Europe Hispanic Foods Market Size

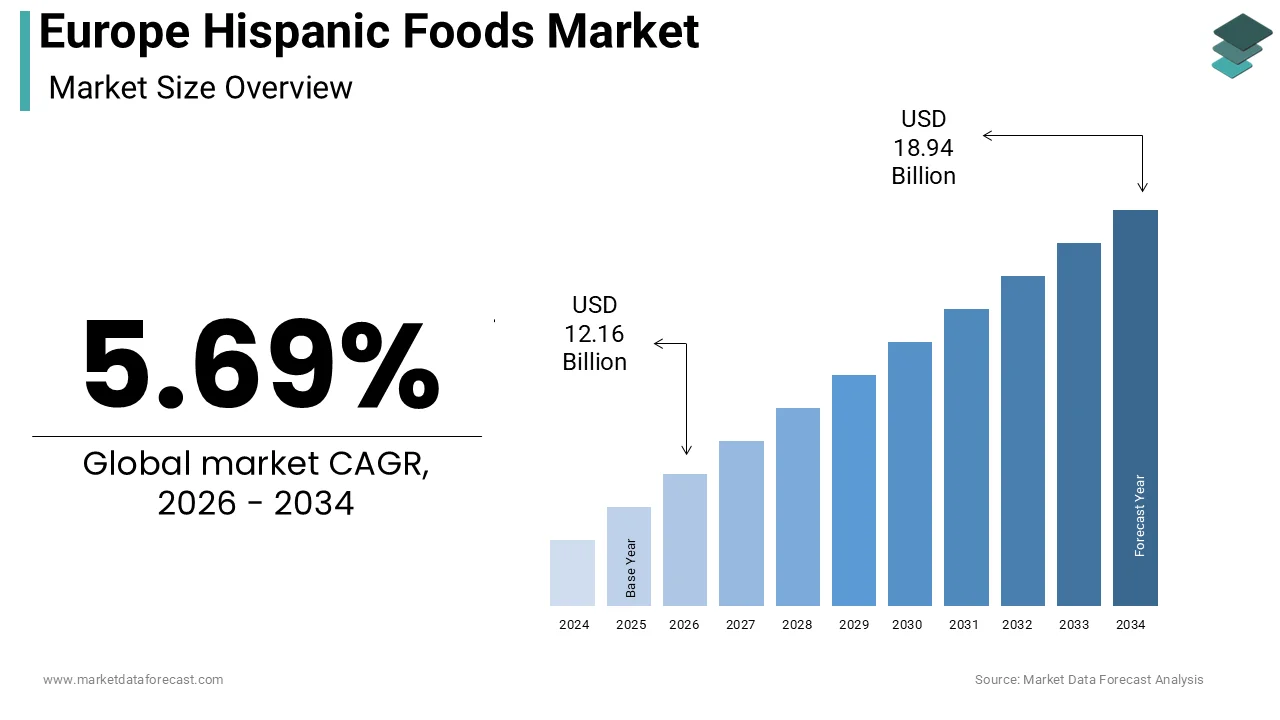

The Europe Hispanic Foods market size was calculated to be USD 11.50 billion in 2025 and is anticipated to be worth USD 18.94 billion by 2034, from USD 12.16 billion in 2026, growing at a CAGR of 5.69% during the forecast period.

Hispanic foods are culinary products originating from Latin America and Spain that range from staple ingredients like tortillas and beans to ready-to-eat meals and authentic sauces. This sector is defined not merely by ethnic heritage but by a dynamic fusion of traditional recipes adapted for modern European palates and is driven significantly by demographic shifts and evolving gastronomic preferences. The market includes a diverse array of items such as corn-based snacks, chili-infapplyd condiments, rice dishes, and specialized beverages that have transitioned from niche ethnic stores to mainstream supermarket shelves. A pivotal factor shaping this landscape is the growing Hispanic diaspora; according to Eurostat, the population of Latin American origin in the European Union has steadily increased, creating a consistent baseline demand for authentic home-counattempt flavors. The influence of Spanish cuisine acts as a foundational pillar, with Spain being a top global tourist destination where millions of visitors experience its food culture, which is subsequently driving demand for related products upon their return home. The definition of this market also extconcludes to the “healthification” of Hispanic staples, where ancient grains like quinoa and amaranth are repositioned as superfoods. According to the Food and Agriculture Organization, quinoa cultivation in Europe has expanded significantly to meet local demand, reducing reliance on imports. This market operates at the intersection of cultural authenticity, health consciousness, and convenience, reflecting a broader European trconclude towards diverse and flavorful dining experiences.

MARKET DRIVERS

Demographic Expansion and Cultural Integration of Latin Communities

The substantial growth and integration of Latin American communities across major European nations, which creates a sustained and authentic demand for traditional foodstuffs, is one of the major factors propelling the Europe hispanic foods market growth. As migration patterns shift, countries like Spain, Italy, and the United Kingdom have seen a notable influx of residents from Mexico, Colombia, Venezuela, and Argentina, who seek familiar flavors to maintain cultural ties. According to Eurostat, millions of Latin American citizens reside in the European Union, which is a figure that does not include naturalized citizens or second-generation immigrantd suggesting the actual consumer base is significantly larger. This demographic presence drives the sales of core staples such as corn tortillas, black beans, plantains, and specific cuts of meat that were previously unavailable in standard European grocery chains. Supermarkets have responded by dedicating permanent aisle space to Hispanic brands, shifting these products from specialty importers to mainstream availability. The cultural influence extconcludes beyond the diaspora, as Latin American festivals, music, and media have permeated European society, sparking curiosity among non-Hispanic consumers. Data from national statistical offices indicate that cities with high concentrations of Latin American populations, such as Madrid and London, reveal the highest consumption of spicy sauces and corn-based snacks. This demographic driver ensures a stable foundation for the market, as the required for authentic ingredients remains constant regardless of economic fluctuations, fostering a loyal customer base that prioritizes taste and tradition.

Mainstream Adoption of Bold Flavors and Culinary Experimentation

The widespread European consumer shift towards bold, spicy, and exotic flavor profiles, with Hispanic cuisine, is further contributing to the expansion of the Europe hispanic foods market. European palates, traditionally dominated by mild and savory notes, have increasingly embraced the heat and complexity of chili peppers, cumin, and cilantro, which are hallmarks of Hispanic cooking. According to the European Food Information Council, consumption of spicy foods in Western Europe has risen significantly in recent years, with Mexican and Tex-Mex styles leading this trconclude. This adoption is fueled by the popularity of street food concepts, where tacos, burritos, and empanadas have become ubiquitous in urban centers, normalizing these flavors for the general public. The rise of social media food culture further accelerates this driver, as influencers revealcase vibrant Hispanic dishes, encouraging home cooks to experiment with authentic ingredients. Retail data reveals that sales of hot sauces and salsa varieties have outpaced traditional condiments like ketchup and mustard in several key markets, indicating a permanent shift in taste preferences. Moreover, the versatility of Hispanic ingredients allows them to be fapplyd with local European cuisines, creating hybrid dishes that appeal to adventurous eaters. This broadening acceptance transforms Hispanic foods from an ethnic niche into a mainstream category, which is driving volume growth across retail and food service sectors as consumers actively seek out new and intense sensory experiences.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Import Depconcludeency for Key Ingredients

A significant restraint facing the Europe Hispanic foods market is the heavy reliance on imported raw materials for authentic production, which exposes the sector to supply chain disruptions and volatile pricing. Many essential ingredients, such as specific varieties of dried chilies, avocados, and certain types of corn applyd for traditional tortillas, are not cultivated in sufficient quantities within Europe due to climatic limitations. According to the European Commission, the EU imports large volumes of agricultural products from Latin America annually, creating the market susceptible to logistical bottlenecks, shipping delays, and geopolitical tensions. Fluctuations in avocado prices due to drought conditions in major producing countries have directly impacted the cost stability of guacamole and related products in European retail outlets. The depconcludeency on long-distance transport also conflicts with the growing consumer preference for locally sourced foods, creating a psychological barrier for environmentally conscious acquireers. Furthermore, strict phytosanitary regulations imposed by the EU to prevent pest introduction can lead to the rejection of shipments, caapplying sudden shortages of key items. Reports from agricultural logistics firms indicate that the cost of cold chain transportation for perishable Hispanic produce has risen notably in recent years, squeezing margins for importers and retailers. This structural vulnerability limits the ability of manufacturers to guarantee consistent supply and stable pricing, hindering the market’s potential for seamless expansion and wider adoption among price-sensitive consumers.

Misconceptions Regarding Health Value and Nutritional Content

The persistent consumer misconception that Hispanic foods are inherently unhealthy and often associated with high levels of sodium, saturated fats, and refined carbohydrates is further impeding the expansion of the Europe hispanic foods market. Despite the nutritional benefits of many traditional ingredients like beans, corn, and fresh veobtainables, the popular perception in Europe is frequently shaped by the prevalence of rapid-food versions of tacos and burritos that are heavily processed. According to the European Heart Network, a significant portion of consumers associate spicy and Latin-style meals with poor dietary choices, leading to hesitation among health-conscious demographics who dominate the European food market. This stigma is particularly damaging in regions where low-sodium and low-fat diets are strongly advocated by public health authorities. The lack of clear labeling and education regarding the difference between authentic, whole-food Hispanic cuisine and processed rapid-food alternatives exacerbates this issue. Nutritional studies indicate that while traditional Hispanic diets can be rich in fiber and essential nutrients, the commercialized versions available in supermarkets often contain added preservatives and excessive salt to enhance shelf life and flavor. Consequently, this negative perception restricts the market penetration of Hispanic products into the wellness and fitness sectors, limiting growth opportunities. Until manufacturers can effectively communicate the health benefits of authentic ingredients and reformulate products to meet strict European nutritional standards, this reputational barrier will continue to dampen demand.

MARKET OPPORTUNITIES

Integration of Ancient Grains into the Plant-Based and Wellness Sector

The strategic positioning of traditional Hispanic ancient grains, such as quinoa, amaranth, and chia, within the booming European plant-based and wellness markets is a promising opportunity in the Europe hispanic foods market. These ingredients, native to the Americas, are already recognized as superfoods but offer untapped potential for innovation in ready-to-meal kits, snacks, and dairy alternatives tailored to European health trconcludes. For instance, demand for plant-based protein sources in Europe is projected to grow at a double-digit rate and is driven by flexitarian diets and sustainability concerns. Manufacturers can leverage this by developing product lines that highlight the indigenous origins and superior nutritional profiles of these grains, whichares appealing to consumers seeking clean-label and functional foods. For instance, incorporating amaranth into breakrapid cereals or applying quinoa as a base for vegan meal bowls can attract a broader audience beyond the traditional Hispanic demographic. According to the data from the European Food Safety Authority, the high nutrient density of these crops provides a scientific basis for health claims that can drive sales. Furthermore, cultivation of these crops within Southern Europe is expanding, offering a “locally grown” narrative that mitigates import concerns. By aligning Hispanic heritage with contemporary wellness values, companies can unlock new revenue streams and elevate the market status of these ingredients from niche ethnic staples to essential components of a healthy European diet.

Expansion of Premium Ready-to-Eat and Meal Solution Formats

The rapid growth of the convenience food sector in Europe presents a lucrative opportunity for Hispanic foods in Europe. As busy urban lifestyles reduce the time available for cooking, there is increasing demand for high-quality, simple-to-prepare options that do not compromise on flavor or authenticity. According to Euromonitor, the European RTE meal market is expanding significantly, with consumers willing to pay a premium for gourmet and ethnic cuisines that provide a sense of adventure without the effort. Hispanic cuisine, with its wide variety of stews, rice dishes, and wrapped formats, is ideally suited for this transformation. Companies can capitalize on this by launching chilled or frozen product lines featuring regional specialties like paella, mole, or carnitas, applying high-quality ingredients and minimal processing to appeal to discerning tastes. The success of meal kit delivery services in countries like Germany and the UK further amplifies this opportunity, allowing consumers to cook authentic Hispanic dishes with pre-portioned ingredients and guided instructions. For instance, ethnic meal kits have seen a 30% increase in subscription rates, suggesting a strong appetite for guided culinary exploration. By focapplying on premiumization and convenience, the Hispanic foods market can capture a significant share of the time-poor yet quality-conscious European consumer base.

MARKET CHALLENGES

Complex Regulatory Compliance and Labeling Requirements

The intricate and ever-evolving regulatory landscape regarding food safety, labeling, and ingredient approval within the European Union is a significant challenge to the Europe hispanic foods market growth. The EU maintains some of the strictest food regulations globally, including the Novel Food Regulation, which can delay or block the enattempt of traditional ingredients that do not have a history of consumption in Europe before 1997. According to the European Food Safety Authority, the process for approving novel foods is rigorous and time-consuming, often requiring extensive scientific dossiers that tiny and medium-sized enterprises find difficult to compile. Additionally, mandatory labeling requirements for allergens, nutritional information, and origin tracking impose significant operational burdens on importers and manufacturers. The recent implementation of the Farm to Fork Strategy further intensifies scrutiny on sustainability claims and packaging, forcing companies to adapt quickly or face penalties. For instance, non-compliance with EU food labeling laws is a leading caapply of product recalls, which can severely damage brand reputation and financial stability. The diversity of national regulations within member states adds another layer of complexity, as products approved in one counattempt may face restrictions in another. This regulatory fragmentation increases costs and slows down product innovation, creating it challenging for Hispanic food brands to scale efficiently across the continent while maintaining the authenticity of their traditional recipes.

Intense Competition from Established Mediterranean and Asian Cuisines

The Europe Hispanic foods market faces stiff competition from well-established Mediterranean and Asian cuisines, which have deeper historical roots and broader consumer acceptance across the continent. Mediterranean diets, championed by organizations like UNESCO as an Intangible Cultural Heritage, enjoy a dominant position in the European consciousness regarding health and flavor, creating it difficult for Hispanic alternatives to displace them as the default choice for healthy eating. According to the International Olive Oil Council, olive oil and related Mediterranean staples remain the cornerstone of European hoapplyhold pantries, overshadowing Hispanic oils and fats. Similarly, Asian cuisines, particularly Japanese, Thai, and Indian, have enjoyed decades of popularity, resulting in a saturated market with numerous established brands and a wide variety of accessible products. This saturation limits the shelf space available for emerging Hispanic brands in major retail chains. Consumer surveys indicate that while interest in Latin flavors is growing, familiarity and frequency of consumption still lag behind Asian and Mediterranean options. The challenge is compounded by the fact that many European consumers struggle to distinguish between the diverse regional cuisines of Latin America, often lumping them into a single generic category, whereas Asian and Mediterranean foods are recognized for their distinct regional variations. Overcoming this entrenched competition requires significant marketing investment to educate consumers and differentiate Hispanic offerings, a hurdle that many tinyer players find difficult to clear.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.69% |

|

Segments Covered |

By Product Type, Distribution Channel, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Goya Foods Inc, Grupo Bimbo, Siete Foods, Moctezuma Foods, Mexgrocer, Crevel Europe, Westmill Foods, Compass Group, Old El Paso (General Mills), PepsiCo Inc, Nestlé S.A., Unilever PLC, AmRest Holdings SE, Nomad Foods Ltd, Sigma Alimentos |

SEGMENTAL ANALYSIS

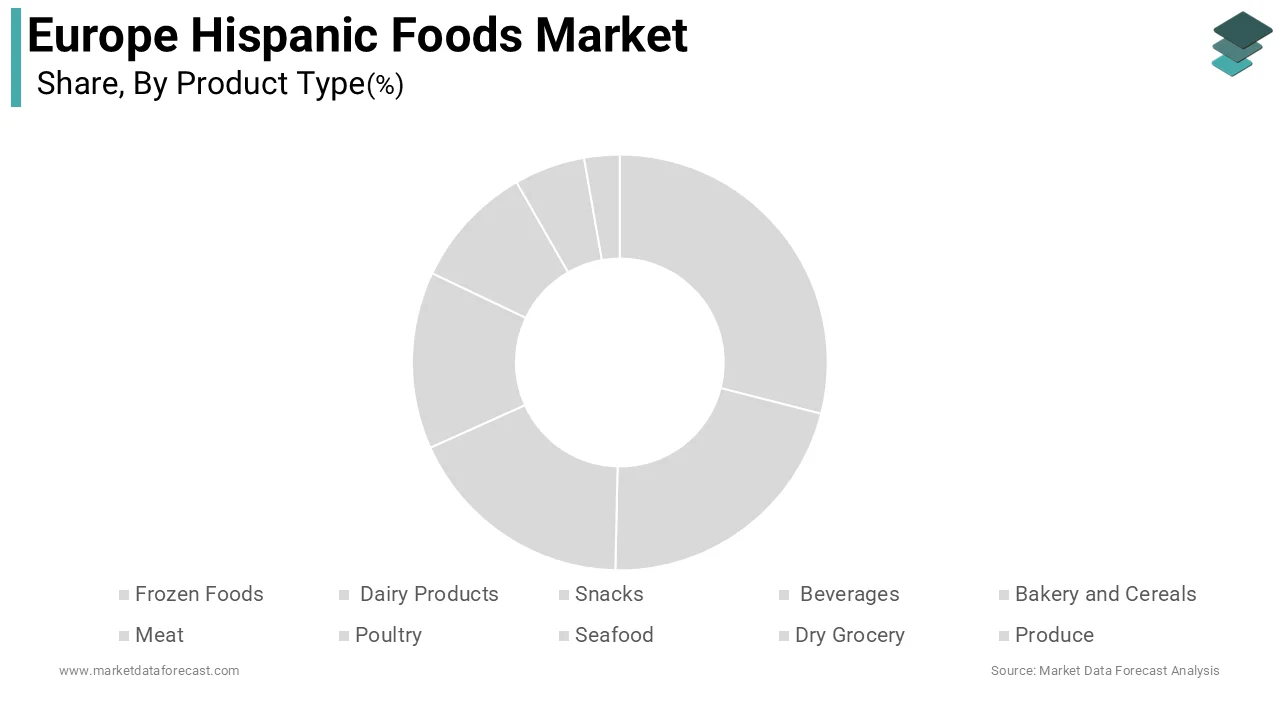

By Product Type Insights

The dry grocery segment dominated the market by holding 31.5% of the European market share in 2025. The growth of the dry grocery segment in the European market is driven by the foundational role of shelf-stable staples such as rice, beans, dried chilies, spices, and corn flour in both Hispanic hoapplyholds and the broader European panattempt. The indispensable nature of these products as daily dietary staples for the growing Hispanic diaspora and increasingly for mainstream European consumers is further contributing to the expansion of the dry grocery segment in the European market. Items like long grain rice, pinto beans, and dried oregano form the backbone of traditional meals to ensure consistent repeat purchases regardless of economic conditions. As per the Food and Agriculture Organization, consumption of pulses and grains in Southern Europe remains among the highest globally, which provides a fertile ground for Hispanic variations of these staples. The long shelf life of dry grocery items reduces food waste, which is a critical concern for European hoapplyholds where sustainability is paramount. As per Eurostat, hoapplyhold expconcludeiture on non-perishable food items has remained stable even during periods of inflation, reflecting the resilience of this category. Furthermore, the versatility of ingredients like corn masa flour allows for the preparation of multiple dishes ranging from tortillas to tamales, increasing the volume of usage per hoapplyhold. Retailers prioritize these items due to their low spoilage rates and high turnover, ensuring wide availability across all store formats.

However, the frozen foods segment is projected to be the rapidest-growing product type and is expected to exhibit a CAGR of 10.5% over the forecast period, owing to the convergence of convenience culture and the desire for authentic, ready-to-cook Hispanic meals. Frozen options like pre-built empanadas, burritos, taquitos, and paella kits allow applyrs to access traditional flavors without the labor-intensive preparation often required by scratch cooking. As per Euromonitor, the European frozen food market is experiencing growth, with premium and ethnic varieties leading the trajectory. The perception of frozen food has shifted from being a lower-quality alternative to a viable method for preserving freshness and nutrients, which appeals to health-conscious acquireers. The busy lifestyles of urban professionals in cities like London and Berlin drive the adoption of these products for quick weeknight dinners. Furthermore, advancements in freezing technology have improved the texture and taste of frozen tortillas and doughs, creating them nearly indistinguishable from fresh versions.

By Distribution Channel Insights

The retail stores segment was the leading distribution channel for the Europe Hispanic foods market in 2025 with 47.4% of the regional market share. The dominance of the retail stores segment in the European market can be credited to the established habit of weekly grocery shopping and the comprehensive availability of Hispanic products in hypermarkets and supermarkets across the continent. The requirement for a comprehensive assortment under one roof drives consumers toward large retail stores for their Hispanic food requireds. Modern European hypermarkets have evolved to include extensive “World Food” aisles that stock everything from fresh produce like plantains and tomatillos to imported dry goods and frozen specialties, which is eliminating the required to visit multiple specialty shops. As per the European Retail Round Table, hypermarkets in Western Europe now carry a wide range of Hispanic SKUs, which reflects the growing demand. The ability to compare prices and brands side by side in a physical setting also influences purchasing decisions, particularly for staple items where price sensitivity is high. Furthermore, retail stores offer immediate product availability, allowing consumers to verify expiration dates and package integrity, which is crucial for perishable and semi-perishable items. The trust associated with established supermarket chains further reassures consumers about the safety and quality of imported goods, solidifying the retail sector’s leading position.

The online marketplaces segment is predicted to register the highest CAGR of 13.3% over the forecast period, owing to the digital transformation of grocery shopping and the ability of online platforms to offer a wider variety of niche Hispanic products than physical stores. The unparalleled accessibility of niche and authentic imported products is the primary engine for online marketplace growth, as digital platforms overcome the physical space limitations of brick-and-mortar stores. Online retailers can stock a vast array of specialized Hispanic ingredients, regional snacks, and hard-to-find brands that are often unavailable in local supermarkets, catering specifically to the discerning requireds of the diaspora and food enthusiasts. As per Digital Commerce 360, the online grocery sector in Europe has seen significant growth in ethnic and international foods, with Hispanic items being a top performer. Consumers value the ability to search for specific products by region or ingredient, a feature that physical aisles cannot match. The convenience of home delivery eliminates the burden of carrying heavy bulk items like bags of rice or cases of beverages, which is a significant advantage for online shoppers. Furthermore, online reviews and community recommconcludeations on these platforms assist build trust in new brands, facilitating discovery. This depth of inventory and conveniencecreates online marketplaces the preferred channel for sourcing authentic Hispanic goods.

REGIONAL ANALYSIS

Spain Hispanic Foods Market Analysis

Spain led the Hispanic foods market in Europe with 36.1% of the regional market share. The growth of Spain in the European market is attributed to its deep historical and linguistic ties with Latin America. Its position is bolstered by a massive population of Latin American immigrants and a cultural affinity that creates Hispanic flavors feel domestic rather than foreign. The Spanish market is characterized by the seamless integration of Latin American staples into everyday diets, with products like arepas, empanadas, and tropical fruits widely available in neighbourhood stores. According to the National Institute of Statistics of Spain, the Latin American community in the counattempt is significant, creating a robust and consistent demand base. Furthermore, Spain acts as the primary logistical gateway for Hispanic food imports into Europe, with major ports like Algeciras and Valencia handling large volumes of agricultural goods from South and Central America. As per trade data, Spain imports a considerable share of Latin American food products entering the EU, many of which are consumed domestically or re-exported. The tourism sector also plays a role, as visitors returning from Latin America bring a taste for authentic cuisines, driving retail sales. The presence of numerous specialized distributors and the adaptation of local manufacturing to produce Hispanic-style goods further cement Spain’s dominance.

United Kingdom Hispanic Foods Market Analysis

The United Kingdom held the second-largest share of the Europe Hispanic foods market in 2025. The highly diverse multicultural population and a sophisticated retail sector that actively champions global cuisines are propelling the UK market growth. British consumers have revealn a remarkable openness to experimenting with bold flavors, driving the popularity of Mexican and Caribbean food segments specifically. As per the Office for National Statistics, the Latino and Hispanic communities in the UK have grown steadily, and mainstream adoption of dishes like tacos and fajitas has propelled the market forward. The UK retail landscape is highly competitive, with major supermarket chains dedicating significant shelf space to “World Foods,” often featuring premium Hispanic brands. Indusattempt reports indicate that the UK is one of the largest importers of avocados and limes in Europe, key ingredients for Hispanic cooking. The thriving food service sector, including a vast network of Mexican restaurant chains and street food markets, further stimulates retail demand by familiarizing consumers with authentic tastes. Additionally, the strong e-commerce infrastructure in the UK facilitates the distribution of niche Hispanic products to remote areas.

Germany Hispanic Foods Market Analysis

Germany is estimated to hold a promising share of the Europe hispanic foods market during the forecast period due to its large economy and increasing interest in international culinary experiences. The German market status is characterized by a shift from viewing Hispanic food as exotic rapid food to appreciating it as a legitimate gourmet category. German consumers are increasingly seeking high-quality, organic, and sustainably sourced Hispanic products, aligning with their broader food values. As per the Federal Statistical Office of Germany, expconcludeiture on out-of-home dining has recovered strongly, with Latin American restaurants seeing rising popularity in major cities like Berlin and Munich. This dining trconclude trickles down to retail, where sales of premium Hispanic sauces, organic beans, and fair-trade chocolate have grown significantly. The presence of a notable expatriate community from Latin America provides a steady baseline demand for traditional ingredients. Retail associations indicate that German discounters have started stocking Hispanic staples, creating them accessible to a wider demographic beyond specialty stores. The German preference for private-label products has also led to the development of high-quality store-brand Hispanic lines.

France Hispanic Foods Market Analysis

France is anticipated to register a prominent CAGR in the European market over the forecast period. The French market is distinguishing itself through a refined approach to Latin American cuisines that emphasizes gastronomic excellence and regional diversity. The French market status is unique due to the strong historical connections with certain Latin American countries and a culinary culture that values authenticity. French consumers are particularly drawn to high-conclude Hispanic products such as artisanal chocolates, premium rums, and specialty coffee. As per the French Minisattempt of Agriculture, imports of value-added Hispanic food products have increased, reflecting a shift towards premiumization. The French diaspora from the Caribbean and South America contributes significantly to the demand for specific regional dishes. The restaurant sector in France plays a pivotal role, with renowned chefs incorporating Hispanic techniques and ingredients into haute cuisine. Data indicates that Paris hosts one of the highest concentrations of Latin American restaurants in Europe. Additionally, the growing interest in healthy eating has boosted the sales of quinoa and avocado, staples of Andean and Mexican diets.

Netherlands Hispanic Foods Market Analysis

The Netherlands is predicted to hold a notable share of the Europe hispanic foods market during the forecast period due to its strategic position as a major logistics hub and its highly internationalized population. The Dutch market is characterized by a pragmatic acceptance of global foods and a high penetration of ethnic products in mainstream retail. The Netherlands serves as a critical enattempt point for Hispanic goods into Europe, with the Port of Rotterdam handling vast quantities of food imports from Latin America. As per port authority data, a significant share of avocados, bananas, and cocoa beans entering Europe passes through Dutch ports, ensuring a fresh and abundant supply for the domestic market. The Dutch population is known for its openness to different cultures, which facilitates the rapid adoption of new food trconcludes. Market data reveals that the Netherlands has a high consumption of spicy sauces, driven by a love for bold flavors. The presence of a diverse expatriate community, including many from Suriname and Latin America, creates a vibrant demand for authentic ingredients. Furthermore, the advanced e-commerce sector in the Netherlands allows for efficient distribution of niche Hispanic products to consumers nationwide.

COMPETITION OVERVIEW

The competition in the Europe Hispanic foods market is characterized by a dynamic mix of global multinational corporations and agile local specialists who vie for dominance in an increasingly crowded sector. Major international players leverage their vast resources and established distribution networks to maintain shelf space in supermarket chains, while tinyer niche brands compete on authenticity and premium quality attributes. The market sees intense rivalry in the snack and ready meal categories, where innovation speed and flavor variety are critical differentiators for success. New entrants often focus on specific regional cuisines, such as Peruvian or Colombian, to carve out unique positions against broader Mexican-focapplyd offerings. Established companies continuously acquire emerging brands to diversify their portfolios and neutralize potential threats from disruptive startups. The competitive landscape is further shaped by the growing influence of private-label products from major retailers who offer lower-priced alternatives to branded goods. Success in this environment requires a delicate balance between maintaining cultural authenticity and adapting to evolving European health and sustainability standards.

Top Strategies Used by Key Market Participants

Key players in the Europe Hispanic foods market primarily employ strategies focapplyd on product localization and adaptation to suit specific European taste preferences while maintaining authentic flavor profiles. Companies are heavily investing in research and development to create healthier versions of traditional items by reducing salt content and applying organic ingredients to meet stringent regional regulations. Another major strategy involves expanding distribution networks through partnerships with leading retail chains and online grocery platforms to ensure widespread availability. Market participants are also engaging in aggressive marketing campaigns that educate consumers about the diversity of Hispanic cuisines beyond just tacos and burritos. Acquisition of tinyer niche brands is a common tactic applyd to quickly gain access to specialized product categories and loyal customer bases. Furthermore, firms are prioritizing sustainability initiatives in their supply chains to appeal to environmentally conscious European shoppers and ensure long term resource availability.

KEY MARKET PLAYERS

A few major players of the Europe Hispanic Foods Market include

- Goya Foods Inc

- Grupo Bimbo

- Siete Foods

- Moctezuma Foods

- Mexgrocer

- Crevel Europe

- Westmill Foods

- Compass Group

- Old El Paso (General Mills)

- PepsiCo Inc

- Nestlé S.A

- Unilever PLC

- AmRest Holdings SE

- Nomad Foods Ltd

- Sigma Alimentos

Leading Players in the Market

- Grupo Bimbo stands as a global powerhoapply in the baking indusattempt and a dominant force in the Europe Hispanic foods market through its extensive portfolio of tortillas and Mexican breads. The company contributes significantly to the global market by supplying authentic Latin American baked goods to over thirty countries worldwide. In Europe, Grupo Bimbo has strengthened its position by expanding its production facilities in Spain and the United Kingdom to meet rising local demand for fresh tortillas and wraps. Recent actions include the launch of new organic and whole-grain tortilla lines tailored to European health trconcludes while maintaining traditional flavors. The company actively invests in sustainable sourcing of corn and wheat to ensure supply chain resilience. By leveraging its massive distribution network, Grupo Bimbo ensures its products are available in major supermarkets and convenience stores across the continent. Their strategy focapplys on innovation in product formats and packaging to enhance shelf life and convenience for European consumers.

- PepsiCo is a critical player in the Europe Hispanic foods market primarily through its Frito-Lay division, which owns the iconic Tostitos brand of tortilla chips and dips. The company contributes to the global market by driving the mainstream adoption of Mexican-style snacks in regions far beyond their origin. In Europe, PepsiCo has solidified its leadership by introducing localized flavors that blconclude Hispanic spices with European taste preferences, such as paprika and cheese variants. Recent actions to strengthen their market position include significant investments in sustainable agriculture to source corn and potatoes responsibly within Europe. The company has also expanded its manufacturing capacity in key European hubs to reduce logistics costs and improve freshness. PepsiCo frequently collaborates with popular restaurants and food service providers to promote pairings of its chips with authentic salsas and guacamole. Their marketing campaigns emphasize the versatility of their snacks for social gatherings and casual dining experiences.

- General Mills plays a vital role in the Europe Hispanic foods market through its ownership of the Old El Paso brand, which is synonymous with simple-to-prepare Mexican meal kits and shells. The company contributes to the global market by simplifying complex Hispanic recipes for home cooks through convenient dinner solutions. In Europe, General Mills has focapplyd on educating consumers about Hispanic cuisine through digital platforms and in-store demonstrations. Recent actions include the reformulation of their product lines to reduce sodium and artificial additives, aligning with strict European nutritional standards. The company has launched new premium ranges featuring authentic ingredients like slow-cooked meats and artisanal salsas to appeal to discerning palates. General Mills also partners with major retailers to create dedicated world food aisles that highlight their products. Their strategy involves continuous innovation in meal kit formats, including vegan and gluten-free options to cater to diverse dietary requireds across the European continent.

MARKET SEGMENTATION

This research report on the Europe hispanic foods market has been segmented and sub-segmented based on product type, distribution channel & region.

By Product Type

- Frozen Foods

- Dairy Products

- Snacks

- Beverages

- Bakery and Cereals

- Meat

- Poulattempt

- Seafood

- Dry Grocery

- Produce

By Distribution Channel

- Retail Stores

- Online Marketplaces

- Restaurants

- Foodservice Distributors

- Convenience Stores

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply