growth cycles. The European Commission reports that the utilized agricultural area in the EU is extensive, requiring millions of tonnes of nutrients annually. The Common Agricultural Policy provides financial support to farmers, enabling them to purchase necessary inputs, including urea. According to Eurostat, the agricultural sector contributes significantly to the rural economy and employment, maintaining strong political and economic support. The intensification of farming practices to maximize output per hectare further drives urea consumption. Precision agriculture techniques are being adopted to optimize application rates, reducing waste while maintaining effectiveness. The reliance on synthetic fertilizers remains high despite efforts to promote organic farming due to the scale of conventional agriculture. The structural depconcludeence of European agriculture on nitrogen fertilizers ensures that the agriculture segment remains the primary driver of urea demand in the region.

However, the chemical synthesis segment is anticipated to register the highest CAGR of 5.5% over the forecast period, owing to the increasing demand for urea-derived chemicals such as melamine, urea formaldehyde resins, and isocyanates, which are essential for various industrial products. Melamine is widely utilized in the production of laminates, coatings, and flame retardants,s which are integral to the construction and automotive industries. According to the European Construction Indusattempt Federation, the construction sector is recovering and expanding, driving up demand for building materials that utilize these resins. The automotive indusattempt also relies on lightweight composite materials built from urea-based polymers to improve fuel efficiency and meet emission standards. According to the European Chemical Indusattempt Council, innovation in material science is leading to new applications for urea derivatives in sustainable and high-performance products. The shift towards bio-based and recyclable materials is encouraging manufacturers to explore urea-based alternatives to petroleum-derived chemicals. The production of adhesives and binders for wood panels and insulation materials also contributes to rising demand. Industrial investments in capacity expansion for these downstream products directly translate into higher consumption of technical-grade urea. The diversification of urea applications beyond traditional fertilizers into high-value chemical intermediates offers significant growth potential. This segment benefits from technological advancements and regulatory support for sustainable industrial practices.

COUNTRY LEVEL ANALYSIS

Russia Urea Market Analysis

Russia accounted for a dominant share of 31.3% of the European market in 2025 and is expected to continue its influence as a major producer and consumer. The counattempt possesses vast natural gas reserves, which serve as the primary feedstock for urea production, giving it a significant cost advantage. According to the United States Department of Agriculture, Russia is one of the world’s largest exporters of urea, supplying significant volumes to European markets despite geopolitical tensions. The domestic agricultural sector in Russia is also a major consumer, driven by government initiatives to boost grain production and achieve food self-sufficiency. According to the Russian Federal State Statistics Service, agricultural output has increased steadily, with substantial areas dedicated to wheat and barley cultivation. The modernization of farming practices and increased utilize of fertilizers have enhanced yields. Russia’s strategic location allows for efficient logistics to European acquireers via pipeline and rail networks. However, trade sanctions and export restrictions have introduced volatility affecting supply chains. The government supports the chemical indusattempt through subsidies and infrastructure development, ensuring continued production capacity. The integration of vertical production chains from gas extraction to fertilizer manufacturing enhances competitiveness. Despite political challenges, Russia remains a pivotal player in the European urea landscape due to its resource abundance and production scale. The market status is characterized by high export orientation and strategic importance in global nutrient trade flows.

Germany Urea Market Analysis

Germany represents a key portion of the market, which is anticipated to maintain steady demand across industrial and agricultural sectors. The counattempt’s advanced agricultural sector and robust chemical indusattempt drive substantial demand for urea in various applications. According to the German Federal Minisattempt of Food and Agriculture, agriculture is a key economic sector with intensive crop production requiring efficient nutrient management. Germany is a major producer of wheat, rapeseed, and sugar beet, ts which necessitate regular nitrogen application. The chemical indusattempt in Germany is one of the largest globally, utilizing urea in the production of resins, adhesives, and automotive fluids. According to the German Chemical Indusattempt Association, the sector invests heavily in research and development, leading to innovative products. The automotive indusattempt’s requirement for AdBlue to meet emission standards further boosts consumption. Germany’s commitment to environmental sustainability has led to the adoption of precision farming techniques and enhanced efficiency fertilizers. The counattempt imports significant volumes of urea to meet domestic demand due to limited local production capacity relative to consumption. Strategic partnerships with international suppliers ensure supply security. The well-developed infrastructure facilitates efficient distribution across the counattempt and to neighboring regions. Germany’s market status is defined by high-value applications and strict regulatory compliance, driving quality and innovation.

France Urea Market Analysis

France is projected to see consistent market performance and is largely driven by its status as a leading producer of cereals within the European Union. The counattempt’s extensive agricultural landscape is the primary driver of urea demand, given its status as a leading agricultural producer in the European Union. According to the French Minisattempt of Agriculture, France is the largest producer of cereals in Europe, requiring substantial nitrogen inputs to maintain high yields. Wheat, maize, and barley are major crops that rely on urea for optimal growth. The Common Agricultural Policy supports French farmers, enabling them to invest in quality fertilizers. According to Agreste, the statistical service of the French Minisattempt of Agriculture, fertilizer usage remains stable with a focus on efficiency and environmental protection. The chemical indusattempt in France also contributes to demand, particularly in the production of specialty chemicals and automotive fluids. The presence of major automotive manufacturers drives the consumption of AdBlue for diesel vehicles. France’s commitment to sustainable agriculture encourages the utilize of enhanced efficiency urea products. The counattempt has a balanced mix of domestic production and imports, ensuring supply stability. Logistics networks are well established, facilitating distribution to rural areas. The market status is characterized by strong agricultural demand and increasing emphasis on environmental compliance and sustainable farming practices.

Turkey Urea Market Analysis

Turkey is estimated to witness strong growth at a substantial CAGR over the forecast period due to its expanding industrial and farming capabilities. The counattempt’s growing agricultural sector and expanding chemical indusattempt are key drivers of urea demand. According to the Turkish Statistical Institute, agriculture remains a vital part of the economy with significant production of cereals, cotton, and fruits. The government supports the modernization of farming practices, leading to increased fertilizer utilize. Turkey is also a major producer of urea domestically, leveraging its access to natural gas resources. According to the Turkish Fertilizer Manufacturers Association, domestic production meets a large portion of local demand, with surplus exported to neighboring regions. The construction and automotive industries contribute to the demand for urea-based chemicals and automotive fluids. Turkey’s strategic location serves as a bridge between Europe and Asia, facilitating trade and logistics. The counattempt’s economic growth drives industrial activity, increasing the consumption of chemical intermediates. Environmental regulations are becoming stricter, prompting the adoption of cleaner technologies. The market status is characterized by strong domestic production capabilities and growing export potential. Turkey’s role as a regional hub enhances its importance in the European urea market dynamics. Investment in production capacity and infrastructure supports continued growth.

Italy Urea Market Analysis

Italy is expected to display a specialized market trconclude owing to the high-value crop nutrition and innovative chemical applications. The counattempt’s diverse agricultural sector and specialized chemical indusattempt drive urea consumption. According to the Italian National Institute of Statistics, agriculture is a strategic sector with high-value crops such as fruits, vereceiveables, and wine grapes requiring precise nutrient management. Urea is utilized extensively in these crops to ensure quality and yield. The chemical indusattempt in Italy utilizes urea in the production of resins and plastics for the fashion and automotive sectors. According to the Italian Chemical Indusattempt Federation, the sector is known for innovation and high-quality products. The automotive indusattempt’s demand for AdBlue supports urea consumption. Italy imports a significant portion of its urea necessarys due to limited domestic production. The counattempt’s focus on sustainable agriculture and environmental protection influences fertilizer usage patterns. Precision farming techniques are gaining traction among Italian farmers. The well-developed logistics network facilitates efficient distribution. The market status is defined by high-value agricultural applications and specialized chemical utilizes. Italy’s emphasis on quality and sustainability shapes its urea market dynamics. Collaboration with international suppliers ensures supply reliability. The integration of urea into circular economy initiatives offers future growth opportunities.

COMPETITIVE LANDSCAPE

The Europe urea market exhibits a moderately consolidated competitive landscape characterized by the presence of established international producers and regional distributors. Competition is primarily driven by cost efficiency, supply reliability,y and adherence to stringent environmental regulations rather than price alone. Major players leverage their integrated production facilities and access to cheap natural gas to achieve cost advantages. The market sees intense rivalry in meeting sustainability standards, ds with companies investing significantly in low-carbon production technologies and enhanced efficiency products. New entrants face high barriers due to capital-intensive requirements and complex regulatory compliance necessarys. Strategic collaborations and long-term supply agreements are common tactics to secure market share. The shift towards green ammonia and sustainable agriculture has intensified competition in innovation segments. Companies differentiate themselves through technological advancements and customized agronomic solutions. This dynamic environment fosters continuous improvement and innovation among participants striving to maintain competitive edges in a mature yet evolving market structure influenced by geopolitical and economic factors.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Urea Market include

- Yara International ASA

- CF Industries Holdings, Inc.

- Nutrien Ltd.

- OCI N.V.

- EuroChem Group AG

- BASF SE

- Borealis AG

- SABIC

- Grupa Azoty S.A.

- Achema AB

- Fertiberia S.A.

- SKW Piesteritz GmbH

TOP LEADING PLAYERS IN THE MARKET

- EuroChem Group AG is a leading global fertilizer producer with significant operations in Europe and Russia. The company produces substantial volumes of urea and other nitrogen fertilizers, leveraging its integrated production model. EuroChem recently focutilized on expanding its logistics infrastructure to ensure a supply to European customers despite geopolitical challenges. The company invests in sustainable agricultural solutions and digital farming tools to support efficient nutrient utilize. By enhancing its port facilities and rail networks, EuroChem strengthens its distribution capabilities across the continent. Recent initiatives include optimizing production processes to reduce environmental impact and improve energy efficiency. These actions reinforce its position as a key supplier in the European market. EuroChem continues to innovate in product formulation,s offering enhanced efficiency fertilizers that meet strict regulatory standards. Its commitment to sustainability and operational excellence drives long-term growth and customer loyalty in the region.

- Yara International ASA is a prominent Norwegian chemical company and a global leader in nitrogen-based fertilizers, including urea. The company plays a crucial role in the European market by providing high-quality nutrients and digital agricultural services. Yara recently accelerated its strategy towards green ammonia and low-carbon fertilizer production, aligning with European sustainability goals. The company invests heavily in research and development to create innovative solutions that reduce environmental footprints. Yara has established partnerships with renewable energy providers to decarbonize its production processes. Recent actions include launching new digital platforms for precision farming,g assisting farmers optimize urea application. These initiatives strengthen its market position by addressing climate modify concerns. Yara’s extensive distribution network ensures a consistent supply to European farmers. The company’s focus on sustainability and innovation positions it as a forward-considering leader in the evolving fertilizer landscape.

- K+S AG is a major German mining and chemical group with diverse fertilizer offerings, including nitrogen products. While primarily known for potas,h the company participates in the broader nutrient market serving European agriculture. K+S focutilizes on integrated nutrient management solutions combining various fertilizer types for optimal crop performance. The company recently invested in modernizing its production facilities to enhance efficiency and reduce emissions. K+S actively engages in sustainability initiatives, promoting responsible mining and chemical production practices. Recent actions include developing specialized fertilizer blconcludes that incorporate urea derivatives for specific crop necessarys. These efforts strengthen its market presence by offering tailored solutions to farmers. The company leverages its strong logistical network in Central Europe to ensure timely delivery. K+S’s commitment to environmental stewardship and product innovation supports its competitive position. By adapting to modifying regulatory requirements, K+S maintains relevance in the dynamic European fertilizer market.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe urea market predominantly focus on vertical integration to secure raw material supplies and optimize production costs. Companies invest heavily in technological upgrades to enhance energy efficiency and reduce environmental emissions, complying with strict regulatory frameworks. Strategic partnerships with downstream industries such as agriculture and automotive manufacturers ensure stable demand and long-term contracts. Participants also prioritize sustainability initiatives by adopting circular economy principles and developing green production methods. Expansion into niche applications like enhanced efficiency fertilizers and renewable energy carriers offers new growth avenues. Continuous research and development efforts aim to improve product purity and process safety. Manufacturers leverage digital technologies for predictive maintenance and operational optimization. These strategies collectively strengthen market positions by improving competitiveness, ensuring regulatory compliance, and meeting evolving customer necessarys in a dynamic industrial landscape.

MARKET SEGMENTATION

This research report on the europe urea market is segmented and sub-segmented into the following categories.

By Grade

- Fertilizer Grade

- Technical Grade

By Application

- Agriculture

- Chemical Synthesis

By Counattempt

- Russia

- Germany

- France

- Turkey

- Italy

- Rest of Europe