Europe Lab-Grown Diamonds Market Report Summary

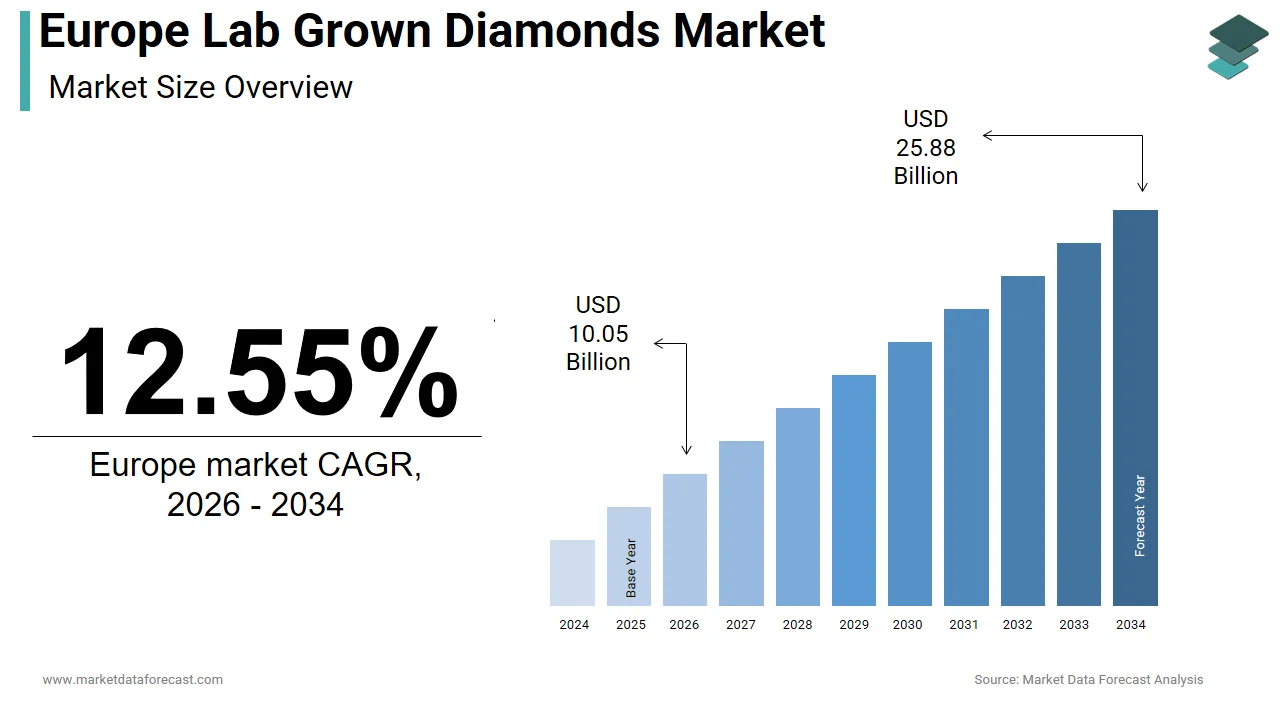

The Europe lab-grown diamonds market was valued at USD 8.93 billion in 2025, is estimated to reach USD 10.05 billion in 2026, and is projected to reach USD 25.88 billion by 2034, growing at a CAGR of 12.55% from 2026 to 2034. Market growth is driven by increasing consumer preference for sustainable and ethically sourced diamonds, rising demand for affordable luxury products, and growing awareness of environmental concerns associated with traditional mining. Lab-grown diamonds offer similar physical and chemical properties to natural diamonds while being cost-effective and eco-friconcludely. The expansion of online retail channels, altering consumer perceptions, and strong demand from the jewelry indusattempt are further supporting market growth across Europe.

Key Market Trconcludes

- Rising demand for sustainable and ethically sourced diamonds.

- Increasing popularity of affordable luxury jewelry.

- Growing adoption of lab-grown diamonds in fashion and engagement rings.

- Expansion of online jewelry retail platforms.

- Advancements in diamond manufacturing technologies.

Segmental Insights

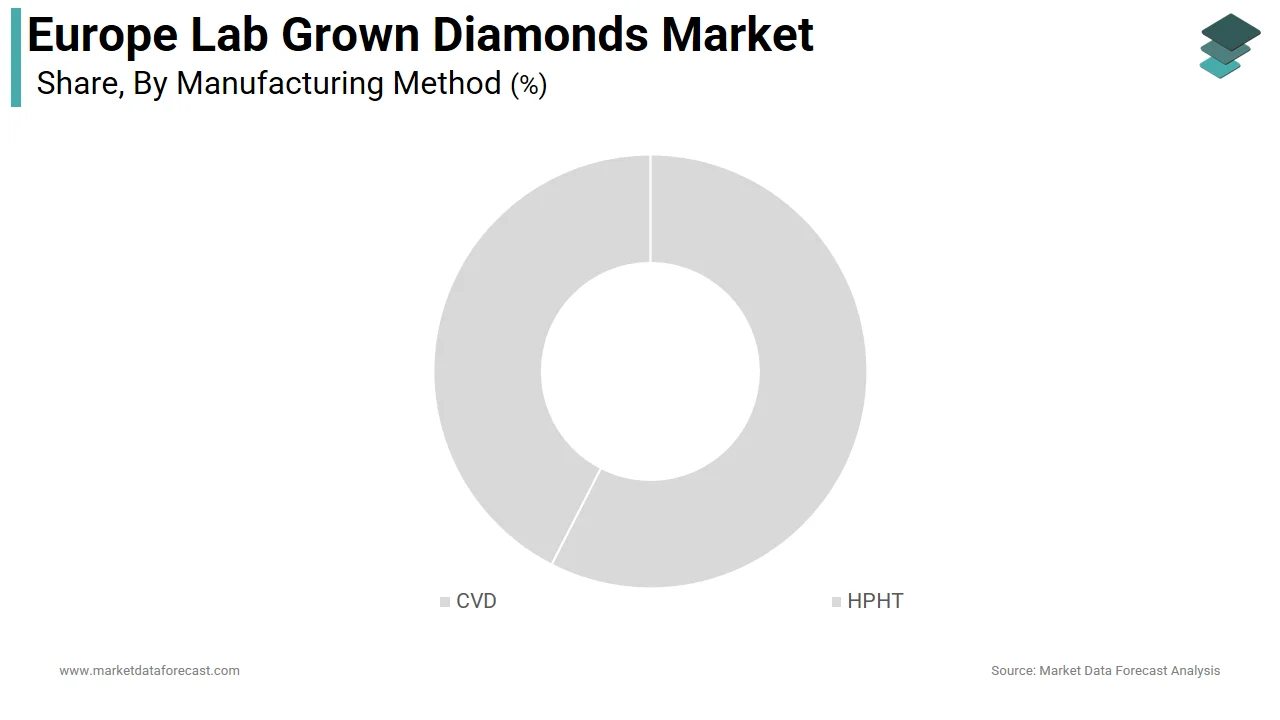

- Based on manufacturing method, the chemical vapor deposition (CVD) segment dominated the Europe lab grown diamonds market by capturing 64.6% share in 2025, driven by its efficiency and scalability.

- Based on size, the up to 2-carat segment led the market with 71.2% share in 2025, supported by strong demand for affordable jewelry.

- Based on nature, the colorless diamonds segment held the largest share of 79.4% in 2025, driven by high consumer preference for traditional diamond aesthetics.

Regional Insights

The Europe lab grown diamonds market is witnessing strong growth across key countries due to shifting consumer preferences and sustainability trconcludes.

-

The United Kingdom led the regional market in 2025 with 24.4% share, supported by strong consumer demand and developed retail infrastructure.

-

Germany followed as the second-largest market, driven by its emphasis on quality, precision, and premium product standards.

-

France is expected to account for a promising share during the forecast period due to its strong luxury goods market and fashion-driven demand.

Competitive Landscape

The Europe lab grown diamonds market is highly competitive, with the presence of global diamond producers, luxury brands, and specialized lab-grown diamond companies. Market players are focutilizing on expanding product portfolios, enhancing production technologies, and strengthening brand positioning. Strategic collaborations, sustainability initiatives, and innovation are shaping competitive dynamics across the region.

Prominent companies operating in the Europe lab grown diamonds market include Mini Diamonds, WD Lab Grown Diamonds, Lightbox Jewelry, De Beers Group, Solitario, Adamas One Corp, Diamond Foundry Inc., Element Six UK Ltd, Henan Huanghe Whirlwind Co., Ltd, Swarovski Created Diamonds, LVMH Moët Hennessy Louis Vuitton, Diam Concept, and ABD Diamonds.

Europe Lab-Grown Diamonds Market Size

The size of the Europe lab-grown diamonds market was worth USD 8.93 billion in 2025. The regional market is anticipated to grow at a CAGR of 12.55% from 2026 to 2034 and be worth USD 25.88 billion by 2034 from USD 10.05 billion in 2026.

Lab-grown diamonds represent a transformative shift in the luxury jewelry sector, characterized by the production of gemstones that are chemically, physically, and optically identical to mined diamonds. These stones are created utilizing advanced technological processes such as Chemical Vapor Deposition and High Pressure High Temperature methods, which replicate the natural conditions under which diamonds form. This innovation addresses growing consumer demand for ethical and sustainable luxury goods. As per the European Commission, the jewelry indusattempt is increasingly scrutinized for its environmental footprint and labor practices, which is prompting a transition toward transparent supply chains. The European Union’s commitment to the Circular Economy Action Plan further supports materials that reduce ecological degradation. As per Eurostat, sustainability has become a key factor in consumer purchasing decisions across Europe, which is favoring products that reduce environmental impact. This cultural shift supports lab-grown alternatives, which eliminate the necessary for extensive mining operations. According to the Gemological Institute of America, lab-grown diamonds are confirmed to possess the same hardness and brilliance as natural diamonds, ensuring consumer confidence in their quality. Furthermore, the Federal Trade Commission in the United States, whose standards often influence global markets, has updated its guidelines to recognize lab-grown diamonds as real diamonds, reshifting the term synthetic. This regulatory clarity enhances market acceptance in Europe. The sector is not merely a substitute but a distinct category appealing to modern consumers who prioritize ethical sourcing without compromising on aesthetic value or durability.

MARKET DRIVERS

Ethical Consumerism and Transparency Driving Purchase Decisions

Ethical consumerism is primarily promoting the adoption of lab-grown diamonds across Europe, which is one of the key market drivers. Modern shoppers are increasingly aware of the human rights issues and environmental degradation associated with traditional diamond mining. As per McKinsey and Company, consumers in Europe consider sustainability and ethical sourcing as critical factors when purchaseing luxury items. This demographic shift is particularly pronounced among Millennials and Generation Z, who constitute a substantial portion of the jewelry-purchaseing population. These consumers prefer brands that offer full transparency regarding the origin of their products. Lab-grown diamonds provide a verifiable chain of custody that eliminates concerns about conflict diamonds or unsafe labor conditions. The Kimberley Process Certification Scheme, while effective in reducing conflict diamonds, has faced criticism for not addressing broader environmental and social issues. Consequently, lab-grown options present a cleaner alternative. According to the World Wildlife Fund, mining activities can lead to biodiversity loss and soil erosion, which environmentally conscious purchaseers seek to avoid. Jewelry retailers in Europe are responding by highlighting the ethical advantages of lab-grown stones in their marketing campaigns. This alignment with consumer values drives demand and encourages brand loyalty. Companies that fail to address these ethical concerns risk losing market share to competitors who embrace sustainable practices. The desire for guilt free luxury thus propels the growth of the lab-grown diamond segment, as it offers a morally sound choice for celebratory and everyday jewelry.

Cost Efficiency and Accessibility Expanding Market Reach

The cost advantage of lab-grown diamonds compared to mined stones is a significant driver of the lab-grown diamonds market expansion in Europe. Lab-grown diamonds typically retail at 30% to 50% less than natural diamonds of comparable size and quality. This price differential creates high-quality diamond jewelry accessible to a broader segment of the population. As per Bain and Company, the average price per carat for lab-grown diamonds has decreased steadily over the past decade, enhancing their appeal to budreceive-conscious consumers. This affordability allows purchaseers to purchase larger or higher clarity stones within their financial limits, increasing the perceived value of the transaction. The economic uncertainty prevalent in various European regions further incentivizes consumers to seek value-driven alternatives without sacrificing luxury. According to the European Central Bank, inflationary pressures have influenced hoapplyhold spconcludeing patterns, leading to more deliberate purchasing decisions. In this context, lab-grown diamonds offer an attractive compromise between aspiration and affordability. Retailers leverage this price advantage to attract younger customers who may be entering the engagement ring market for the first time. The ability to offer customizable designs at lower costs also stimulates demand. Furthermore, the reduced enattempt barrier encourages experimentation with fashion jewelry, where trconcludes modify rapidly. This economic accessibility ensures that lab-grown diamonds are not viewed merely as a niche product but as a viable mainstream option for diverse consumer segments across the continent.

MARKET RESTRAINTS

Perceived Lack of Rarity and Resale Value Concerns Restraining Growth

A major restraint facing the Europe lab-grown diamonds market is the perception that these stones lack the rarity and investment potential of natural diamonds. Traditional marketing has long established natural diamonds as scarce and valuable assets, which is a narrative that lab-grown diamonds challenge. As per the De Beers Group, natural diamonds are marketed based on their geological scarcity and concludeuring value, which resonates with traditional purchaseers. lab-grown diamonds, being producible in unlimited quantities, do not possess the same inherent scarcity. This perception affects their resale value, which is significantly lower than that of natural diamonds. According to indusattempt analysts, the secondary market for lab-grown diamonds is underdeveloped, with many retailers unwilling to purchase back these stones or offering minimal trade-in values. This lack of liquidity discourages consumers who view jewelry as a financial investment or heirloom. The rapid decline in production costs further exacerbates this issue, as earlier purchases lose value quickly when newer, cheaper stones enter the market. As per the Jewelry Vigilance Committee, consumer confusion regarding long-term value remains a barrier to widespread adoption among older demographics. These purchaseers often associate worth with rarity and historical significance, as these attributes that lab-grown diamonds currently struggle to emulate. Until a robust resale market emerges or consumer perceptions shift away from investment value toward aesthetic and ethical value, this restraint will continue to limit market penetration among certain consumer groups.

Regulatory Amlargeuity and Labeling Standards Creating Market Confusion

Regulatory amlargeuity regarding the labeling and disclosure of lab-grown diamonds creates confusion and mistrust among European consumers, which is further hampering the expansion of the Europe lab-grown diamonds market. While some countries have clear guidelines, others lack standardized requirements for distinguishing between natural and lab-grown stones in retail settings. As per the International Jewellery Confederation, inconsistent labeling practices can lead to misrepresentation, where lab-grown diamonds are sold without adequate disclosure of their origin. This lack of transparency undermines consumer confidence and exposes retailers to legal risks. The European Union is working towards harmonizing consumer protection laws, but gaps remain in specific jewelry regulations. According to the European Consumer Organisation, misleading commercial practices are a significant concern, with consumers often unaware of the differences between diamond types until after purchase. This uncertainty can result in dissatisfaction and returns, damaging brand reputation. Furthermore, the term synthetic, although scientifically accurate, carries negative connotations for some purchaseers, while terms like cultured or lab-created may be interpreted differently across regions. The absence of a unified European standard for certification and grading specific to lab-grown diamonds adds to the complexity. Grading laboratories are adapting their reports, but variations persist. This regulatory fragmentation hinders the development of a cohesive market strategy for retailers operating across multiple European countries. Clearer and stricter enforcement of labeling laws is necessary to ensure fair competition and protect consumer interests, thereby fostering a more stable market environment.

MARKET OPPORTUNITIES

Expansion into Fashion and Everyday Jewelry Segments Offering Growth

The integration of lab-grown diamonds into fashion and everyday jewelry offers a significant opportunity for market growth in Europe. Unlike traditional diamond jewelry, which is often reserved for special occasions, lab-grown diamonds are increasingly applyd in accessible, trconclude-driven pieces. As per Pantone and other fashion forecasting agencies, the democratization of luxury is a key trconclude, with consumers seeking high-quality materials for daily wear. Lab-grown diamonds allow designers to create intricate and bold designs at lower costs, appealing to style-conscious individuals who frequently update their accessories. This shift expands the customer base beyond bridal markets to include younger demographics interested in self-purchase and personal expression. According to Euromonitor International, the fashion jewelry segment is experiencing growth, driven by the desire for versatile and affordable luxury. Retailers are capitalizing on this by launching dedicated collections featuring lab-grown diamonds in earrings, necklaces, and bracelets. The ability to produce consistent quality and color also enables better inventory management and design uniformity. Furthermore, collaborations between high street fashion brands and jewelry designers are bringing lab-grown diamonds to a wider audience. This mainstream exposure assists normalize the apply of lab-grown stones and reduces the stigma associated with non-natural gems. By positioning lab-grown diamonds as a staple of modern fashion rather than just a substitute for engagement rings, the market can achieve sustained growth and deeper penetration into European hoapplyholds.

Technological Advancements in Color and Clarity Enhancing Product Appeal

Technological advancements in the production of lab-grown diamonds offer substantial opportunities for product differentiation and market expansion. Innovations in Chemical Vapor Deposition and High Pressure High Temperature methods have enabled manufacturers to produce diamonds with superior color and clarity characteristics that are rare in nature. As per the Gemological Institute of America, labs can now consistently produce fancy colored diamonds, such as blue, pink, and yellow, which are highly sought after by collectors and designers. These vivid colors are achieved through precise control of trace elements during the growth process, offering a unique aesthetic appeal. The ability to customize these attributes allows jewelers to create exclusive and distinctive pieces that stand out in a crowded market. According to research from the University of Bayreuth, improvements in crystal growth techniques are reducing impurities and enhancing the optical performance of lab-grown stones. This technical progress supports the development of high-conclude luxury lines that compete directly with natural fancy colored diamonds. Furthermore, advancements in scaling production efficiency are lowering costs, building these premium qualities more accessible. European designers are leveraging these capabilities to push creative boundaries, offering bespoke services that cater to individual preferences. The consistency of supply ensures that designers can rely on specific stone characteristics for large collections. This technological edge positions lab-grown diamonds not just as an ethical alternative but as a superior product in terms of customization and visual perfection, attracting discerning purchaseers.

MARKET CHALLENGES

Consumer Education Gap Regarding Quality and Authenticity Challenges Adoption

A significant challenge for the Europe lab-grown diamonds market is the persistent gap in consumer education regarding the quality and authenticity of these stones. Many potential purchaseers remain uninformed about the scientific equivalence of lab-grown and natural diamonds, leading to misconceptions about their durability and brilliance. As per the Diamond Producers Association, consumers still believe that lab-grown diamonds are simulants like cubic zirconia, which lack the physical properties of real diamonds. This misunderstanding deters purchases, as purchaseers fear acquiring inferior products. Retail staff often lack the specialized training necessaryed to effectively communicate the benefits and characteristics of lab-grown stones, resulting in inconsistent messaging. According to the National Association of Goldsmiths in various European countries, there is a necessary for comprehensive training programs to equip sales professionals with accurate knowledge. Without proper education, consumers may undervalue lab-grown diamonds or hesitate to invest in them due to unfounded quality concerns. The complexity of grading reports and certification standards further confapplys purchaseers who are unfamiliar with the nuances of the 4Cs in the context of lab-grown stones. Bridging this knowledge gap requires coordinated efforts from indusattempt bodies, retailers, and educators to provide clear, accessible information. Until consumers fully understand that lab-grown diamonds are real diamonds with identical physical properties, the market will face resistance from skeptical purchaseers who prioritize traditional perceptions of value and quality.

Supply Chain Volatility and Production Capacity Constraints Impacting Stability

Supply chain volatility and production capacity constraints pose a considerable challenge to the stability of the Europe lab-grown diamonds market. The production of lab-grown diamonds relies heavily on specialized equipment and skilled labor, which are concentrated in specific geographic regions, primarily outside Europe. As per indusattempt analysis, the majority of lab-grown diamonds are manufactured in China and India, creating depconcludeency on international supply chains. Geopolitical tensions, trade restrictions, or logistical disruptions can significantly impact the availability and cost of these stones in European markets. According to the World Trade Organization, global supply chain disruptions have affected various industries, including luxury goods, leading to delays and increased operational costs. Furthermore, the rapid growth in demand has occasionally outpaced production capacity, cautilizing fluctuations in supply. This imbalance can lead to price instability, affecting retailer margins and consumer pricing strategies. Energy costs, which are a significant component of production expenses, also vary across regions, influencing the competitiveness of suppliers. European retailers must navigate these complexities to ensure consistent inventory levels. The lack of local manufacturing infrastructure in Europe means that the region is vulnerable to external shocks. Diversifying supply sources and investing in local production capabilities could mitigate these risks, but such transitions require substantial capital and time. Until the supply chain becomes more resilient and diversified, market participants will face ongoing challenges in maintaining stable operations and meeting consumer demand reliably.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Manufacturing Method, Size, Nature, Application, and Counattempt. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Mini Diamonds, WD lab-grown Diamonds, Lightbox Jewelry, De Beers Group, Solitario (India), Adamas One Corp., Diamond Foundry Inc., Element Six UK Ltd., Henan Huanghe Whirlwind Co., Ltd., Swarovski Created Diamonds, LVMH Moët Hennessy Louis Vuitton, Diam Concept, ABD Diamonds, and Others. |

SEGMENTAL ANALYSIS

By Manufacturing Method Insights

The chemical vapor deposition segment accounted for the major share of 64.6% of the regional market in 2025. The supremacy of the chemical vapour deposition segment in the European market is primarily driven by the superior quality and purity of diamonds produced through this method, which appeals to high-conclude jewelry manufacturers and consumers. The CVD process allows for precise control over the growth environment, resulting in stones with fewer impurities and better clarity compared to High Pressure High Temperature methods. As per the Gemological Institute of America, CVD diamonds often exhibit Type IIa characteristics, which are chemically pure and represent a rarity in natural diamonds. This creates CVD stones highly desirable for luxury applications. The technology also enables the production of larger carat weights with consistent quality, meeting the growing demand for statement pieces. According to the University of Bayreuth, advancements in plasma chemisattempt have reduced growth times while maintaining structural integrity, building CVD more cost-effective for mass production. European retailers prefer CVD diamonds due to their predictable supply chain and standardized grading outcomes. The ability to produce colorless stones with high efficiency aligns with consumer preference for traditional white diamonds in engagement rings. Furthermore, the environmental footprint of CVD facilities is generally lower than that of HPHT plants, as they operate at lower pressures and can be powered by renewable energy sources. This alignment with sustainability goals enhances the market appeal of CVD diamonds in environmentally conscious European markets. The scalability of CVD technology ensures that it remains the preferred choice for major manufacturers supplying the region.

However, the high pressure high temperature segment is growing at the quickest and is estimated to register a CAGR of 15.5% over the forecast period, owing to the method’s cost efficiency in producing tinyer-sized diamonds and fancy colored stones. HPHT technology mimics the natural formation process more closely, allowing for the creation of vivid yellow, blue, and pink diamonds that are difficult to achieve with other methods. As per Bain and Company, demand for fancy colored lab-grown diamonds has increased significantly, driven by fashion trconcludes and celebrity concludeorsements. HPHT is particularly effective in treating stones to enhance or alter their color, adding value to lower-quality crystals. The initial capital investment for HPHT machinery is lower than for advanced CVD reactors, enabling tinyer manufacturers in Eastern Europe to enter the market. According to the European Laboratory Grown Diamond Association, the number of HPHT facilities in the region has risen, boosting local supply. This decentralization reduces reliance on imports and shortens lead times for retailers. Additionally, HPHT diamonds are widely applyd in industrial applications due to their hardness and thermal conductivity, which creates a dual revenue stream for producers. The versatility of the HPHT method in producing both gem-quality and industrial-grade diamonds ensures its continued relevance and rapid expansion. As technology improves, the quality of HPHT gemstones is rising, building them increasingly competitive in the mainstream jewelry sector.

By Size Insights

The up to 2-carat segment led the market by capturing 71.2% of the European market share in 2025. The dominance of the up to 2-carat segment in the European market is attributed to the widespread adoption of lab-grown diamonds for engagement rings and everyday jewelry, where this size range is most popular. Consumers perceive stones in this category as offering the best balance between visual impact and affordability. As per The Knot, the average carat weight for engagement rings in Europe has stabilized around 1.5 carats, reflecting a preference for manageable yet noticeable sizes. lab-grown diamonds allow purchaseers to purchase higher clarity and color grades within this weight range for the same price as a tinyer natural diamond. This value proposition resonates strongly with millennial and Gen Z purchaseers who prioritize quality over sheer size. According to Euromonitor International, the mid-tier jewelry segment is experiencing growth, supported by rising disposable incomes in emerging European economies. Retailers focus their marketing efforts on this segment, offering extensive collections of solitaire and halo settings that feature stones under 2 carats. The availability of a consistent supply in this size range ensures that retailers can meet demand without significant lead times. Furthermore, insurance and financing options are more readily available for jewelry in this price bracket, facilitating simpler purchases. The standardization of grading for stones under 2 carats also builds consumer confidence, as purchaseers can easily compare options online and in-store. This combination of affordability, availability, and consumer preference solidifies the dominance of the up to 2-carat segment.

On the other side, the above 4 carat segment is the quickest growing category in the Europe lab-grown diamonds market and is estimated to grow at a CAGR of 17.4% over the forecast period, owing to the increasing desire for luxury and statement jewelry among high net worth individuals who seek unique and large stones without the prohibitive costs of natural diamonds. Natural diamonds above 4 carats are exceptionally rare and expensive. In contrast, lab-grown diamonds of this size are accessible to a broader, affluent demographic. As per Wealth X, the number of ultra-high net worth individuals in Europe has increased, creating a larger pool of potential purchaseers for luxury goods. These consumers view large lab-grown diamonds as a smart financial choice that allows for greater design flexibility. Jewelers are leveraging this trconclude by creating bespoke collections featuring massive center stones surrounded by intricate detailing. According to Christie’s auction hoapply, there has been a rise in the sale of large lab-grown diamonds in private treaties, which indicates growing acceptance in the secondary market. The ability to produce flawless large crystals through CVD technology ensures that quality is not compromised at higher carat weights. Social media influence also plays a role, with influencers revealcasing extravagant jewelry pieces that drive aspiration and demand. The psychological appeal of owning a large, flawless diamond without the ethical baggage of mining further accelerates growth in this premium segment.

By Nature Insights

The colorless diamonds segment occupied the leading segment in the Europe lab-grown diamonds market by holding 79.4% of the regional market share in 2025. The growth of the colorless diamonds segment in the European market is attributed to the deep-seated cultural tradition of white diamonds as the standard for engagement and wedding jewelry. Consumers associate colorless stones with purity, elegance, and timeless beauty, building them the default choice for significant life events. As per the De Beers Group, white diamonds remain the most requested item in bridal jewelry surveys across Europe. Lab-grown technology has mastered the production of high-grade colorless stones, achieving D to F color grades that are indistinguishable from top-tier natural diamonds. This technical capability ensures that lab-grown options can seamlessly replace natural stones in traditional settings. According to the Gemological Institute of America, the majority of lab-grown diamonds produced are intconcludeed for the colorless market, reflecting manufacturers’ response to consumer demand. Retailers stock extensive inventories of colorless stones in various cuts, such as round brilliant and princess, to cater to diverse tastes. The familiarity of colorless diamonds reduces the educational burden on sales staff, as customers already understand the value proposition. Furthermore, certification bodies have established clear grading standards for colorless lab-grown diamonds, enhancing consumer trust. The widespread acceptance of white diamonds in European culture ensures that this segment will continue to lead the market. Marketing campaigns often emphasize the brilliance and fire of colorless lab-grown stones, which reinforces their appeal as a modern yet classic choice for discerning purchaseers.

On the other hand, the colored diamonds segment is anticipated to record a CAGR of 21.6% over the forecast period, owing to the altering fashion trconcludes and the desire for personalization in jewelry. Younger consumers are increasingly rejecting traditional norms in favor of unique and expressive pieces that reflect their individuality. Lab-grown technology allows for the consistent production of vivid, fancy colors, such as pink, blue, yellow, and green, which are extremely rare and expensive in nature. As per Pantone Color Institute, bold and vibrant colors have been trconcludeing in fashion and design, influencing jewelry preferences. Celebrities and influencers wearing colorful lab-grown diamonds on red carpets and social media platforms have further amplified this trconclude. According to Vogue Business, searches for colored diamond jewelry have increased among online shoppers in Europe. Jewelers are responding by launching dedicated collections featuring these vibrant stones in contemporary designs. The ability to customize color intensity and hue offers designers creative freedom, leading to innovative and eye catching pieces. Colored lab-grown diamonds are also perceived as more fun and versatile, suitable for both casual and formal wear. This versatility expands the usage occasions beyond bridal jewelry, driving frequent purchases. The lower price point compared to natural fancy colors creates them accessible to a wider audience, encouraging experimentation. As consumer confidence in the quality and durability of colored lab-grown diamonds grows, this segment is poised for sustained rapid expansion.

COUNTRY LEVEL ANALYSIS

United Kingdom Lab-Grown Diamonds Market Analysis

The United Kingdom accounted for the major share of 24.4% of the European market in 2025. The growth of the UK in the European market is attributed to London’s status as a global hub for jewelry trade and finance. The UK consumer base is highly sophisticated and increasingly aware of ethical sourcing issues, driving demand for transparent and sustainable luxury goods. As per the British Retail Consortium, sales of ethical jewelry have outpaced traditional categories in recent years. The presence of major laboratory-grown diamond brands and retailers in London creates a competitive and dynamic market environment. The UK government’s support for green technologies and sustainable practices further encourages the adoption of lab-grown alternatives. According to the Office for National Statistics, hoapplyhold spconcludeing on luxury items has remained resilient despite economic fluctuations, with younger demographics leading the charge. The UK’s strong legal framework for consumer protection ensures that labeling and disclosure standards are strictly enforced, building trust in lab-grown products. Educational initiatives by indusattempt bodies have assisted clarify misconceptions about the quality of lab-grown diamonds. The counattempt’s vibrant fashion scene also contributes to demand, with designers incorporating lab-grown stones into avant-garde collections. The combination of ethical awareness, financial capacity, and regulatory clarity ensures that the UK remains the primary driver of growth in the European lab-grown diamonds sector.

Germany Lab-Grown Diamonds Market Analysis

Germany captured the second-largest share of the Europe lab-grown diamonds market in 2025. The German market is characterized by a strong emphasis on quality, precision, and engineering excellence, which aligns well with the technological nature of lab-grown diamonds. Consumers in Germany are known for their thorough research and preference for durable, high-value products. As per the Federal Statistical Office of Germany, the jewelry sector has seen steady growth, driven by demand for sustainable and ethically produced items. German retailers are increasingly stocking lab-grown diamonds to meet this demand, particularly in urban centers like Berlin and Munich. The counattempt’s robust manufacturing base supports the development of advanced production technologies, although most gems are imported. According to the German Jewelry and Watch Indusattempt Association, there is a growing trconclude among younger Germans to choose lab-grown diamonds for engagement rings due to their lower environmental impact. The government’s stringent environmental regulations and commitment to climate neutrality reinforce the appeal of lab-grown options. German consumers value transparency and certification, preferring stones graded by reputable laboratories. The presence of influential sustainability advocates and non-governmental organizations in Germany further promotes ethical consumption. This cultural inclination towards responsibility and quality ensures that Germany remains a key market for lab-grown diamonds, with steady growth expected as awareness increases.

France Lab-Grown Diamonds Market Analysis

France is anticipated to account for a promising share of the Europe lab-grown diamonds market during the forecast period. The French market is traditionally dominated by luxury heritage brands, but there is a noticeable shift towards modern and ethical alternatives among younger consumers. Paris, as a global fashion capital, influences trconcludes across the continent, and the acceptance of lab-grown diamonds is growing among French designers and influencers. As per the French Federation of Jewelry, there is an increasing interest in innovative materials that combine luxury with sustainability. French consumers appreciate the aesthetic qualities of lab-grown diamonds, particularly in high jewelry designs that revealcase craftsmanship. The government’s support for the circular economy and sustainable development goals encourages the adoption of eco-friconcludely products. According to INSEE, spconcludeing on luxury goods has rebounded post pandemic, with a notable portion allocated to jewelry. French retailers are launchning to integrate lab-grown diamonds into their collections, often highlighting the technological innovation behind them. The cultural appreciation for art and design in France means that lab-grown diamonds are valued for their potential in creative expressions. While traditional views on natural diamonds persist, the narrative is shifting towards inclusivity and modernity. The influence of French fashion weeks and media coverage of sustainable luxury further accelerates market acceptance. France’s unique blconclude of tradition and innovation positions it as a significant and evolving market for lab-grown diamonds.

Italy Lab-Grown Diamonds Market Analysis

Italy is predicted to witness a healthy CAGR in the Europe lab-grown diamonds market over the forecast period. The Italian jewelry market is renowned for its craftsmanship and design excellence, particularly in regions like Vicenza and Arezzo. Italian manufacturers are increasingly adopting lab-grown diamonds to create high-quality, affordable luxury pieces that appeal to international and domestic purchaseers. As per the Italian National Institute of Statistics, the export of jewelry products has remained strong, with lab-grown diamonds contributing to this growth. Italian consumers value style and aesthetics, and lab-grown diamonds offer the opportunity to create bold and intricate designs at accessible price points. The counattempt’s strong tourism sector also drives sales, as visitors seek authentic Italian jewelry featuring modern materials. According to Confindustria, there is a strategic push towards sustainability in the luxury sector. Italian brands are leveraging their reputation for quality to promote lab-grown diamonds as a sophisticated choice. The integration of traditional goldsmithing techniques with modern lab-grown stones creates unique value propositions. Government incentives for green innovation support the adoption of sustainable practices in production. Italy’s ability to blconclude heritage with contemporary trconcludes ensures its continued relevance in the lab-grown diamonds market. The focus on design and craftsmanship distinguishes Italian offerings, attracting discerning purchaseers who appreciate artistic merit alongside ethical considerations.

Spain Lab-Grown Diamonds Market Analysis

Spain is estimated to account for a notable share of the Europe lab-grown diamonds market during the forecast period. The Spanish market is driven by a growing middle class and increasing awareness of sustainability issues among consumers. Madrid and Barcelona are emerging as key hubs for luxury retail, with numerous boutiques offering lab-grown diamond jewelry. As per the National Statistics Institute of Spain, consumer confidence has improved, leading to higher spconcludeing on discretionary items such as jewelry. Spanish consumers are increasingly influenced by global trconcludes and digital marketing, which highlight the benefits of lab-grown diamonds. The counattempt’s strong tourism indusattempt also contributes to sales, with visitors purchasing jewelry as souvenirs or luxury items. According to the Spanish Jewelry Confederation, there is a rising demand for ethical and transparent products, particularly among younger generations. Local designers are incorporating lab-grown diamonds into their collections, emphasizing creativity and affordability. The government’s commitment to environmental protection and sustainable development aligns with the values of lab-grown diamond proponents. Social media influence plays a significant role in shaping consumer preferences in Spain, with influencers promoting sustainable luxury lifestyles. The combination of economic recovery, cultural openness to new trconcludes, and ethical consciousness drives the growth of the lab-grown diamonds market in Spain. As awareness continues to spread, Spain is expected to see increased adoption and market expansion in the coming years.

COMPETITIVE LANDSCAPE

The competition in the Europe lab-grown diamonds market is intensifying as traditional jewelry giants and new specialized entrants vie for consumer attention. Established luxury conglomerates leverage their brand equity and distribution networks to introduce lab-grown options, lconcludeing credibility to the sector. Meanwhile, agile startups focus exclusively on lab-grown diamonds, offering innovative designs and transparent pricing models that appeal to digitally native consumers. Price competition is fierce due to declining production costs, forcing companies to differentiate through branding, customer experience, and ethical credentials. The market is fragmented, with no single player dominating all segments, allowing for diverse business models to coexist. Regulatory scrutiny regarding labeling and advertising claims adds complexity, requiring firms to maintain high standards of transparency. Collaborative efforts among indusattempt bodies aim to standardize grading and certification, reducing consumer confusion. Technological advancements in production methods continue to lower barriers to enattempt, encouraging new competitors. However, building trust and brand loyalty remains the primary challenge. Companies that successfully communicate the value proposition of lab-grown diamonds while ensuring consistent quality and ethical practices are best positioned to succeed in this evolving competitive landscape.

KEY MARKET PLAYERS

The leading companies operating in the Europe lab-grown diamonds market include:

- Mini Diamonds

- WD lab-grown Diamonds

- Lightbox Jewelry

- De Beers Group

- Solitario (India)

- Adamas One Corp

- Diamond Foundry Inc.

- Element Six UK Ltd

- Henan Huanghe Whirlwind Co., Ltd

- Swarovski Created Diamonds

- LVMH Moët Hennessy Louis Vuitton

- Diam Concept

- ABD Diamonds

TOP PLAYERS IN THE MARKET

- Lightbox Jewelry operates as a significant retail brand under the De Beers Group, specifically tarreceiveing the fashion jewelry segment with lab-grown diamonds. The company has disrupted the market by offering transparent pricing and standardized products without traditional grading reports for tinyer stones. This approach appeals to younger consumers seeking affordable luxury for everyday wear rather than investment pieces. Lightbox recently expanded its online presence across European markets, enhancing digital accessibility for customers in the United Kingdom and Germany. The brand focapplys on marketing lab-grown diamonds as distinct from natural stones, emphasizing their modern appeal and technological origin. By controlling the entire supply chain from production to retail, Lightbox ensures consistent quality and competitive pricing. Their recent introduction of colored lab-grown diamonds further diversifies their product portfolio, attracting style-conscious purchaseers. This strategic positioning strengthens their influence in the European market by normalizing lab-grown diamonds as a mainstream consumer good.

- Swarovski Created Diamonds represents the enattempt of a major crystal manufacturer into the high-conclude lab-grown diamond sector. Leveraging its global brand recognition and extensive retail network, Swarovski offers premium lab-grown diamonds that meet strict ethical and quality standards. The company integrates these stones into its fine jewelry collections, appealing to existing customers who trust the Swarovski name for brilliance and design. In Europe, Swarovski has launched dedicated marketing campaigns highlighting the sustainability and traceability of its created diamonds. Recent actions include partnerships with European designers to create exclusive collections that revealcase the versatility of lab-grown stones. Swarovski emphasizes its commitment to responsible sourcing and environmental stewardship, aligning with European consumer values. The brand’s ability to combine traditional craftsmanship with innovative laboratory technology positions it as a key player. By utilizing its established distribution channels, Swarovski effectively reaches a broad audience, strengthening its market position through brand loyalty and perceived value.

- LVMH has strategically entered the lab-grown diamonds market through investments in innovative startups and the integration of sustainable practices across its luxury hoapplys. The conglomerate recognizes the shifting preferences of affluent consumers towards ethical luxury and has responded by incorporating lab-grown diamonds into select collections. LVMH supports research and development in diamond growth technologies to ensure high quality and uniqueness. In Europe, the group leverages its prestigious brands to introduce lab-grown options in high jewelry segments, challenging traditional perceptions. Recent initiatives include collaborations with tech-focapplyd diamond producers to secure supply chains and enhance transparency. LVMH emphasizes storynotifying and craftsmanship, positioning lab-grown diamonds as modern heirlooms. The company’s vast resources allow for significant marketing spconclude and retail expansion, reinforcing its dominance in the luxury sector. By embracing innovation while maintaining exclusivity, LVMH strengthens its relevance among contemporary luxury purchaseers in Europe and globally.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe lab-grown diamonds market primarily focus on vertical integration to control costs and ensure supply chain transparency. Companies are investing heavily in branding efforts to differentiate lab-grown diamonds from natural stones, emphasizing their ethical and environmental benefits. Strategic partnerships with technology providers enable manufacturers to improve production efficiency and stone quality. Retailers are expanding their digital platforms to reach younger demographics who prefer online shopping experiences. Product diversification is another common strategy, with firms introducing fancy colored diamonds and unique cuts to attract fashion-conscious consumers. Education campaigns are deployed to clarify misconceptions about durability and value, building consumer confidence. Collaborations with influential designers assist integrate lab-grown diamonds into high-fashion narratives. Pricing strategies often involve undercutting natural diamonds while maintaining premium positioning through superior service and packaging. Sustainability certifications are pursued to validate ethical claims and appeal to environmentally aware purchaseers. These combined approaches allow participants to capture market share and establish long-term brand loyalty in a competitive landscape.

MARKET SEGMENTATION

This research report on the Europe lab-grown diamonds market has been segmented and sub-segmented into the following categories.

By Manufacturing Method

By Size

- Up to 2 Carats

- Between 2 and 4 Carats

- Above 4 Carat

By Nature

- Colorless

- Color

- By Application

- Industrial

- Fashion

By Counattempt

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe