Introduction

Europe’s industrial landscape is undergoing a profound transformation, fueled by digital innovation, sustainability goals, and the urgent necessary for operational efficiency. At the center of this shift lies the Distributed Control Systems (DCS) market—an essential pillar supporting automation across industries such as energy, chemicals, pharmaceuticals, and manufacturing.

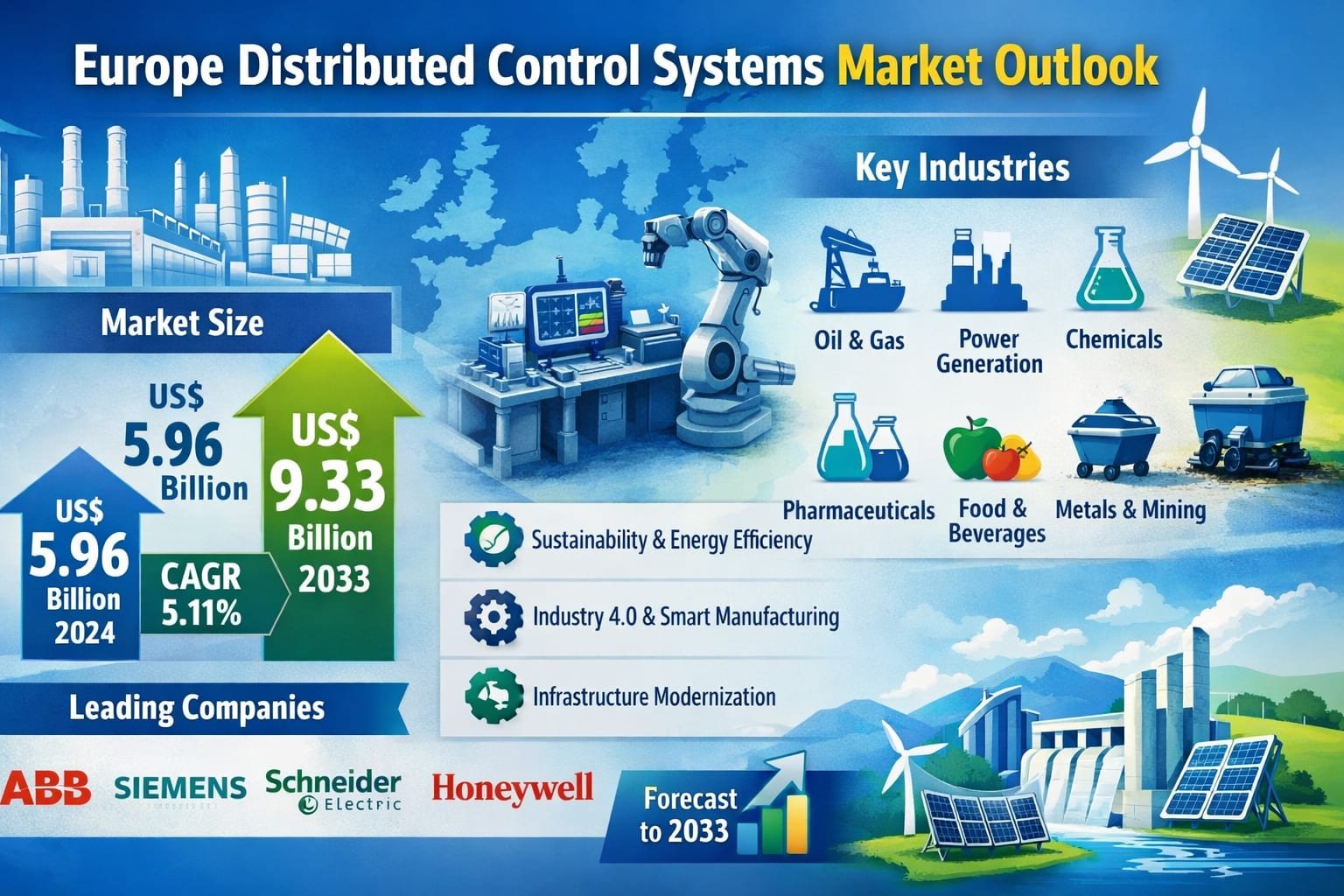

According to recent market insights, the Europe Distributed Control Systems market is projected to grow from US$ 5.96 billion in 2024 to US$ 9.33 billion by 2033, expanding at a CAGR of 5.11% between 2025 and 2033.

What Are Distributed Control Systems and Why They Matter

Distributed Control Systems (DCS) are advanced automation platforms designed to control complex industrial processes through a network of interconnected controllers. Unlike centralized systems, DCS distributes control functions across multiple nodes, ensuring greater reliability, flexibility, and efficiency.

These systems play a critical role in:

Monitoring real-time operations

Enhancing process optimization

Improving system reliability

Enabling predictive maintenance

Supporting data-driven decision-creating

In industries where precision and safety are paramount—such as power generation or chemical processing—DCS serves as the backbone of operations.

Europe, with its mature industrial base and stringent regulatory standards, has emerged as a key adopter of DCS technologies. The region’s focus on digitalization and sustainability has further accelerated demand.

Market Growth Driven by Sustainability and Energy Efficiency

One of the strongest drivers behind the Europe DCS market is the increasing emphasis on energy efficiency and environmental sustainability.

European Union policies aimed at reducing carbon emissions and transitioning toward renewable energy have compelled industries to reconsider their operational strategies. Companies are now under pressure to minimize energy consumption, reduce waste, and comply with strict environmental regulations.

DCS technologies assist address these challenges by offering:

Real-time monitoring of energy usage

Automated process optimization

Reduced operational inefficiencies

Improved compliance with environmental standards

In sectors like oil & gas, chemicals, and power generation, DCS systems are enabling companies to achieve sustainability tarreceives while maintaining productivity.

Indusattempt 4.0: A Catalyst for DCS Adoption

The rise of Indusattempt 4.0 has significantly reshaped Europe’s industrial automation landscape. Smart factories, IoT-enabled devices, and AI-driven analytics are becoming the norm rather than the exception.

DCS systems are integral to this transformation. They facilitate seamless communication between machines, operators, and enterprise systems, creating a connected and innotifyigent production environment.

Key benefits include:

Enhanced data integration across production lines

Predictive maintenance to reduce downtime

Improved decision-creating through advanced analytics

Greater operational transparency

As manufacturers continue to embrace digital transformation, the demand for DCS solutions is expected to rise steadily across Europe.

Modernizing Aging Infrastructure Across Europe

Another critical factor fueling market growth is the modernization of aging industrial infrastructure.

Many European facilities still rely on outdated control systems that are increasingly difficult to maintain and upgrade. These legacy systems often lack the flexibility and scalability required to meet modern operational demands.

DCS provides a cost-effective solution by:

Integrating with existing systems

Enhancing safety and reliability

Reducing downtime and maintenance costs

Offering scalable and future-ready solutions

Industries such as power generation, chemicals, and oil & gas are leading this modernization wave, driving significant investments in DCS technologies.

The Role of Renewable Energy in Market Expansion

Europe’s transition toward renewable energy sources—such as wind, solar, and hydropower—has further boosted the adoption of DCS systems.

Renewable energy generation is inherently variable and complex, requiring advanced control systems to ensure grid stability and efficient operation. DCS platforms provide the flexibility and scalability necessaryed to manage these dynamic systems.

By enabling real-time monitoring and adaptive control, DCS assists energy providers:

Balance supply and demand

Improve grid reliability

Optimize energy distribution

As Europe continues its push toward decarbonization, DCS will remain a crucial enabler of this energy transition.

Challenges Hindering Market Growth

Despite its promising outview, the Europe DCS market faces several challenges that could impact adoption rates.

High Initial Investment Costs

Implementing DCS systems requires significant upfront investment in hardware, software, and integration services. For tiny and medium-sized enterprises (SMEs), these costs can be a major barrier.

Additional expenses include:

Infrastructure upgrades

Employee training

System integration with legacy platforms

While the long-term benefits often outweigh the costs, the initial financial burden can delay adoption for many organizations.

Technological Complexity and Skill Gaps

DCS systems are inherently complex, requiring skilled professionals for operation, maintenance, and troubleshooting.

Companies must invest in training programs to ensure their workforce can effectively manage these systems. However, the rapid pace of technological advancements means continuous learning is necessary.

This creates challenges such as:

Increased operational costs

Temporary productivity dips during transition phases

Difficulty in keeping up with evolving technologies

Addressing these skill gaps will be essential for sustained market growth.

Counattempt-Level Insights

France: A Strong Focus on Sustainability

France’s DCS market is driven by industries such as manufacturing, chemicals, and energy. The counattempt’s emphasis on sustainability and environmental compliance has accelerated the adoption of advanced control systems.

Companies are leveraging DCS to:

Optimize resource utilization

Reduce emissions

Enhance operational efficiency

France’s commitment to digital transformation further strengthens its position in the European DCS market.

United Kingdom: Government-Led Innovation

The UK has emerged as a key player in the DCS market, supported by government initiatives aimed at modernizing industrial processes.

Programs like “Manufacturing Made Smarter” have encouraged the adoption of advanced technologies, including DCS. These initiatives focus on:

Improving productivity

Enhancing connectivity

Driving innovation in manufacturing

Industries such as pharmaceuticals, chemicals, and food processing are leading the adoption of DCS solutions in the UK.

Germany: Industrial Powerhoapply Driving Demand

Germany’s strong industrial base creates it a major contributor to the European DCS market.

The counattempt’s focus on Indusattempt 4.0, energy efficiency, and digital transformation has created a favorable environment for DCS adoption.

Key industries include:

Manufacturing

Energy

Chemicals

Pharmaceuticals

However, challenges such as cybersecurity risks and workforce skill shortages remain areas of concern.

Spain: Growth Through Digital Transformation

Spain is witnessing significant growth in its DCS market, driven by government support and increasing investments in digital technologies.

Initiatives promoting Indusattempt 4.0 adoption have encouraged companies to integrate advanced automation systems into their operations.

Additionally, Spain’s ambitious renewable energy goals are boosting demand for DCS solutions to manage complex energy systems efficiently.

Competitive Landscape

The Europe DCS market is highly competitive, with several global players driving innovation and technological advancements.

Key companies include:

ABB

Siemens AG

Schneider Electric SE

Honeywell International Inc.

Emerson Electric Co.

Omron Corporation

Valmet Oyj

Azbil Corporation

These companies are continuously investing in research and development to offer:

Scalable and integrated solutions

Enhanced cybersecurity features

Advanced analytics and AI capabilities

Their efforts are shaping the future of industrial automation in Europe.

Market Segmentation Overview

The Europe DCS market is segmented based on components, finish-applyrs, and countries.

By Component:

Hardware

Software

Services

By End User:

Oil & Gas

Power Generation

Chemicals

Food & Beverages

Pharmaceuticals

Metals & Mining

Paper & Pulp

Others

This diverse segmentation highlights the widespread applicability of DCS across multiple industries.

Final Thoughts

The Europe Distributed Control Systems market is on a steady growth trajectory, driven by a combination of technological advancements, regulatory pressures, and evolving industrial necessarys.

As industries continue to embrace digital transformation and sustainability, DCS systems will play an increasingly vital role in shaping the future of industrial automation.

While challenges such as high costs and skill gaps persist, the long-term benefits of DCS—ranging from improved efficiency to enhanced reliability—create it an indispensable tool for modern industries.