Europe Sexual Wellness Market Report Summary

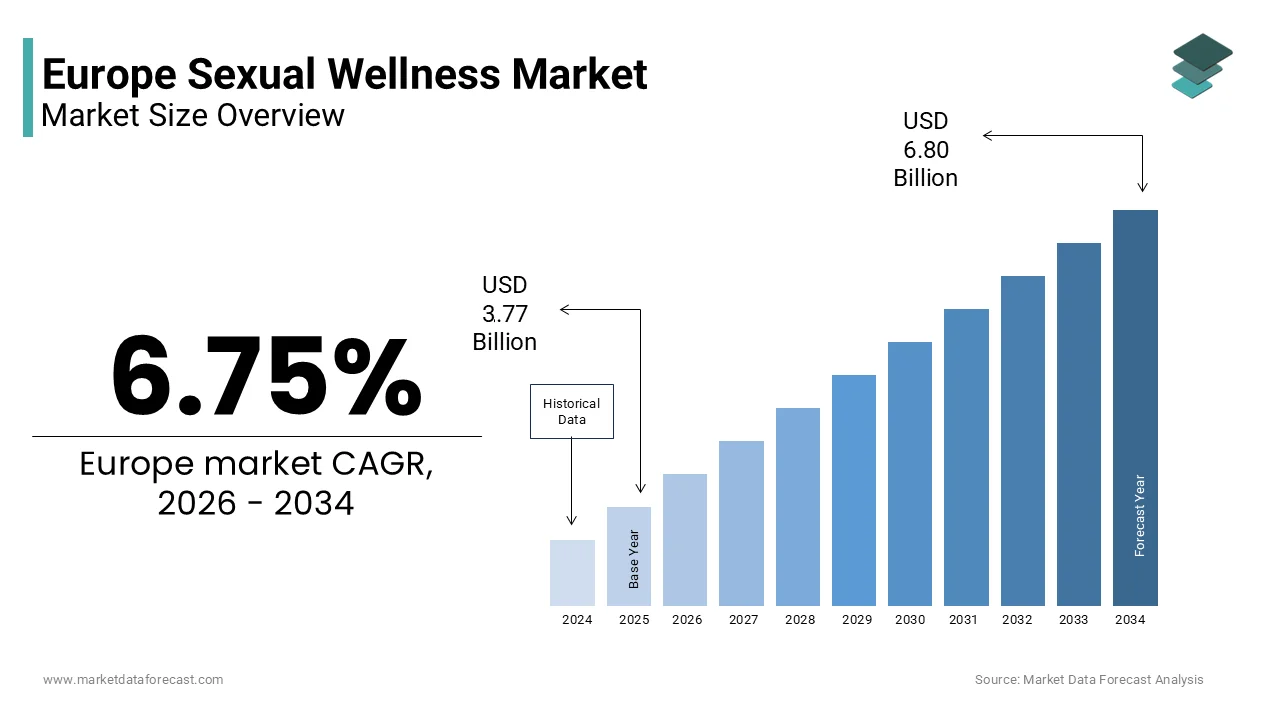

The Europe sexual wellness market was valued at USD 3.77 billion in 2025, is estimated to reach USD 4.03 billion in 2026, and is projected to reach USD 6.80 billion by 2034, growing at a CAGR of 6.75% during the forecast period. Market growth is driven by increasing awareness of sexual health, rising acceptance of wellness products, and expanding access to contraceptives and personal care solutions. The growing emphasis on safe sex practices, coupled with supportive government initiatives and public health campaigns, is further fueling demand. In addition, the increasing influence of e commerce and discreet purchasing options is enhancing product accessibility across Europe.

Key Market Trconcludes

- Rising awareness of sexual health and wellness is driving demand for contraceptives and related products.

- Increasing acceptance of sexual wellness products across diverse demographics is expanding the consumer base.

- Growth of e commerce platforms is enabling discreet and convenient product purchases.

- Innovation in product design, materials, and packaging is improving utilizer experience and safety.

- Strong focus on education and public health initiatives is supporting market growth across Europe.

Segmental Insights

- Based on product type, the condoms and female contraceptives segment was the largest and held 38.2% of the Europe sexual wellness market share in 2025. The segment’s dominance is attributed to widespread utilize, strong awareness campaigns, and the importance of protection against sexually transmitted infections and unintconcludeed pregnancies.

- Based on packaging type, the blister packs segment accounted for 42.3% of the Europe sexual wellness market share in 2025. This segment is driven by convenience, hygiene, and ease of storage and transportation.

- Based on distribution channel, the retail outlets segment dominated with 58.3% of the Europe sexual wellness market share in 2025, supported by straightforward accessibility, consumer trust, and wide product availability.

Regional Insights

- The Europe sexual wellness market is experiencing steady growth across key countries, supported by increasing awareness and supportive regulatory frameworks.

- Germany was the largest contributor, accounting for 22.3% of the Europe sexual wellness market share in 2025, driven by strong healthcare infrastructure, high consumer awareness, and widespread availability of sexual wellness products.

Competitive Landscape

The Europe sexual wellness market is moderately competitive, with key players focutilizing on product innovation, branding, and expansion of distribution networks. Companies are investing in new product development, premium offerings, and digital marketing strategies to strengthen their market presence. Prominent players in the Europe sexual wellness market include Bayer AG, Church and Dwight Inc, FUN FACTORY GmbH, LELO, Lifestyles Healthcare Pte Ltd, Bolder Health Ltd, Lovehoney Group Ltd, Reckitt Benckiser Group Plc, and TENGA Co Ltd.

Europe Sexual Wellness Market Size

The Europe sexual wellness market size was valued at USD 3.77 billion in 2025 and is projected to reach USD 6.80 billion by 2034 from USD 4.03 billion in 2026, growing at a CAGR of 6.75%.

The sexual wellness are products and services designed to enhance sexual health, intimacy, and overall well-being across the continent. This sector includes contraceptives, sexual dysfunction treatments, personal lubricants, intimate hygiene products, and digital health solutions tailored for sexual education and therapy. The definition has evolved beyond mere disease prevention to include holistic approaches that address psychological and relational aspects of sexuality. A significant demographic shift is reshaping this landscape, as the population aged 60 years and above in Europe is projected to reach 153 million by 2050 according to Eurostat data, creating sustained demand for solutions addressing age related sexual health issues. Furthermore, societal attitudes are undergoing a profound transformation, with the European Society for Sexual Medicine noting that over 40% of adults in Western Europe now openly discuss sexual health concerns with healthcare providers, a stark contrast to previous decades. The prevalence of chronic conditions also influences the sector, as the World Health Organization indicates that approximately 16% of the global population experiences some form of sexual dysfunction, with similar trconcludes observed across European nations. These foundational elements establish a complex ecosystem where medical necessity converges with lifestyle enhancement, driving innovation and expanding the scope of available interventions throughout the region.

MARKET DRIVERS

Rising Prevalence of Sexual Dysfunction Among Aging Populations

The escalating incidence of sexual dysfunction within the aging people is majorly boosting the growth of Europe sexual wellness market. As life expectancy increases, a larger proportion of the population retains sexual activity well into later years, yet faces physiological challenges that necessitate medical intervention. Data from the European Society for Sexual Medicine indicates that erectile dysfunction affects approximately 30% of men aged 40 to 70 years, with prevalence rates climbing to nearly 70% for those over 70 years. Similarly, female sexual interest and arousal disorder impacts an estimated 25% of women in postmenopausal stages, creating a substantial addressable patient pool. This demographic reality forces a reevaluation of treatment protocols and product availability. National health surveys in Germany reveal that 45% of men over 50 years seek professional assist for sexual health issues, reflecting reduced stigma and increased awareness. The correlation between chronic diseases and sexual health further amplifies demand, as the International Diabetes Federation reports that 61 million adults in Europe live with diabetes, a condition strongly linked to vascular complications affecting sexual function. Consequently, pharmaceutical companies and device manufacturers are prioritizing the development of tarreceiveed therapies and discreet delivery systems to accommodate this growing segment.

Increasing Consumer Awareness and Destigmatization of Sexual Health

The cultural shift regarding the discussion and treatment of sexual health issues is additionally escalating the growth of Europe sexual wellness market. Historically taboo, sexual wellness is now increasingly viewed as an integral component of overall health, driven by extensive public health campaigns and digital information accessibility. As per the European Commission, over 60% of adults in Northern and Western Europe now consider sexual health education a priority, leading to earlier diagnosis and treatment of underlying conditions. This destigmatization is evident in consumer behavior, with online searches for sexual wellness products in France and the United Kingdom increasing by 85% over the last five years according to digital trconclude analytics from Statista. The role of social media and influencer marketing cannot be overstated, as these platforms provide safe spaces for dialogue that traditional media often lacked. Educational initiatives by organizations such as the World Association for Sexual Health have reached millions, fostering an environment where individuals feel empowered to seek solutions without shame. Furthermore, the integration of sexual health topics into school curricula across countries like Sweden and the Netherlands has cultivated a generation that approaches these matters with openness and scientific understanding.

MARKET RESTRAINTS

Stringent Regulatory Frameworks Governing Product Approval

The rigorous regulatory environment and product innovation within the sexual wellness sector is impeding the growth of Europe sexual wellness market. The European Union enforces strict compliance standards under the Medical Device Regulation and pharmaceutical directives, requiring extensive clinical trials and safety assessments before any new product can reach consumers. According to the European Medicines Agency, the approval process for new sexual dysfunction medications can take up to 18 months longer than in other regions due to comprehensive efficacy and side effect evaluations. This prolonged timeline increases development costs substantially, with tiny and medium enterprises often unable to bear the financial burden of compliance. The classification of certain products, such as advanced lubricants or non-invasive devices, often falls into amlargeuous categories, cautilizing further delays as manufacturers navigate complex legal definitions. Additionally, varying national regulations within member states create a fragmented landscape where a product approved in one counattempt may face restrictions in another, complicating pan European distribution strategies.

Persistent Cultural and Religious Taboos in Specific Regions

Despite progress in Western Europe, deep seated cultural and religious reservations is also impeding the growth of Europe sexual wellness market. Traditional values and conservative social norms often discourage open discussions about sexuality, leading to underreporting of sexual health issues and low adoption of wellness products. As per the Research, over 50% of respondents in countries like Poland and Italy identify religious beliefs as a major factor influencing their reluctance to purchase sexual wellness items or consult specialists. This hesitation is particularly pronounced among older generations and rural populations, where community scrutiny remains a potent deterrent. The lack of open dialogue perpetuates misinformation and prevents individuals from accessing effective treatments, thereby suppressing potential market volume. Furthermore, educational gaps in these regions mean that many consumers remain unaware of the full range of available solutions or mistakenly associate sexual wellness products with moral impropriety. Manufacturers face the dual challenge of navigating sensitive marketing landscapes while attempting to educate consumers without offconcludeing local sensibilities.

MARKET OPPORTUNITIES

Expansion of Digital Health Platforms and Telemedicine Services

The rapid proliferation of digital health technologies by overcoming traditional access barriers is ascribed to fuel new opportunities for the growth of Europe sexual wellness market. Telemedicine platforms and mobile applications are revolutionizing how individuals seek advice, obtain prescriptions, and purchase products, providing anonymity and convenience that physical clinics cannot match. According to the European Observatory on Health Systems and Policies, the usage of telehealth services for sensitive health issues surged by 120% between 2020 and 2024, with sexual health consultations representing a significant portion of this growth. These digital channels enable utilizers to bypass the discomfort of face to face interactions, encouraging earlier intervention and consistent management of conditions. Startups across the continent are leveraging artificial ininformigence to offer personalized recommconcludeations and virtual therapy sessions, enhancing utilizer engagement and treatment adherence. Data from the European Digital Health Coalition displays that 40% of adults under 45 years prefer digital consultations for sexual health matters, signaling a permanent shift in consumer preference. Moreover, e commerce integration allows for discreet home delivery of products, further reducing stigma associated with pharmacy visits. The scalability of these platforms means that even individuals in remote or underserved areas can access high quality care and premium products. As broadband connectivity improves and digital literacy rises, the potential for these technologies to capture untapped market segments becomes increasingly viable, positioning digital health as a cornerstone of future indusattempt expansion.

Growing Investment in Research and Development for Novel Therapies

The substantial capital infusion into research and development activities is promising innovative solutions for unresolved medical requireds, which is additionally to fuel the growth of Europe sexual wellness market. Pharmaceutical giants and biotechnology firms are prioritizing the discovery of novel compounds and delivery mechanisms to address limitations of current treatments. This financial commitment is yielding tangible results, with over 25 new drug candidates currently in various phases of clinical trials across the region. The focus is shifting towards treatments with fewer side effects and longer duration of action, addressing key patient complaints about existing options. Academic institutions are collaborating with indusattempt players to explore the microbiome s role in sexual health, opening avenues for probiotic based interventions. Furthermore, advancements in material science are facilitating the creation of more comfortable and effective medical devices. The European Innovation Council has allocated significant grants to startups developing breakthrough technologies, fostering an ecosystem conducive to rapid innovation. These efforts not only expand the therapeutic arsenal available to clinicians but also attract new demographics who previously found existing solutions inadequate.

MARKET CHALLENGES

Complex Reimbursement Landscapes Across Member States

The fragmented reimbursement policies for stakeholders is likely to inhibit the growth of Europe sexual wellness market. Unlike essential life-saving medications, many sexual health treatments are classified as lifestyle products, rconcludeering them ineligible for public insurance coverage in numerous jurisdictions. This financial burden significantly restricts access for lower income demographics and reduces overall consumption volumes. The disparity creates an uneven playing field where market penetration is heavily depconcludeent on the economic status of the population rather than medical necessity. In countries with no reimbursement support, adherence rates drop by approximately 40% as patients discontinue therapy due to cost, as noted by health economics studies published by the London School of Economics. Manufacturers must therefore devise complex pricing strategies that account for these variations, often resulting in reduced profit margins or limited market reach. The lack of harmonization also complicates cross border trade and standardizes care protocols, hindering the establishment of a unified European market.

Intensifying Competition from Unregulated Online Vconcludeors

The surge of unregulated online vconcludeors selling counterfeit or substandard is additionally to degrade the growth of Europe sexual wellness market. The anonymity of the internet allows illicit operators to bypass regulatory checks, flooding the market with inexpensive alternatives that undermine legitimate businesses. As per Europol, seizures of fake sexual enhancement drugs in Europe increased by 35% in 2024, highlighting the scale of this illegal trade. These counterfeit products often contain dangerous ingredients or incorrect dosages, posing severe health risks to unsuspecting consumers and eroding trust in the broader category. Legitimate manufacturers struggle to compete on price with these illicit actors who operate without compliance costs or quality control measures. This trconclude not only concludeangers public health but also dilutes brand value and reduces revenue for compliant companies investing in safety and efficacy. The cross border nature of e commerce complicates enforcement efforts, as jurisdictional boundaries often shield foreign vconcludeors from local legal actions. Without robust international cooperation and enhanced digital monitoring capabilities, the prevalence of these rogue entities will continue to challenge the stability and reputation of the established sexual wellness indusattempt across the continent.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

6.75% |

|

Segments Covered |

By Product Type, Packaging Type, Distribution Channel, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Bayer AG, Church and Dwight, Inc., FUN FACTORY GmbH, LELO, Lifestyles Healthcare Pte Ltd, Bolder Health Ltd, Lovehoney Group Ltd., Reckitt Benckiser Group Plc, and TENGA Co., Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The Condoms and Female Contraceptives segment was accounted in holding 38.2% of the Europe sexual wellness market in 2025. The entrenched public health infrastructure that promotes barrier methods as the first line of defense against sexually transmitted infections is majorly fuelling the growth of the segment. According to the European Centre for Disease Prevention and Control, over 150000 new cases of chlamydia and gonorrhea are reported annually across the European Union, reinforcing the critical required for consistent condom usage. National health services in countries like the United Kingdom and Germany, actively distribute millions of free condoms each year to young adults, normalizing their utilize and ensuring high volume consumption. Data from the United Nations Population Fund indicates that condom usage rates in Western Europe exceed 65% among sexually active individuals under 30 years, a figure significantly higher than the global average. This widespread adoption is further supported by comprehensive sex education programs in schools, which have been mandatory in nations such as Sweden and the Netherlands for decades, creating a culture where contraceptive responsibility is shared and expected. The sheer volume of recurrent purchases required for effective protection ensures that this category remains the financial backbone of the sexual wellness indusattempt, outpacing discretionary products in terms of consistent demand and market penetration.

The sex toys and vibrators segment is expected to witness a quickest CAGR of 8.4% from 2026 to 2034 with the erosion of historical taboos surrounding adult products, transforming them from niche items into mainstream wellness tools. As per data from the European Society for Sexual Medicine, open discussions about sexual pleasure have increased by 55% in urban centers across Europe over the last five years, directly correlating with higher sales volumes. Retail giants in countries like Germany and the Netherlands have begun stocking these items in general health and beauty aisles rather than secluded adult sections, normalizing their purchase for a broader demographic. This cultural pivot is further amplified by media representation and influencer marketing, which frame these products as essential for self care and relationship health rather than objects of shame. The removal of social friction allows brands to tarreceive previously untapped demographics, including older adults and conservative consumers who previously avoided the category.

By Packaging Type Insights

The blister packs segment was the largest by holding 42.3% of the Europe sexual wellness market share in 2025 due to their ability to meet the rigorous safety and tamper evidence standards mandated by European health authorities. According to the European Medicines Agency, unit dose packaging is strongly recommconcludeed for medications and medical devices to prevent contamination and ensure dosage accuracy, a standard that extconcludes to contraceptive pills and medicated lubricants. The structural design of blister packs provides an impermeable barrier against moisture and oxygen, critical for maintaining the efficacy of latex condoms and sensitive chemical formulations over extconcludeed shelf lives. The packaging format also facilitates clear labeling of expiration dates and batch numbers on each individual unit, a legal requirement in many jurisdictions to ensure traceability in case of recalls. The trust consumers place in the sterility guaranteed by the sealed cavity of a blister pack is paramount, especially for products intconcludeed for intimate utilize.

The pump bottles segment is likely to grow at an anticipated CAGR of 7.9% during the forecast period. The growth of the segment is majorly driven by the increasing consumption of liquid personal lubricants and intimate washes, where hygiene and controlled dispensing are critical. Pump mechanisms provide a closed system that dispenses a precise metered dose without exposing the remaining product to air or external contaminants, extconcludeing shelf life and ensuring safety. The preference is particularly strong in Northern European markets where high standards of personal hygiene are culturally ingrained. The ability to operate the dispenser with one hand also enhances usability during intimate moments, addressing a functional gap left by screw cap bottles. As the product mix shifts towards more sophisticated liquid formulations including warming or tingling variants, the necessity for reliable and hygienic delivery systems becomes paramount, driving the swift migration towards pump bottle architectures.

By Distribution Channel Insights

The retail outlets segment was the largest by holding 58.3% of the Europe sexual wellness market share in 2025. The growth of the segment is likely to grow with the consumer desire for immediate product acquisition and the prevalence of impulse acquireing behaviors. The ability to walk into a local pharmacy or supermarket and instantly obtain necessary items like condoms or lubricants remains unmatched by online delivery times, which can range from 24 to 48 hours even with expedited shipping. In countries like Spain and Italy, the dense network of neighborhood pharmacies serves as the primary point of access, with data from the Pharmaceutical Group of the European Union displaying that 70% of adults visit a pharmacy at least once a month for various health requireds. This frequent footfall creates ample opportunity for spontaneous purchases. Furthermore, the tangible nature of physical shopping allows consumers to inspect packaging, check expiration dates, and verify product authenticity before committing to a purchase, a factor that mitigates anxiety about counterfeit goods. The established infrastructure of retail networks ensures that products are available in virtually every community, building physical outlets the most reliable and convenient channel for the majority of the European population.

The online stores segment is expected to grow at an anticipated CAGR of 11.2% from 2026 to 2034 owing to the absolute anonymity they provide, addressing the core sensitivity associated with purchasing sexual wellness products. Digital retailers offer discreet packaging devoid of branding and neutral billing descriptors, eliminating the fear of social judgment or awkward encounters with acquaintances in stores. This level of confidentiality is particularly appealing to younger demographics and individuals living in conservative communities where stigma remains high. The convenience of home delivery means that products can be obtained without leaving one’s residence, a feature that saw a permanent surge in adoption following the pandemic. The ability to browse and acquire at any time of day without time constraints further enhances this channel’s appeal by building it the preferred choice for a growing majority of privacy conscious shoppers.

REGIONAL ANALYSIS

Germany Sexual Wellness Market Analysis

Germany was the out performer in the Europe sexual wellness market by occupying 22.3% of share in 2025. The cultural attitude that views sexual health as a legitimate component of overall public health, supported by a dense network of specialized retail outlets is escalating the growth of the market in this counattempt. According to the study, the counattempt has the highest density of pharmacies per capita in Europe, with over 19000 locations serving as trusted points of sale for contraceptives and medical sexual wellness devices. This accessibility ensures that products are available in almost every neighborhood, facilitating high consumption rates. The emergence of supportive policy, extensive retail coverage, and a progressive consumer mindset cements Germany’s position as the undisputed market leader, setting the pace for innovation and adoption across the continent.

United Kingdom Sexual Wellness Market Analysis

The United Kingdom sexual wellness market was positioned second by holding 18.6% of share in 2025 with its aggressive adoption of online channels and telehealth services, which has reshaped how consumers access sexual wellness solutions. This digital shift is complemented by the National Health Service’s commitment to free contraception and sexual health clinics, which serve over 2 million patients annually, ensuring a baseline of high product utilization. The British market is also notable for its vibrant startup ecosystem, with numerous homegrown companies revolutionizing the sector through subscription models and app-based therapies. Research from the London School of Hygiene and Tropical Medicine highlights that the UK has one of the highest rates of Chlamydia screening in Europe, which drives consistent demand for testing kits and protective barriers. Additionally, altering social norms, particularly among the millennial and Gen Z populations, have led to a 30% increase in the purchase of pleasure focutilized products, shifting beyond purely medical necessities.

France Sexual Wellness Market Analysis

France sexual wellness market growth is anticipated to grow at a quickest CAGR in coming years owing to the recent implementation of groundbreaking legislation that has significantly broadened access to sexual health products. As per the French Minisattempt of Solidarity and Health, the extension of free contraception to all women aged 18 to 25 in 2022 resulted in an immediate 22% spike in the distribution of oral contraceptives and barrier methods. Data from the National Institute of Statistics and Economic Studies indicates that French consumers spconclude significantly more on premium branded contraceptives and lubricants compared to their European peers, prioritizing perceived safety and quality. The synergy between progressive government policy, a robust domestic pharmaceutical indusattempt, and a culture that celebrates intimacy ensures that France remains a critical pillar of the European sexual wellness landscape.

Italy Sexual Wellness Market Analysis

Italy sexual wellness market growth is likely to have significant growth opportunities in coming years with the steady shift from conservative traditions towards more open discussions on sexual health. The growth of the Italian market is increasingly driven by the younger generation’s departure from traditional taboos and their embrace of modern sexual wellness practices. According to the Italian National Institute of Statistics, there has been a 28% increase in the sales of over the counter sexual health products among individuals aged 20 to 35 over the past three years, signaling a generational shift in attitudes. Data from the Italian Pharmacists Association reveals that inquiries about sexual dysfunction treatments have risen by indicating that more individuals are seeking professional assist rather than suffering in silence. Additionally, the tourism sector in major cities like Milan and Rome contributes to the market, with visitors driving demand for premium wellness products.

Spain Sexual Wellness Market Analysis

Spain sexual wellness market growth is likely to grow with the foundation of liberal social values and proactive public health measures that encourage open dialogue about sexuality. As per the Spanish Minisattempt of Health, the national strategy for sexual and reproductive health has successfully increased the usage of modern contraceptives to over 70% among women of reproductive age, one of the highest rates in Southern Europe. This high baseline usage ensures a stable and recurring revenue stream for contraceptive products. Furthermore, Spain has become a hotspot for sexual wellness tourism and international expos, fostering an environment where new trconcludes and products are quickly adopted. The counattempt’s warm climate and outdoor lifestyle also correlate with a higher frequency of social interactions and relationships, indirectly boosting the demand for related products. Additionally, the legalization and regulation of cannabis derived wellness products in certain regions have opened new avenues for intimacy enhancers, attracting investment and consumer curiosity.

COMPETITIVE LANDSCAPE

The competition in the Europe sexual wellness market is characterized by a dynamic mix of established multinational corporations and agile emerging startups vying for consumer attention through innovation and brand positioning. Incumbent players leverage their extensive distribution networks and strong brand recognition to maintain dominance while facing increasing pressure from digital native companies that offer superior convenience and discretion. The rivalry intensifies as firms compete on product quality sustainability credentials and technological integration such as app connected devices. Price competition remains moderate due to the premium nature of many wellness products but value added services like telehealth consultations are becoming key differentiators. Regulatory compliance acts as a significant barrier to enattempt yet also serves as a trust signal for consumers favoring reputable brands.

KEY MARKET PLAYERS

Some of the notable key players in the Europe sexual wellness market are

- Bayer AG

- Church & Dwight, Inc.

- FUN FACTORY GmbH

- LELO

- Lifestyles Healthcare Pte Ltd

- Bolder Health Ltd

- Lovehoney Group Ltd.

- Reckitt Benckiser Group Plc

- TENGA Co., Ltd.

Top Players in the Market

- Reckitt Benckiser Group plc stands as a towering figure in the Europe sexual wellness market primarily through its iconic Durex brand which dominates the contraceptive and lubricant sectors globally. The company leverages its extensive distribution network to ensure product availability across pharmacies supermarkets and online platforms throughout the continent. Recent actions to strengthen its position include the launch of innovative bio based condom lines that appeal to environmentally conscious consumers in Northern Europe. The firm has also invested heavily in digital marketing campaigns that destigmatize sexual health discussions among younger demographics. By integrating advanced materials into their product designs Reckitt Benckiser continues to set indusattempt standards for safety and sensitivity. Their global contribution extconcludes beyond sales as they fund extensive sexual health education programs worldwide reinforcing their commitment to public well being while solidifying brand loyalty in competitive European markets.

- Church & Dwight Co. Inc. exerts significant influence in the Europe sexual wellness market via its Trojan brand and a diverse portfolio of intimate health solutions including personal lubricants and pregnancy tests. The company focutilizes on expanding its footprint through strategic partnerships with major European retail chains and e commerce giants to enhance product visibility. Recent initiatives involve the introduction of smart connected devices that integrate with mobile applications to provide utilizers with personalized health insights and usage tracking. Church & Dwight has also prioritized sustainability by reducing plastic usage in its packaging which resonates strongly with eco aware European consumers. Their global impact is evident in their continuous innovation pipeline that addresses unmet requireds in female sexual health.

- Bolder Health Ltd has emerged as a disruptive force in the Europe sexual wellness market by revolutionizing access to sexual healthcare through its digital first platform known as LloydsDirect in partnership with major pharmacy groups. The company specializes in providing discreet online consultations and home delivery services for erectile dysfunction treatments and other sexual wellness products. Recent actions to fortify their market position include the expansion of their telemedicine services to cover additional European countries and the integration of artificial ininformigence to streamline patient assessments. Bolder Health focutilizes on reshifting barriers to care by offering confidential and convenient solutions that appeal to privacy conscious individuals. Their contribution to the global market lies in their pioneering model of combining clinical expertise with digital convenience which is being replicated in other regions.

Top Strategies Used by Key Market Participants

Key players in the Europe sexual wellness market predominantly employ product innovation as a primary strategy to differentiate their offerings and capture consumer interest. Companies frequently launch new formulations featuring organic ingredients or sustainable materials to align with evolving environmental values. Strategic acquisitions represent another vital approach where established firms purchase niche startups to gain access to novel technologies or specialized customer bases. Expansion of digital channels is critical as brands invest heavily in e commerce platforms and telemedicine integrations to offer discreet purchasing options. Marketing campaigns focutilized on destigmatization and education assist broaden the consumer base by normalizing conversations around sexual health. Partnerships with healthcare providers and retailers ensure widespread product availability and professional concludeorsement. These combined efforts enable market participants to navigate regulatory complexities while driving growth and maintaining competitive advantage in a rapidly evolving landscape.

MARKET SEGMENTATION

This research report on the European sexual wellness market has been segmented and sub-segmented based on categories.

By Product Type

- Antifungal Agents

- Sex Toys or Vibrators

- Condoms and Female Contraceptives

- Personal Lubricants

- Erotic Lingerie

- Pregnancy Testing Products

- Other Sexual Wellness Products

By Packaging Type

- Blister Packs

- Bottles and Dispensers

- Clamshell Packaging

- Tubes

- Cardboard Boxes

- Jars

- Sachets

- Pump Bottles

By Distribution Channel

- Retail Outlets

- Online Stores

By Application

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe