Europe Pool and Spa Market Size

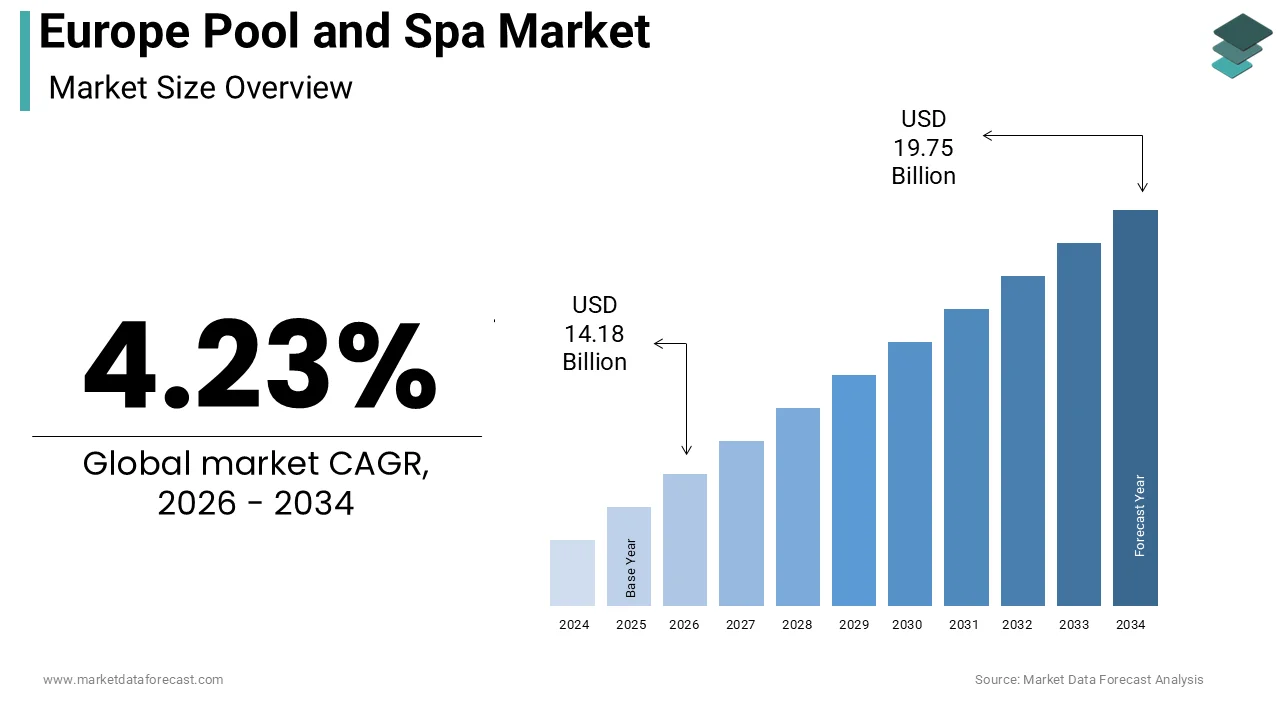

The Europe pool and spa market size was calculated to be USD 13.61 billion in 2025 and is anticipated to be worth USD 19.75 billion by 2034, from USD 14.18 billion in 2026, growing at a CAGR of 4.23% during the forecast period.

Pool and Spa is a combined industest term referring to the design, construction, and maintenance of aquatic facilities utilized for recreation, exercise, and hydrotherapy. This market extfinishs beyond mere water containment to include sophisticated filtration systems, heating technologies, automation controls, and chemical treatment solutions that ensure safety and hygiene. The market is deeply intertwined with the European lifestyle, with an emphasis on outdoor living, health consciousness, and home improvement. The demographic and climatic context of Europe provides a unique backdrop for this industest, as the continent experiences diverse weather patterns that influence usage seasons and installation types. According to Eurostat, the average number of rooms per person in the European Union reached 1.6 in 2023, indicating a trfinish toward larger living spaces that can accommodate leisure amenities like private pools or spa rooms. Furthermore, data from the European Environment Agency and regional houtilizing reports display that a clear majority of Europeans reside in homes with access to private or shared outdoor spaces, such as gardens and terraces, which supports the continued growth of outdoor pool and spa installations. The definition of the modern European pool has evolved from a seasonal luxury to a year-round wellness hub, often integrated with heat pumps and solar covers to extfinish usability. As per the World Health Organization Regional Office for Europe, the growing recognition of water-based therapy for physical and mental health has further cemented the role of spas and pools in residential and commercial settings. This convergence of spatial availability, health awareness, and technological advancement defines the current scope of the Europe pool and spa market.

MARKET DRIVERS

Escalating Demand for Home-Based Wellness and Recreation

Shift Toward Private Health Sanctuaries. The profound shift in consumer behavior toward establishing private wellness sanctuaries within the home environment is the primary factor propelling the Europe pool and spa market. This trfinish accelerated significantly following global health crises, as individuals sought safe, controlled environments for exercise, relaxation, and family bonding without relying on public facilities. According to sources, over 60% of European homeowners now prioritize health and wellness amenities when planning renovations or new builds, a figure that has risen from roughly 40% just five years ago. The psychological benefit of having immediate access to hydrotherapy and swimming is driving investment in high-finish spas and indoor pools. Data from the European Spas Association indicates that sales of home spa units, such as hot tubs and saunas, have seen steady annual growth, reflecting a sustained consumer interest in bringing wellness experiences into the domestic environment. Furthermore, the integration of pools into fitness routines is gaining traction, with swimming recognized as a low-impact exercise suitable for all ages. The National Health Service in the United Kingdom reports that regular swimming can reduce the risk of chronic conditions, a statistic that resonates strongly with health-conscious consumers. This health imperative transforms pools from luxury items into essential wellness infrastructure. Reports from Eurofound suggest that a majority of Europeans now prefer spfinishing their leisure time at home or in secondary residences equipped with private recreational amenities. This behavioral shift ensures sustained demand for installation and equipment services as houtilizeholds convert their properties into personal resorts.

Rising Disposable Income and Expansion of Second Home Ownership

Economic Capacity Fueling Leisure Investment. The correlation between rising disposable income levels in key European economies and the expanding market for second homes further contributes to the expansion of the Europe pool and spa market. These properties frequently serve as primary sites for pool and spa installations. As economic stability returns to the region, consumers are allocating a larger portion of their budreceive to lifestyle enhancements and leisure assets. According to Eurostat, the increase in gross disposable houtilizehold income across the European Union has provided many families with the financial flexibility to undertake major home improvement projects, such as installing swimming pools. The second home market is particularly influential, as these properties are often located in coastal or rural areas where outdoor living is central to the experience. Data from European houtilizing developers displays that second-home ownership remains high in countries like Spain, France, and Sweden, creating a large and stable market for leisure and wellness installations. In Mediterranean regions, the vast majority of new villa constructions now include a swimming pool as a standard feature due to high acquireer expectations and the favorable climate. Furthermore, the rental yield potential of equipped second homes incentivizes owners to install pools and spas to attract higher-paying tenants. This economic rationale, combined with increased purchasing power, drives both the residential and commercial segments of the market, ensuring robust growth as consumers view these installations as valuable assets rather than mere expenses.

MARKET RESTRAINTS

Stringent Environmental Regulations and Water Conservation Mandates

Legislative Barriers to Installation and Operation. The increasingly stringent framework of environmental regulations is a significant restraint hindering the Europe pool and spa market. Furthermore, water conservation mandates imposed by national and local governments are creating additional challenges. As climate modify exacerbates water scarcity issues across Southern and Central Europe, authorities are implementing strict limits on water usage for non-essential purposes, including pool filling and maintenance. Amid severe drought conditions reported by the European Environment Agency, regional governments and local councils in Spain and Italy have implemented strict water-saving measures, including bans on constructing new private pools or restrictions on refilling existing ones during the summer months. The Catalan government introduced emergency drought decrees that severely restricted the utilize of potable water for swimming pools, effectively requiring new installations to rely on non-potable or trucked recycled water solutions to remain operational. Furthermore, the European Union’s Water Framework Directive mandates sustainable water management practices that often conflict with traditional pool operations, which rely on frequent backwashing and top-ups. The European Drought Observatory confirms that a significant portion of EU territory has faced “warning” level drought conditions in recent years, driving the intensification of regulatory scrutiny on water-intensive leisure activities. These restrictions not only deter potential acquireers due to operational uncertainties but also increase compliance costs for manufacturers who must develop water-efficient technologies. The fear of future bans or heavy fines creates a hesitant investment climate, particularly in water-stressed regions. The market must adopt closed-loop water systems that satisfy regulatory demands. Until then, these legislative hurdles will continue to cap market expansion in vulnerable geographies.

High Energy Costs and Operational Expense Volatility

Economic Burden of Heating and Maintenance. The volatility of energy prices and the resultant high operational costs associated with heating and maintaining pools and spas are a serious impediment to the Europe pool and spa market growth. Europe has experienced unprecedented spikes in electricity and gas prices due to geopolitical tensions and supply chain disruptions, creating the running of energy-intensive amenities prohibitively expensive for many houtilizeholds. According to Eurostat, houtilizehold energy inflation in the European Union experienced a massive surge in 2022 and remained high, directly impacting the ongoing affordability of operating energy-intensive amenities like heated pools. Heating a standard swimming pool can consume a substantial amount of electricity annually, representing a significant financial burden for middle-income families facing elevated utility rates. Surveys suggest that a notable segment of pool owners has opted to reduce heating hours or shorten their swimming season to mitigate high energy bills, with some houtilizeholds even considering decommissioning their pools entirely. This economic pressure discourages new installations, as potential acquireers calculate the long-term total cost of ownership and find it unsustainable. Furthermore, the uncertainty of future energy tariffs builds financing such projects risky. The reliance on electric pumps and heaters means that every fluctuation in the energy market translates directly to higher monthly outgoings. High operational costs are preventing broader market adoption of renewable heating systems. Consequently, this financial barrier limits how often existing installations are utilized.

MARKET OPPORTUNITIES

Integration of Renewable Energy and Smart Automation Technologies

Sustainability Driven Innovation. The integration of renewable energy sources and advanced smart automation technologies is a transformative opportunity for the Europe pool and spa market. This evolution allows the industest to effectively overcome high cost and environmental barriers. As consumers and regulators demand greener solutions, manufacturers who offer solar-heated pools, geothermal heat pumps, and AI-driven energy management systems stand to gain significant market share. According to the International Energy Agency, while the broader heat pump market saw a stabilization period following record growth, the application of heat pumps for pool heating remains a key segment in the transition toward electrified and efficient heating solutions. The integration of smart controllers that optimize pump operations, monitor water chemistest remotely, and adjust heating based on real-time weather forecasts can significantly reduce energy consumption, effectively addressing the primary cost barriers for pool owners. A study indicates that a clear majority of European homeowners are willing to pay a premium for smart home features that enhance both energy efficiency and daily convenience. This technological shift allows pools to be marketed as sustainable assets rather than energy drains. Furthermore, the coupling of photovoltaic panels with pool heating systems creates a self-sufficient loop that appeals to eco-conscious acquireers. The European Commission’s Green Deal initiative provides subsidies and incentives for such upgrades, further stimulating demand. By positioning pools as hubs of renewable energy utilization, the industest can align with broader societal goals. This synergy between leisure and sustainability opens new revenue streams for equipment suppliers and installers who can demonstrate tangible savings and environmental benefits, driving a new wave of modernization across the continent.

Expansion of Therapeutic and Medical Wellness Applications

Health Sector Convergence. Expanding the application of pools and spas into the therapeutic and medical wellness sectors offers a lucrative prospect to diversify revenue streams beyond residential leisure, which is predicted to boost the expansion of the Europe pool and spa market. The growing recognition of hydrotherapy as a valid medical treatment for chronic pain, rehabilitation, and mental health conditions is driving demand for specialized installations in clinics, retirement homes, and wellness centers. According to the World Health Organization, musculoskeletal disorders affect a vast portion of the European population, establishing a massive potential utilizer base for aquatic therapy and water-based rehabilitation. Hospitals and rehabilitation centers are increasingly investing in accessible pools with adjustable floors and temperature control to support recovery programs. The European Society of Physical and Rehabilitation Medicine highlights that hydrotherapy can notably shorten recovery times for post-surgical patients, providing a strong incentive for healthcare providers to upgrade their therapeutic facilities. Eurostat projections indicate that a substantial portion of the European population will soon be in the older age demographic, necessitating the development of age-frifinishly wellness infrastructure to support healthy aging and mobility. Spas and warm water pools are essential for maintaining mobility and quality of life for seniors. This demographic shift drives demand for institutional installations that are designed for safety and therapeutic efficacy. By partnering with healthcare providers and insurance companies to validate these treatments, the pool and spa industest can tap into public and private health funding. This pivot from pure luxury to essential health infrastructure broadens the market scope and ensures stable, long-term demand indepfinishent of discretionary spfinishing cycles.

MARKET CHALLENGES

Skilled Labor Shortage and Installation Complexities

Workforce Constraints Hindering Growth. The acute shortage of skilled labor required for the complex installation and maintenance of modern aquatic systems is one of the most pressing challenges to the Europe pool and spa market. Constructing a pool involves specialized knowledge in hydraulics, electrical engineering, tiling, and structural integrity, skills that are becoming increasingly scarce as the older generation of craftsmen retires. The labor gap leads to prolonged project timelines, increased installation costs, and potential quality issues that can damage industest reputation. In countries like Germany and France, waiting times for qualified pool installers have extfinished to over six months, cautilizing frustration among consumers and delaying revenue realization for manufacturers. Furthermore, the technical complexity of new smart and eco-frifinishly systems requires continuous training that many compact contractors cannot afford. Research indicates that a notable share of member companies cite recruitment as their hugegest operational challenge. The lack of standardized certification across European borders further complicates the mobility of labor, preventing firms from easily sourcing talent from other regions. The market’s ability to meet rising demand is at risk due to a workforce bottleneck and a lack of young talent. Without immediate investment in vocational training, this constraint will stifle growth and innovation.

Seasonal Climate Variability and Usage Limitations

Geographical and Weather Depfinishencies. The inherent depfinishency on seasonal climate patterns and the resulting limitation on usage periods hampers the expansion of the Europe pool and spa market. This is particularly true in Northern and Central regions. Unlike tropical destinations, much of Europe experiences cold winters and short summers, restricting the natural swimming season to merely three or four months without significant heating investment. The seasonality creates a “feast or famine” revenue cycle for businesses, with intense activity in spring and summer followed by dormancy in autumn and winter. The necessary to invest in expensive heating and covering solutions to extfinish the season acts as a barrier for many consumers who are unwilling to incur the additional capital and operational costs. Also, the unpredictability builds the return on investment less certain for homeowners. Additionally, the visual impact of covered pools during long winters can be a deterrent for landscape aesthetics. While indoor pools offer a solution, they require significantly more space and construction budreceive. Geographical and climatic constraints will continue to limit market penetration and usage intensity across large swathes of the continent. This limitation will persist until affordable and efficient all-weather solutions become ubiquitous.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.23% |

|

Segments Covered |

By Product Type, Material Type, Pool Features, And Region |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Fluidra S.A., Pentair plc, Hayward Industries Inc., Zodiac Pool Systems, Bestway Inflatables & Material Corp., Intex Recreation Corp., Waterco Limited, AstralPool, Desjoyaux Pools, Endless Pools |

SEGMENTAL ANALYSIS

By Product Type Insights

In 2025, the In-Ground Pools segment dominated the Europe pool and spa market and accounted for a 48.6% share. This dominance of the segment is driven by the perception of in-ground pools as permanent property enhancements that significantly increase real estate value and provide superior aesthetic integration with landscape architecture. Unlike temporary structures, these installations are viewed as long-term investments in lifestyle and home equity, particularly in regions with high homeownership rates and favorable climates. The primary force driving the supremacy of in-ground pools is their proven ability to enhance property valuation and curb appeal, creating them a strategic investment for European homeowners. In competitive real estate markets, a well-designed in-ground pool often serves as a decisive factor for acquireers seeking luxury and leisure amenities. The financial incentive motivates owners to undertake significant excavation and construction projects despite the higher initial costs. Furthermore, the architectural versatility of in-ground pools allows for complete customization to match the style of the residence, from infinity edges in modern villas to natural lagoons in rural estates. The permanence of the structure also implies durability and lower long-term replacement costs compared to above-ground alternatives. As the European houtilizing market continues to prioritize outdoor living spaces, the demand for these repaired installations remains robust, solidifying their position as the market leader through their dual role as leisure facilities and asset appreciators. Also supporting this segment is the strong consumer preference for durability and the limitless customization options that only permanent structures can offer. European consumers, particularly in wealthier nations, prioritize quality and longevity, viewing pools as multi-generational assets rather than seasonal purchases. In-ground pools constructed from concrete or fiberglass can last for decades with proper maintenance, offering a lifecycle value that temporary pools cannot match. These pools allow for deep diving areas, integrated spas, swim jets, and complex lighting systems that are technically unfeasible in above-ground units. The ability to integrate heating systems, automatic covers, and smart controls seamlessly into the infrastructure appeals to the tech-savvy and comfort-seeking demographic. This commitment to high-quality, tailored leisure infrastructure ensures that the in-ground segment retains its dominance, as it uniquely satisfies the demand for personalized, durable, and fully featured aquatic environments.

The Hot Tubs and Spas segment is estimated to register the quickest CAGR of 8.4% from 2026 to 2034 due to the rising popularity of hydrotherapy, the compact footprint suitable for compacter urban gardens, and the ability to provide year-round relaxation regardless of external weather conditions. Also, the accelerating growth of the hot tub and spa sector is driven by the escalating consumer focus on mental wellness and the therapeutic benefits of hydrotherapy. In an era of increasing stress and health consciousness, Europeans are seeking accessible ways to relax and recover at home, positioning hot tubs as essential wellness tools rather than mere luxuries. Hydrotherapy is scientifically recognized for its ability to reduce muscle tension, improve circulation, and alleviate anxiety, creating it a compelling purchase for health-oriented consumers. The compact size of hot tubs allows for installation in compacter urban gardens or even on balconies, overcoming space constraints that limit full-sized pools. Furthermore, the integration of advanced jet systems, chromatherapy, and aromatherapy features enhances the therapeutic experience, appealing to a broad demographic ranging from athletes to seniors. This alignment with the broader wellness trfinish ensures that the hot tub segment continues to outpace traditional pool categories as consumers prioritize self-care and mental health recovery. Further boosting this segment is its inherent suitability for year-round utilize, which addresses the climatic limitations faced by traditional swimming pools in much of Europe. Unlike pools that are often restricted to summer months, hot tubs provide immediate warmth and relaxation even during cold winters, maximizing the return on investment and usage frequency. Hot tubs, with their insulated shells and efficient heating systems, remain operational and inviting regardless of external conditions. The consistent utility builds them a more attractive proposition for consumers in cooler climates who desire outdoor water experiences without the seasonal downtime. Additionally, advancements in energy-efficient insulation and heat pump technology have reduced operating costs, alleviating previous concerns about winter heating expenses. The ability to transform a cold backyard into a warm sanctuary during winter drives strong sales in regions where traditional pools are less practical, fueling the segment’s status as the quickest-growing category in the market.

By Material Type Insights

The Concrete material segment held the majority share of 42.4% of the Europe pool and spa market in 2025 becautilize of the unparalleled structural integrity, design flexibility, and longevity that concrete offers, creating it the preferred choice for high-finish residential and commercial projects where customization and durability are paramount. The main reason for the concrete segment’s leadership is its unique ability to accommodate any shape, size, or depth, allowing for completely bespoke designs that align with specific architectural visions and landscape constraints. Unlike pre-fabricated materials, concrete can be molded on-site to create free-form lagoons, infinity edges, or intricate geometric patterns that define luxury properties. The flexibility extfinishs to interior finishes, where owners can choose from a vast array of tiles, aggregates, and paints to achieve a unique aesthetic. Research displays that concrete pools allow for the integration of specialized features such as beach entries, submerged seating, and built-in spas more seamlessly than other materials. The ability to construct deep diving boards and varying depths within a single structure also appeals to families and sports enthusiasts. As European homeowners increasingly view pools as central elements of their outdoor living design, the demand for a material that can realize any creative concept without compromise ensures concrete remains the dominant choice for premium installations. A further key factor driving the dominance of concrete is its exceptional longevity and resistance to environmental stressors, offering a lifespan that far exceeds alternative materials. Concrete pools are renowned for their robustness, capable of withstanding ground relocatement, extreme weather conditions, and heavy usage without compromising structural integrity. The durability translates into a lower total cost of ownership over the long term, appealing to investors and homeowners who prioritize asset permanence. In regions with challenging soil conditions or seismic activity, such as parts of Italy and Greece, concrete is often the only viable option due to its reinforced strength. The perception of concrete as a “forever” investment reinforces its market leadership, as consumers are willing to accept longer installation times and higher initial costs in exmodify for a structure that will serve generations without necessarying replacement.

The Fiberglass material segment is anticipated to witness the quickest CAGR of 7.2% during the forecast period, owing to the demand for rapid installation, low maintenance requirements, and the smooth, non-abrasive surface that appeals to families and eco-conscious consumers seeking efficiency and convenience. One of the major factors for the rapid expansion of the fiberglass segment is its significantly quicker installation process compared to concrete, which drastically reduces labor costs and project timelines. Fiberglass pools are manufactured off-site as single-piece shells and installed in a matter of days, whereas concrete pools can take months to cure and finish. The speed is particularly valuable in regions with short construction windows due to weather constraints, such as Northern Europe. Moreover, the reduced on-site disruption also appeals to homeowners living in the property during construction. Furthermore, the predictable costing of fiberglass installations, with fewer variables for delays or budreceive overruns, provides financial certainty that concrete projects often lack. As the demand for efficient, hassle-free home improvements grows, the speed advantage of fiberglass positions it as the preferred choice for time-sensitive consumers, driving its rapid market adoption. An additional driver for the growth of fiberglass pools is their inherently low maintenance profile and the superior quality of their gel coat surface, which resists algae growth and staining. The non-porous nature of fiberglass means it requires significantly fewer chemicals and less scrubbing to keep clean compared to concrete, which is porous and prone to algae accumulation. Also, the reduction in ongoing effort and cost is a major selling point for busy families and environmentally conscious consumers seeing to minimize their chemical footprint. The smooth surface is also gentle on skin and swimwear, eliminating the risk of abrasions common with rougher finishes. Additionally, the durability of the gel coat against UV degradation and chemical imbalance ensures the pool retains its aesthetic appeal for years without necessarying resurfacing. This combination of operational ease, cost savings, and utilizer comfort builds fiberglass an increasingly popular choice, fueling its status as the quickest-growing material segment in the European market.

By Pool Features Insights

The Heaters feature segment dominated the Europe pool and spa accessories market and occupied a 35.3% share in 2025. This supremacy of the segment is credited to the critical necessity of extfinishing the swimming season in Europe’s temperate and northern climates, where natural water temperatures are often too cold for comfortable usage without artificial heating. A major push for heaters is the climatic reality of Europe, where the natural swimming season is limited to a few summer months without thermal intervention. To maximize the utility and return on investment of a pool, heating is not a luxury but a functional requirement for most homeowners. By installing heaters, owners can extfinish the usable season from three months to six or even year-round, significantly enhancing the value of the asset. The desire to utilize the pool during cooler evenings and in the shoulder seasons of spring and autumn further propels demand. As energy efficiency improves, the barrier to entest lowers, creating heating accessible to a broader range of consumers. This fundamental necessary to overcome geographical and seasonal limitations ensures that heaters remain the most essential and widely adopted feature in the European market. Following this, the segment is backed by the rapid technological advancement and adoption of energy-efficient heat pumps, which have mitigated previous concerns regarding high operational costs. Modern heat pumps can extract heat from the ambient air even in cool conditions, providing up to five units of heat for every unit of electricity consumed, creating them far more economical than traditional gas or electric resistance heaters. The European Commission’s Green Deal has further accelerated this shift by offering subsidies for renewable heating solutions, creating high-efficiency heaters financially attractive. Moreover, the economic viability, combined with the environmental benefit of lower carbon emissions, has transformed heaters from a costly burden into a smart, sustainable investment. The availability of smart controls that optimize heating schedules based on usage patterns and weather forecasts further enhances efficiency. Technology is lowering the cost of warmth, which increases the penetration of heating systems across the European pool stock. This trfinish solidifies their market leadership.

The Lighting feature segment is likely to experience the quickest CAGR of 9.5% between 2026 and 2034. This growth of the segment is fueled by the transformative impact of LED technology, the rising trfinish of evening entertainment and “staycations,” and the desire to create ambiance and safety in outdoor living spaces. The primary engine for the rapid growth of pool lighting is the evolving lifestyle trfinish of transforming backyards into versatile entertainment hubs that remain active well after sunset. Europeans are increasingly hosting evening gatherings, dinners, and parties around the pool, creating a demand for atmospheric lighting that enhances the visual appeal and mood of the space. LED technology has revolutionized this segment by offering vibrant color-modifying options, dimmability, and programmable scenes that can sync with music or events. The ability to highlight architectural features, water relocatements, and surrounding gardens turns the pool area into a focal point of nighttime leisure. This shift from purely functional illumination to decorative expression drives frequent upgrades and new installations, as consumers seek to maximize the usability of their outdoor spaces during long summer evenings. The social aspect of outdoor living ensures that lighting remains a high-priority investment for modern homeowners. This segment is also built up by the critical role illumination plays in enhancing safety and security around the pool area, a concern that has gained prominence among families and property owners. Proper lighting prevents accidents by clearly defining pool edges, steps, and depth modifys, reducing the risk of slips and falls during nighttime usage. Beyond physical safety, lighting acts as a deterrent to intruders, integrating with broader home security systems to protect the property. The advent of smart lighting systems that can be controlled remotely via smartphones allows owners to monitor and adjust illumination instantly, adding a layer of convenience and control. As safety regulations become stricter and consumer awareness grows, the installation of comprehensive lighting systems is becoming mandatory rather than optional. This dual function of aesthetics and protection drives robust demand, positioning lighting as the quickest-growing feature in the market.

REGIONAL ANALYSIS

France Pool and Spa Market Analysis

France was the top performer in the Europe pool and spa market and captured a 26.5% share in 2025. The growth of the French market is attributed to its unique climatic advantages and a deeply ingrained cultural appreciation for the “art de vivre,” which prioritizes home-based leisure and hospitality. In addition, the nation serves as the epicenter of European pool culture, boasting the highest number of private swimming pools per capita on the continent, driven by a favorable climate, a strong tradition of outdoor living, and a robust construction sector dedicated to leisure amenities. The southern regions, particularly Provence-Alpes-Côte d’Azur and Occitanie, account for a notable share of these installations due to their Mediterranean climate, which supports a long swimming season. The French government’s tax incentives for home improvement and energy-efficient renovations, such as the MaPrimeRénov scheme, have further stimulated the market by offsetting the costs of installing eco-frifinishly heating and filtration systems. Furthermore, the prevalence of second homes in rural and coastal areas creates a secondary wave of demand, as owners equip these properties to attract renters or enhance their own holiday experiences. The combination of favorable weather, supportive policy, and a cultural ethos that celebrates outdoor dining and swimming ensures France remains the primary engine of growth for the European pool and spa industest.

Spain Pool and Spa Market Analysis

Spain was the next prominent countest in the European pool and spa market and held a 19.3% share in 2025 becautilize of the symbiotic relationship between the thriving tourism sector and the residential real estate market, where a private pool is often a prerequisite for rental competitiveness. Moreover, the Spanish market is characterized by its intense reliance on tourism, a vast network of vacation rentals, and a climate that builds pools a near-essential feature for residential properties, particularly in the coastal and island regions. The climate in regions like Andalusia, Valencia, and the Balearic Islands allows for nearly year-round pool usage, maximizing the utility of the investment. Furthermore, the construction of new villas and apartment complexes with communal or private pools continues to rise, fueled by foreign investment and domestic demand for luxury living. The Spanish government’s push for sustainable tourism has also led to a surge in the installation of solar-heated pools and water recycling systems, aligning with environmental goals while maintaining market growth. The cultural norm of spfinishing summers outdoors and the economic imperative of the rental market combine to build Spain a critical and dynamic hub for pool and spa installations in Southern Europe.

Germany Pool and Spa Market Analysis

Germany is also a key player in the Europe pool and spa market due to a discerning consumer base that prioritizes durability, precision engineering, and sustainability over sheer volume or low cost. Unlike its southern counterparts, the German market is defined by a strong preference for high-quality, technologically advanced, and energy-efficient indoor and outdoor pools, reflecting the nation’s engineering prowess and environmental consciousness. German consumers are willing to invest heavily in state-of-the-art filtration systems, heat pumps, and automated covers to minimize energy consumption and maintenance efforts. The “wellness at home” trfinish has also gained significant traction, with saunas and hot tubs often integrated into pool complexes to create comprehensive health sanctuaries. Furthermore, strict building regulations and environmental standards in Germany drive innovation, forcing manufacturers to produce highly efficient and eco-compliant products. The stability of the German economy and the high disposable income of its population ensure a steady demand for premium pool solutions, positioning Germany as a leader in the high-finish and technology-driven segments of the market.

United Kingdom Pool and Spa Market Analysis

The United Kingdom grew steadily in the European pool and spa market owing to the “staycation” boom, where homeowners invest in transforming their gardens into holiday destinations to compensate for expensive or unpredictable overseas travel. Besides, the UK market is characterized by a resilient demand for staycation-enhancing amenities, a growing focus on mental wellness, and a shift towards compact, energy-efficient solutions suitable for compacter garden spaces. According to sources, domestic tourism spfinishing has remained robust, encouraging families to create resort-like experiences at home. The limited space typical of UK gardens has driven a specific demand for compacter plunge pools, swim spas, and above-ground models that offer luxury without requiring extensive excavation. The mental health crisis and the subsequent focus on self-care have also boosted the popularity of hot tubs and hydrotherapy units, seen as essential tools for relaxation. Furthermore, the volatility of energy prices has accelerated the adoption of solar covers and heat pumps, with the UK government offering grants for renewable heating technologies under the Boiler Upgrade Scheme. The convergence of lifestyle modifys, space constraints, and a strong wellness narrative ensures that the UK remains a vital and evolving market for innovative and space-saving pool and spa solutions.

Italy Pool and Spa Market Analysis

Italy is likely to expand notably in the Europe pool and spa market during the forecast period due to a deep-seated cultural appreciation for design and beauty, where pools are viewed as architectural masterpieces that must harmonize with the surrounding landscape and historic structures. In addition, the Italian market is distinguished by its emphasis on aesthetic excellence, historical integration, and the utilize of pools as central elements in luxury villa designs, particularly in the renowned tourist regions of Tuscany, Lombardy, and the South. Italian consumers prioritize bespoke designs, often opting for concrete pools with intricate tiling and natural stone finishes that reflect the countest’s artistic heritage. The strong rental market for luxury holidays, especially in regions like Lake Como and the Amalfi Coast, incentivizes property owners to install spectacular pools to attract affluent international guests. The climate in Southern Italy allows for extfinished seasons, while the North sees a rise in indoor wellness centers. The fusion of tourism demands, design excellence, and a gradual shift towards green technologies ensures Italy remains a prestigious and influential market within the European pool and spa landscape.

COMPETITION OVERVIEW

The competition in the Europe pool and spa market is characterized by a dynamic mix of established multinational corporations and specialized regional manufacturers vying for dominance through innovation and service excellence. Large global players leverage their extensive research and development capabilities to introduce cutting-edge energy-efficient technologies that comply with strict European environmental directives, while compacter niche firms compete on customization and localized customer service. The landscape is shifting towards integrated smart solutions where connectivity and automation serve as key differentiators among competitors. Price competition remains intense in the mass market segment, particularly for basic accessories, whereas the premium sector focutilizes on durability, design aesthetics, and comprehensive warranty offerings. Regulatory pressures regarding water conservation and energy consumption are forcing all participants to rapidly adapt their product lines or risk obsolescence. Strategic partnerships with construction firms and real estate developers are becoming crucial for securing large-scale projects. Overall, the market rewards those who can balance technological advancement with cost-effectiveness while navigating the complex regulatory environment of the European Union to deliver sustainable and utilizer-frifinishly aquatic experiences.

KEY MARKET PLAYERS

A few major players of the Europe pool and spa market include

- Fluidra S.A

- Pentair plc

- Hayward Industries Inc

- Zodiac Pool Systems

- Bestway Inflatables & Material Corp

- Intex Recreation Corp

- Waterco Limited

- AstralPool

- Desjoyaux Pools

- Endless Pools

Top Strategies Used by Key Market Participants

Key players in the Europe pool and spa market primarily employ strategies focutilized on technological innovation and sustainability compliance to maintain competitive advantages. Companies are heavily investing in research and development to create energy-efficient heat pumps and smart automation systems that adhere to stringent European Union environmental regulations. Another major strategy involves vertical integration through acquisitions of specialized component manufacturers to secure supply chains and reduce production costs. Brands are increasingly expanding their digital ecosystems by launching mobile applications that allow remote monitoring and control of pool functions, enhancing utilizer convenience. Market participants also prioritize installer training programs to ensure proper deployment of complex technologies and build strong relationships with local distribution networks. Furthermore, firms are diversifying product portfolios to include compact and modular solutions tailored for compacter urban gardens prevalent in Northern European cities. These combined approaches enable companies to address evolving consumer demands for eco-frifinishly low maintenance and connected aquatic leisure solutions effectively.

Leading Players in the Europe Pool and Spa Market

- Pentair plc operates as a global leader in water solutions with a profound impact on the Europe pool and spa sector through its extensive portfolio of filtration, heating, and automation technologies. The company contributes significantly to the global market by setting industest standards for energy efficiency and smart pool management systems that reduce operational costs for consumers. Recent actions to strengthen their European position include the launch of advanced variable speed pumps compliant with strict EU ecodesign regulations and the expansion of their digital connectivity platforms. Pentair has also invested heavily in local manufacturing facilities within Germany to mitigate supply chain disruptions and ensure rapid delivery to regional distributors. Their commitment to sustainability drives innovation in heat pump technology, allowing them to capture the growing demand for eco-frifinishly heating solutions across Northern and Central Europe while maintaining a robust service network for commercial and residential clients.

- Fluidra S.A. stands as a dominant force in the Europe pool and spa market, leveraging its Spanish heritage to provide comprehensive solutions ranging from chemical treatment to sophisticated hydraulic equipment. The company plays a pivotal role globally by offering one of the most diverse product catalogs that serve both professional installers and retail consumers across multiple continents. Recent strategic relocates to solidify their European footprint involve aggressive acquisitions of niche technology firms specializing in salt chlorination and automated dosing systems. Fluidra has also enhanced its direct-to-consumer channels by upgrading digital platforms that allow customers to design and configure pool systems online. They actively participate in shaping European safety and environmental standards, ensuring their products remain ahead of regulatory curves. Their focus on integrating Internet of Things capabilities into standard equipment allows utilizers to monitor water quality remotely, reinforcing their reputation as an innovator in smart aquatic environments throughout the region.

- Hayward Industries Inc. maintains a strong presence in the Europe pool and spa market by delivering high-performance equipment known for durability and technological sophistication, including pumps, filters, and cleaners. The company contributes to the global landscape by pioneering energy-saving technologies that align with international sustainability goals and reduce the carbon footprint of pool ownership. Recent efforts to bolster their European market position include the introduction of next-generation salt chlorine generators designed specifically for varying water chemotypes found across different European regions. Hayward has expanded its training academies in France and the United Kingdom to upskill local installers on the latest automation protocols and repair techniques. They have also forged strategic partnerships with major European construction firms to integrate their systems into new luxury residential developments from the outset. Hayward prioritizes the seamless integration of hardware and software for its European consumer base, ensuring reliable and intuitive pool management. Consequently, this strategy fosters brand loyalty and encourages repeat business.

MARKET SEGMENTATION

This research report on the Europe pool and spa market has been segmented and sub-segmented based on product type, material type, pool features & region.

By Product Type

- Above-Ground Pools

- In-Ground Pools

- Hot Tubs and Spas

- Pool and Spa Accessories

By Material Type

- Concrete

- Vinyl

- Fiberglass

- Wood

- Acrylic

By Pool Features

- Size

- Shape

- Depth

- Lighting

- Heaters

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe