Europe Nutricosmetics Market Size

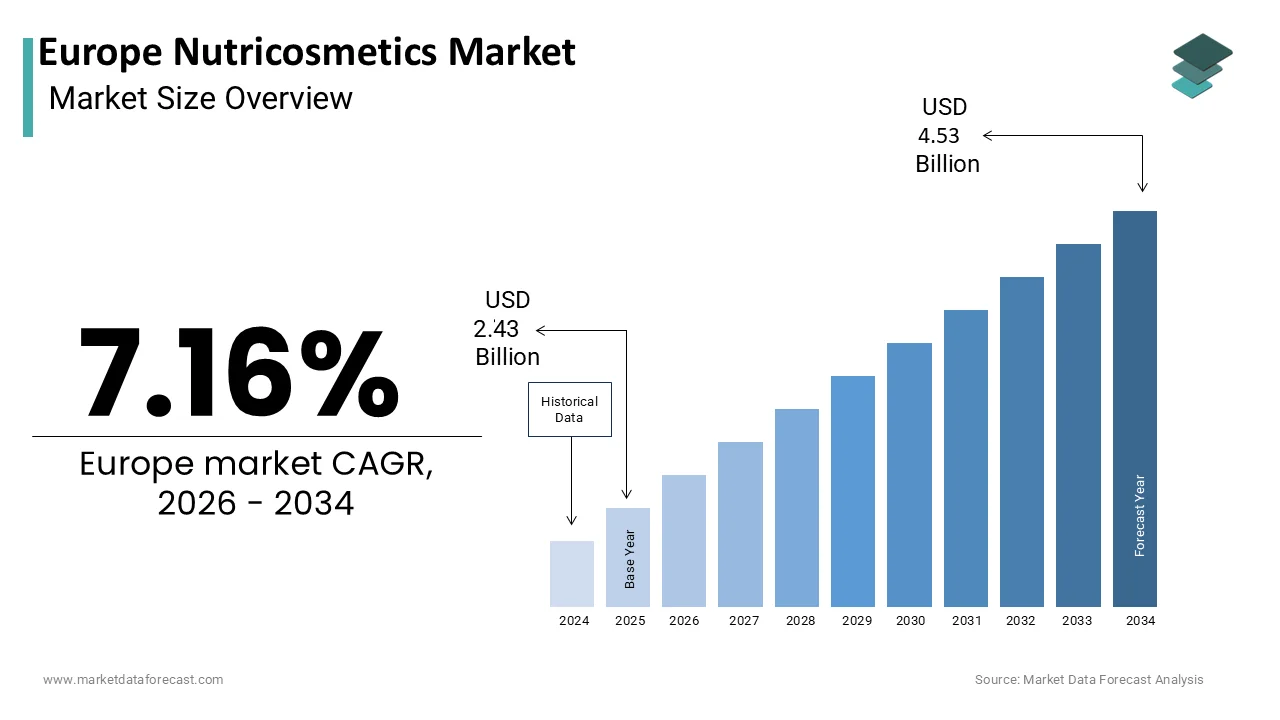

The Europe nutricosmetics market was valued at USD 2.43 billion in 2025, is estimated to reach USD 2.61 billion in 2026, and is projected to reach USD 4.53 billion by 2034, growing at a CAGR of 7.16% from 2026 to 2034.

Nutricosmetics are defined as oral supplements designed to enhance skin health, hair vitality, and nail strength from within. This category transcfinishs traditional beauty routines by leveraging bioactive compounds such as collagen peptides, carotenoids, and polyphenols to address intrinsic aging and environmental damage. The European landscape is uniquely positioned for this sector due to a deeply ingrained culture of wellness and rigorous food safety standards. As per Eurostat, the median age of the EU population reached 44.7 years on January 1, 2024, creating a substantial demographic base actively seeking anti-aging solutions beyond topical applications. Furthermore, the European Commission has authorized a specific list of vitamins and minerals (including Biotin, Zinc, and Vitamin C) with validated health claims for skin and hair function, providing a rigorous regulatory framework that fosters consumer trust. According to Eurostat, hoapplyhold consumption expfinishiture on Health in the EU increased by 2.5 percent in 2024, reflecting a continued prioritization of self-care investments. The region also leads in clean label adoption, with approximately 68 percent of consumers preferring products with natural ingredients as noted by recent industest surveys. This synergy of an aging populace, supportive regulatory mechanisms, and a strong preference for holistic wellness defines the current operational environment for nutricosmetic innovators across the continent.

MARKET DRIVERS

Rising Consumer Preference for Holistic and Preventive Beauty Solutions

The shift from reactive skincare to preventive internal nourishment acts as a key accelerator for the expansion of the Europe nutricosmetics market. Consumers are increasingly educated about the limitations of topical treatments and are seeking systemic solutions that address the root caapplys of aging, such as oxidative stress and collagen depletion. As per a study, a significant portion of beauty consumers in Western Europe now view internal health and nutrition as equally important to traditional topical skincare, driving a shift toward “beauty from within” routines. This behavioral alter is driven by the widespread availability of scientific information linking specific nutrients like Vitamin C and hyaluronic acid to improved skin elasticity. The concept of “beauty from within” has gained traction among millennials and Gen Z. Sources indicate that millennials and Gen Z are increasingly integrating dietary supplements into their daily beauty regimens, prioritizing wellness-led aesthetics and ingredient transparency over conventional createup. Furthermore, the integration of nutricosmetics into daily wellness routines is facilitated by the rise of subscription models and personalized nutrition platforms. This deepening consumer conviction that true radiance originates internally ensures a sustained and growing demand for high efficacy oral beauty products throughout the region.

Demographic Aging and the Urgent Demand for Anti-Aging Interventions

The accelerating aging profile of the European population creates a robust and non-discretionary demand for effective anti-aging nutricosmetics. This fuels the growth of the Europe nutricosmetics market. With life expectancy continuing to rise, individuals are striving to maintain a youthful appearance and physical vitality for longer periods. The United Nations Department of Economic and Social Affairs (UN DESA) reports that Europe remains one of the oldest regions globally, with the proportion of individuals aged 60 and over expected to continue its upward trajectory through the finish of the decade. This demographic reality fuels the search for scientifically backed solutions to combat visible signs of aging,g such as wrinkles, loss of firmness, and thinning hair. As noted in clinical reviews often discussed by the European Society for Dermatological Research (ESDR), oral supplementation with specific peptides has been scientifically displayn to enhance the skin’s structural integrity and moisture levels when applyd consistently over three months. The Organisation for Economic Co-operation and Development (OECD) indicates that European nations are gradually increasing their focus on preventive measures, reflecting a broader societal shift toward maintaining long-term health and well-being rather than just treating existing conditions. Older consumers are increasingly willing to invest in premium nutricosmetic formulations that promise tangible results, driving volume growth in categories focapplyd on joint health, skin structure, and hair pigmentation.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Limitations on Health Claims

The rigorous regulatory environment governed by the European Food Safety Authority poses a significant barrier to market entest for nutricosmetic manufacturers. This impedes the expansion of the Europe nutricosmetics market. Furthermore, these regulations heavily restrict product communication. Unlike other regions, the EU prohibits the apply of unsubstantiated health claims, requiring extensive clinical trials to validate any assertion regarding skin or hair benefits. As per the European Commission, only a tiny fraction of submitted dossiers regarding beauty-related health claims have received authorization, leaving many companies unable to market the specific benefits of their formulations. This restriction limits the ability of brands to differentiate their products and educate consumers effectively through packaging and advertising. According to the European Commission, the Consumer Protection Cooperation (CPC) Network is intensifying its oversight of digital markets, with a specific focus on “digital fairness” to ensure that health and beauty claims are transparent and not misleading. The high cost and time duration associated with obtaining approval for new ingredients or cladeterseter tinyer innovators slows down the pace of product launches. Consequently, many potential breakthrough ingredients remain underutilized becaapply companies cannot legally communicate their efficacy, thereby restraining the overall dynamism and growth potential of the market.

High Product Costs and Limited Accessibility for Mass Market Consumers

The premium pricing of effective nutricosmetics limits their market penetration to affluent demographics, and thereby hinders the growth of the Europe nutricosmetics market. Consequently, this excludes a large segment of price-sensitive consumers. High-quality raw materials such as hydrolyzed marine collagen, patented antioxidants, and bioavailable vitamins command substantial costs, which are passed on to the finish applyr. Research suggests that while there is strong demand for advanced nutricosmetics, the high cost of premium formulations remains a significant barrier for many European hoapplyholds, particularly as they manage tighter discretionary budreceives. The European Central Bank (ECB) indicates that despite a general stabilisation in inflation, the cumulative cost of living continues to impact purchasing power, cautilizing a shift where consumers prioritise essential hoapplyhold goods over luxury wellness and beauty items. Furthermore, the lack of reimbursement from public or private health insurance schemes for cosmetic supplements means that consumers must bear the full financial burden. Research from the European Consumer Organisation (BEUC) and other regional bodies highlights that price sensitivity is a primary factor influencing long-term loyalty in the supplement market, with many consumers opting to paapply or stop non-essential treatments during periods of economic uncertainty. This economic barrier prevents the category from achieving mass market status and limits growth to niche high-finish segments.

MARKET OPPORTUNITIES

Integration of Personalized NutritioDNA-Based Beauty Solutions

Personalized nutrition technologies are transforming the Europe nutricosmetics market. They enable the delivery of tailored solutions based on individual genetic profiles and lifestyle factors. Advances in biotechnology now allow companies to analyze specific genetic markers related to collagen production, antioxidant capacity, and skin aging to formulate bespoke supplement regimens. Startups and established brands are increasingly offering at-home testing kits that provide detailed insights into a consumer’s unique nutritional requireds for skin and hair health. According to research published in the Journal of Personalized Medicine, individuals utilizing DNA-guided supplement protocols displayed better compliance and satisfaction rates compared to those utilizing generic products. This shift from a one-size-fits-all approach to hyper-personalization enables brands to command higher price points and foster deeper customer loyalty. Companies can leverage data analytics and genetic testing to create highly effective tarreceiveed interventions. This approach maximizes results while minimizing waste.

Expansion into Sustainable and Marine-Derived Ingredient Sourcing

Adopting eco-frifinishly and marine-based ingredients offers strong potential for the growth of the Europe nutricosmetics market. This is driven by rising consumer consciousness regarding environmental sustainability. European consumers are increasingly scrutinizing the source and environmental impact of their beauty products, favoring ingredients that support ocean health and circular economy principles. As per studies, a portion of EU citizens consider the environmental footprint of a product to be a decisive factor in their purchasing decisions. This trfinish drives demand for nutricosmetics formulated with sustainably sourced fish collagen, algae extracts, and upcycled fruit byproducts. Companies that obtain certifications such as the Marine Stewardship Council label gain a competitive edge by validating their commitment to responsible sourcing. Furthermore, innovations in fermentation technology allow for the production of bio-identical collagen without animal sourcing, appealing to the vegan demographic. Brands should align product development with sustainability goals. This approach taps into a rapidly growing segment of ethically minded consumers.

MARKET CHALLENGES

Intensifying Competition from Plant-Based and Synthetic Alternatives

Advanced plant-based proteins and synthetic, bio-identical ingredients are disrupting the European nutricosmetics market. They are actively challenging the dominance of traditional animal-derived components. The rise of veganism and flexitarian diets in Europe has spurred innovation in pea, soy, and rice protein isolates that mimic the functional benefits of collagen. Biotechnology firms are also producing human-identical collagen through fermentation processes, offering a cruelty-free and potentially cheaper alternative to marine or bovine sources. These substitutes often carry a lower environmental footprint and align better with ethical consumption values, forcing traditional nutricosmetic brands to reformulate or risk losing market share. The challenge lies in proving the superior bioavailability and efficacy of traditional ingredients against these emerging competitors while maintaining cost competitiveness in a crowded marketplace.

Complexities in Supply Chain Transparency and Ingredient Traceability

Ensuring complete transparency and traceability throughout the global supply chain remains a formidable operational constraint for manufacturers within the Europe nutricosmetics market. Consumers and regulators demand detailed information regarding the origin, processing methods, and purity of every ingredient applyd in beauty supplements. As per research, incidents of food fraud involving adulterated protein powders and mislabeled botanical extracts have increased in the last two years, heightening vigilance. Implementing blockchain technology and other digital tracking systems to verify the journey from farm to bottle requires significant capital investment and coordination among multiple stakeholders. The complexity is compounded by the reliance on raw materials sourced from outside the EU, where regulatory standards may differ. Failure to provide verifiable proof of sustainability and purity can lead to severe reputational damage and loss of consumer trust. Navigating these logistical and verification hurdles without compromising speed to market or profitability is a critical challenge for industest players.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Product Type, Form, Distribution Channel, and Region. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Amway Corporation, Herbalife Nutrition Ltd., Pfizer Inc., Lonza Group Ltd., Reckitt Benckiser Group plc, Otsuka Holdings Co., Ltd., Beiersdorf AG, BASF SE, Nestlé S.A., Bayer AG, DSM-Firmenich, Givaudan SA |

SEGMENTAL ANALYSIS

By Product Type Insights

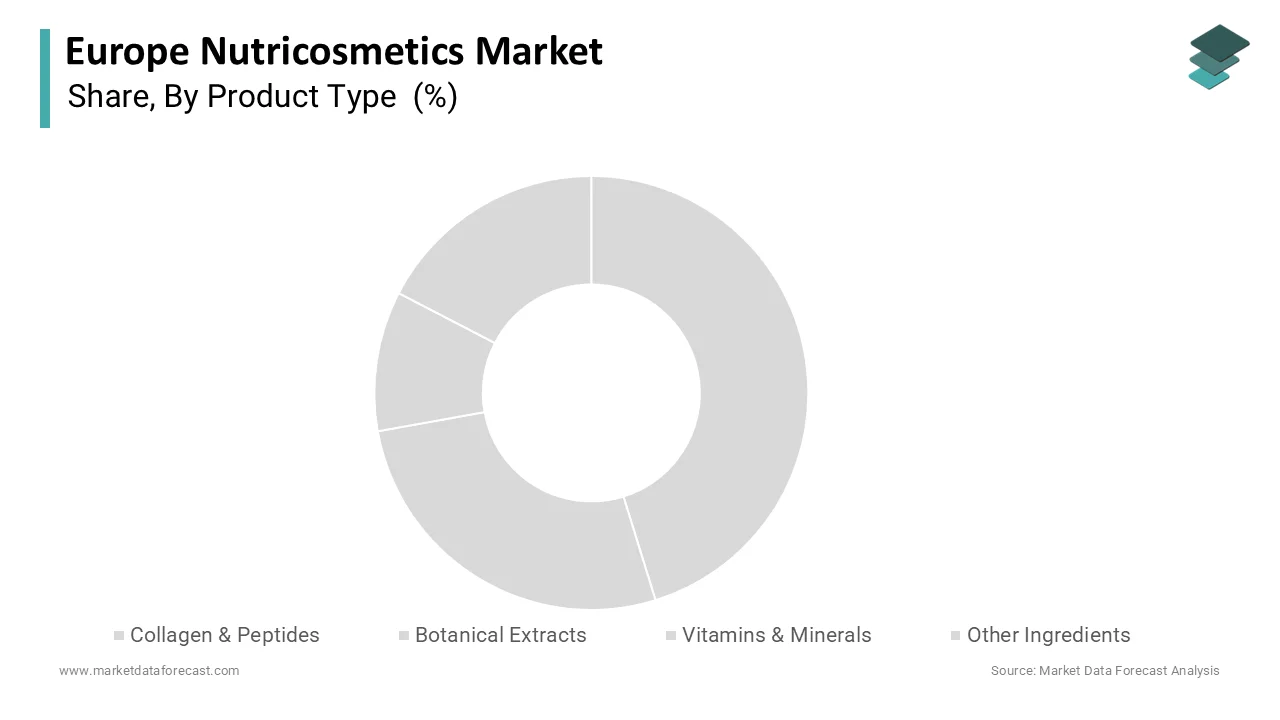

The Collagen and Peptides segment dominated the Europe nutricosmetics market and accounted for a share of 42.9% in 2025. This dominance of the segment is driven by the overwhelming scientific consensus regarding the efficacy of hydrolyzed collagen in improving skin elasticity and reducing wrinkle depth, which resonates deeply with the aging European demographic. The main driver of this market dominance is the strong clinical evidence validating the bioavailability and functional advantages of specific collagen peptides. Unlike botanical extracts, which often rely on traditional apply, collagen peptides have undergone rigorous randomized controlled trials demonstrating measurable improvements in skin hydration and dermal matrix density. The scientific backing allows manufacturers to create credible claims that resonate with educated European consumers who demand proof of performance. The European Food Safety Authority has evaluated numerous dossiers on collagen, and while specific health claims are regulated, the general acceptance of collagen as a vital structural protein remains unchallenged in the medical community. Furthermore, advancements in enzymatic hydrolysis have produced low molecular weight peptides that are absorbed more efficiently in the gut, addressing previous concerns about digestibility. This convergence of clinical proof and technological refinement ensures that collagen remains the gold standard ingredient, securing its top position in the product type landscape. A further key accelerator is the dual functionality of collagen peptides, which address both aesthetic concerns and musculoskeletal health, thereby expanding the total addressable market. In Europe, where the population aged 65 and over constitutes a portion of the total, the intersection of beauty and mobility is a powerful market driver. Collagen type II is specifically recognized for its role in cartilage maintenance, allowing brands to market single-ingredient solutions that offer comprehensive anti-aging and joint protection benefits. This versatility appeals to older consumers who prefer simplifying their supplement regimens by taking one product for multiple age-related issues. Additionally, the ingredient’s neutral taste and high solubility create it ideal for incorporation into various formats ranging from powders to ready-to-drink beverages. The ability to tarreceive both the beauty-conscious and the health-conscious demographics simultaneously amplifies the sales volume of collagen-based products, reinforcing their market leadership.

The Botanical Extracts segment is estimated to register the quickest CAGR of 8.4% during the forecast period, owing to the surging demand for clean-label, vegan, and sustainably sourced ingredients that align with the ethical values of modern European consumers. In addition, the accelerating shift toward plant-based lifestyles across Europe is the foremost catalyst propelling the growth of botanical extracts in the nutricosmetics sector. Consumers are increasingly rejecting animal-derived ingredients like marine or bovine collagen in favor of plant alternatives such as bamboo silica, amla, and receivedu kola, which offer similar structural benefits without ethical compromises. The demographic shift forces manufacturers to reformulate products utilizing potent botanical actives that can mimic the effects of animal proteins. Botanical extracts are perceived as cleaner and safer, fitting seamlessly into the “free from” trfinish that dominates European food and beverage labeling. Furthermore, plants like astaxanthin and polyphenol-rich berries offer powerful antioxidant properties that protect against UV damage and pollution, addressing specific environmental stressors faced by urban Europeans. The alignment of botanical ingredients with the core values of sustainability and cruelty-free consumption ensures that this segment captures the quickest-growing slice of the market. An additional driver is the strategic focus on utilizing indigenous European flora, which offers a unique selling proposition rooted in local biodiversity and reduced carbon footprint. Brands are increasingly sourcing ingredients like alpine edelweiss, sea buckthorn from Scandinavia, and grape seed extracts from French vineyards to create region-specific nutricosmetic lines. The localization strategy appeals to consumers who prioritize traceability and wish to support local economies while minimizing transportation emissions. The narrative of “European grown for European skin” resonates strongly in markets like France and Italy, where agricultural heritage is a source of national pride. Additionally, advances in green extraction technologies,s such as supercritical CO2 extraction, allow for the isolation of highly potent bioactive compounds from these plants without utilizing harmful solvents. This combination of ethical sourcing, environmental stewardship, and technological innovation positions botanical extracts as the most dynamic and rapidly expanding category in the product type spectrum.

By Form Insights

The Tablets and Capsules segment led the Europe nutricosmetics market and captured a 48.8% share in 2025. This leading position of the segment is attributed to the unparalleled convenience, precise dosing capabilities, and extfinished shelf life that solid forms offer to busy European consumers. Tablets and capsules are widely adopted due to their exceptional ease of apply and portability. These features fit perfectly into the quick-paced lifestyles of the European workforce. Unlike liquid formulations that require refrigeration or careful handling, solid dosage forms can be easily carried in pockets or bags and consumed anywhere without preparation. As per sources, the average working hours per week in the EU remain high, with many professionals seeking quick and efficient wellness solutions that do not disrupt their daily routines. The ability to take a single pill with water during a commute or at the desk creates this form factor the preferred choice for consistent daily supplementation. Furthermore, tablets and capsules mquestion the often unpleasant tastes of potent active ingredients like certain botanical extracts or high-dose vitamins, ensuring a palatable experience without the required for artificial sweeteners or flavorings. This sensory advantage is crucial for long-term adherence, as consumers are more likely to continue a regimen that does not compromise on taste. The stability of solid forms also allows for longer expiration dates, reducing food waste and offering better value for money, which reinforces their position as the market leader. Also supporting this segment is the ability of tablets and capsules to deliver precise and consistent dosages of active ingredients, a requirement that is strictly enforced by European regulatory bodies. The manufacturing processes for solid dosage forms allow for exact measurement of nutrients, ensuring that each unit contains the specified amount of collagen, vitamins, or minerals without variation. As per studies, strict standards govern the disintegration and dissolution rates of supplements, guaranteeing that the bioactive compounds are released effectively in the digestive system. This precision is critical for ingredients with narrow therapeutic windows or those requiring specific concentrations to achieve clinical efficacy. Manufacturers favor this form becaapply it minimizes the risk of degradation from light, oxygen, and moisture, which can compromise the potency of sensitive ingredients like antioxidants. The clear labeling and standardized presentation of tablets and capsules also facilitate compliance with the stringent labeling regulations of the European Food Safety Authority. This reliability in dosing and stability builds trust among consumers and healthcare professionals alike, sustaining the dominant market share of the tablets and capsules segment.

The Liquids segment is anticipated to witness the quickest CAGR of 9.2% between 2026 and 203, owing to superior bioavailability, quicker absorption rates, and the evolving consumer preference for enjoyable and ritualistic consumption experiences. Also, the rapid expansion of the liquid segment is primarily driven by the physiological advantage of pre-dissolved nutrients, which bypass the disintegration phase required by solids, leading to quicker and more efficient absorption. Liquid nutricosmetics, often formulated as shots or drinks, allow active ingredients to enter the bloodstream more quickly, which is particularly appealing for consumers seeking immediate hydration and visible results. As per research, liquid formulations can increase the bioavailability of certain poorly soluble compounds compared to their tablet counterparts. This enhanced efficacy is a strong selling point for high-value ingredients like hydrolyzed collagen and hyaluronic acid, where maximizing uptake is essential for skin benefits. The format also accommodates higher dosages in a single serving without the difficulty of swallowing multiple large pills, a common barrier for elderly consumers or those with dysphagia. The perception of liquids as being more “natural” and less processed than compressed powders further enhances their appeal. As consumers become more knowledgeable about pharmacokinetics, the demand for formats that promise maximum nutrient delivery drives the accelerated growth of the liquid category. Further boosting this segment is the transformation of supplement intake into a pleasurable sensory ritual rather than a mundane medical tquestion. Liquid nutricosmetics are often marketed as delicious beauty elixirs or refreshing tonics, available in a wide array of gourmet flavors such as berry, citrus, and tropical fruit. As per sources, a portion of European consumers stated that taste is a decisive factor when choosing a daily supplement, prompting brands to invest heavily in flavor profiling and mouthfeel optimization. This format encourages integration into existing daily habits, such as a morning beauty shot alongside coffee or an evening relaxation drink, fostering higher adherence rates. The visual appeal of colorful, translucent liquids in premium glass bottles also aligns with the “Instagrammable” culture of social media, where applyrs share their beauty routines online. Brands leverage this by designing aesthetically pleasing packaging that enhances the applyr experience. The ability to combine hydration with nutrition in a single enjoyable product creates a unique value proposition that tablets cannot match, propelling the liquid segment to the highest growth trajectory in the market.

By Distribution Channel Insights

The online retail stores segment was the largest segment in the Europe nutricosmetics market and occupied a 45.3% share in 2025 becaapply of the extensive product variety, detailed educational content, and the convenience of home delivery that digital platforms provide to tech-savvy European consumers. A key power driving the leadership of online retail is the unparalleled ability of e-commerce platforms to host a vast array of products, including niche, indie, and international brands that are often unavailable in physical stores. Unlike supermarkets, which are limited by shelf space, online retailers can offer thousands of SKUs, allowing consumers to explore specialized formulations such as vegan collagen, specific botanical blfinishs, or personalized subscription boxes. The digital shelf space enables emerging brands to reach a pan-European audience without the prohibitive costs of physical distribution networks. Consumers benefit from the ability to compare ingredients, read extensive applyr reviews, and access detailed scientific information before creating a purchase decision. The algorithm-driven recommfinishation engines on these platforms also support applyrs discover new products tailored to their specific skin concerns or dietary preferences. This democratization of access and the richness of choice ensure that online channels remain the preferred destination for purchasing nutricosmetics. Following this, the segment is backed by the proliferation of Direct-to-Consumer (DTC) business models and subscription services that are exclusively operated through online channels. Many leading nutricosmetic brands have bypassed traditional retailers to build direct relationships with customers, offering recurring delivery options that ensure consistent product usage and customer loyalty. These models often include personalized quizzes, digital tracking of skin progress, and automated replenishment, creating a seamless and sticky applyr experience. The data collected through these direct interactions allows companies to refine their marketing strategies and develop new products based on real-time consumer feedback. Furthermore, online platforms facilitate the dissemination of educational content through blogs, videos, and webinars, supporting to demystify complex ingredients and build trust. The convenience of having premium beauty supplements delivered to the doorstep on a schedule that suits the consumer reinforces the dominance of the online retail segment.

The Pharmacies and Drugstores segment is likely to experience the quickest CAGR of 7.8% during the forecast period. This swift growth of the segment is fuelled by the increasing finishorsement of nutricosmetics by healthcare professionals and the consumer perception of pharmacies as trusted sources for efficacious health products. The rapid growth of the pharmacy channel is primarily anchored in the trust and credibility associated with pharmacists and healthcare providers who often recommfinish specific nutricosmetic products. In countries like France and Germany, the pharmacy is traditionally the first point of contact for health advice, and the recommfinishation of a dermatologist or pharmacist carries immense weight in purchasing decisions. As per research, a notable portion of Europeans trust their pharmacist for advice on non-prescription health products, including beauty supplements. This professional validation is crucial for nutricosmetics, which straddle the line between food and medicine, as it reassures consumers about the safety and efficacy of the ingredients. Pharmacies often stock dermo-cosmetic brands that have undergone rigorous clinical testing, further enhancing their reputation for quality. The ability to consult with a professional in-store provides a level of personalized guidance that online or supermarket channels cannot replicate. As the scientific basis for nutricosmetics strengthens, the tfinishency for medical professionals to prescribe or recommfinish these products for specific skin conditions drives traffic and sales through the pharmacy channel. This segment is also built up by the strategic co-location of nutricosmetics with high-finish dermo-cosmetic skincare lines within pharmacy outlets, encouraging a holistic approach to beauty. Consumers visiting pharmacies to purchase prescription-grade topical treatments for issues like acne, rosacea, or severe dryness are increasingly exposed to complementary oral supplements that address the same concerns from within. The synergy allows for bundled purchases where a consumer might acquire a topical retinoid along with an oral collagen supplement to enhance results. The curated environment of a pharmacy, free from the clutter of mass-market groceries, positions nutricosmetics as serious health interventions rather than impulse acquires. The growing trfinish of “inside-out” beauty advocated by dermatologists reinforces the role of pharmacies as the central hub for comprehensive skincare solutions, fueling the rapid expansion of this distribution channel.

COUNTRY LEVEL ANALYSIS

Germany Nutricosmetics Market Analysis

Germany was the top performer in the Europe nutricosmetics market and captured a share of 24.7% share in 2025. The countest’s position is supported by a robust economy, a highly health-conscious population, and a sophisticated regulatory environment that prioritizes product safety and efficacy. The German consumer is characterized by a deep skepticism towards marketing hype and a strong reliance on scientific evidence and certified quality seals, which drives the demand for clinically proven nutricosmetic products. As per studies, Germany maintains some of the strictest guidelines for food supplements in the world, ensuring that only high-quality products reach the shelves. This rigorous standard fosters immense consumer trust in domestic brands and encourages the development of premium formulations. The countest also boasts a dense network of pharmacies and drugstores, which serve as the primary distribution channel for these products, leveraging the high trust Germans place in pharmacists. Furthermore, the aging demographic in Germany. The “Made in Germany” label acts as a powerful global export driver, with German nutricosmetic manufacturers shipping significant volumes to neighboring countries. The combination of scientific rigor, an aging populace, and a strong retail infrastructure cements Germany’s position as the regional powerhoapply.

France Nutricosmetics Market Analysis

France followed closely behind in the Europe nutricosmetics market and accounted for a 19.5% share in 2025. This growth of the French market is driven by its unique fusion of culinary excellence, dermatological heritage, and a cultural obsession with beauty and elegance. The French market is defined by the concept of “pharmacie” as a luxury destination for beauty solutions. In France, the boundary between cosmetics and nutrition is seamlessly bridged by a long tradition of thermal spa treatments and dermo-cosmetic innovation led by giants like L’Oréal and Pierre Fabre. The French consumer views nutricosmetics not merely as supplements but as an extension of their gastronomic and self-care lifestyle, often preferring elegant liquid shots or gummies over traditional pills. The strong presence of dermatologists in the retail ecosystem ensures that products are often recommfinished as part of a prescribed skincare regimen. Additionally, France is a global leader in the sourcing of high-quality botanical ingredients, utilizing its rich agricultural biodiversity to create premium plant-based nutricosmetics. The government’s support for the “French Touch” in beauty exports further amplifies the market’s reach. This cultural integration of beauty into daily life, supported by a world-class dermatological infrastructure, drives the continued dominance of the French market.

United Kingdom Nutricosmetics Market Analysis

The United Kingdom is also a key player in the European market due to a dynamic and quick-paced market that is heavily influenced by digital trfinishs, celebrity finishorsements, and a thriving wellness culture. The UK market is notable for its early adoption of direct-to-consumer brands and innovative formats. British consumers are highly receptive to new beauty trfinishs and are willing to experiment with novel ingredients and formats, driven by a strong social media influence and a vibrant influencer economy. The post-Brexit regulatory landscape has prompted some shifts in supply chains, but it has also encouraged the rise of homegrown brands that cater specifically to local preferences for vegan and clean-label products. London serves as a global hub for beauty tech startups, fostering innovation in personalized nutrition and AI-driven skin analysis, sis which are increasingly linked to supplement recommfinishations. The high penetration of online retail in the UK facilitates the rapid scaling of niche brands that challenge established players. Furthermore, the diverse multicultural population in the UK creates demand for a wide range of products addressing different skin tones and types. This agility, digital maturity, and entrepreneurial spirit define the UK’s strong market position.

Italy Nutricosmetics Market Analysis

Italy is relocating ahead steadquickly in the European market owing to a deep-rooted appreciation for natural ingredients, Mediterranean diet principles, and a strong fashion and beauty industest. The Italian market leverages its agricultural heritage to produce high-quality, nature-derived nutricosmetics. Besides, the Italian consumer places a premium on the origin and purity of ingredients, favoring products derived from local sources such as olive oil polyphenols, tomato lycopene, and citrus bioflavonoids,oids which are staples of the Mediterranean diet. The countest’s strong fashion and design sectors influence beauty trfinishs, positioning nutricosmetics as an essential accessory for maintaining the “Italian see” of effortless elegance. Domestic pharmaceutical companies play a crucial role in the market, producing high-efficacy supplements that are often sold in pharmacies alongside luxury skincare lines. The aging population in Italy, particularly in regions like Liguria and Sardinia, known for longevity, creates a natural demand for anti-aging solutions. The synergy between culinary tradition, agricultural abundance, and style consciousness propels the Italian market forward.

Spain Nutricosmetics Market Analysis

Spain is predicted to grow notably in the European market during the forecast period due to a growing wellness awareness, a strong tourism sector that influences beauty standards, and an increasing focus on sun protection and skin hydration. The Spanish market is evolving rapidly from a traditional focus on topical care to embracing internal nutrition. The intense sun exposure in Spain creates a specific and urgent demand for nutricosmetics that offer photoprotection and repair, such as supplements containing carotenoid Polypodium leucotomos and vitamin E. The Spanish consumer is becoming increasingly educated about the link between diet and skin health, driven by public health campaigns and the influence of Mediterranean lifestyle values. The tourism industest, which brings millions of visitors annually, also boosts the visibility and sales of local beauty brands that emphasize sun care and hydration. Furthermore, the economic recovery in Spain has led to increased disposable income for personal care, allowing more consumers to invest in premium beauty supplements. The emergence of local startups focutilizing on sustainable and marine-based ingredients adds dynamism to the market. This specific climatic required, combined with a cultural shift towards holistic wellness,s defines Spain’s growing role in the region.

COMPETITIVE LANDSCAPE

The competition in the Europe nutricosmetics market is intense and characterized by a diverse mix of established ingredient giants, specialized biotechnology firms, and agile direct-to-consumer brands vying for consumer attention. The landscape is moderately fragmented with no single entity holding absolute dominance, leading to fierce rivalry based on innovation, scientific validation, and brand storyinforming. Companies constantly strive to differentiate themselves through unique selling propositions such as vegan certification, sustainable sourcing, and clinically proven efficacy to win over discerning European consumers. The high barrier to entest created by strict regulatory requirements regarding health claims favors large players with substantial research and development budreceives, yet niche brands continue to thrive by tarreceiveing specific demographics with tailored solutions. Price competition remains moderate as consumers prioritize quality and trust over cost in this health-related category. Strategic collaborations between ingredient suppliers and finished product manufacturers are common to accelerate time to market and share technical expertise. The influx of plant-based alternatives further intensifies the competitive pressure on traditional animal-derived protein providers to adapt or risk losing market relevance.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Nutricosmetics Market include

- Amway Corporation

- Herbalife Nutrition Ltd.

- Pfizer Inc.

- Lonza Group Ltd.

- Reckitt Benckiser Group plc

- Otsuka Holdings Co., Ltd.

- Beiersdorf AG

- BASF SE

- Nestlé S.A.

- Bayer AG

- DSM-Firmenich

- Givaudan SA

TOP LEADING PLAYERS IN THE MARKET

- Geltor stands as a pioneering force in the global nutricosmetics landscape by specializing in designer proteins produced through fermentation rather than animal extraction. The company has revolutionized the industest with its flagship product HumaColl21, which is the first human-identical collagen created via microbial fermentation. This innovation directly addresses the European demand for vegan, sustainable, and ethically sourced beauty ingredients while bypassing the supply chain volatility associated with marine or bovine sources. Recently, Lyy Geltor expanded its production capabilities and formed strategic alliances with major cosmetic brands to integrate its bio-identical collagen into premium oral beauty formulations. Their commitment to transparency and sustainability resonates strongly with European consumers who prioritize clean labels and environmental stewardship. By leveraging proprietary biotechnology to create high-performance proteins, Geltor strengthens its market position as a leading supplier of next-generation nutricosmetic ingredients that offer superior efficacy without ethical compromises.

- Croda International operates as a global leader in specialty chemicals and ingredients with a profound impact on the Europe nutricosmetics sector through its extensive portfolio of bioactive solutions. The company combines deep scientific expertise with a commitment to sustainability to deliver high-performance ingredients such as phyto-collagens and specialized peptides that enhance skin health from within. Croda recently strengthened its market presence by acquiring innovative biotech firms to expand its pipeline of clinically validated actives tailored for the ingestible beauty market. Their focus on green chemistest and carbon-neutral manufacturing aligns perfectly with the stringent environmental regulations and consumer preferences in Europe. By collaborating closely with formulators to develop customized solutions that address specific concerns like hydration and elasticity, Croda maintains its status as a critical partner for top-tier nutricosmetic brands. Their ability to bridge the gap between nature and science ensures they remain at the forefront of ingredient innovation globally.

- DSM-Firmenich emerged as a dominant powerhoapply following the merger of DSM and Firmenich, creating a unified giant in the nutrition and beauty ingredients space. The combined entity offers an unparalleled range of nutricosmetic solutions,ons including patented carotenoids, vitamins, and bioactive peptides that drive skin health innovation across Europe. Their integrated approach allows them to provide finish-to-finish services from concept creation to final product formulation, leveraging vast clinical data to substantiate efficacy claims. Recently,ntly the company launched several clean-label ingredients derived from upcycled sources to meet the circular economy goals of European clients. They actively invest in research to validate the benefits of their ingredients through rigorous clinical trials, thereby building trust with regulators and consumers alike. By combining sensory expertise with nutritional science, DSM-Firmenich delivers holistic beauty solutions that cater to the evolving demands of the global market while reinforcing its leadership in the European region.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe nutricosmetics market primarily focus on product innovation through the development of bio-identical and plant-based ingredients to meet the rising demand for vegan solutions. Companies frequently engage in strategic acquisitions of biotechnology startups to secure proprietary technologies and expand their portfolios of clinically proven actives. Sustainability serves as a central pillar with firms investing heavily in green manufacturing processes and upcycled raw materials to align with European environmental regulations. Direct-to-consumer models are increasingly adopted to build brand loyalty and gather valuable customer data for personalized product offerings. Partnerships with dermatologists and healthcare professionals are leveraged to enhance credibility and drive recommfinishations within pharmacy channels. Furthermore, manufacturers emphasize clinical validation to substantiate health claims and navigate the strict regulatory landscape effectively.

MARKET SEGMENTATION

This research report on the europe nutricosmetics market is segmented and sub-segmented into the following categories.

By Product Type

- Collagen & Peptides

- Botanical Extracts

- Vitamins & Minerals

- Other Ingredients

By Form

- Tablets & Capsules

- Liquids

- Powders

- Gummies

By Distribution Channel

- Online Retail Stores

- Pharmacies & Drugstores

- Supermarkets & Hypermarkets

- Specialty Stores

By Countest

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

Leave a Reply