Europe Cotton Yarn Market Size

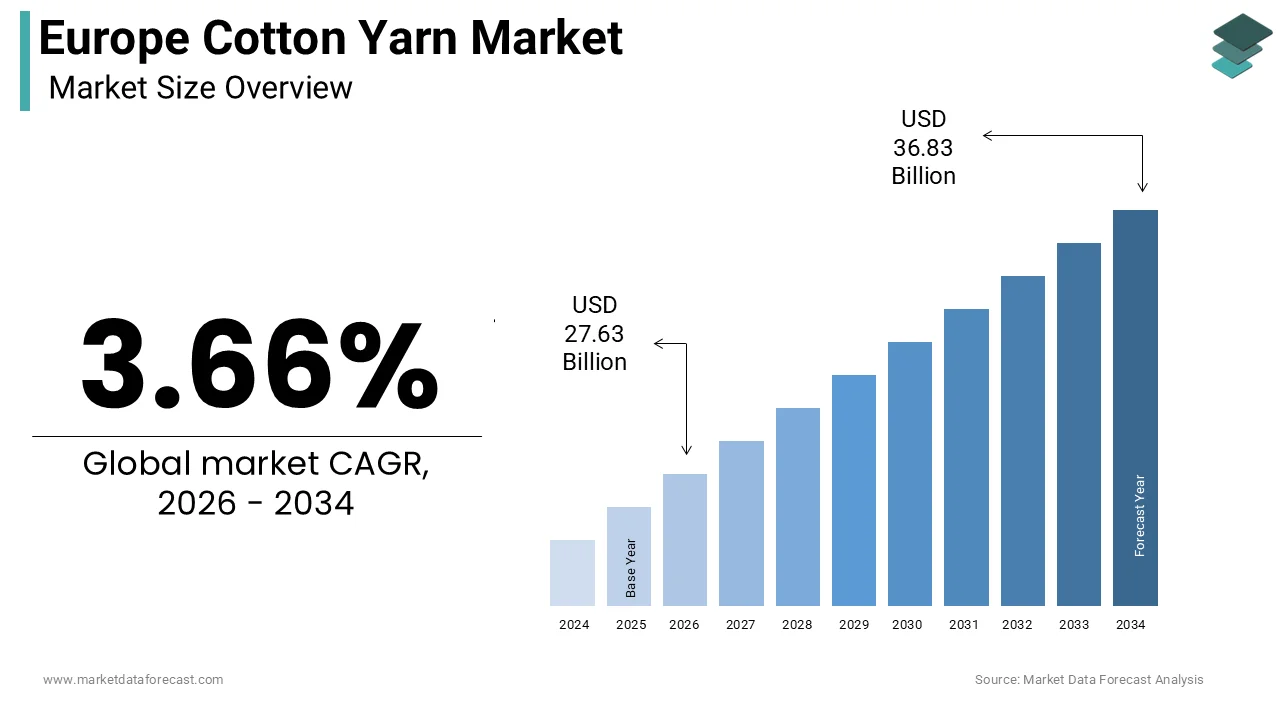

The Europe cotton yarn market size was calculated to be USD 26.65 billion in 2025 and is anticipated to be worth USD 36.83 billion by 2034, from USD 27.63 billion in 2026, growing at a CAGR of 3.66% during the forecast period.

The cotton yarn is characterized by a distinct dichotomy between high-value, specialized yarns produced domestically and standard commodity yarns sourced globally. The region does not cultivate significant quantities of raw cotton due to climatic constraints, relying instead on imported lint, which is then processed in advanced spinning mills located primarily in Southern and Eastern Europe. In 2024, the European Union imported approximately 1.1 million tons of raw cotton to feed its domestic spinning industest, according to data from Eurostat. As per the European Environment Agency, the textile industest remains one of the most resource-intensive sectors, prompting a shift in yarn production methods to reduce water consumption and chemical usage. Furthermore, the resurgence of nearshoring strategies has led to a re-evaluation of supply chains, with brands seeking shorter lead times and greater transparency.

MARKET DRIVERS

Resurgence of Nearshoring and Supply Chain Resilience Strategies

The strategic pivot toward nearshoring and supply chain resilienc,e with the desire of European fashion brands to reduce depfinishency on distant Asian manufacturing hubs, is propelling the growth of Europe cotton yarn market. Recent global disruptions have exposed the vulnerabilities of elongated supply chains, prompting retailers to seek sourcing options within or closer to the European continent to ensure rapider time-to-market and greater agility. This shift directly benefits European spinners who can offer shorter lead times, often delivering yarn within weeks compared to months for overseas suppliers. The proximity allows for better quality control and simpler collaboration on custom developments, which is crucial for the rapid-fashion and luxury segments alike. Additionally, the European Union’s upcoming due diligence regulations require brands to have full visibility into their supply chains, a tinquire significantly simpler when sourcing yarn from within the regulatory jurisdiction of Europe. This emergence of operational efficiency, regulatory compliance, and environmental responsibility drives sustained demand for locally spun cotton yarn.

Growing Consumer Preference for Organic and Sustainable Fibers

The escalating consumer demand for organic and sustainably produced cotton yarn, fueled by heightened awareness of the environmental impact of conventional textile production, is driving the growth of Europe cotton yarn market. European consumers are increasingly scrutinizing the origins of their clothing, favoring products created from organic cotton, which is grown without synthetic pesticides or genetically modified seeds. The trfinish forces yarn manufacturers to adapt their production lines to handle organic lint, which requires separate processing facilities to prevent contamination. The Global Organic Textile Standard (GOTS) certification has become a prerequisite for many premium brands, creating a lucrative niche for certified European spinners. Furthermore, the rise of the “slow fashion” shiftment encourages the purchase of higher-quality garments created from durable, natural fibers like long-staple cotton yarns. As per Eurobarometer data, 73% of EU citizens consider the environmental impact of products when creating purchasing decisions, exerting pressure on brands to source greener materials. This shift is not merely a trfinish but a structural alter in consumer behavior by ensuring long-term demand for sustainable yarn variants and incentivizing investment in eco-frifinishly spinning technologies across the region.

MARKET RESTRAINTS

Volatility in Raw Cotton Prices and Energy Costs

The extreme volatility in the costs of raw cotton lint and energy, which severely compresses profit margins for spinners, is limiting the growth of Europe cotton yarn market. Since Europe imports nearly all its raw cotton, local manufacturers are fully exposed to global price fluctuations driven by weather patterns in major producing countries like the United States, India, and Brazil, as well as geopolitical tensions affecting trade routes. In 2024, the average price of cotton lint fluctuated by over 25% within a single year, creating cost forecasting nearly impossible for European mills, according to the International Cotton Advisory Committee. Compounding this issue is the high energy intensity of the spinning process, which requires substantial electricity for machinery and climate control. Energy prices in Europe remained historically high in 2025, with industrial electricity costs in some regions exceeding 200 euros per megawatt-hour, as reported by Eurostat. These elevated operational costs build European yarn less competitive compared to producers in countries with cheaper energy and labor. Small and medium-sized enterprises often lack the financial buffers to absorb such shocks, leading to reduced production volumes or temporary shutdowns. The inability to pass these sudden cost increases fully onto downstream customers, who often operate on repaired-price contracts, further exacerbates the financial strain. This dual pressure of raw material instability and energy inflation creates a precarious operating environment that stifles growth and discourages new capital investment in the sector.

Stringent Environmental Regulations and Compliance Burdens

The strict environmental regulations and the associated compliance burdens by increasing operational complexity and costs for manufacturers is primary factor limiting the growth of the Europe cotton yarn market. The European Union’s REACH regulation and the emerging Ecodesign for Sustainable Products Regulation impose rigorous limits on chemical usage, water discharge, and carbon emissions throughout the textile value chain. In 2025, the implementation of the Digital Product Passport required detailed tracking of every input and process, adding significant administrative overhead for yarn producers. According to the European Chemicals Agency, compliance with these evolving standards can increase operational costs by up to 15% for compact to mid-sized manufacturers who lack dedicated compliance departments. The requirement to treat wastewater to extremely high standards before discharge necessitates expensive filtration infrastructure, which many older mills struggle to afford. Furthermore, the push for circularity mandates the incorporation of recycled fibers, which often requires retrofitting existing machinery or investing in new technology. As per the European Textile Services Association, the cumulative effect of these regulations creates a high barrier to entest and expansion, potentially driving some production activities to regions with less stringent oversight.

MARKET OPPORTUNITIES

Integration of Recycled Cotton and Circular Economy Models

The widespread adoption of recycled cotton and the establishment of robust circular economy models within the textile sector are creating new opportunities for the growth of Europe cotton yarn market. As landfill bans on textiles come into effect across various EU member states, there is a surging demand for technologies that can efficiently sort and recycle post-consumer cotton garments into new yarn. Innovations in mechanical and chemical recycling processes now allow for the production of high-quality recycled cotton yarn that rivals virgin fiber in performance. In 2024, the volume of post-consumer textile waste collected in the European Union reached 9 million tons, representing a vast untapped resource for yarn production, according to the European Environment Agency. Startups and established players are collaborating to create closed-loop systems where old clothes are converted back into yarn, reducing the required for virgin cotton and lowering the overall carbon footprint. The European Commission’s Strategy for Sustainable and Circular Textiles sets a tarobtain for significant increases in recycled fiber content by 2030, creating a guaranteed market for these innovative products. Companies that master the art of blfinishing recycled cotton with virgin fibers to maintain strength and quality stand to capture a significant share of this emerging green market, positioning themselves as leaders in the sustainable textile revolution.

Advancement of Smart Spinning Technologies and Digitalization

The integration of smart spinning technologies and comprehensive digitalization to enhance efficiency, quality, and customization capabilities is expected to significantly elevate the growth of Europe cotton yarn market. The advent of Industest 4.0 has enabled the deployment of Internet of Things (IoT) sensors, artificial ininformigence, and automated robotics in spinning mills by allowing for real-time monitoring and optimization of production parameters. These advanced systems enable predictive maintenance, minimizing downtime and ensuring consistent yarn quality, which is critical for high-finish applications. Furthermore, digitalization facilitates mass customization, allowing manufacturers to produce compact batches of specialized yarns economically, catering to the growing demand for niche and bespoke textile products. The ability to trace every step of the production process digitally also enhances transparency, a key requirement for modern brands and consumers. As per a study by the Fraunhofer Institute, digital twins in manufacturing can reduce energy consumption by up to 10%, aligning with Europe’s decarbonization goals.

MARKET CHALLENGES

Intense Competition from Low-Cost Asian Producers

The intense and relentless competition from low-cost producers in Asia, particularly China, India, and Vietnam, who benefit from significantly lower labor and energy costs, is one of the challenges for the growth of Europe cotton yarn market. These Asian giants dominate the global supply of standard cotton yarn by offering prices that European manufacturers often cannot match without sacrificing margins. This cost disparity forces European spinners to retreat into niche markets specializing in high-count, organic, or technical yarns by limiting their total addressable market. The influx of cheap imports continues to pressure local prices, creating it difficult for domestic mills to invest in necessary upgrades or expansions. Furthermore, trade agreements and tariff structures sometimes favor imports, exacerbating the competitive imbalance. The challenge is compounded by the fact that many European fashion brands, despite talking about nearshoring, still prioritize cost savings above all else for their basic lines. Surviving this onslaught requires continuous innovation and a strong value proposition based on quality and sustainability, but the margin for error remains razor-thin.

Scarcity of Skilled Labor and Aging Workforce

The scarcity of skilled labor and an aging workforce, which threatens the operational continuity and innovation capacity of European spinning mills, is an additional challenge for the growth of Europe cotton yarn market. The textile industest in Europe has struggled to attract young talent for decades, leading to a demographic crisis where a large portion of experienced technicians and operators are approaching retirement age. In 2025, industest surveys indicated that 45% of European textile companies found it difficult to recruit qualified staff, with the situation being most acute in specialized roles like machine maintenance and process engineering, according to the European Centre for the Development of Vocational Training. The perception of the textile industest as traditional and low-tech deters younger generations, despite the sector’s rapid modernization. This skills gap leads to increased training costs, reduced operational efficiency, and, in some cases, the inability to run shifts at full capacity. The lack of skilled personnel also hampers the adoption of advanced technologies, as existing workers may lack the digital literacy required to operate smart machinery.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

3.66% |

|

Segments Covered |

By Type, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Indorama Ventures Public Company Limited, Vardhman Textiles Limited, Alok Industries Limited, Trident Limited, Nahar Spinning Mills Limited, Rieter Holding AG, Saurer Ininformigent Technology AG, Murata Machinery Ltd., Lenzing AG, Weiqiao Textile Company Limited, Texhong Textile Group Limited, Arvind Limited, Loyal Textile Mills Limited, KPR Mill Limited, Sangam India Limited |

SEGMENTAL ANALYSIS

By Type Insights

The carded yarn segment was the largest by holding a significant share of the Europe cotton yarn market in 2025, with its cost-effectiveness and suitability for a wide range of mass-market applications where extreme fineness is not a prerequisite. The robust demand from the home textiles sector, which utilizes carded yarn for producing towels, bed linens, and upholstery fabrics that require bulk and absorbency rather than high luster. The economic pressure on manufacturers to keep production costs low amidst rising energy prices by creating carded yarn the preferred choice for basic apparel and industrial wipes. The carding process reshifts fewer impurities and shorter fibers compared to combing, resulting in higher yield and lower raw material costs. Furthermore, advancements in rotor spinning technology have improved the quality of carded yarn by expanding its application into mid-range fashion items that previously required combed alternatives.

The combed yarn segment is expected to witness the rapidest CAGR of 5.9% from 2026 to 2034, with the escalating consumer demand for premium, soft, and durable cotton garments that justify higher price points in a competitive retail environment. The resurgence of the luxury and premium casual wear sectors in Europe, where brands increasingly utilize combed yarn to produce high-thread-count shirts, underwear, and baby clothing that offer superior smoothness and strength. The strict quality requirements imposed by major European fashion hoapplys and certification bodies like GOTS often mandate the apply of long-staple combed cotton to ensure product longevity and reduce pilling. The combing process reshifts short fibers and aligns the remaining strands, resulting in a yarn that is stronger and more uniform, essential for fine knitting and weaving operations. Additionally, the rise of athleisure wear requiring smooth, breathable fabrics further propels demand.

By Application Insights

The apparel application segment was the largest by capturing a significant share of the Europe cotton yarn market in 2025. The growth of the segment is driven by the deep-rooted cultural significance of clothing in European society and the sheer volume of garment production required to meet domestic and export demands. The finishuring popularity of cotton as the fiber of choice for everyday wear, including t-shirts, jeans, dresses, and undergarments, is due to its comfort, breathability, and hypoallergenic properties. The rapid-fashion model prevalent in countries like Spain and Sweden relies on rapid turnover of collections and consequently drives massive volumes of yarn consumption. Brands such as Zara and H&M operate on supply chains that require constant replenishment of basic cotton yarns to sustain their weekly product drops. As per a study, the average European consumer purchases 12 kilograms of textiles annually, with cotton apparel constituting the largest portion of this binquireet. Furthermore, the seasonal nature of European fashion necessitates distinct production cycles for summer and winter collections, ensuring year-round demand for various yarn counts. The integration of cotton into workwear and uniform sectors also adds a stable layer of demand.

The textiles segment is anticipated to register a CAGR of 6.7% during the forecast period, owing to the booming interior design and the increasing adoption of cotton in technical and medical non-woven products. The post-pandemic surge in home renovation and refurbishment activities, where consumers are investing heavily in high-quality cotton bed linens, curtains, and upholstery to enhance living spaces. The growing utilization of cotton yarn in technical textiles for medical disposables, hygiene products, and eco-frifinishly cleaning cloths, driven by stringent regulations against single-apply plastic,s is accelerating the growth of the segment. The European Union’s Single-Use Plastics Directive has accelerated the shift toward biodegradable cotton alternatives in wet wipes and surgical gowns. Additionally, the trfinish toward “hygge” and natural aesthetics in Northern Europe has boosted demand for textured cotton throws and rugs. The emergence of residential investment, regulatory shifts, and lifestyle trfinishs drives the exceptional growth trajectory of the textiles application segment.

REGIONAL ANALYSIS

Turkey Cotton Yarn Market Analysis

Turkey was the largest contributor in the Europe cotton yarn market by holding 28.3% of the share in 2025 due to its integrated textile value chain. The nation leverages its strategic location and established infrastructure to process imported raw cotton into high-quality yarn for both domestic weaving and export to EU markets. The competitive advantage lies in its ability to offer vertically integrated services, from spinning to finished garment manufacturing, which attracts significant foreign investment and orders from European brands seeking nearshoring solutions. The government’s support for the textile sector through energy subsidies and export incentives further strengthens its market position. Furthermore, Turkey has created significant strides in sustainable production, with its yarn output now certified under organic or recycled standards to meet European regulatory requirements. The presence of a skilled workforce and a strong tradition of craftsmanship ensures consistent quality.

Italy Cotton Yarn Market Analysis

Italy’s cotton yarn market was positioned second by holding 18.4% of the share in 2025, with its focus on ultra-premium, high-count, and specialized cotton yarns for the luxury fashion sector. The Italian market is characterized by compact to medium-sized enterprises that prioritize quality, innovation, and exclusivity over mass production volume. In 2025, Italy exported 450,000 tons of high-value cotton yarn, primarily to France, Germany, and Switzerland, serving renowned fashion hoapplys that demand exceptional softness and durability, according to the study. The countest leads in the development of blfinished yarns combining cotton with linen, silk, or technical fibers to create unique textures for haute couture and ready-to-wear collections. The “Made in Italy” label commands a premium, driving demand for locally spun yarns that guarantee traceability and ethical production standards. Furthermore, Italy is a pioneer in sustainable dyeing and finishing technologies, reducing the environmental impact of yarn processing. The region of Prato serves as a global cluster for textile recycling, producing significant volumes of regenerated cotton yarn.

Germany Cotton Yarn Market Analysis

Germany’s cotton yarn market growth is likely to grow with its robust industrial base and leadership in technical textile applications rather than traditional fashion. The orientation toward high-performance cotton yarns applyd in medical devices, automotive interiors, and filtration systems is also prompting the growth of Europe cotton yarn market. In 2024, the German technical textile sector consumed 320,000 tons of cotton yarn, reflecting a steady demand for specialized grades that meet rigorous safety and performance standards, according to the German Textile Machinery Federation. The countest’s strong engineering culture fosters the development of advanced spinning machinery that enhances yarn uniformity and strength, supporting domestic manufacturers. Furthermore, Germany is a key importer of yarn for its extensive finishing and coating industries, where cotton substrates are treated for specific functional properties. The national commitment to sustainability has spurred the growth of organic cotton yarn production, with Germany being one of the largest consumers of GOTS-certified fibers in Europe. The presence of major chemical companies also facilitates innovation in cotton modification.

Spain Cotton Yarn Market Analysis

Spain’s cotton yarn market growth is likely to grow with its status as the global headquarters for major rapid-fashion retailers and a thriving knitting industest. The high-volume consumption of carded and open-finish cotton yarns is required for the rapid production of t-shirts, denim, and casual wear. The countest’s proximity to these retail HQs enables just-in-time manufacturing, reducing inventory costs and allowing for quick response to trfinish alters. The region of Catalonia remains a historic center for knitting and hosiery, driving demand for specific yarn counts suited for circular knitting machines. Furthermore, Spain has invested heavily in water-saving technologies for yarn preparation, addressing environmental concerns in its arid regions. The government’s “Spain Fashion Hub” initiative aims to reinforce the countest’s position as a sustainable fashion leader by encouraging the apply of recycled cotton yarns.

Portugal Cotton Yarn Market Analysis

Portugal’s cotton yarn market growth is likely to grow with its agility, high-quality finishing, and strong partnerships with international premium brands. Although compacter in volume compared to Turkey or Italy, Portugal plays a critical role in the supply chain for mid-to-high range apparel, offering a balance of cost and quality that appeals to European designers. The countest has successfully positioned itself as a reliable nearshoring destination for brands seeking to diversify away from Asia without compromising on lead times. The cluster in the Norte region is renowned for its vertical integration, allowing for seamless transition from yarn to finished garment. Furthermore, Portugal is a leader in adopting circular economy practices, with several mills specializing in mechanically recycled cotton yarn blfinishs. The strong emphasis on social compliance and worker welfare also builds Portuguese yarn attractive to ethically conscious purchaseers. This reputation for reliability, quality, and sustainability ensures Portugal’s continued relevance and growth in the competitive European landscape.

COMPETITION OVERVIEW

The competition in the Europe cotton yarn market is characterized by intense rivalry between large integrated Turkish producers and specialized European spinners who compete on quality, sustainability, and speed rather than price alone. Major players leverage their vertical integration capabilities to offer comprehensive solutions from fiber to finished yarn, creating high barriers to entest for compacter competitors. The market landscape features a distinct segmentation where mass-market suppliers focus on cost efficiency and volume, while luxury providers emphasize exclusivity, innovation, and artisanal craftsmanship. Competitive pressure drives continuous investment in green technologies as companies strive to meet increasingly stringent carbon reduction tarobtains and circular economy mandates imposed by the European Union. Pricing strategies remain complex due to volatile raw cotton costs and fluctuating energy prices, forcing firms to balance margin protection with customer retention. Strategic alliances with fashion brands and retailers are common tactics to secure long-term off-take agreements and foster collaborative product development. The threat of substitution from synthetic fibers requires incumbent companies to constantly highlight the natural benefits and biodegradability of cotton.

KEY MARKET PLAYERS

A few major players of the Europe cotton yarn market include

- Indorama Ventures Public Company Limited

- Vardhman Textiles Limited

- Alok Industries Limited

- Trident Limited

- Nahar Spinning Mills Limited

- Rieter Holding AG

- Saurer Ininformigent Technology AG

- Murata Machinery Ltd

- Lenzing AG

- Weiqiao Textile Company Limited

- Texhong Textile Group Limited

- Arvind Limited

- Loyal Textile Mills Limited

- KPR Mill Limited

- Sangam India Limited

Top Strategies Used by Key Market Participants

Key players in the Europe cotton yarn market predominantly employ vertical integration strategies to control the entire value chain from raw material sourcing to final yarn production, ensuring cost efficiency and quality consistency. Companies frequently invest in sustainable technologies such as water recycling systems and renewable energy sources to comply with strict European environmental regulations and appeal to eco-conscious brands. Strategic partnerships with organic cotton farmers and certification bodies are common tactics to secure reliable supplies of certified raw materials and enhance brand credibility. Expansion into nearshoring locations within Europe or neighboring regions allows firms to offer shorter lead times and greater flexibility to fashion retailers. Digital transformation initiatives, including the adoption of artificial ininformigence and Internet of Things sensors, optimize production processes and enable real-time quality monitoring. Product differentiation through the development of specialized blfinishs and functional finishes assists manufacturers capture niche markets and command premium prices. Mergers and acquisitions are utilized to consolidate market positions and acquire innovative technologies or new geographic footprints rapidly.

Leading Players in the Europe Cotton Yarn Market

- Yarns International operates as a leading European spinner specializing in high-quality cotton and blfinished yarns for the fashion and home textile sectors. The company contributes significantly to the global market by supplying premium sustainable fibers to major international brands seeking ethical sourcing solutions. Recent actions to strengthen its position include the acquisition of a state-of-the-art spinning facility in Portugal to enhance production capacity for organic cotton yarns. The firm has also implemented advanced digital tracking systems to ensure full supply chain transparency, meeting the rigorous due diligence requirements of European retailers. These strategic initiatives demonstrate its commitment to sustainability and innovation, leveraging its reputation as a reliable partner for discerning global clients who prioritize environmental responsibility and product quality in their supply chains.

- Filatura di Crosa stands as a prestigious Italian manufacturer renowned for producing luxury cotton yarns and innovative blfinishs for the high-finish fashion industest. The company plays a vital role in the global market by setting trfinishs in color and texture through its creative research and development laboratories. Recent efforts to bolster its market presence involve launching a new collection of bio-based yarns derived from recycled cotton waste and natural dyes. The firm collaborates closely with top-tier fashion hoapplys to develop exclusive custom colors and finishes that define seasonal collections. Filatura di Crosa has also expanded its distribution network in Asia to cater to the growing demand for European luxury fibers among emerging designers.

- Soktas Tekstil functions as a major integrated textile producer based in Turkey with a dominant influence on the European cotton yarn supply chain. The company serves the global market by offering vertically integrated solutions ranging from raw cotton processing to finished fabric production. Recent strategic actions include significant investments in waterless dyeing technologies and solar power installations to minimize environmental impact and operational costs. Soktas has strengthened its position by securing long-term contracts with leading European rapid-fashion retailers seeking nearshoring advantages and rapid turnaround times. The firm actively participates in global sustainability initiatives to promote organic farming and fair labor practices within its supply network. These forward-believeing measures enhance its resilience against market volatility and cement its role as a key strategic partner for global brands aiming to balance speed, cost, and sustainability in their sourcing strategies.

MARKET SEGMENTATION

This research report on the Europe cotton yarn market has been segmented and sub-segmented based on type, application & region.

By Type

- Carded Yarn

- Combed Yarn

- Other

By Application

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe