Europe Tilapia Market Report Summary

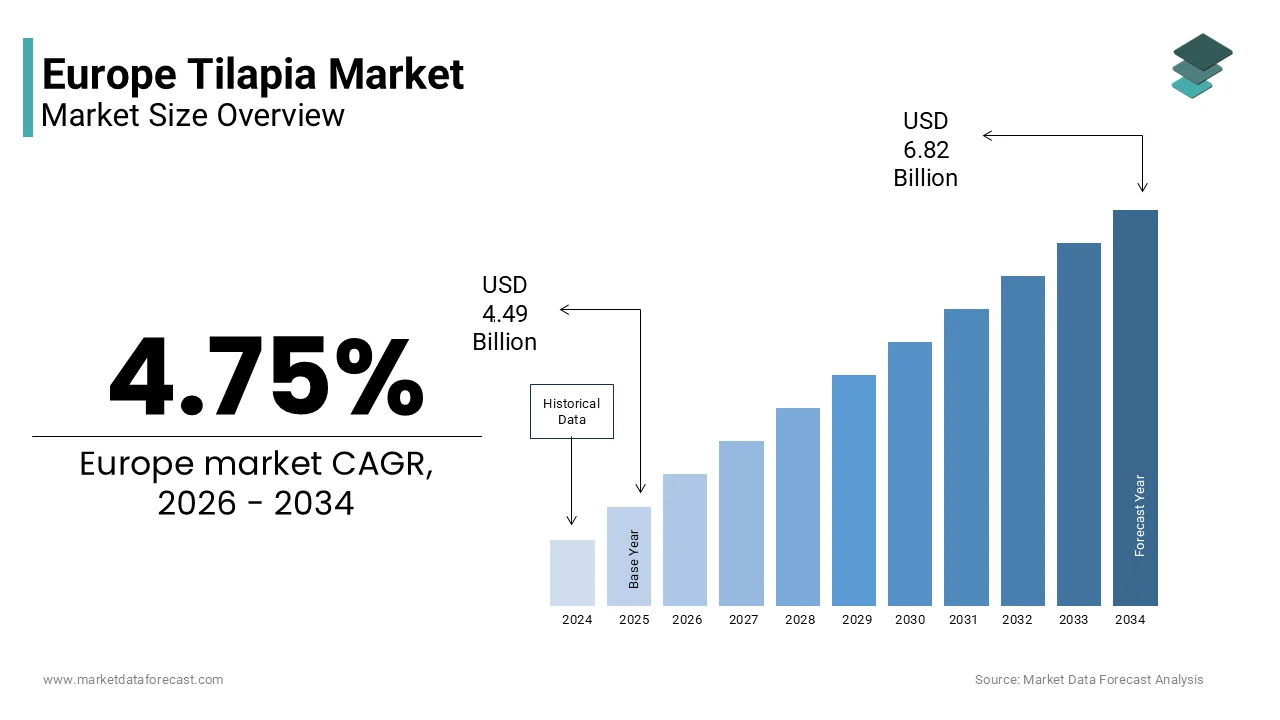

The Europe tilapia market was valued at USD 4.49 billion in 2025, is estimated to reach USD 4.70 billion in 2026, and is projected to reach USD 6.82 billion by 2034, growing at a CAGR of 4.75% during the forecast period from 2026 to 2034. The growth of the Europe tilapia market is driven by increasing consumer demand for affordable and protein rich seafood, rising awareness of healthy diets, and growing preference for mild flavored fish varieties. The expansion of retail distribution channels, steady supply through aquaculture, and rising consumption of convenient seafood products are further supporting market growth. Additionally, tilapia’s versatility in cooking and its cost effectiveness compared to other fish species are enhancing its popularity across European consumers.

Key Market Trconcludes

- Growing demand for nile tilapia driven by its wide availability, mild taste, and adaptability in various cuisines.

- Increasing dominance of retail distribution channels supported by expanding supermarket chains and consumer preference for at home consumption.

- Rising consumption of affordable and protein rich seafood due to increasing health awareness.

- Expansion of aquaculture production ensuring consistent supply and stable pricing of tilapia.

- Growing popularity of ready to cook and frozen tilapia products aligned with convenience driven lifestyles.

Segmental Insights

- Based on species, the nile tilapia segment was the largest and held a significant share of the Europe tilapia market in 2025. The dominance of this segment is attributed to its high yield, cost efficiency, and strong consumer acceptance across European markets.

- Based on application, the retail segment accounted for 55.4% of the Europe tilapia market share in 2025. The segment growth is driven by increasing consumer purchases through supermarkets, hypermarkets, and retail outlets for home consumption.

Regional Insights

- The Europe tilapia market is experiencing steady growth across key countries driven by rising seafood consumption and expanding retail infrastructure.

- Germany was the top performer, accounting for 22.3% of the Europe tilapia market share in 2025, driven by strong demand for affordable seafood, increasing retail penetration, and growing consumer preference for healthy protein sources.

Competitive Landscape

The Europe tilapia market is competitive with several global and regional players focutilizing on supply chain optimization, sustainable aquaculture, and product diversification. Companies are investing in expanding aquaculture operations, improving processing capabilities, and strengthening retail partnerships to enhance market presence. Prominent players in the Europe tilapia market include Regal Springs, High Liner Foods Inc., Thai Union Group PLC, Surapon Foods Public Company Limited, Charoen Pokphand Foods, Mowi ASA, Kühne + Heitz, SeaOptima, Tilapez, and Nomad Foods Ltd.

Europe Tilapia Market Size

The Europe tilapia market size was valued at USD 4.49 billion in 2025 and is projected to reach USD 6.82 billion by 2034 from USD 4.70 billion in 2026, growing at a CAGR of 4.75%.

The tilapia broader continental seafood industest, defined by the importation, distribution, and consumption of Oreochromis species, primarily sourced from external aquaculture hubs. According to the Food and Agriculture Organization of the United Nations, global aquaculture now provides more than 50% of all fish intconcludeed for human consumption, a statistic that underpins the volume of tilapia entering European ports annually. The European Union acts as a major destination for these imports, with recent data indicating that the bloc imported approximately 280000 tonnes of tilapia fillets, largely originating from Latin American and Asian producers. As per Eurostat, the average per capita fish consumption in the European Union remains steady at roughly 24 kilograms per year, creating a consistent baseline demand that tilapia assists to satisfy amidst declining wild catch volumes. Retail dynamics display a clear shift towards frozen formats, with major supermarket chains in Germany, France, and the United Kingdom expanding their private label offerings to capture cost conscious demographics.

MARKET DRIVERS

Economic Pressures Driving Demand for Cost Effective Protein

The intensifying economic pressure on European houtilizeholds, which has fundamentally altered protein purchasing patterns in favor of budreceive friconcludely alternatives is propelling the growth of Europe tilapia market. As inflation rates across the Eurozone surged to historic highs, with food inflation exceeding 10% in several member states according to the study, consumers have been forced to reevaluate their spconcludeing on premium seafood items. Traditional whitefish species, such as Atlantic cod and European hake have seen their retail prices increase dramatically due to dwindling wild stocks and high fuel costs for fishing fleets by creating a significant price gap that tilapia effectively fills. Tilapia delivers high biological value protein, providing roughly 26 grams per 100 gram serving, which rivals more expensive meats and fish at a fraction of the cost. Supermarket chains in price sensitive markets like Poland, Italy, and Spain have responded by expanding their private label tilapia ranges, recognizing the species as a key traffic driver for budreceive conscious shoppers. This demand for tilapia remains resilient even when overall consumer confidence wavers, cementing its role as a counter cyclical commodity within the European food binquireet. The sustained affordability of tilapia allows it to penetrate deeper into the mass market, securing its position as a primary protein source for millions of Europeans navigating a challenging economic landscape.

Culinary Adaptability and Integration into Diverse Diets

The exceptional culinary versatility of the species, which allows it to seamlessly integrate into the diverse gastronomic traditions found across the continent, which is also accelerating the growth of Europe tilapia market. Unlike fish with strong oceanic flavors that may clash with certain spices or sauces, tilapia possesses a mild, neutral taste and a firm texture that creates it an ideal canvas for a wide array of flavor profiles ranging from Mediterranean herbs to Asian stir fry sauces. Food service operators and industrial manufacturers are increasingly utilizing tilapia, as a primary ingredient in value added products such as breaded goujons, marinated fillets, and pre seasoned meal kits, thereby expanding its appeal beyond the raw frozen products. As per the data from the European Association of Fish Producers Organizations, innovation in convenience seafood is a growth vector, with tilapia based innovations accounting for a significant portion of new product launches in the frozen aisle. The boneless nature of tilapia fillets further enhances its utility in institutional feeding programs, including school canteens and corporate cafeterias in countries like France and Spain, where ease of preparation and safety are paramount. This culinary flexibility enables the species to transcconclude cultural barriers, appealing to both traditional European palates and the growing demographic of consumers seeking international cuisine experiences.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Sustainability Mandates

The increasing rigorous regulatory environment imposed by the European Union, which demands strict adherence to environmental sustainability and food safety standards, which is limiting the growth of Europe tilapia market. The EU Import Control System mandates comprehensive documentation and traceability for all aquaculture products, creating substantial administrative and financial burdens for exporters, particularly tiny-scale farmers in developing nations. According to the European Commission, potential tilapia shipments face delays or outright rejection due to non-compliance with updated residue monitoring plans or insufficient certification documentation. As per the International Trade Centre, the technical capacity required to implement advanced traceability systems is often lacking among tinyer suppliers in Latin America and Asia by leading to a consolidation of supply sources and limiting market diversity. These regulatory hurdles, while designed to protect consumer health and marine ecosystems, inadvertently create supply bottlenecks that restrict the volume of compliant fish. The stringent nature of these rules also discourages new entrants from establishing supply lines, building the market vulnerable to disruptions from existing certified suppliers. Furthermore, the constant evolution of these regulations requires continuous adaptation from importers, increasing operational complexity and costs.

Persistent Negative Consumer Perceptions Regarding Aquaculture

The persistent negative perception regarding the quality and safety of farmed fish, specifically concerning antibiotic utilize and environmental impact, which is additionally restricting the growth of Europe tilapia market. Despite advancements in aquaculture technology, a lingering stigma associates farmed tilapia with poor water quality, unnatural feeding practices, and inferior nutritional value compared to wild caught alternatives. According to a survey conducted by the European Consumer Organisation, many respondents expressed significant concerns about the utilize of chemicals and antibiotics in fish farming, which directly correlates with a hesitation to purchase tilapia products regularly. Misinformation regarding the diet of tilapia, often erroneously believed to consist of waste materials, continues to circulate despite modern farms utilizing high quality vereceiveable-based feeds that ensure product safety. Media coverage of isolated contamination incidents in global supply chains has amplified these fears, leading to a trust deficit that is difficult to overcome. This perceptual barrier forces retailers and brands to invest heavily in educational marketing campaigns to reassure purchaseers about modern farming standards, increasing the cost of customer acquisition. The stigma effectively confines tilapia to the lower price tier of the market, preventing it from competing in premium segments where margins are higher.

MARKET OPPORTUNITIES

Adoption of Recirculating Aquaculture Systems for Local Production

The rapid advancement and adoption of Recirculating Aquaculture Systems, which offer the potential to establish viable local production facilities within the continent is solely setting up new opportunities for the growth of Europe tilapia market. These closed loop technologies allow for the intensive farming of warm water species like tilapia in controlled indoor environments, indepconcludeent of external climate conditions and with minimal water exmodify. According to the European Maritime and Fisheries Fund, investment in land-based aquaculture technologies has surged by 25% over the last five years, reflecting strong governmental and institutional support for sustainable domestic production. Facilities already operational in countries like Denmark and the Netherlands have demonstrated that RAS technology can achieve yields of up to 100 kilograms of fish per cubic meter of water, displaycasing remarkable efficiency. This shift aligns perfectly with the European Green Deal objectives, promoting food sovereignty and reducing reliance on third countest imports. The ability to strictly control water quality, feed inputs, and disease management in RAS facilities ensures a product free from antibiotics and contaminants, which is directly addressing consumer safety concerns. As energy costs for these systems decrease and technology becomes more scalable, the economic case for European tilapia farming strengthens, offering a pathway to capture a significant share of the fresh fish market and insulate the region from global supply shocks.

Expansion of Value Added and Convenience Product Segments

The strategic expansion into value added and convenience product lines that cater to the evolving lifestyle requireds of modern consumers is additionally to elevate the growth of Europe tilapia market. As urbanization increases and time for meal preparation decreases, there is a burgeoning demand for pre marinated, breaded, and ready to cook seafood solutions that offer restaurant quality meals with minimal effort. Manufacturers can leverage this trconclude by developing tilapia-based products infutilized with regional and exotic flavors, such as lemon herb, spicy Cajun, or teriyaki glazes, thereby elevating the perceived value of the species. These innovations allow tilapia to compete in higher price brackets and attract demographics that previously viewed it solely as a budreceive commodity. Retailers are increasingly dedicating prime shelf space to these convenient options, recognizing their ability to drive binquireet size and purchase frequency. As per research, product launches featuring clean label ingredients and explicit sustainability claims see a 15% higher success rate, providing a clear roadmap for product development. By transforming tilapia from a raw ingredient into a gourmet convenience item, where the industest can overcome price sensitivity and build stronger brand loyalty. This approach also facilitates deeper penetration into the food service sector, where consistency, portion control, and ease of preparation are critical operational requirements. The expansion into value added segments effectively diversifies revenue streams, reduces exposure to raw commodity price fluctuations, and opens new avenues for market growth.

MARKET CHALLENGES

Volatility in Global Logistics and Supply Chain Stability

The form of extreme volatility within global logistics networks and the escalating costs of international freight, given its heavy reliance on imports from distant continents is one of the challenges for the growth of Europe tilapia market. Since, the vast majority of tilapia consumed in Europe is shipped from Latin America and Asia, any disruption in maritime routes, port operations, or container availability has an immediate and severe impact on supply availability and retail pricing. Port congestion in major European hubs, such as Rotterdam and Hamburg frequently leads to unplanned delays that compromise the shelf life of perishable seafood products, resulting in increased waste and financial loss. As per the World Bank Logistics Performance Index, inconsistencies in customs clearance times add an average of 4 days to the total transit duration, heightening the risk of quality degradation before the product reaches the consumer. These logistical bottlenecks force distributors to maintain larger inventory buffers, tying up working capital and increasing storage costs. Furthermore, the depconcludeence on long haul transportation exposes the market to fluctuations in bunker fuel prices, which are inevitably passed on to the final consumer, potentially dampening demand. Geopolitical tensions and shifting trade policies can also abruptly alter tariff structures, rconcludeering previously viable supply routes economically unfeasible.

Intense Competition from Established Whitefish Alternatives

The intense competition from established whitefish species that possess deep rooted cultural acceptance, across the continent is also to limit the growth of Europe tilapia market. Species such as Alinquirea pollock, European hake, and pangasius occupy similar niches and often benefit from preferential treatment in retail promotions, food service contracts, and industrial processing applications. Alinquirea pollock is widely utilized in processed foods and rapid food chains throughout Europe, enjoys a dominant position due to its long-standing presence, established supply networks, and neutral flavor profile that is familiar to consumers. As per the Seafood Industest Ininformigence Network, strong consumer loyalty to these traditional species creates it exceptionally difficult for tilapia to gain significant market share without resorting to aggressive and often unsustainable pricing strategies. Retail purchaseers frequently prioritize these alternatives due to their predictable supply volumes and familiar taste profiles that require minimal consumer education or marketing spconclude. The high degree of substitutability means that any minor price increase or perceived quality issue with tilapia prompts an immediate switch by both conclude consumers and food manufacturers to competing species. Additionally, well-funded marketing campaigns by industest bodies representing traditional European fish stocks further reinforce the status quo by building it challenging for tilapia to break through.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.75% |

|

Segments Covered |

By Species, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Regal Springs, High Liner Foods Inc., Thai Union Group PLC, Surapon Foods Public Company Limited, Charoen Pokphand Foods, Mowi ASA, Kühne and Heitz, SeaOptima, Tilapez, and Nomad Foods Ltd |

SEGMENTAL ANALYSIS

By Species Insights

The nile tilapia segment was the largest by holding a significant share of the Europe tilapia market in 2025 owing to the species’ superior biological characteristics and its alignment with European import requirements. According to the Food and Agriculture Organization of the United Nations, Nile Tilapia can reach a marketable size of 500 grams in just 6 to 8 months under optimal conditions, which is significantly rapider than the 9 to 12 months required for Blue or Mozambique Tilapia. This rapid turnover allows exporters to meet the high volume demands of European retailers more effectively while keeping production costs low. Furthermore, the fillet yield of Nile Tilapia is consistently higher, often exceeding 35% of the live weight by providing better value for European importers who pay for processed fillets. As per the Global Aquaculture Alliance, over 90% of global tilapia production consists of Nile Tilapia genetics, ensuring a stable and massive supply chain dedicated to this specific variety. European food processors prefer this species due to its uniform fillet size and mild flavor profile, which suits a wide range of culinary applications from frozen dinners to fresh counters. The standardization of Nile Tilapia in global trade has built it the default choice for European purchaseers, marginalizing other species that lack similar scale and consistency in supply.

The blue tilapia segment is swiftly emerging at a rapidest CGAR of 6.8% from 2026 to 2034 owing to the species’ superior tolerance to cooler water temperatures, which aligns increasingly with the rise of land-based aquaculture projects within Northern Europe. Unlike the Nile Tilapia which thrives in tropical warmth, Blue Tilapia can survive and grow in water temperatures as low as 14 degrees Celsius by building it the ideal candidate for Recirculating Aquaculture Systems in countries like Denmark and the Netherlands. According to the Federation of European Aquaculture Producers, the number of land-based farming facilities utilizing cold tolerant strains has increased in the last three years, directly boosting the availability of Blue Tilapia. As per research published by the European Maritime and Fisheries Fund, investments in breeding programs focutilized on cold tolerance have yielded strains that maintain robust growth rates even in suboptimal thermal conditions. The push for locally sourced seafood to reduce carbon footprints favors Blue Tilapia, as it allows for year-round production without excessive energy consumption. Retailers are launchning to label these locally farmed variants as premium sustainable options, attracting environmentally conscious consumers willing to pay a higher price point.

By Application Insights

The retail segment was the largest by holding 55.4% of the Europe tilapia market share in 2025 owing to the widespread availability of frozen tilapia fillets in supermarket chains and the increasing consumer preference for home cooked meals that offer high protein value at affordable prices. A major driving factor is the aggressive expansion of private label ranges by major European grocery retailers who utilize tilapia as a key value product to attract budreceive conscious shoppers. Supermarkets in Germany, the United Kingdom, and France have dedicated substantial shelf space to frozen tilapia, often pricing it 25% lower than cod or hake, which drives high turnover rates. As per the study, frozen seafood sales in the retail channel grew annually, with tilapia being a top contributor due to its long shelf life and ease of preparation. The convenience factor also plays a crucial role, as modern retail packaging offers skinless and boneless fillets that require minimal preparation time, appealing to busy working families. Retailers leverage tilapia in promotional campaigns focutilized on healthy eating, highlighting its low-fat content to health aware demographics. The sheer scale of retail distribution networks ensures that tilapia reaches every corner of the continent, from hypermarkets in urban centers to discount stores in rural areas, solidifying its position as the primary channel for tilapia consumption.

The food service segment is anticipated to grow at a CAGR of 7.5% during the coming years owing to the recovering hospitality industest and the strategic adoption of tilapia by restaurant chains and institutional caterers seeking cost effective yet versatile menu options. Following the post pandemic rebound, the number of food service outlets across Europe has increased significantly, with many operators integrating tilapia into their menus to manage rising food costs without compromising portion sizes. Fast food chains and casual dining restaurants are increasingly replacing traditional whitefish with tilapia in dishes such as fish tacos, burgers, and grilled platters due to its mild taste and consistent texture. As per data from the Seafood Industest Ininformigence Network, contract caterers supplying schools, hospitals, and corporate canteens have increased their tilapia procurement to meet nutritional guidelines, while adhering to strict budreceive constraints. The versatility of tilapia allows chefs to experiment with diverse cuisines, from Mediterranean to Asian fusion, broadening its appeal to diners seeking variety. Furthermore, the standardization of portion-controlled fillets simplifies kitchen operations and reduces waste, building it highly attractive for high volume food service providers.

REGIONAL ANALYSIS

Germany Tilapia Market Analysis

Germany was the top performer in the Europe tilapia market of 22.3% share in 2025 due to its massive population and strong culture of frozen food consumption. The high reliance on discount supermarket chains that prioritize value oriented protein sources for their extensive private label portfolios. The German consumer’s pragmatic approach to food shopping, where price per kilogram is a decisive metric, favoring tilapia over more expensive domestic fish, which is leveraging the growth of Europe tilapia market. The robust logistics infrastructure in Germany facilitates efficient distribution from entest ports to inland retail centers, ensuring consistent availability. As per the German Frozen Food Institute, the per capita consumption of frozen fish products has remained stable at 5.5 kilograms annually, with tilapia contributing significantly to this volume. Environmental awareness is also shaping the market, with German retailers increasingly demanding ASC certified tilapia, pushing suppliers to adhere to strict sustainability standards. The presence of major food processing companies in the countest further boosts demand for raw tilapia inputs for value added ready meals.

United Kingdom Tilapia Market Analysis

The United Kingdom tilapia market was accounted in holding 18.3% of share in 2025 with a diverse multicultural population and a well-established food service sector. The popularity of ethnic cuisines, particularly Caribbean and Asian dishes, where tilapia is a traditional and preferred ingredient by creating a steady baseline demand beyond just price considerations. The rise of meal kit delivery services in the UK has also contributed to growth, as these platforms frequently feature tilapia recipes due to its ease of cooking and mild flavor. As per the British Retail Consortium, seafood remains a top category for weekly grocery shopping, with frozen tilapia often featured in promotional bundles aimed at families. The trade environment has led importers to diversify sourcing strategies, but the demand remains resilient due to the lack of viable local substitutes at similar price points. Additionally, health campaigns promoting low fat protein sources have resonated with UK consumers, further boosting tilapia consumption in both retail and hospitality channels.

France Tilapia Market Analysis

France tilapia market is esteemed to grow steadily in coming years with a sophisticated culinary scene that is increasingly embracing sustainable and affordable seafood options. France is evolving from a traditional preference for fresh wild fish to a greater acceptance of high quality frozen farmed species due to economic pressures and supply constraints of wild stocks. French retailers are also innovating with value added tilapia products, such as marinated fillets and breaded portions, to appeal to consumers seeking gourmet experiences at home. As per the National Interprofessional Committee for Seafood, the average French houtilizehold now purchases frozen fish products 15 times a year, with tilapia gaining traction as a versatile ingredient for family dinners. The strong emphasis on food safety and traceability in France means that certified tilapia performs exceptionally well, building trust among discerning consumers. This shift towards practical yet quality conscious consumption patterns ensures France remains a critical pillar of the European tilapia market.

Spain Tilapia Market Analysis

Spain tilapia market growth is likely to grow with its status as a seafood loving nation with a vast food service industest. The high frequency of fish consumption, where tilapia serves as an accessible alternative to increasingly scarce and expensive traditional species like hake and sole is greatly influencing the growth of tilapia market in Spain. A major driving factor is the tourism industest, which creates immense demand for affordable seafood in hotels and resorts along the Mediterranean and Atlantic coasts, where tilapia is widely utilized in buffets and à la carte menus. The hypermarkets offering large format packs of frozen tilapia that appeal to large families and cost conscious shoppers. The culinary flexibility of tilapia allows it to be incorporated into traditional Spanish stews and rice dishes, facilitating its acceptance among local consumers who might otherwise prefer native species.

Italy Tilapia Market Analysis

Italy tilapia market growth is likely to grow with an inclination towards convenient protein sources amidst altering lifestyle patterns. The Italy reflects a gradual shift from strictly fresh seafood purchases to a hybrid model where frozen tilapia fills the gap for quick weeknight meals and industrial food production. The booming ready meal sector in Italy, where food manufacturers utilize tilapia as a primary ingredient for frozen pasta sauces with fish and pre-cooked entrees that cater to the busy urban workforce. The economic disparity between Northern and Southern Italy also influences consumption, with tilapia finding strong footholds in the South where price sensitivity is higher and traditional fish prices have become prohibitive. As per the Italian Association of Fish Industries, the utilize of tilapia in processed seafood products has doubled in the last four years, indicating a structural modify in how the species is consumed. Furthermore, the rise of international food trconcludes in Italian cities has introduced tilapia to younger demographics through fusion cuisine offerings in restaurants.

COMPETITIVE LANDSCAPE

The competition in the Europe tilapia market is characterized by a high degree of rivalry among international processors and distributors who vie for shelf space in major retail chains. The market landscape features a mix of global seafood conglomerates and specialized regional importers who compete primarily on price consistency and sustainability credentials. Since the product is largely perceived as a commodity by many consumers differentiation often hinges on certification status and brand reputation for quality. Intense pressure from alternative whitefish species like pangasius and pollock further complicates the competitive environment forcing players to constantly innovate. Companies are engaging in aggressive marketing campaigns to highlight the nutritional benefits and ethical sourcing of their tilapia to sway consumer preference. Supply chain resilience has emerged as a key battleground with firms striving to minimize disruptions from global logistics challenges. The entest of local recirculating aquaculture systems adds a new dimension to competition by offering fresh locally produced alternatives that challenge the dominance of imported frozen products. This dynamic environment requires continuous adaptation and strategic investment to maintain market relevance.

KEY MARKET PLAYERS

Some of the notable key players in the Europe tilapia market are

- Regal Springs

- High Liner Foods Inc.

- Thai Union Group PLC

- Surapon Foods Public Company Limited

- Charoen Pokphand Foods

- Mowi ASA

- Kühne + Heitz

- SeaOptima

- Tilapez

- Nomad Foods Ltd

Top Players in the Market

- High Liner Foods stands as a preeminent processor and distributor of frozen seafood with a substantial footprint across the European continent. The company leverages its extensive global supply chain to source high quality tilapia from certified farms in Latin America and Asia for distribution throughout Europe. Their contribution to the global market involves setting rigorous standards for sustainability and traceability which influence sourcing practices worldwide. Recently the company has focutilized on expanding its value added product lines by introducing seasoned and breaded tilapia options tailored to European taste preferences. They have also invested heavily in digital traceability technologies to provide consumers with transparent information about the origin and farming methods of their fish. This strategic shift strengthens their brand reputation among environmentally conscious European shoppers and solidifies relationships with major retail partners who demand full supply chain visibility.

- Thai Union Group operates as a global seafood giant with a significant influence on the Europe tilapia market through its diverse portfolio of branded and private label products. The company utilizes its massive production capabilities in Thailand and other Asian hubs to ensure a consistent and cost-effective supply of tilapia fillets to European distributors. Their global involvement includes pioneering initiatives in sustainable aquaculture and reducing the environmental impact of fish farming operations. In recent actions to strengthen their position the group has launched new ready to cook meal kits featuring tilapia that cater to the busy lifestyles of European consumers. They have also formed strategic partnerships with European retailers to develop exclusive product ranges that emphasize health benefits and eco-friconcludely packaging. These efforts demonstrate their commitment to innovation and responsiveness to local market trconcludes while maintaining their status as a leading global supplier.

- Maruha Nichiro Corporation is a leading Japanese seafood conglomerate that plays a critical role in the Europe tilapia market through its sophisticated logistics network and processing expertise. The company sources tilapia from various global regions and processes it in facilities that meet strict European food safety regulations before distributing it to wholesale and retail channels. Their global market contribution is marked by advanced freezing technologies that preserve the texture and flavor of tilapia during long distance transportation. They have also increased their investment in certification programs to ensure all their tilapia products comply with the highest sustainability standards required by European purchaseers. These actions enhance their reliability as a supplier and assist them capture a larger share of the premium frozen seafood segment.

Top Strategies Used by Key Market Participants

Key players in the Europe tilapia market primarily employ strategies focutilized on vertical integration and sustainability certification to secure their competitive advantage. Companies are increasingly investing in direct partnerships with aquaculture farms to control the quality of raw materials and ensure a stable supply chain amidst global volatility. Obtaining recognized eco labels such as the Aquaculture Stewardship Council certification has become a standard practice to meet the stringent demands of European retailers and consumers. Another major strategy involves product innovation where manufacturers develop value added items like marinated fillets and ready meals to differentiate their offerings from commodity competitors. Expansion of cold chain infrastructure is also critical as firms upgrade logistics networks to maintain product freshness and reduce spoilage rates during transit. Furthermore, participants are leveraging digital tools for traceability to build consumer trust and transparency regarding the origin and farming practices of their tilapia products.

MARKET SEGMENTATION

This research report on the European tilapia market has been segmented and sub-segmented based on categories.

By Species

- Nile Tilapia

- Blue Tilapia

- Mozambique Tilapia

- Wami Tilapia

By Application

- Food Industest

- Pharmaceutical Industest

- Animal Feed

- Pet Food

- Food Service

- Retail

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply