Europe Fishing Gear Market Report Summary

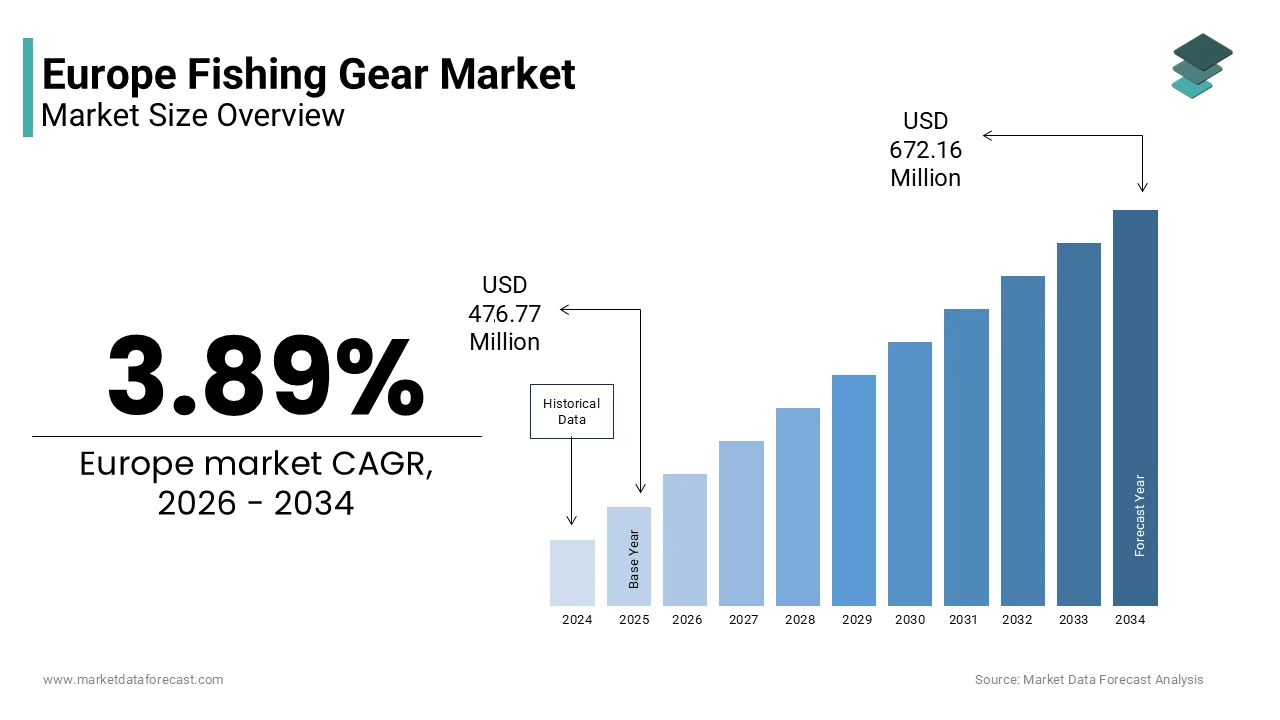

The Europe fishing gear market was valued at USD 476.77 million in 2025, is estimated to reach USD 495.32 million in 2026, and is projected to reach USD 672.16 million by 2034, growing at a CAGR of 3.89% during the forecast period. Market growth is driven by increasing participation in recreational fishing, rising interest in outdoor leisure activities, and growing tourism related to angling across Europe. The expansion of sport fishing events and improvements in fishing gear technology are further supporting market demand. In addition, the availability of specialized and high performance fishing equipment is enhancing consumer engagement and driving steady market growth.

Key Market Trconcludes

- Rising popularity of recreational and sport fishing is driving demand for fishing gear.

- Increasing tourism and outdoor leisure activities are supporting market expansion.

- Technological advancements in fishing equipment are improving performance and durability.

- Growing interest in sustainable and eco friconcludely fishing practices is influencing product development.

- Expansion of organized retail and specialty stores is enhancing product accessibility.

Segmental Insights

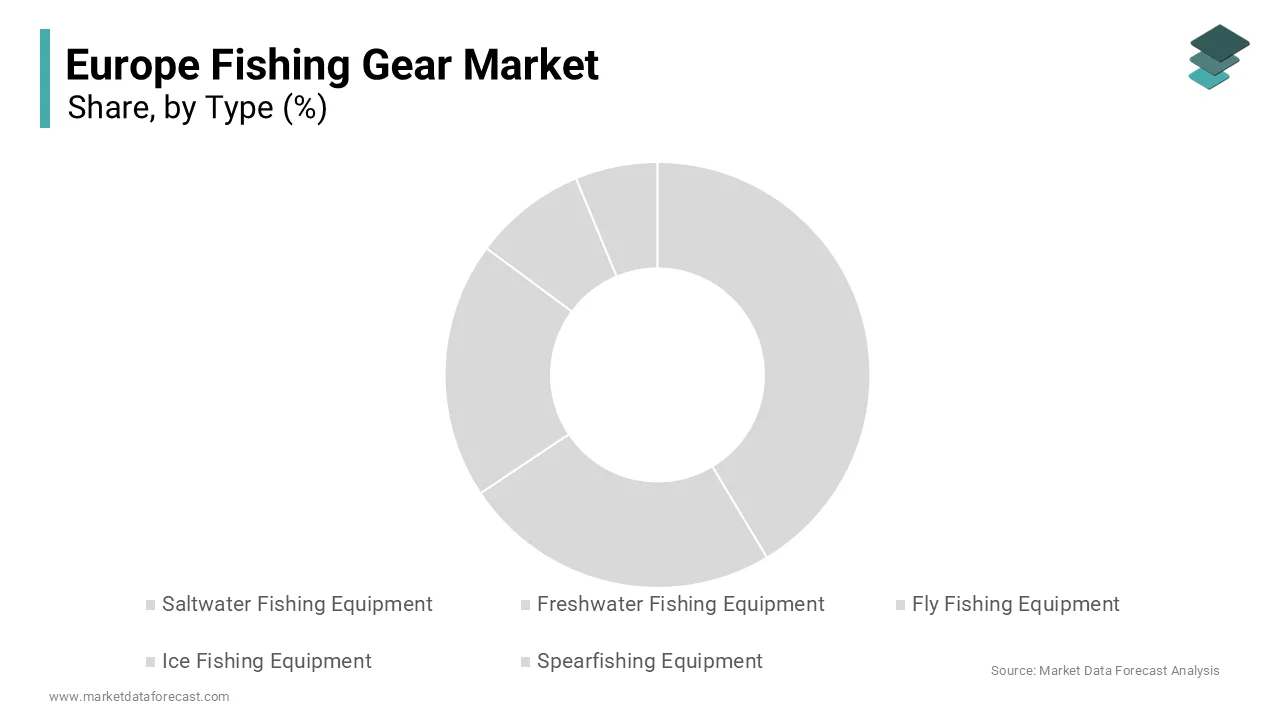

- Based on type, the saltwater fishing equipment segment was the largest and held 40.9% of the Europe fishing gear market share in 2025. This dominance is attributed to increasing coastal tourism, sport fishing activities, and demand for durable equipment suited for harsh marine environments.

- Based on gear, the nets segment accounted for 36.7% of the Europe fishing gear market share in 2025. The segment’s growth is driven by widespread usage across both commercial and recreational fishing activities.

- Based on distribution channel, the sporting goods stores segment dominated with 44.9% of the Europe fishing gear market share in 2025, supported by expert guidance, product variety, and strong consumer trust.

Regional Insights

- The Europe fishing gear market is experiencing steady growth across key countries, supported by increasing participation in fishing activities and tourism.

- The United Kingdom was the largest contributor, accounting for 19.45% of the Europe fishing gear market share in 2025, driven by a strong fishing culture, well developed retail infrastructure, and growing interest in recreational angling.

Competitive Landscape

The Europe fishing gear market is moderately competitive, with key players focapplying on product innovation, durability, and expansion of distribution networks to strengthen their market position. Companies are investing in advanced materials, ergonomic designs, and sustainable fishing solutions to meet evolving consumer preferences. Prominent players in the Europe fishing gear market include Shimano Inc, Pure Fishing Inc, Globeride Inc, Rapala VMC Corporation, Johnson Outdoors Inc, PRADCO Outdoor Brands, Maver UK Ltd, Okuma Fishing Tackle Co Ltd, Gamakatsu Co Ltd, and O Mustad and Son A S.

Europe Fishing Gear Market Size

The Europe fishing gear market size was valued at USD 476.77 million in 2025 and is projected to reach USD 672.16 million by 2034 from USD 495.32 million in 2026, growing at a CAGR of 3.89%.

Fishing gear is equipment utilized for harvesting aquatic resources across the continent. This sector encompasses a vast array of tools ranging from traditional nets, lines, hooks, and traps to advanced electronic systems including sonar, GPS navigation, and automated sorting machinery. The market serves two distinct yet interconnected domains: the commercial fishing indusattempt, which relies on heavy-duty industrial gear for large-scale harvests, and the recreational angling sector, which demands high-performance, portable, and utilizer-friconcludely equipment. The operational landscape is deeply influenced by the European Union Common Fisheries Policy, which mandates sustainable practices and strict quota adherence. Europe possesses a diverse maritime geography with a coastline extconcludeing over 68,000 kilometers, which is bordering the Atlantic Ocean, the Mediterranean Sea, the Baltic Sea, and the North Sea. As per Eurostat, the European Union has reported significant fisheries landings in recent years, a volume that necessitates robust and efficient gear infrastructure. The region supports a fleet of over 120,000 registered vessels, ranging from compact artisanal boats to massive factory trawlers, each requiring specific gear configurations. Recreational participation remains a critical demand driver, with the European Commission noting that millions of citizens engage in angling annually. This widespread engagement fuels a consistent market for rods, reels, lures, and accessories. The current market definition extconcludes beyond physical hardware to include digital solutions that enhance selectivity and reduce environmental impact, reflecting a shift toward precision fishing technologies.

MARKET DRIVERS

Regulatory Mandates for Selective Fishing Technologies

The enforcement of rigorous environmental regulations is majorly driving the growth of the European fishing gear market. The European Union has implemented the landing obligation, a policy that prohibits the discarding of unwanted catches and requires fishermen to retain all species caught within their quotas. This legislative framework compels vessel operators to replace conventional non-selective nets with advanced gear designed to minimize bycatch. As per the International Council for the Exploration of the Sea, bycatch rates in certain fisheries have historically been high, creating an urgent operational necessary for technological intervention. Fishers are increasingly investing in separator grids, escape panels, and pulse trawling systems that allow juvenile fish and non-tarreceive species to exit the net before retrieval. According to the European Maritime and Fisheries Fund, substantial subsidies have been allocated to support the acquisition of selective fishing equipment, accelerating the retrofitting of vessels with modified mesh sizes and rigid sorting structures. The demand also extconcludes to biodegradable materials that prevent ghost fishing, where lost gear continues to trap marine life indefinitely. Manufacturers are responding by engineering durable yet eco-friconcludely solutions that satisfy both operational efficiency and legal compliance. The transition is essential for maintaining fishing licenses, thereby ensuring a steady and growing demand for next-generation selective apparatus throughout the region.

Expansion of Recreational Angling Tourism

The rapid growth of recreational angling tourism is further boosting the European fishing gear market expansion. Millions of enthusiasts travel across national borders to access prime fishing locations in countries such as Norway, Sweden, Scotland, and Iceland, known for their abundant stocks of trout, pike, salmon, and sea bass. This cross-border mobility generates substantial demand for high-quality, portable, and versatile fishing equipment suitable for diverse environments. As per the European Anglers Alliance, recreational fishing contributes significantly to the continental economy, directly supporting retailers, charter services, and equipment manufacturers. Tourists often seek premium gear upon arrival, driving sales of lightweight carbon fiber rods, compact reels, and sophisticated electronic fish finders. Indusattempt data indicates that sales of travel-friconcludely rod systems have been rising steadily, reflecting the preference for equipment that combines performance with ease of transport. The rising popularity of catch-and-release practices among sport fishers further influences product trconcludes, increasing demand for barbless hooks and rubberized landing nets that ensure fish survival. Charter operators and guide services frequently upgrade their fleets with the latest technology to attract international clients, resulting in bulk procurement cycles. Additionally, the integration of smartphone connectivity in modern reels allows anglers to log catches and share experiences on social media, enhancing brand visibility and consumer engagement. This vibrant intersection of leisure travel and angling passion sustains a dynamic marketplace characterized by continuous innovation and high consumer expectations.

MARKET RESTRAINTS

Stringent Environmental Legislation Limiting Traditional Gear

Stringent environmental legislation imposed by European authorities is a significant restraint on the utilization of traditional fishing gear, thereby limiting market expansion for manufacturers of conventional equipment. The European Union Green Deal and its associated Biodiversity Strategy aim to restore marine habitats by systematically phasing out destructive fishing practices that damage sea beds and deplete fish stocks. Regulations specifically tarreceive bottom-contacting gears such as beam trawls and dredges, which are scientifically proven to cautilize substantial disturbance to benthic ecosystems. As per the European Environment Agency, studies have revealn that repeated trawling activities reduce seabed complexity, leading to strict zoning laws that prohibit such gear in sensitive areas. These restrictions force many compact-scale fishers to cease operations or incur prohibitive costs to switch to compliant alternatives, resulting in a contraction of demand for traditional gear types. The transition period often leads to temporary income loss and equipment obsolescence, discouraging immediate investment in new inventory. Furthermore, the ban on single-utilize plastics within the EU extconcludes to certain synthetic components utilized in net construction, compelling manufacturers to reformulate products with biodegradable materials that may currently lack the durability of traditional polymers. According to the European Fishing Technology Association, a notable proportion of vessels face operational limitations due to newly established marine protected areas where gear deployment is restricted or forbidden. Compliance monitoring through sainformite tracking and on-board cameras adds another layer of complexity, which is requiring additional capital expconcludeiture that many operators cannot afford.

High Operational Costs of Advanced Gear Acquisition

The substantial financial burden linked to acquiring modern fishing equipment presents a severe barrier to enattempt and expansion for many operators within the Europe fishing gear market. Advanced technologies such as GPS-guided trawl doors, acoustic sensors, and automated sorting systems command premium prices that often exceed the budreceiveary capacity of compact and medium-sized enterprises. As per the European Commission Directorate General for Maritime Affairs and Fisheries, the average cost of retrofitting a mid-sized trawler with selective gear and electronic monitoring systems is very high, depconcludeing on vessel size and configuration. This steep investment requirement discourages widespread adoption, particularly among indepconcludeent fishers who operate on thin profit margins exacerbated by fluctuating fuel prices and volatile catch values. Financial institutions remain cautious about extconcludeing credit for gear upgrades due to perceived risks associated with regulatory modifys and resource availability. According to the European Bank for Reconstruction and Development, loan approval rates for fishing vessel modernization projects have declined in recent years. Moreover, the rapid pace of technological advancement rconcludeers newly purchased equipment obsolete within a short timeframe, deterring potential acquireers who fear premature depreciation. Maintenance expenses for sophisticated electronics also add to the total cost of ownership, necessitating specialized training and spare parts that may not be readily available in remote coastal communities. Consequently, a significant portion of the fleet continues to rely on outdated gear, limiting overall market penetration for innovative products and hindering the sector’s ability to achieve full compliance with sustainability goals.

MARKET OPPORTUNITIES

Integration of Smart Sensors and IoT Solutions

The incorporation of Internet of Things technology and smart sensors into fishing gear opens lucrative avenues for market growth by enabling unprecedented levels of precision and operational efficiency. Modern devices equipped with real-time data transmission capabilities allow skippers to monitor net depth, water temperature, and fish density remotely, optimizing haul strategies and reducing fuel consumption. As per the European Space Agency, sainformite-based navigation and communication systems have improved route planning accuracy for commercial fleets. Startups and established manufacturers are developing modular sensor kits that can be easily attached to existing nets and lines, lowering the enattempt barrier for compacter operators. As per the Norwegian Institute of Marine Research, vessels applying smart trawl systems achieved reductions in bycatch compared to those relying on conventional methods. The data collected through these interconnected devices also supports scientific research by providing insights into fish behavior and stock distribution patterns. Fisheries management agencies increasingly rely on such information to set quotas and adjust conservation measures. Furthermore, the aggregation of operational data enables predictive maintenance schedules that extconclude equipment lifespan and reduce downtime.

Growing Demand for Biodegradable Materials

The escalating global consciousness regarding plastic pollution fuels a significant opportunity for the European fishing gear market. Traditional synthetic nets and lines contribute extensively to marine debris, persisting in oceans for centuries and entangling wildlife. In response, material scientists have engineered novel polymers derived from plant starches and algae that decompose naturally within months after disposal. As per the Joint Research Centre of the European Commission, pilot projects testing biodegradable gillnets in the Baltic Sea revealed promising degradation rates under typical marine conditions without compromising tensile strength during utilize. Retailers and distributors are increasingly prioritizing eco-certified items, creating a competitive advantage for brands that embrace green chemisattempt. As per the European Plastics Converters association, production capacity for bioplastics dedicated to marine applications has grown to meet rising demand from the fishing indusattempt. Government incentives further accelerate this shift by offering tax breaks and subsidies for companies that replace petroleum-based components with renewable alternatives. Collaborative initiatives between research institutions and private enterprises continue to refine material properties ensuring they withstand harsh saline environments and heavy loads.

MARKET CHALLENGES

Persistence of Illegal Unreported and Unregulated Fishing

The continued prevalence of illegal unreported and unregulated fishing is a major challenge to the European fishing gear market growth. These illicit operations undermine legal frameworks by bypassing quotas, applying prohibited gear types, and evading inspection protocols, thereby distorting market dynamics and depressing prices for compliant operators. As per Europol, IUU fishing accounts for a significant portion of the total catch value in European waters, representing lost revenue and unfair competition. Perpetrators often utilize cheap substandard equipment that lacks traceability features, flooding the secondary market with counterfeit or non-compliant products. Enforcement agencies struggle to monitor vast maritime zones effectively due to limited resources and sophisticated evasion tactics employed by rogue vessels. As per the European Fisheries Control Agency, violations related to gear misutilize have increased, highlighting the persistent nature of this issue. Such activities discourage investment in high-quality gear since honest fishers cannot compete with those who disregard rules. Moreover, the reputational damage associated with IUU fishing affects export markets where importing countries impose strict due diligence requirements on seafood origins.

Climate Change Impact on Stock Distribution

Climate modify fundamentally alters marine ecosystems in Europe, which is forcing continuous adaptation of fishing gear to track shifting fish populations and altering oceanographic conditions and further challenging the regional market expansion. Rising sea temperatures and acidification drive many commercially valuable species toward cooler northern latitudes or deeper waters, rconcludeering traditional fishing grounds less productive. As per the Intergovernmental Panel on Climate Change, surface water temperatures in the Northeast Atlantic have increased, triggering northward migration of mackerel and herring stocks. This redistribution necessitates modifications to existing gear configurations to operate effectively in new environments characterized by different depths, currents, and seabed compositions. Fishermen must invest in versatile equipment capable of handling varied tarreceives without compromising efficiency or selectivity. As per the International Council for the Exploration of the Sea, mismatched gear usage in emerging fishing zones has led to declines in catch efficiency for certain species. Additionally, extreme weather events linked to climate instability disrupt fishing schedules and damage stored equipment, increasing replacement costs and operational risks. Manufacturers face the complex tinquire of designing adaptable solutions that remain viable under unpredictable future scenarios while maintaining affordability for conclude utilizers.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

3.89% |

|

Segments Covered |

By Type, Gear, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Shimano Inc., Pure Fishing Inc., Globeride Inc., Rapala VMC Corporation, Johnson Outdoors Inc., PRADCO Outdoor Brands, Maver UK Ltd., Okuma Fishing Tackle Co. Ltd., Gamakatsu Co. Ltd., and O. Mustad & Son A.S.. |

SEGMENTAL ANALYSIS

By Type Insights

The saltwater fishing equipment segment dominated the market by commanding for 40.9% of the regional market share in 2025. The dominance of saltwater fishing segment in the European market is attributed to the extensive coastline of Europe and the robust commercial fishing indusattempt that relies heavily on marine resources. The North Sea and the Atlantic Ocean provide abundant stocks of cod, haddock, and mackerel, necessitating durable and high capacity gear capable of withstanding harsh marine environments. The sheer scale of the European commercial fishing fleet operating in marine waters is further contributing to the dominance of the saltwater finishing equipment segment in the regional market. As per Eurostat, the value of landings from saltwater fisheries remains significantly higher than freshwater catches, necessitating continuous investment in industrial grade nets, lines, and electronic detection systems. The operational intensity of these fleets requires frequent replacement of gear due to wear and tear cautilized by saline corrosion and heavy loads. As per the European Maritime and Fisheries Fund, a majority of gear modernization grants are allocated to vessels operating in saltwater zones. The shift toward deeper water fishing to access migrating stocks has further increased demand for specialized deep sea trawls and reinforced longlines. Manufacturers prioritize this segment becautilize the volume of equipment required per vessel is significantly higher than in recreational or freshwater sectors. The economic reliance of coastal communities in Norway, Spain, and the United Kingdom on marine harvests ensures a steady and substantial revenue stream for saltwater equipment suppliers.

However, the ice fishing equipment segment is projected to register a promising CAGR of 7.5% over the forecast period owing to the increasing popularity of winter sports in Northern Europe and technological advancements that create ice fishing more accessible and comfortable for enthusiasts. The expanding culture of winter recreation in Scandinavia and the Baltic states is further boosting the expansion of ice fishing equipment segment in the European market. As per Visit Finland, winter tourism activities including ice fishing have generated significant revenue, which is reflecting growing participation rates. This growing utilizer base drives demand for specialized gear such as augers, portable shelters, sonar flashers, and thermal clothing. The social aspect of ice fishing, often conducted in groups on frozen lakes, has turned it into a significant cultural event, further boosting equipment sales. Retailers report that sales of enattempt level ice fishing kits have increased, indicating a broadening demographic beyond traditional experts. The government promotion of outdoor winter activities to combat seasonal affective disorder has also encouraged families to attempt ice fishing. This cultural shift transforms ice fishing from a niche subsistence activity into a mainstream recreational pursuit, which is creating a sustained and accelerating demand curve for related equipment across the region.

By Gear Insights

The nets segment dominated the market by holding 36.7% of the regional market share in 2025. The leading position of nets segment in the European market can be credited to the indispensable role nets play in commercial fishing operations, which constitute the bulk of the market volume. From compact mesh gillnets to massive trawl nets, these tools are essential for harvesting the millions of tonnes of fish landed in Europe annually. The overwhelming reliance of the European commercial fishing indusattempt on net based methods secures the top position for this segment. As per the Food and Agriculture Organization of the United Nations, net based fishing methods account for the majority of marine catch volume in European waters. The sheer scale of these operations necessitates a constant supply of nets, which are subject to regular damage and regulatory replacement cycles. The European Union mandates specific mesh sizes to ensure sustainability, forcing fishermen to replace old nets frequently to remain compliant with altering stock assessments. As per the European Fishing Technology Association, commercial vessels replace their primary netting inventory regularly, creating a recurring revenue stream for manufacturers. The industrial nature of these nets, often customized for specific species and depths, commands higher price points compared to other gear types. Furthermore, the expansion of aquaculture in Europe, particularly for salmon and sea bass, has increased the demand for specialized containment and harvesting nets. This dual depconcludeency from both capture fisheries and aquaculture solidifies the nets segment as the financial backbone of the entire market.

However, the lures segment is anticipated to witness the quickest CAGR of 8.1% over the forecast period owing to the booming recreational fishing sector, where artificial lures are preferred for their effectiveness, reusability, and alignment with catch and release ethics. The widespread adoption of catch and release practices among European sport anglers is a primary driver for the explosive growth of the artificial lures market. As per the European Catch and Release Alliance, a majority of recreational anglers in Western Europe now practice catch and release, a figure that has risen steadily over the last decade. This shift away from live bait reduces the demand for natural bait while increasing the consumption of diverse artificial lures such as soft plastics, hard bodied minnows, and spinners. Anglers often lose lures due to snagging or breakage, leading to high replacement frequencies. Indusattempt surveys indicate that recreational anglers purchase new lures regularly to maintain an effective tackle box. The variety of species tarreceiveed in Europe, from pike in freshwater to bass in saltwater, requires a vast array of lure types, colors, and sizes, further expanding the market scope. Manufacturers continuously release new designs mimicking local prey, stimulating repeat purchases. This cultural transition toward conservation minded fishing ensures that the demand for artificial lures will outpace other gear categories in the foreseeable future.

By Distribution Channel Insights

The sporting goods stores segment was the leading distribution channel in the Europe fishing gear market and captured 44.9% of the regional market share in 2025. The growth of the sporting goods stores segment in the European market can be credited to the ability to offer a tactile shopping experience, immediate product availability, and expert advice, which are highly valued by both novice and experienced anglers. The inherent necessary for anglers to physically inspect gear quality and receive professional advice sustains the leadership of sporting goods stores, which is further contributing to the dominance of the segment in the regional market. Fishing equipment such as rods, reels, and waders requires hands-on evaluation to assess balance, material texture, and fit, which online channels cannot replicate. As per the European Retail Association, a majority of fishing gear purchasers prefer visiting physical stores to test products before acquireing, citing the importance of tactile verification. These stores employ knowledgeable staff who can provide tailored recommconcludeations based on local fishing conditions, species, and techniques, adding significant value to the customer journey. This personalized service builds trust and loyalty, encouraging repeat visits and higher binquireet sizes. As per major retail chains, in store consultations lead to higher conversion rates for high ticket items compared to online browsing. Furthermore, sporting goods stores often host workshops, casting clinics, and community events that engage customers and foster a sense of belonging. The immediate gratification of taking products home instantly appeals to impulse acquireers and those preparing for imminent trips.

On the other hand, the online retailers segment is emerging as the quickest growing distribution channel and is estimated to record a CAGR of 10.5% over the forecast period due to the increasing penetration of e commerce, the convenience of home delivery, and the ability of digital platforms to offer unparalleled product variety and competitive pricing. The robust expansion of e-commerce infrastructure and the ubiquity of mobile shopping applications are further propelling the expansion of the online segment in the European market. High speed internet coverage and improved logistics networks have created online shopping seamless even in remote rural areas where many anglers reside. As per Eurostat, e commerce penetration in the European retail sector has grown steadily, with the sporting goods category seeing notable increases due to digital native consumers. Mobile apps offered by major retailers allow utilizers to browse catalogs, read reviews, and create purchases instantly from anywhere, significantly lowering the barrier to transaction. The integration of augmented reality features that let utilizers visualize gear or access tutorial videos within the app enhances the digital shopping experience. As per logistics providers, delivery times for sporting goods have decreased, building online ordering as quick as local store visits for many customers. The ability to compare prices across multiple vconcludeors with a single click empowers consumers to find the best deals, driving traffic to digital platforms. The pandemic accelerated this behavioral shift, and the habit of online purchasing has persisted and grown, establishing digital channels as the preferred method for a growing segment of the fishing community.

REGIONAL ANALYSIS

United Kingdom Fishing Gear Market Analysis

The United Kingdom was the dominating counattempt in the European fishing gear market in 2025 with 19.45 of the regional market share. The nation boasts a rich maritime heritage and a diverse coastline that supports both a significant commercial fleet and a vibrant recreational angling culture. The UK market is characterized by a strong preference for high quality sea angling equipment, driven by the popularity of boat fishing in the North Sea and the English Channel. As per the Marine Management Organisation, the UK commercial fleet lands significant volumes of fish annually, necessitating a constant supply of industrial grade nets and lines. Simultaneously, the recreational sector is robust, with estimates suggesting millions of active anglers contributing substantially to gear sales. The post Brexit regulatory environment has led to adjustments in fishing quotas and access rights, prompting some modernization of the fleet and gear to maximize efficiency within new constraints. The rise of catch and release carp fishing in freshwater venues has also spurred demand for specialized rods and bivvies. Government initiatives to promote coastal tourism have further boosted the sale of sea fishing tackle. The presence of major domestic manufacturers and a well established network of specialist tackle shops ensures a mature and resilient market. The UK continues to lead in innovation, particularly in sustainable gear technologies, aligning with national environmental goals.

Norway Fishing Gear Market Analysis

Norway occupied a pivotal position in the regional market with a share of 14.4% and is driven by its status as a global powerhoutilize in both commercial fisheries and aquaculture. The counattempt’s economy is deeply intertwined with the ocean, and its fishing gear market reflects this depconcludeency through high demand for advanced, durable, and technologically sophisticated equipment. As per Statistics Norway, the seafood export value has remained substantial, underpinning massive investment in state of the art trawling and processing gear. The harsh Arctic and North Atlantic conditions require gear that can withstand extreme weather, favoring premium products with long lifespans. Norway is also a leader in aquaculture, particularly salmon farming, which drives a specialized segment of the market for containment nets, feeding systems, and harvesting tools. The recreational sector is equally significant, with ice fishing and sea angling being popular national pastimes supported by a strong culture of outdoor life. The government actively funds research into selective fishing technologies to minimize bycatch, accelerating the adoption of smart sensors and modified nets. Norwegian companies are at the forefront of developing eco friconcludely gear, influencing trconcludes across Europe. The high disposable income of the population allows for the procurement of top tier equipment, sustaining a high value market despite the relatively compacter population size.

Spain Fishing Gear Market Analysis

Spain commands a substantial share of the European fishing gear market by leveraging its extensive Mediterranean and Atlantic coastlines to support a diverse fishing indusattempt. The counattempt is a hub for both compact scale artisanal fishing and large industrial fleets, creating a bifurcated demand for varied types of gear. As per the Spanish Minisattempt of Agriculture, Fisheries and Food, the national fleet comprises a large number of vessels, building it one of the largest in the EU. The Mediterranean region favors static gear like traps and gillnets, while the Atlantic fleet utilizes more dynamic trawling equipment. Spain is also a premier destination for recreational fishing tourism, attracting visitors annually who contribute to the sales of rods, reels, and charter boat supplies. The warm climate allows for year round fishing activities, sustaining consistent demand throughout the year. Recent efforts to combat overfishing in the Mediterranean have led to regulatory modifys promoting selective gear, driving a replacement cycle for compliant equipment. The growth of sport fishing tournaments along the Costa del Sol and the Balearic Islands has further stimulated the market for high performance lures and tackle. Local manufacturing capabilities remain strong, providing cost effective solutions for the domestic market while exporting to neighboring countries. The cultural significance of seafood in Spanish cuisine ensures continued political and economic support for the fishing sector.

France Fishing Gear Market Analysis

France holds a considerable share of the regional market due to its access to multiple marine basins including the Atlantic, the Mediterranean, and the North Sea, as well as extensive inland waterways. The French market is characterized by a balanced mix of commercial and recreational segments, with a strong emphasis on quality and tradition. As per FranceAgriMer, the French fishing fleet is diverse, ranging from compact coastal boats to large offshore trawlers, each requiring specific gear configurations. The counattempt has a passionate recreational angling community, particularly for freshwater species like pike and zander, driving steady sales of rods and lures. The implementation of the EU Green Deal has prompted French authorities to enforce stricter environmental standards, accelerating the shift toward eco friconcludely and selective fishing gear. France is also a leader in marine research, collaborating with indusattempt players to test and deploy innovative technologies such as acoustic deterrents and smart nets. The tourism sector along the French Riviera and the Atlantic coast boosts seasonal sales of sea angling equipment. Government subsidies for fleet modernization have supported operators upgrade to more efficient and compliant gear. The presence of several renowned European fishing gear brands headquartered in France strengthens the domestic supply chain and fosters innovation. The market is mature but continues to evolve in response to sustainability mandates and altering consumer preferences.

Denmark Fishing Gear Market Analysis

Denmark secures a notable share of the European fishing gear market by punching above its weight due to its highly efficient and technologically advanced fishing indusattempt. Located at the gateway to the Baltic and North Seas, Denmark serves as a critical hub for maritime activities in Northern Europe. As per Statistics Denmark, the counattempt possesses one of the most modern fishing fleets in the world, with a high degree of automation and digitalization. This technological sophistication drives demand for cutting edge gear, including GPS integrated systems, automated sorting nets, and precision sensors. Denmark is also a major player in aquaculture, particularly in trout and eel farming, which creates a specialized niche for containment and harvesting equipment. The Danish population has a strong tradition of recreational fishing, with simple access to coastlines and numerous lakes fostering a broad base of amateur anglers. The government’s commitment to sustainability is evident in its early adoption of selective fishing methods and support for green technology initiatives. Danish companies are often pioneers in developing biodegradable fishing materials and energy efficient gear. The central location facilitates distribution to other Nordic and Baltic markets, enhancing its regional influence. High standards of living and environmental awareness among consumers ensure a preference for premium, sustainable products, shaping a distinct and forward seeing market profile.

COMPETITIVE LANDSCAPE

The competition in the Europe fishing gear market is characterized by a dynamic mix of established global giants and specialized regional manufacturers vying for dominance through innovation and brand loyalty. Large multinational corporations leverage their extensive distribution networks and massive research budreceives to introduce cutting edge technologies that set indusattempt standards. These leaders often compete on product quality durability and technological integration rather than price alone creating a premium market environment. Smaller niche players differentiate themselves by focapplying on specific local fishing traditions or unique environmental conditions such as Arctic ice fishing or Mediterranean bottom trawling. The rise of sustainability regulations has intensified competition as companies race to develop eco friconcludely materials and selective gear solutions that comply with strict European Union mandates. Digital channels have lowered enattempt barriers for new entrants who utilize social media and direct sales models to challenge traditional retail dominance. Mergers and acquisitions are frequent as firms seek to consolidate market share and acquire proprietary technologies. This fiercely competitive landscape drives continuous improvement in product performance and environmental stewardship benefiting both commercial operators and recreational anglers throughout the continent.

KEY MARKET PLAYERS

Some of the notable key players in the Europe fishing gear market are

- Shimano Inc.

- Pure Fishing Inc.

- Globeride Inc.

- Rapala VMC Corporation

- Johnson Outdoors Inc.

- PRADCO Outdoor Brands

- Maver UK Ltd.

- Okuma Fishing Tackle Co. Ltd.

- Gamakatsu Co. Ltd.

- O. Mustad & Son A.S.

Top Players in the Market

- Pure Fishing stands as a global leader with a profound impact on the Europe fishing gear market through its extensive portfolio of iconic brands. The company manufactures premium rods, reels, lines, and lures that cater to both recreational anglers and professional guides across the continent. Pure Fishing recently intensified its focus on sustainability by launching initiatives to reduce plastic waste in packaging and developing eco friconcludely product lines. The firm has also invested heavily in digital platforms to engage directly with consumers through educational content and virtual fishing communities. Their commitment to innovation is evident in the integration of advanced materials like carbon fiber and specialized coatings that enhance durability in harsh European marine environments. By collaborating with local fisheries management bodies, Pure Fishing ensures its products meet strict regulatory standards for selectivity and conservation. These strategic shifts reinforce their reputation as a responsible indusattempt steward while expanding their reach into emerging recreational segments throughout Northern and Southern Europe.

- Shimano Inc maintains a dominant presence in the Europe fishing gear market by delivering high precision engineering and technological excellence in fishing reels and components. The Japanese giant has deeply embedded itself in the European ecosystem by sponsoring major fishing tournaments and partnering with local charter operators to revealcase product reliability. Shimano recently expanded its manufacturing footprint within Europe to reduce supply chain latency and better serve regional demand fluctuations. The company introduced a new series of electric reels designed specifically for the deep sea fishing conditions found in the Atlantic and Mediterranean waters. Their recent actions include the launch of a comprehensive recycling program for old fishing gear, aligning with European Union circular economy goals. Shimano also leverages data analytics to understand angler preferences, allowing for rapid product iteration and customization. This proactive approach to customer engagement and environmental responsibility solidifies their position as a preferred choice for serious anglers seeking performance and durability in challenging European waters.

- Rapala VMC Corporation exerts significant influence over the Europe fishing gear market through its legconcludeary status in lure manufacturing and fish finding technology. The Finnish headquartered company leverages its deep understanding of Nordic and Baltic fishing conditions to design products that resonate with local anglers. Rapala recently strengthened its market position by acquiring niche brands specializing in ice fishing equipment to capitalize on the growing winter sports sector. The corporation has pioneered the development of smart lures equipped with sensors that transmit data to smartphones, revolutionizing how anglers interact with their gear. Their commitment to sustainable practices is highlighted by the introduction of lead free tackle options to protect aquatic ecosystems from heavy metal contamination. Rapala actively participates in stock restoration projects across Europe, fostering goodwill among conservation groups and regulatory bodies. By continuously innovating in both traditional bait designs and modern electronic solutions, Rapala ensures its relevance across diverse fishing cultures from the Arctic Circle to the Mediterranean Sea.

Top Strategies Used by Key Market Participants

Key players in the Europe fishing gear market primarily employ product innovation strategies to maintain competitive advantages and meet evolving regulatory demands. Companies frequently invest in research and development to create lightweight durable materials and smart technologies that enhance fishing efficiency. Strategic acquisitions allow major firms to expand their brand portfolios and enter niche segments such as ice fishing or eco friconcludely tackle. Partnerships with local distributors and charter services support manufacturers penetrate regional markets more effectively and build brand loyalty among conclude utilizers. Sustainability initiatives have become central to corporate strategies as firms seek to align with European Union environmental goals and appeal to conscious consumers. Digital transformation efforts include the launch of direct to consumer online platforms and mobile applications that provide educational content and community engagement. These multifaceted approaches enable market participants to navigate complex regulatory landscapes while driving growth through enhanced product offerings and strengthened customer relationships across the diverse European region.

MARKET SEGMENTATION

This research report on the European fishing gear market has been segmented and sub-segmented based on categories.

By Type

- Saltwater Fishing Equipment

- Freshwater Fishing Equipment

- Fly Fishing Equipment

- Ice Fishing Equipment

- Spearfishing Equipment

By Gear

- Rods

- Reels

- Lines

- Hooks

- Lures

- Baits

- Nets

- Traps

By Distribution Channel

- Sporting Goods Stores

- Online Retailers

- Catalog Retailers

- Specialty Shops

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe