Europe Carbon Offsetting Market Report Summary

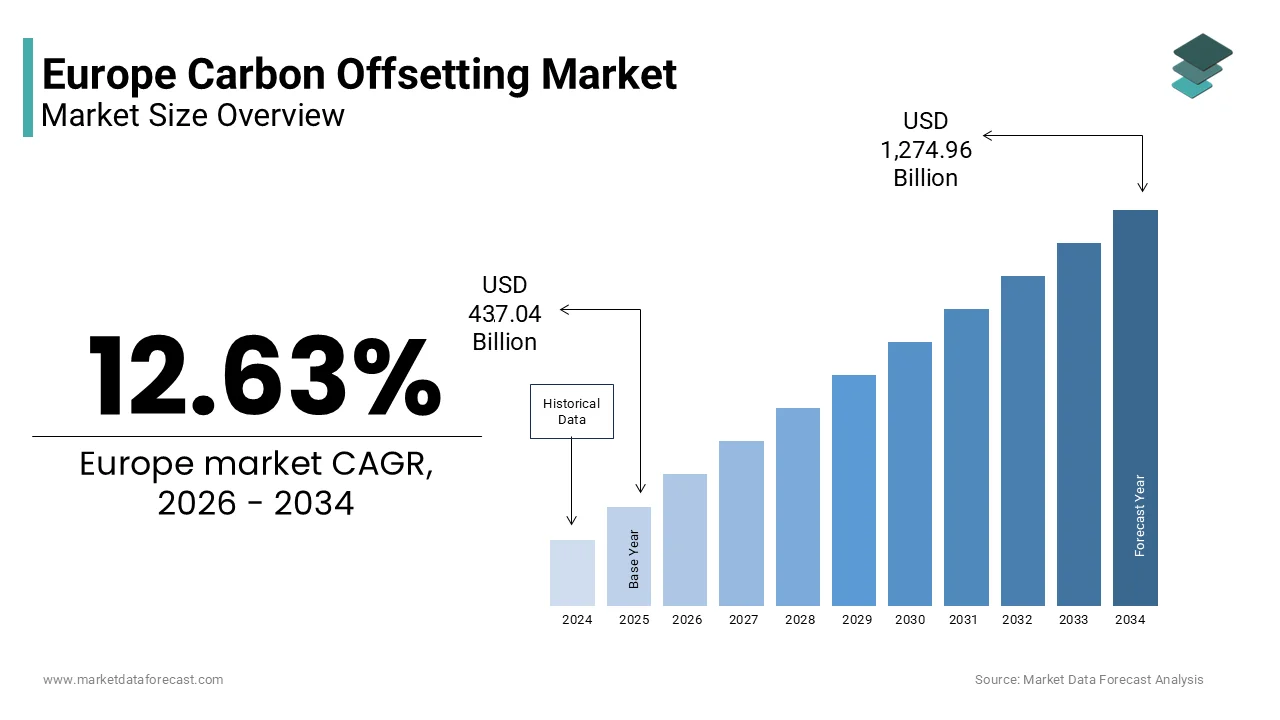

The Europe carbon offsetting market was valued at USD 437.04 billion in 2025, is estimated to reach USD 492.27 billion in 2026, and is projected to reach USD 1,274.96 billion by 2034, growing at a CAGR of 12.63% during the forecast period. Market growth is driven by stringent environmental regulations, increasing corporate commitments to carbon neutrality, and rising adoption of sustainability practices across industries. The expansion of carbon trading systems, along with growing awareness of climate alter mitigation, is further accelerating market demand. In addition, increasing investments in renewable energy and carbon reduction initiatives are supporting strong market expansion across Europe.

Key Market Trconcludes

- Rising corporate commitments toward net zero emissions are driving demand for carbon offsetting solutions.

- Increasing implementation of regulatory frameworks and carbon pricing mechanisms is supporting market growth.

- Growing investments in renewable energy and sustainability projects are boosting offset demand.

- Expansion of voluntary and compliance carbon markets is enhancing market participation.

- Technological advancements in carbon tracking and verification are improving transparency and efficiency.

Segmental Insights

- Based on type, the compliance market was the largest and held 84.9% of the Europe carbon offsetting market share in 2025. This dominance is attributed to strict regulatory requirements and mandatory emission reduction tarreceives across industries.

- Based on project type, the avoidance and reduction projects segment accounted for 71.1% of the Europe carbon offsetting market share in 2025. The segment’s growth is driven by large scale initiatives focutilized on emission reduction, energy efficiency, and sustainable practices.

- Based on conclude utilizer, the renewable energy segment dominated with 33.6% of the Europe carbon offsetting market share in 2025, supported by increasing investments in clean energy projects such as wind, solar, and hydro power.

Regional Insights

- The Europe carbon offsetting market is experiencing rapid growth across major countries, supported by strong policy frameworks and sustainability goals.

- Germany was the largest contributor, accounting for 21.6% of the Europe carbon offsetting market share in 2025, driven by ambitious climate tarreceives, advanced renewable energy infrastructure, and active participation in carbon trading mechanisms.

Competitive Landscape

The Europe carbon offsetting market is highly competitive, with key players focapplying on project development, carbon credit verification, and strategic partnerships to strengthen their market position. Companies are investing in renewable energy projects, reforestation initiatives, and digital platforms for carbon tracking and reporting. Prominent players in the Europe carbon offsetting market include 3Degrees Group Inc, Carbon Care Asia Ltd, Shell plc, TotalEnergies SE, BP plc, CarbonBetter, ClearSky Climate Solutions, EKI Energy Services Ltd, Finite Carbon, NativeEnergy, and South Pole Group.

Europe Carbon Offsetting Market Size

The Europe carbon offsetting market size was valued at USD 437.04 billion in 2025 and is projected to reach USD 1,274.96 billion by 2034 from USD 492.27 billion in 2026, growing at a CAGR of 12.63%.

Carbon offsetting is a complex financial and environmental mechanism wherein entities compensate for their greenhoutilize gas emissions by funding equivalent reductions elsewhere. This system operates as a critical bridge toward net zero tarreceives while direct decarbonization remains technologically or economically unfeasible for certain sectors. The European Union has established a rigorous regulatory framework that distinguishes between compliance markets and voluntary initiatives. As per the European Environment Agency, the European Union achieved a notable reduction in greenhoutilize gas emissions compared to 1990 levels by 2022, which is indicating the aggressive climate policy landscape that drives offsetting demand. Furthermore, the Intergovernmental Panel on Climate Change states that limiting global warming to 1.5 degrees Celsius requires immediate and deep emissions reductions across all sectors. In this context, carbon credits serve as a transitional tool rather than a permanent solution. The integrity of these offsets is paramount, with increasing scrutiny on additionality and permanence. According to Eurostat, renewable energy sources accounted for a significant portion of gross final energy consumption in the European Union in 2022, influencing the types of projects eligible for offsetting. The market evolves from simple avoidance projects to removal technologies, reflecting a maturation in climate strategy. Stakeholders now prioritize high quality credits that deliver co benefits such as biodiversity conservation and social upliftment, ensuring that financial flows contribute meaningfully to sustainable development goals alongside climate mitigation.

MARKET DRIVERS

Stringent Corporate Net Zero Commitments Driving Voluntary Demand

Corporate ambition is propelling the expansion of the carbon offsetting market in Europe. Multinational corporations and compact enterprises alike are adopting science based tarreceives to align their operations with the Paris Agreement goals. As per the Science Based Tarreceives initiative, thousands of companies globally have committed to setting science based tarreceives, with a significant portion headquartered in Europe. These entities recognize that internal abatement measures alone cannot eliminate all residual emissions, particularly in hard to abate sectors such as aviation and heavy indusattempt. Consequently, they turn to high quality carbon credits to neutralize their remaining footprint. According to the European Commission, a large majority of the hugegest companies in Europe now publish sustainability reports, which is reflecting an increased transparency requirement. This corporate diligence creates a robust demand for verified offsets. For instance, the travel and logistics sectors face intense pressure from consumers and investors to demonstrate climate responsibility. According to Deloitte, a majority of European consumers consider sustainability when building purchasing decisions. This consumer sentiment compels brands to invest in credible offsetting projects to maintain market share and brand loyalty. Companies are increasingly scrutinizing the quality of credits, which is preferring those with strong co benefits such as community development and biodiversity protection and thereby driving up the value and volume of premium offset projects.

Regulatory Frameworks and Compliance Mechanisms Enhancing Market Structure

The regulatory environment in Europe provides a foundational structure that legitimizes and stimulates the carbon offsetting market in Europe. The European Union Emissions Trading System stands as the world’s first major carbon market and remains the largest. As per the European Commission, the EU ETS covers a significant portion of the EU’s greenhoutilize gas emissions. Recent reforms under the Fit for 55 package have tightened the cap on emissions, reducing the availability of free allowances and increasing the cost of carbon. This regulatory tightening forces industries to seek cost effective compliance strategies, including the purchase of offsets where permitted or investing in external reduction projects. The introduction of the Carbon Border Adjustment Mechanism further intensifies the necessary for accurate carbon accounting and offsetting strategies for importers. According to the International Carbon Action Partnership, the price of carbon allowances in the EU ETS has reached record highs in recent years, which is signalling the economic viability of low carbon investments. Additionally, national governments are implementing complementary policies. France and Germany, for example, have introduced domestic carbon pricing mechanisms that interact with the broader European framework. These regulations create a predictable demand signal for carbon credits. As regulatory standards for offset quality rise, the market shifts toward higher integrity projects, ensuring that the offsets purchased contribute genuinely to emission reductions.

MARKET RESTRAINTS

Integrity Concerns and Quality Verification Issues Restraining Growth

A significant restraint facing the Europe carbon offsetting market is the persistent concern regarding the integrity and quality of carbon credits. Critics argue that many offset projects fail to deliver the promised emission reductions due to issues with additionality, permanence, and leakage. As per The Guardian, investigations have revealed that several major carbon offsetting schemes approved by international bodies may not be reducing global emissions as claimed. Such revelations erode trust among acquireers and regulators. The lack of standardized verification methods exacerbates this problem, leading to a fragmented market where credit quality varies widely. Furthermore, the permanence of carbon storage in nature based solutions, such as foresattempt projects, is vulnerable to risks like wildfires and disease. According to the World Resources Institute, the reversal of carbon sequestration due to natural disturbances poses a significant challenge to the reliability of nature based offsets. These integrity issues lead to reputational risks for companies that purchase questionable credits. Greenwashing accusations can damage brand value and invite regulatory scrutiny. Consequently, many corporations are delaying large scale purchases until clearer standards and verification protocols are established.

Complexity in Standardization and Regulatory Fragmentation Impeding Scalability

The absence of a unified global standard for carbon offsetting creates significant operational challenges that restrain the regional market expansion. While the European Union has robust internal mechanisms, the voluntary carbon market operates across borders with varying methodologies and certification bodies. As per the Integrity Council for the Voluntary Carbon Market, the lack of a single global benchmark for high quality credits complicates the assessment of project validity. Buyers must navigate multiple standards such as Verra and Gold Standard, each with different criteria for additionality and monitoring. This complexity discourages compacter enterprises from participating, limiting the market to larger corporations with dedicated sustainability teams. Moreover, regulatory divergence between European nations adds another layer of difficulty. According to the Organisation for Economic Cooperation and Development, inconsistent policy frameworks across jurisdictions hinder the development of a liquid and transparent carbon market. This regulatory patchwork prevents seamless trading of credits and limits price discovery. Investors face uncertainty regarding the long term viability of certain offset types due to potential policy shifts. The resulting instability creates long term contracting difficult, reducing the flow of upfront capital necessaryed for project development. Until a harmonized regulatory framework emerges, the market will struggle to achieve the scale necessary to create a significant impact on global emissions.

MARKET OPPORTUNITIES

Expansion into High Quality Removal Technologies Offering New Avenues

A major opportunity for the Europe carbon offsetting market is in the rapid advancement and deployment of carbon removal technologies. Unlike traditional avoidance projects, removal technologies physically extract carbon dioxide from the atmosphere and store it permanently. This shift aligns with the growing demand for durable and verifiable climate solutions. As per the European Academy of Sciences, carbon dioxide removal will be essential to meet the net zero tarreceives set by the European Union. Technologies such as direct air capture, bioenergy with carbon capture and storage, and enhanced weathering are gaining traction. The European Innovation Council has allocated funding to support the development of these emerging technologies. For instance, the Northern Lights project in Norway demonstrates the commercial viability of large scale carbon storage. The demand for removal credits is expected to outstrip supply in the coming years, creating a premium market segment. According to McKinsey and Company, global demand for carbon removal could reach significant levels by 2050, highlighting immense growth potential. European firms are well positioned to lead this technological revolution due to strong research and development capabilities and supportive policy environments. Investing in removal technologies offers companies a way to future proof their climate strategies against tightening regulations and increasing scrutiny of avoidance offsets.

Integration of Biodiversity and Social Co Benefits Enhancing Value Proposition

The integration of biodiversity and social co benefits into carbon offsetting projects presents a significant opportunity for the European carbon offsetting market. Buyers are increasingly seeking credits that deliver multiple positive impacts beyond carbon reduction. This holistic approach aligns with broader environmental, social, and governance agconcludeas of corporations and investors. As per the United Nations Environment Programme, nature based solutions that protect and restore ecosystems can provide a substantial portion of cost effective mitigation necessaryed to keep global warming below 2°C. Projects that combine carbon sequestration with habitat restoration, water conservation, and community livelihood improvement are attracting premium prices. Agroforesattempt projects in Southern Europe, for example, not only capture carbon but also prevent soil erosion and support local farmers. The European Biodiversity Strategy for 2030 emphasizes integrating nature restoration into climate action. According to the World Bank, investments in nature based solutions can yield significant economic returns through improved ecosystem services. Companies that purchase these high integrity credits can enhance brand reputation and demonstrate genuine commitment to sustainable development. This trconclude is driving the creation of new certification standards that explicitly account for co benefits, which is expanding the appeal of carbon offsetting to a broader range of stakeholders.

MARKET CHALLENGES

Risk of Greenwashing Accusations Damaging Corporate Reputation

A primary challenge for the Europe carbon offsetting market is the heightened risk of greenwashing accusations, which can severely damage corporate reputation and stakeholder trust. As scrutiny of environmental claims intensifies, companies face greater liability for misleading or exaggerated statements about their climate impact. As per the European Commission, proposed directives on empowering consumers for the green transition aim to ban generic environmental claims unless backed by recognized proof of excellent environmental performance. This regulatory crackdown means that companies relying on low quality offsets to claim carbon neutrality may face legal penalties and public backlash. The distinction between carbon neutrality and net zero is often blurred in marketing communications, leading to consumer confusion and skepticism. According to the London School of Economics, many corporate net zero plans lack credibility due to overreliance on offsets rather than direct emission reductions. This perception undermines the legitimacy of the offsetting indusattempt. The fear of reputational damage leads some organizations to reduce visibility in the carbon market or adopt conservative offsetting strategies, slowing financial flows to climate projects. Media and NGOs actively monitor corporate climate actions, ready to expose discrepancies. To mitigate this risk, companies must prioritize transparency, engage in rigorous due diligence, and communicate climate strategies clearly and honestly.

Volatility in Carbon Credit Prices Creating Financial Uncertainty

The volatility of carbon credit prices poses a significant challenge to the stability and predictability of the Europe carbon offsetting market. Price fluctuations are driven by regulatory alters, supply chain disruptions, and shifts in market sentiment. As per the European Energy Exalter, prices for carbon allowances in the EU ETS have experienced notable swings, influenced by energy crises and economic uncertainties. This volatility extconcludes to the voluntary carbon market, where prices for different types of credits vary widely. The lack of price transparency and liquidity exacerbates the issue. Buyers struggle to budreceive for offsetting necessarys when prices are unpredictable. According to BloombergNEF, the average price of nature based carbon credits has displayn considerable variation depconcludeing on project type and location. This financial uncertainty creates it difficult for project developers to secure long term financing, as revenue streams are not guaranteed. Investors hesitate to commit capital to projects with uncertain returns. Furthermore, price volatility can lead to speculative trading, distorting the true value of carbon reductions. Small and medium sized enterprises are particularly vulnerable, lacking resources to hedge against risk. To address this challenge, greater market transparency, standardized contracts, and mechanisms such as price floors or ceilings are necessaryed. Without stabilization measures, the carbon offsetting market will remain susceptible to shocks that impede growth and effectiveness in combating climate alter.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

12.63% |

|

Segments Covered |

By Type, Project Type, End User, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

3Degrees Group, Inc., Carbon Care Asia Ltd., Shell plc, TotalEnergies SE, BP plc, CarbonBetter, ClearSky Climate Solutions, EKI Energy Services Ltd., Finite Carbon, NativeEnergy, and South Pole Group |

SEGMENTAL ANALYSIS

By Type Insights

The compliance market led the market and held 84.9% of the European market share in 2025. This supremacy is primarily driven by the mandatory nature of the European Union Emissions Trading System, which legally binds heavy industries to cap their emissions. The regulatory framework creates an inelastic demand for allowances and offsets as companies face severe financial penalties for non-compliance. As per the European Commission, the EU ETS covers a significant portion of the EU’s greenhoutilize gas emissions and includes power stations, industrial plants, and flights within the European Economic Area. The strict enforcement mechanisms ensure that entities prioritize purchasing compliance credits to meet their legal obligations. The price stability and liquidity provided by the regulated exalter further cement its position as the primary vehicle for carbon management in Europe. According to the International Carbon Action Partnership, the total value of transactions in the EU ETS has reached very high levels in recent years, demonstrating the massive financial scale of the compliance sector. The continuous tightening of emission caps under the Fit for 55 packages ensures that the compliance market will retain its leading position.

On the other conclude, the voluntary market represents the rapidest growing segment within the Europe carbon offsetting market and is estimated to grow at a CAGR of 19.4% over the forecast period owing to the increasing corporate social responsibility mandates and consumer demand for transparent climate action. Unlike the compliance sector, the voluntary market allows companies to exceed regulatory requirements and achieve net zero status through high integrity projects. As per the Tinquireforce on Scaling Voluntary Carbon Markets, demand for voluntary carbon credits could increase significantly by 2030. This surge is driven by multinational corporations headquartered in Europe that are setting ambitious science based tarreceives. The proliferation of environmental, social, and governance reporting standards further compels firms to disclose their carbon footprints and offsetting activities. According to Ecosystem Marketplace, the value of the global voluntary carbon market has grown substantially, with Europe being a significant contributor due to its robust corporate sustainability frameworks. The flexibility of the voluntary market allows for innovation in project types, such as biodiversity focutilized initiatives and community development programs. This adaptability attracts a diverse range of acquireers, including compact and medium enterprises that are not covered by the EU ETS.

By Project Type Insights

The avoidance and reduction projects segment held the dominating position and accounted for 71.1% of the regional market share in 2025. The growth of the avoidance and reduction projects segment can be credited to the mature infrastructure of renewable energy and energy efficiency initiatives that have been established over decades. These projects offer a cost effective method for preventing emissions at the source, building them attractive to both compliance and voluntary acquireers. As per the International Energy Agency, renewable energy sources have avoided a significant volume of carbon dioxide emissions globally, with Europe contributing strongly through wind and solar expansions. The proven methodology for calculating emission reductions in these sectors provides a high level of certainty for investors and regulators. According to Eurostat, the share of renewables in the EU energy mix has risen steadily, reflecting the extensive deployment of avoidance technologies. The scalability of these projects allows for the generation of large credit volumes, ensuring market liquidity. Furthermore, the alignment with national energy security goals enhances political support for avoidance projects.

However, the removal and sequestration projects segment is estimated to witness the rapidest CAGR of 24.4% over the forecast period owing to the urgent necessary for permanent carbon storage to achieve net zero tarreceives. As avoidance opportunities become saturated, attention shifts to technologies that actively rerelocate carbon dioxide from the atmosphere. As per the European Academy of Sciences, carbon dioxide removal is essential to counterbalance hard to abate emissions from sectors such as aviation and heavy indusattempt. The development of direct air capture facilities and enhanced weathering techniques is gaining momentum across the continent. The Northern Lights project in Norway exemplifies this trconclude, aiming to store large volumes of carbon underground. According to the Global CCS Institute, the number of carbon capture and storage facilities in development in Europe has increased significantly in recent years. Policy support plays a crucial role in this expansion, with the European Union allocating billions of euros through the Innovation Fund for low carbon technologies. Buyers are increasingly willing to pay a premium for removal credits due to their higher permanence and additionality compared to avoidance projects. As technological costs decline and scaling effects kick in, removal projects are expected to capture a larger share of the market. This transition marks a pivotal shift in climate strategy from merely reducing future emissions to actively reversing past contributions.

By End User Insights

The renewable energy segment led the market by accounting for 33.6% of the regional market share in 2025. The growth of the renewable energy segment in the European market is attributed to the extensive integration of wind, solar, and hydroelectric projects that generate verifiable emission reductions. Energy producers utilize carbon credits to monetize the environmental benefits of clean electricity generation, enhancing project viability. As per the European Wind Energy Association, wind energy has avoided a substantial volume of carbon dioxide emissions in the EU, building renewable energy projects a primary source of high quality offsets. The sector benefits from strong policy support and established certification methodologies that facilitate simple verification and trading. According to Eurostat, investments in renewable energy infrastructure in the EU have consistently exceeded significant levels annually, creating a robust pipeline of offsettable projects. The alignment with the European Green Deal objectives ensures continued government backing and financial incentives. Energy companies also purchase offsets to compensate for intermittent reliance on backup fossil fuel systems during peak demand periods. This dual role as both generators and acquireers of credits strengthens the sector’s market position. The transparency of energy production data allows for accurate monitoring and reporting, reducing the risk of greenwashing. Furthermore, the global demand for green energy certificates often overlaps with carbon offset markets, amplifying financial flows into this segment. The maturity of the renewable energy indusattempt in Europe provides a stable foundation for its continued leadership.

However, the transportation segment is emerging as the rapidest growing conclude utilizer segment in the Europe carbon offsetting market and is estimated to grow at a CAGR of 21.2% over the forecast period owing to the difficulty of decarbonizing aviation and maritime transport, which rely heavily on liquid fuels. As per the European Environment Agency, transport accounts for a significant share of total EU greenhoutilize gas emissions, building it a critical tarreceive for offsetting strategies. Airlines and shipping companies are increasingly purchasing high quality carbon credits to meet international regulatory requirements and corporate sustainability goals. The International Civil Aviation Organization’s Carbon Offsetting and Reduction Scheme for International Aviation mandates that airlines offset growth in emissions above 2020 levels. According to the International Air Transport Association, the aviation indusattempt has committed to achieving net zero carbon emissions by 2050, driving significant demand for offsets. Maritime transport faces similar challenges, with the International Maritime Organization setting stricter emission reduction tarreceives. Logistics companies are also integrating offsetting into their supply chain services to meet customer demands for low carbon shipping options. The visibility of transport emissions and the pressure from environmentally conscious travelers further accelerate this trconclude. As alternative fuel technologies develop, the transportation sector will continue to be a major driver of carbon offset demand, particularly for high integrity removal projects that address residual emissions.

REGIONAL ANALYSIS

Germany Carbon Offsetting Market Analysis

Germany led the market by holding 21.6% of the European market share in 2025. The dominance of Germany in the European market is attributed to the counattempt’s robust industrial base and ambitious climate legislation. As per the German Environment Agency, Germany has set strict emission reduction tarreceives for 2030 compared to 1990 levels, which is driving significant demand for compliance and voluntary offsets among manufacturing and energy companies. The presence of major automotive and chemical industries creates a substantial pool of hard to abate emissions that require offsetting. According to Destatis, investments in environmental protection measures by German companies have reached record highs in recent years. The Energiewconcludee policy, focutilized on transitioning to renewable energy, also generates a large volume of domestic carbon credits. German corporations are increasingly adopting science based tarreceives, further boosting the voluntary market. The counattempt’s strong financial sector facilitates trading and financing of carbon projects, enhancing market liquidity. Public awareness of climate issues in Germany is among the highest in Europe, which is pressuring businesses to demonstrate tangible climate action.

United Kingdom Carbon Offsetting Market Analysis

The United Kingdom had the second major share of the European carbon offsetting market in 2025. Despite leaving the European Union, the UK has maintained a stringent climate policy framework through its own UK Emissions Trading Scheme. As per the UK Committee on Climate Change, the counattempt has legally binding tarreceives to reach net zero emissions by 2050. This commitment drives consistent demand for carbon offsets across various sectors, particularly in finance and professional services. London serves as a global center for carbon trading and finance, facilitating significant transaction volumes. According to the Office for National Statistics, the UK service sector contributes the majority of the counattempt’s economic output, and is a major acquireer of voluntary offsets. The UK government’s Ten Point Plan for a Green Industrial Revolution includes investments in hydrogen and carbon capture technologies, generating new offset opportunities. The counattempt’s strong legal framework provides certainty for investors in carbon projects, while its historical leadership in climate diplomacy enhances influence on international carbon markets.

France Carbon Offsetting Market Analysis

France is estimated to hold a prominent share of the European carbon offsetting market during the forecast period. The counattempt’s market is driven by a strong emphasis on nuclear energy and a growing focus on nature based solutions. As per the French Minisattempt of Ecological Transition, France aims to achieve carbon neutrality by 2050, with intermediate tarreceives for 2030. The Low Carbon Strategy label promotes high quality domestic offset projects, particularly in foresattempt and agriculture. According to INSEE, French companies are increasingly integrating environmental criteria into procurement processes. The agricultural sector provides significant carbon sequestration potential, with initiatives like the 4 per 1000 gaining traction. French energy giants are investing heavily in renewable energy projects abroad, generating international carbon credits. Strict reporting requirements for large companies mandate disclosure of climate related risks, driving demand for verified offsets. The French government also supports carbon farming practices that reward farmers for sequestering carbon in soils.

Italy Carbon Offsetting Market Analysis

Italy is expected to exhibit a healthy CAGR in the European carbon offsetting market during the forecast period. The counattempt’s market dynamics are influenced by its significant manufacturing sector and abundant renewable energy resources, particularly solar and geothermal. As per the Italian National Institute of Statistics, Italy has built progress in reducing carbon intensity, though industrial emissions remain a challenge. The National Integrated Energy and Climate Plan sets ambitious tarreceives for renewable adoption and energy efficiency, driving demand for offsets during the transition. Italian companies, especially in fashion and automotive, are increasingly engaging in voluntary offsetting to enhance global brand image. According to Legambiente, demand for green certifications among Italian consumers is rising, prompting businesses to invest in credible carbon projects. Italy’s geographical diversity offers opportunities for foresattempt and land utilize projects. Government incentives for energy efficiency improvements in buildings indirectly support offsetting by generating verified savings.

Spain Carbon Offsetting Market Analysis

Spain is predicted to account for a notable share of the European carbon offsetting market over the forecast period. The counattempt’s market is propelled by its exceptional renewable energy potential, particularly wind and solar power. As per the Spanish Minisattempt for the Ecological Transition and the Demographic Challenge, Spain has set aggressive tarreceives for renewable electricity generation by 2030. Spanish utilities are active participants in the European carbon market, leveraging renewable portfolios to generate and trade credits. According to the National Statistics Institute of Spain, investment in green technologies has surged, supported by European recovery funds. The tourism sector, a vital component of the Spanish economy, is increasingly adopting carbon neutrality goals to appeal to environmentally conscious travelers. Hotels and airlines purchase voluntary offsets to mitigate operational footprints. Spain’s vast land area also offers opportunities for reforestation and soil carbon sequestration projects. Government support for green hydrogen production further expands the scope for low carbon projects.

COMPETITIVE LANDSCAPE

The competition in the Europe carbon offsetting market is characterized by a fragmented yet dynamic landscape where established sustainability consultancies compete with emerging technology driven startups. Large multinational firms leverage their extensive global networks and brand reputation to secure contracts with major corporations seeking comprehensive net zero strategies. These incumbents often possess deep expertise in regulatory compliance and risk management which appeals to risk averse institutional acquireers. Conversely agile new entrants disrupt the market by offering transparent digital platforms that address longstanding concerns regarding credit quality and double counting. The barrier to enattempt remains moderate due to the necessary for specialized knowledge in carbon accounting and project verification. Competitive differentiation increasingly relies on the integrity and type of carbon credits offered with a clear premium placed on removal based solutions over traditional avoidance projects. Price competition is intensifying as market liquidity improves but quality assurance remains the primary deciding factor for sophisticated acquireers. Regulatory alters such as the European Union Green Claims Directive further shape competitive dynamics by raising standards for environmental claims. Companies that fail to adapt to these stricter requirements face reputational risks and potential exclusion from preferred supplier lists. Collaboration is also becoming a key competitive tactic as firms join indusattempt alliances to standardize methodologies and promote best practices. This collaborative competition fosters a more robust and credible market ecosystem overall.

KEY MARKET PLAYERS

Some of the notable key players in the Europe carbon offsetting market are

- 3Degrees Group, Inc.

- Carbon Care Asia Ltd.

- Shell plc

- TotalEnergies SE

- BP plc

- CarbonBetter

- ClearSky Climate Solutions

- EKI Energy Services Ltd.

- Finite Carbon

- NativeEnergy

- South Pole Group

Top Players in the Market

- South Pole is a leading sustainability solutions provider that plays a pivotal role in the Europe carbon offsetting landscape. The company develops and manages a diverse portfolio of high quality carbon credits from renewable energy and foresattempt projects. South Pole actively advises corporations on achieving net zero tarreceives through science based strategies. Recently the firm has expanded its digital platforms to enhance transparency and traceability of carbon credits. This technological integration allows acquireers to verify the authenticity and impact of their purchases. South Pole collaborates with governments and businesses to design customized climate action plans. Their extensive global network ensures access to verified emission reductions across various sectors. By focapplying on additionality and community benefits South Pole strengthens trust in voluntary carbon markets. The company continues to innovate in carbon removal technologies to meet evolving client demands.

- ClimatePartner is a prominent specialist in carbon neutrality certification and climate protection projects within Europe. The company enables businesses to calculate reduce and offset their carbon footprints effectively. ClimatePartner partners with thousands of companies including major e commerce platforms and manufacturers. They provide labeled products that communicate verified climate action to consumers. Recent initiatives include the development of blockchain based tracking systems for enhanced credit integrity. ClimatePartner focutilizes heavily on nature based solutions that support biodiversity and local communities. Their rigorous verification processes ensure that offset projects meet international standards. The firm actively engages in policy advocacy to improve regulatory frameworks for carbon markets. By offering conclude to conclude climate services ClimatePartner assists organizations transition toward sustainable operations. Their utilizer friconcludely interfaces simplify complex carbon accounting for compact and medium enterprises.

- Norsk Klima is a significant contributor to the European carbon market with a strong focus on industrial decarbonization. The company facilitates the trading of carbon allowances and offsets for heavy industries and energy providers. Norsk Klima provides expert consulting on compliance with the European Union Emissions Trading System. They develop innovative financial instruments to hedge against carbon price volatility. Recent efforts involve investing in direct air capture technologies and carbon storage infrastructure. The firm collaborates with research institutions to advance carbon removal methodologies. Norsk Klima emphasizes the importance of permanent sequestration over temporary avoidance measures. Their strategic partnerships with Nordic energy firms enhance the supply of high integrity credits. By integrating digital monitoring tools Norsk Klima improves the accuracy of emission reporting. The company supports corporate clients in navigating the complexities of international carbon regulations.

Top Strategies Used by Key Market Participants

Key players in the Europe carbon offsetting market primarily employ vertical integration strategies to control the entire value chain from project development to credit retirement. Companies are increasingly investing in proprietary technology platforms that utilize blockchain for enhanced transparency and immutable tracking of carbon credits. This approach builds trust among acquireers who demand proof of additionality and permanence. Another major strategy involves diversification into carbon removal technologies such as direct air capture and biochar production. This shift addresses the growing demand for durable offsets that go beyond traditional avoidance projects. Strategic partnerships with non governmental organizations and local communities are also common to ensure social co benefits and secure long term project viability. Furthermore firms are expanding their advisory services to assist clients navigate complex regulatory landscapes and achieve science based tarreceives. Mergers and acquisitions are frequently utilized to consolidate market position and acquire specialized expertise in niche sectors like blue carbon or soil sequestration. These combined strategies enable participants to offer comprehensive climate solutions while maintaining competitive advantage in a rapidly evolving market environment.

MARKET SEGMENTATION

This research report on the European carbon offsetting market has been segmented and sub-segmented based on categories.

By Type

- Compliance Market

- Voluntary Market

By Project Type

- Avoidance or Reduction Projects

- Removal or Sequestration Projects

By End User

- Renewable Energy

- Foresattempt and Land

- Industrial

- Houtilizehold and Appliances

- Transportation

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe