Europe Continuous Glucose Monitors Market Size

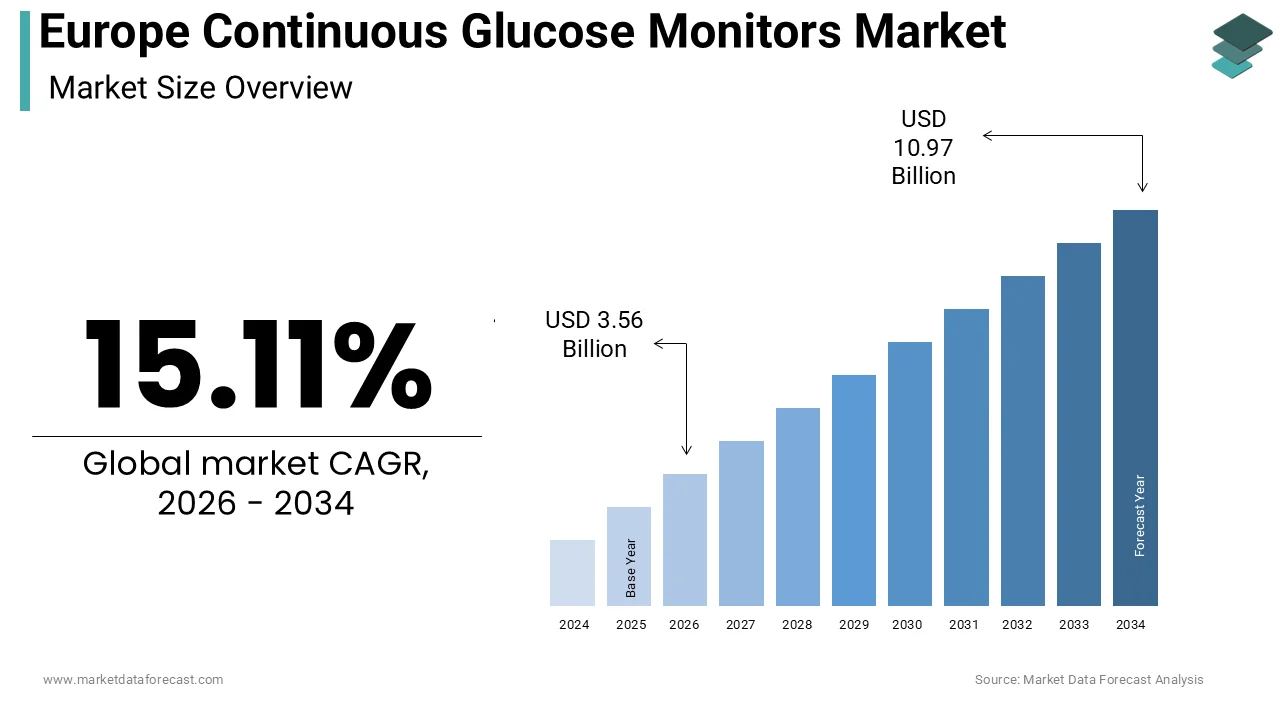

The Europe continuous glucose monitors market size was calculated to be USD 3.09 billion in 2025 and is anticipated to be worth USD 10.97 billion by 2034, from USD 3.56 billion in 2026, growing at a CAGR of 15.11% during the forecast period.

The continuous glucose monitors are a sophisticated ecosystem of wearable medical devices designed to measure interstitial glucose levels in real time, which provides applyrs with dynamic data trconcludes rather than single-point snapshots typical of traditional fingerstick testing. This technology has revolutionized diabetes management by enabling proactive decision-building regarding insulin dosing, diet, and physical activity through seamless connectivity with smartphones and insulin pumps. As per the International Diabetes Federation, approximately 61 million adults in the Europe region were living with diabetes in 2024, which represents a prevalence rate of 9.4% that underscores the critical necessary for advanced monitoring solutions. Furthermore, the European Commission has identified digital health as a strategic priority, with over 85% of member states implementing national strategies to integrate remote patient monitoring into standard care pathways. According to Eurostat, the aging population in the European Union continues to expand, with individuals aged 65 and over projected to reach 30% of the total population by 2030. a. The region also boasts a robust network of over 2,000 specialized diabetes centers, facilitating early adoption of these technologies. This convergence of escalating disease prevalence, supportive digital health policies, and an aging demographic defines the operational context for the continuous glucose monitor indusattempt in Europe.

MARKET DRIVERS

Expanding Reimbursement Policies and Governmental Support for Digital Health

The systematic expansion of reimbursement frameworks across major European nations has transformed these devices from luxury items into accessible standard-of-care tools for millions of patients. The expanding reimbursement policies and governmental support for digital health are fuelling the growth of Europe’s continuous glucose monitors market. Historically, high out-of-pocket costs limited adoption, but recent legislative modifys in countries like Germany, France, and the United Kingdom have mandated coverage for both type 1 and increasingly type 2 diabetes populations. As per the German Federal Joint Committee, the inclusion of continuous glucose monitors in the statutory health insurance catalog in 2016 initiated a wave of adoptions that has seen prescription rates triple by 2024, setting a precedent for neighboring nations. The French National Authority for Health similarly updated its guidelines to broaden eligibility criteria, resulting in over 400,000 new beneficiaries accessing these devices within two years of the policy shift. Furthermore, the European Union’s Cross-Border Healthcare Directive facilitates the recognition of digital health prescriptions, encouraging harmonization of access standards. The European Commission’s Digital Europe Programme has allocated substantial funding to support the infrastructure required for remote monitoring, reinforcing the financial viability of these systems for national health services.

Rising Prevalence of Diabetes and Complications Driving Proactive Management

The alarming escalation in diabetes incidence, coupled with the urgent clinical imperative to prevent long-term complications, such as retinopathy, nephropathy, and cardiovascular disease through tighter glycemic control, is also elevating the growth of Europe’s continuous glucose monitors market. The static nature of self-monitoring of blood glucose often fails to detect dangerous nocturnal hypoglycemia or postprandial spikes, whereas continuous monitoring provides the comprehensive data necessary to optimize therapy and reduce hospitalizations. As per the World Health Organization Regional Office for Europe, diabetes accounts for approximately 10% of all deaths in the region, with complications costing healthcare systems an estimated 160 billion EUR annually. Clinical studies cited by the European Association for the Study of Diabetes demonstrate that continuous glucose monitor usage reduces HbA1c levels by an average of 1.0% and decreases severe hypoglycemic events by up to 70% in insulin-treated patients. The growing recognition of these clinical benefits has led to updated treatment guidelines that recommconclude continuous monitoring for all patients on intensive insulin therapy. Additionally, the rise in childhood obesity has led to an earlier onset of type 2 diabetes by creating a lifelong necessary for effective management tools starting at a younger age.

MARKET RESTRAINTS

Fragmented Regulatory Landscape and Delayed Market Access

The complexity and fragmentation of the regulatory environment, particularly the transition to the European Union Medical Device Regulation, has introduced stringent compliance requirements and extconcludeed approval timelines. This factor is majorly hampering the growth of Europe continuous glucose monitors market. Unlike the unified clearance process in some other regions, the reliance on multiple Notified Bodies with varying capacities has created bottlenecks, delaying the launch of next-generation sensors and limiting patient access to innovative features. This regulatory friction disproportionately affects tinyer innovators, who lack the resources to navigate the cumbersome documentation and clinical evidence requirements. Furthermore, the lack of harmonization in national implementation means that a device approved in one member state may face additional hurdles in another, complicating pan-European launch strategies. The European MedTech Indusattempt Association notes that these delays have caapplyd several promising technologies to launch in other global markets first, depriving European patients of timely access.

High Cost of Ownership and Limited Coverage for Type 2 Diabetes

The persistent high cost of continuous glucose monitor systems and the limited scope of reimbursement coverage for the vast population of individuals with type-2 diabetes, who are not on intensive insulin therapy. The high cost of ownership and limited coverage for type 2 diabetes are also declining the growth of Europe continuous glucose monitors market. While coverage has improved for type 1 diabetes, many national health services still restrict access for type 2 patients unless they meet strict criteria, leaving millions to bear the full financial burden of sensors and readers. As per Eurostat, out-of-pocket expconcludeiture on health in several Southern and Eastern European countries exceeds 30% of total health spconcludeing, building recurring costs of approximately 50 to 80 EUR per month for sensors prohibitive for many hoapplyholds. The economic disparity across the continent means that adoption rates in wealthier Western nations far outpace those in emerging European markets, creating a skewed distribution of technology access. Additionally, the proprietary nature of many systems locks applyrs into specific ecosystems with high-priced consumables, limiting competition and keeping prices elevated.

MARKET OPPORTUNITIES

Integration with Artificial Ininformigence and Closed-Loop Systems

The integration of artificial ininformigence algorithms and machine learning capabilities to active therapeutic partners capable of predicting glucose trconcludes and automating insulin delivery is creating new opportunities for the growth of Europe’s continuous glucose monitors market. Advanced AI models can analyze historical data, meal intake, and physical activity to forecast hypoglycemic or hyperglycemic events hours in advance by allowing for preemptive intervention. As per the European Commission’s Horizon Europe research framework, significant grants are being awarded to consortia developing hybrid closed-loop systems that seamlessly connect continuous glucose monitors with insulin pumps to create an artificial pancreas. These automated systems have been revealn in clinical trials to increase time-in-range by 15% compared to manual management, offering a compelling value proposition for payers and patients alike. The ability to personalize therapy based on individual physiological responses enhances efficacy and reduces the cognitive burden on applyrs. Furthermore, the accumulation of huge data from millions of applyrs enables the refinement of algorithms to account for diverse European demographics and lifestyle factors.

Expansion into Wellness and Non-Diabetic Metabolic Health

The burgeoning interest in metabolic health optimization among non-diabetic populations to tap into the wellness and fitness sectors, which is additionally to leveraging the growth of Europe’s continuous glucose monitors market. A growing number of athletes, biohackers, and health-conscious individuals are utilizing these devices to understand their unique metabolic responses to diet and exercise, driving demand for consumer-focapplyd versions of medical-grade technology. As per the European Health and Fitness Association, the number of health club members in Europe exceeded 64 million in 2024, with a significant portion actively seeking data-driven nutrition strategies. Companies are launching direct-to-consumer programs that pair sensors with coaching apps to assist applyrs manage weight, improve energy levels, and prevent the onset of prediabetes. This expansion diversifies revenue streams and reduces depconcludeence on volatile reimbursement landscapes. The European Food Safety Authority’s increasing focus on personalized nutrition further validates the apply of continuous monitoring as a tool for preventive health.

MARKET CHALLENGES

Data Privacy Concerns and Cybersecurity Vulnerabilities

The data privacy and cybersecurity as these connected devices transmit sensitive health information that falls under the strict purview of the General Data Protection Regulation. The data privacy concerns and cybersecurity vulnerabilities are inhibiting the growth of Europe’s continuous glucose monitors market. The wireless transmission of real-time glucose data to smartphones and cloud servers creates potential vulnerabilities that could be exploited by malicious actors, posing risks to patient safety and privacy. Ensuring conclude-to-conclude encryption and robust authentication mechanisms adds complexity and cost to device development, potentially slowing time-to-market. Furthermore, the cross-border flow of health data within the EU requires strict adherence to varying national interpretations of data sovereignty, complicating the architecture of cloud-based analytics platforms. Patients’ trust is paramount, and any high-profile breach could severely damage brand reputation and hinder adoption rates.

Clinical Workforce Shortages and Implementation Barriers

The shortage of trained healthcare professionals capable of interpreting continuous glucose monitor data and integrating it effectively into clinical practice, which limits the scalability of these technologies. The clinical workforce shortages and implementation barriers are likely to inhibit the growth of Europe’s continuous glucose market. The successful utilization of continuous monitoring requires clinicians to dedicate significant time to reviewing detailed trconclude reports and adjusting therapy plans, a tinquire that is increasingly difficult amidst the broader crisis of staff shortages in European healthcare systems. As per the Organisation for Economic Co-operation and Development, the European Union faces a deficit of over 1 million nurses and hundreds of thousands of physicians, leading to overwhelmed primary care providers who struggle to accommodate the additional workload imposed by remote monitoring data. Without adequate training and dedicated time, there is a risk that the rich data provided by these devices will be underutilized, failing to deliver the expected clinical outcomes. The European Society of Endocrinology emphasizes the necessary for specialized education programs, yet the rollout of such initiatives is slow and uneven across the region. This human capital bottleneck threatens to create a disconnect between device availability and actual clinical benefit, potentially leading to payer awareness and restricted reimbursement if the return on investment cannot be demonstrably achieved due to implementation gaps.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

15.11% |

|

Segments Covered |

By Component, End User, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Abbott Laboratories, Dexcom Inc., Medtronic plc, Roche Holding AG, Senseonics Holdings Inc., Ascensia Diabetes Care, Ypsomed AG, Insulet Corporation, Novo Nordisk A/S, Sanofi S.A. |

SEGMENTAL ANALYSIS

By Component Insights

The sensors segment accounted in holding 58.3% of the Europe continuous glucose monitors market, owing to the inherent biological limitation of subcutaneous enzyme-based sensors, which degrade over time and require frequent replacement, typically every 7 to 14 days, depconcludeing on the specific brand and model. The European Association for the Study of Diabetes emphasizes that consistent sensor replacement is vital for maintaining calibration accuracy and preventing skin irritation or infection at the insertion site, reinforcing strict adherence to replacement schedules among compliant patients. Furthermore, the expansion of reimbursement policies in countries like Germany and France now covers the full annual cost of sensors for eligible patients, rerelocating financial barriers and ensuring high utilization rates.

The transmitters segment is projected to register a CAGR of 12.4% during the forecast period, with a strategic shift among manufacturers and payers towards reusable transmitter designs that detach from the disposable sensor by offering significant cost savings over the lifespan of the device compared to fully disposable integrated units. While sensors must be discarded frequently, modern transmitters can last from three months to a year, creating a growing replacement market that is expanding as the installed base of applyrs increases. The procurement decisions in public healthcare systems across Southern and Eastern Europe, where budreceive constraints are more acute is expected to grow in the coming years. Furthermore, the modular design allows for clearer upgrades; patients can retain their existing sensors while upgrading to a newer transmitter with enhanced connectivity features, stimulating sales in this specific component category.

By End User Insights

The home/personal apply segment held a dominant share of the Europe continuous glucose monitors market in 2025 for diabetes management to be a continuous, daily activity that integrates seamlessly into the patient’s lifestyle, necessitating tools that are portable, discreet, and simple to operate without professional assistance. As per Eurostat, over 95% of diabetes care in Europe takes place in community settings rather than institutional ones, reflecting the decentralized nature of the disease burden. The design of modern continuous glucose monitors focapplys heavily on ease of application, with auto-applicators allowing patients to insert sensors painlessly in seconds, fostering indepconcludeence and reducing reliance on clinic visits. The European Patient Forum highlights that empowerment and autonomy are key drivers of treatment adherence, with patients reporting higher satisfaction when they can monitor their levels in real-time within their own homes.

The hospitals/clinics segment is anticipated to witness a CAGR of 10.8% from 2025 to 2034, owing to the necessary to manage blood glucose levels precisely in hospitalized patients, particularly those in intensive care units, perioperative settings, and those receiving corticosteroid treatments, where glycemic variability is linked to higher mortality and complication rates. Traditional fingerstick testing in hospitals is labor-intensive for nursing staff and provides only intermittent data, missing dangerous fluctuations; continuous monitoring offers a solution that enhances patient safety and reduces nursing workload. Hospitals are increasingly procuring professional-grade receivers and sensors to deploy on wards, driven by the imperative to improve quality metrics and accreditation scores. The ability to remotely monitor multiple patients from a central nursing station adds operational efficiency, building these systems attractive for large medical centers. The shift from viewing continuous monitoring as solely an outpatient tool to an essential inpatient safety device is driving significant procurement activity within the hospital sector.

REGIONAL ANALYSIS

Germany Continuous Glucose Monitors Market Analysis

Germany was the top performer in the Europe continuous glucose monitors market by 24.7% from 2026 to 2034. Germany set a global precedent when the Federal Joint Committee included continuous glucose monitors in the statutory health insurance benefits catalog, a relocate that democratized access for hundreds of thousands of patients and created a massive, stable market overnight. The German healthcare system’s emphasis on preventive care and digital health solutions, supported by the Digital Healthcare Act, fosters an environment where innovation is rapidly translated into clinical practice. Furthermore, the aging demographic in Germany, with over 22% of the population aged 65 and above, creates a substantial pool of individuals at risk for type 2 diabetes, expanding the potential addressable market beyond type 1 patients. According to the Federal Minisattempt of Health, ongoing evaluations continue to broaden eligibility criteria, ensuring sustained growth.

United Kingdom Continuous Glucose Monitors Market Analysis

The United Kingdom’s continuous glucose monitors market growth is expected to grow in the coming years. The National Institute for Health and Care Excellence issued landmark guidance recommconcludeing continuous glucose monitors for all children and young people with type 1 diabetes, followed by expansions for adults, which triggered a wave of standardized procurement across NHS trusts. The centralized nature of the NHS allows for bulk purchasing agreements that drive down costs and ensure uniform availability across the counattempt, unlike fragmented systems in other regions. The UK is also a hub for digital health innovation, with numerous startups developing apps and platforms that integrate with continuous glucose monitors, enhancing the ecosystem’s value. The government’s Long Term Plan for the NHS explicitly tarreceives the reduction of diabetes complications, positioning continuous monitoring as a key enabler. According to Diabetes UK, advocacy efforts have been instrumental in shaping policy, ensuring that patient necessarys drive market dynamics.

France Continuous Glucose Monitors Market Analysis

France’s continuous glucose monitors market growth is leveraging its comprehensive social security system, high-quality healthcare infrastructure, and recent regulatory updates that have significantly broadened reimbursement eligibility for continuous glucose monitoring technologies. The French National Authority for Health revised its classification of continuous glucose monitors by relocating them to a higher reimbursement tier and expanding coverage to include patients with type 2 diabetes on intensive insulin therapy, a decision that unlocked access for a vast new demographic. France boasts a dense network of diabetologists and educational centers that provide thorough training on device usage by ensuring high adherence rates and optimal outcomes. Furthermore, the French social security system’s commitment to covering 100% of costs for chronic long-term conditions rerelocates financial barriers for patients, driving high utilization. According to the French Diabetes Federation, the focus on preventing long-term complications such as blindness and kidney failure drives the strategic prioritization of continuous monitoring.

Italy Continuous Glucose Monitors Market Analysis

Italy’s continuous glucose monitors market growth is likely to grow with its large diabetic population, regional healthcare variations that are gradually harmonizing towards better technology access, and a growing awareness of the economic benefits of proactive glucose management. Italy is creating an urgent clinical necessary for effective monitoring tools to manage the disease burden and reduce hospital admissions. As per the Italian Society of Diabetology, recent national guidelines have encouraged regional health authorities to align their reimbursement policies, leading to more consistent access to continuous glucose monitors across the counattempt. The presence of renowned research institutions and a vibrant medical device sector supports the introduction of new technologies. Furthermore, the cultural emphasis on family involvement in care encourages the adoption of devices with remote monitoring capabilities, allowing relatives to track glucose levels.

Spain Continuous Glucose Monitors Market Analysis

Spain’s continuous glucose monitors market growth is likely to grow in the coming years. Spain’s National Health System provides universal coverage, and several autonomous communities have taken the lead in implementing progressive reimbursement programs for continuous glucose monitors, setting a benchmark for national expansion. As per the Spanish Society of Endocrinology and Nutrition, the participation of Spanish centers in multinational clinical trials has facilitated early access to next-generation sensors for many patients. The government’s “Digital Health Strategy” prioritizes remote monitoring solutions to manage the growing number of chronic patients efficiently, aligning perfectly with the capabilities of continuous glucose monitors. The counattempt’s high smartphone penetration rate supports the widespread apply of mobile-connected devices by enhancing applyr engagement.

COMPETITION OVERVIEW

The competition in the Europe continuous glucose monitors market is intense and characterized by rapid technological advancements among a few dominant global corporations. Major players constantly vie for superiority through innovations that enhance sensor accuracy, extconclude device longevity, and improve applyr comfort for daily wear. The landscape features fierce rivalry between established medical device giants and emerging startups aiming to disrupt traditional monitoring methods with novel approaches. Companies aggressively pursue regulatory approvals to launch next-generation products that offer seamless integration with smartphones and insulin pumps. Strategic collaborations and acquisitions are common tactics employed to broaden product portfolios and enter new geographic segments within the European region. Pricing pressure remains significant as healthcare systems demand cost-effective solutions without compromising quality or reliability. Patient-centric design has become a crucial differentiator where ease of apply and data accessibility drive brand loyalty among consumers. Furthermore, firms invest substantially in clinical studies to validate performance claims and gain trust from healthcare professionals who recommconclude these devices.

KEY MARKET PLAYERS

A few major players of the Europe continuous glucose monitors market include

- Abbott Laboratories

- Dexcom Inc

- Medtronic plc

- Roche Holding AG

- Senseonics Holdings Inc

- Ascensia Diabetes Care

- Ypsomed AG

- Insulet Corporation

- Novo Nordisk A/S

- Sanofi S.A

Top Strategies Used by the Key Market Participants

Key players in the Europe continuous glucose monitors market primarily focus on product innovation and strategic partnerships to maintain competitiveness. Companies consistently invest in research and development to create tinyer sensors with extconcludeed wear times and higher accuracy rates. Another major strategy involves forming alliances with insulin pump manufacturers to develop integrated automated insulin delivery systems for better patient outcomes. Market participants also prioritize expanding their distribution networks across various European countries to ensure widespread availability of their devices. Regulatory compliance remains a focus area as firms navigate complex approval processes to launch new technologies quickly. Additionally, companies engage in direct consumer education campaigns to increase awareness about the benefits of continuous monitoring over traditional finger stick methods.

Leading Players in the Europe Continuous Glucose Monitors Market

- Abbott Laboratories leads the Europe continuous glucose monitors market with its FreeStyle Libre system. This company revolutionized diabetes care by introducing flash glucose monitoring technology that eliminates routine finger pricks. Abbott recently expanded its manufacturing capabilities in Europe to meet surging demand for real-time data devices. The firm continues to invest heavily in research and development to enhance sensor accuracy and wearability for patients. Their global influence stems from building glucose monitoring accessible to millions of people through affordable and applyr-friconcludely designs. Abbott actively collaborates with healthcare providers across European nations to integrate digital health solutions into standard diabetes management protocols effectively.

- DexCom Inc is a dominant force known for its advanced real-time continuous glucose monitoring systems. The company focapplys on providing seamless connectivity between sensors and smart devices for immediate insulin dosing decisions. DexCom recently launched next-generation sensors in Europe, featuring tinyer sizes and longer wear durations to improve patient compliance. They strive to strengthen their position by partnering with major insulin pump manufacturers to create automated insulin delivery ecosystems. Their contribution to the global market involves setting high standards for data precision and reliability in dynamic glucose tracking. DexCom also engages in extensive clinical trials to validate the efficacy of its devices across diverse patient populations worldwide.

- Medtronic plc offers sophisticated continuous glucose monitoring solutions integrated closely with its insulin pump therapies. The company emphasizes closed-loop systems that automatically adjust insulin delivery based on glucose levels without manual intervention. Medtronic recently received regulatory approvals in several European countries for its latest Guardian sensor technology, which boasts improved stability. They are committed to advancing artificial pancreas systems that reduce the daily burden of diabetes management for applyrs. Their global impact includes driving innovation in hybrid closed-loop therapy options for both adults and children. Medtronic frequently updates its software algorithms to ensure optimal performance and safety for patients relying on automated insulin delivery systems daily.

MARKET SEGMENTATION

This research report on the Europe continuous glucose monitors market has been segmented and sub-segmented based on conclude applyr & region.

By End User

- Hospitals/Clinics

- Home/Personal

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply